Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

Chapter 09 - Short-Term Profit Planning: Cost-Volume-Profit (CVP) Analysis

9-44 CVP Analysis; Uncertainty/Sensitivity Analysis (60-75 min)

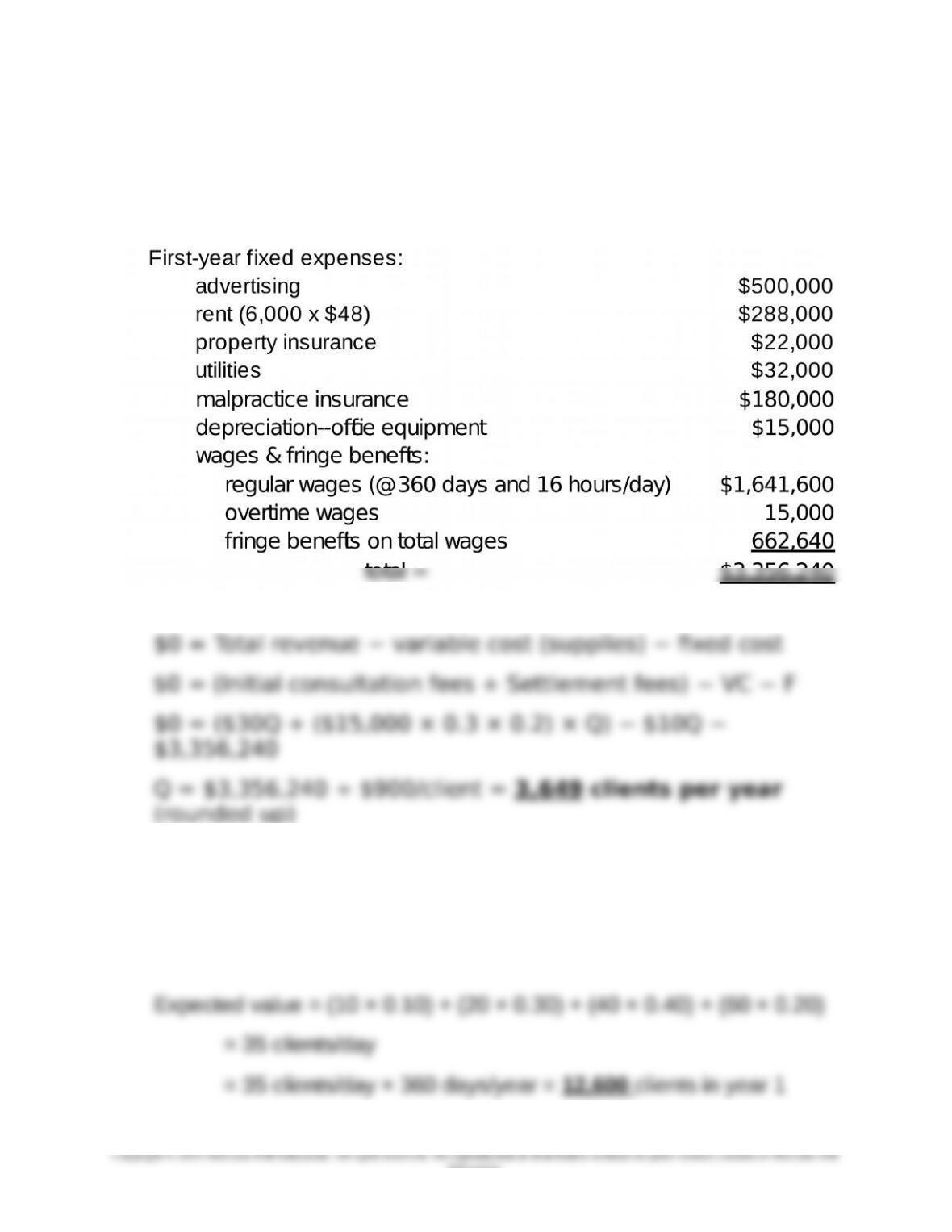

1. To break even, during the first year of operations, 3,649 clients

(rounded up) must visit the law office being considered by Don Carson

and his colleagues as calculated below.

Breakeven Calculation:

2. Based on the report of the marketing consultant, the expected

number of new clients during the first year is 12,600 as calculated

below. Therefore, it is entirely feasible for the law office to break even

during the first year of operations as the breakeven point is 3,649

clients (see above).

9-50

Education.

Chapter 09 - Short-Term Profit Planning: Cost-Volume-Profit (CVP) Analysis

9-44 (Continued-1)

Since there is uncertainty in the prediction of the number of clients

per year, based on a probability distribution, further sensitivity

analysis should be considered, with the objective of determining the

potential loss if in fact the number of clients falls short of the forecast.

3. Sensitivity Analysis: Sensitivity analysis is used to deal more

effectively with uncertainty or risk. Sensitivity analysis is a "what-if”

type of analysis used to determine the outcomes if any parameters

change from the initial assumptions. For example, revenues or costs

prevalent in decision making include the following:

As the business environment is becoming more dynamic and

competitive, sensitivity analysis provides management with an

understanding of the impact of changes in the environment.

Sensitivity analysis aids management in identifying the key

variables and assumptions, so the variables can be monitored

or a decision made to obtain additional information.

The use of probability distributions to determine expected

values is an excellent way to conduct a sensitivity analysis.

This approach allows Carson to see the distribution of costs

higher standard deviations for greater uncertainty.

9-51

Education.

Chapter 09 - Short-Term Profit Planning: Cost-Volume-Profit (CVP) Analysis

9-44 (Continued-2)

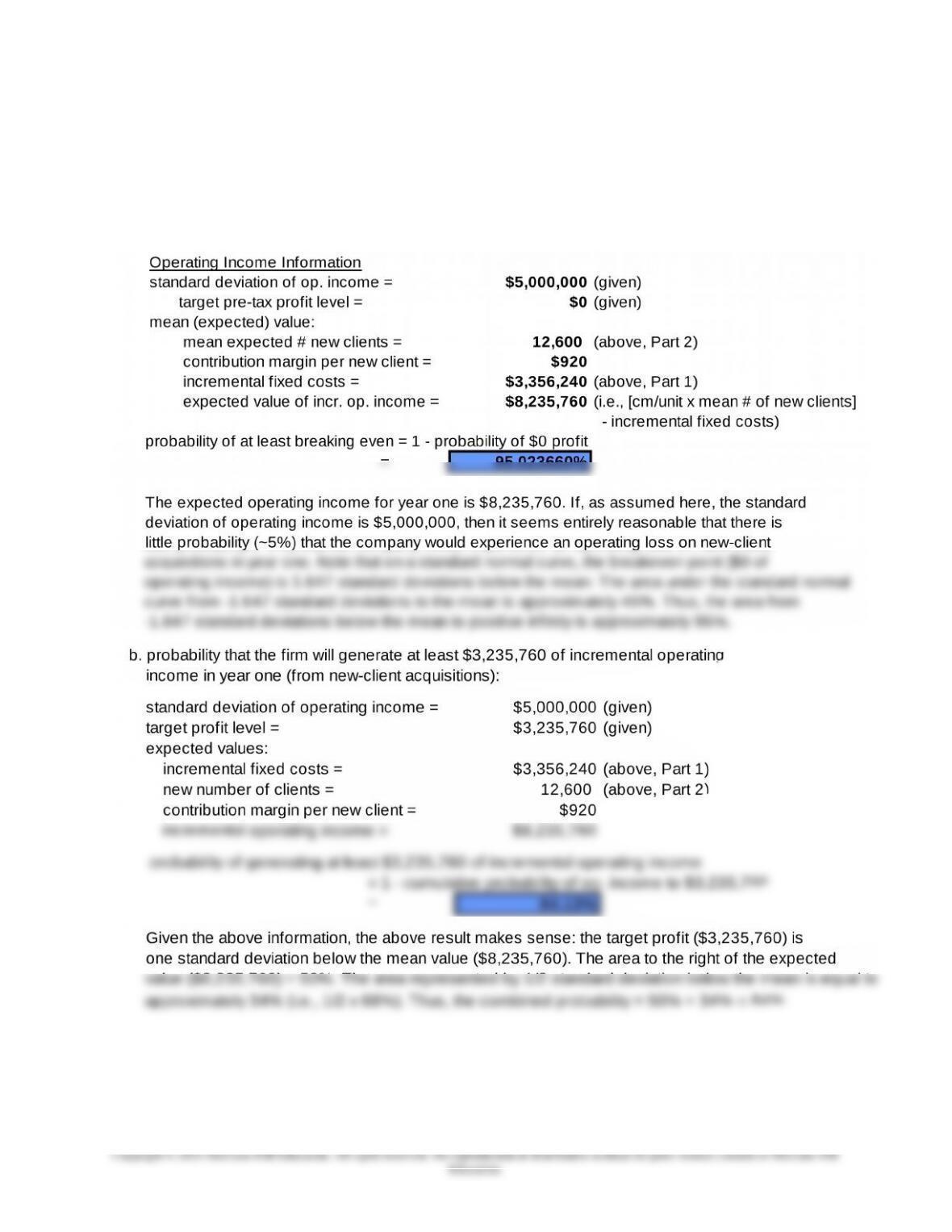

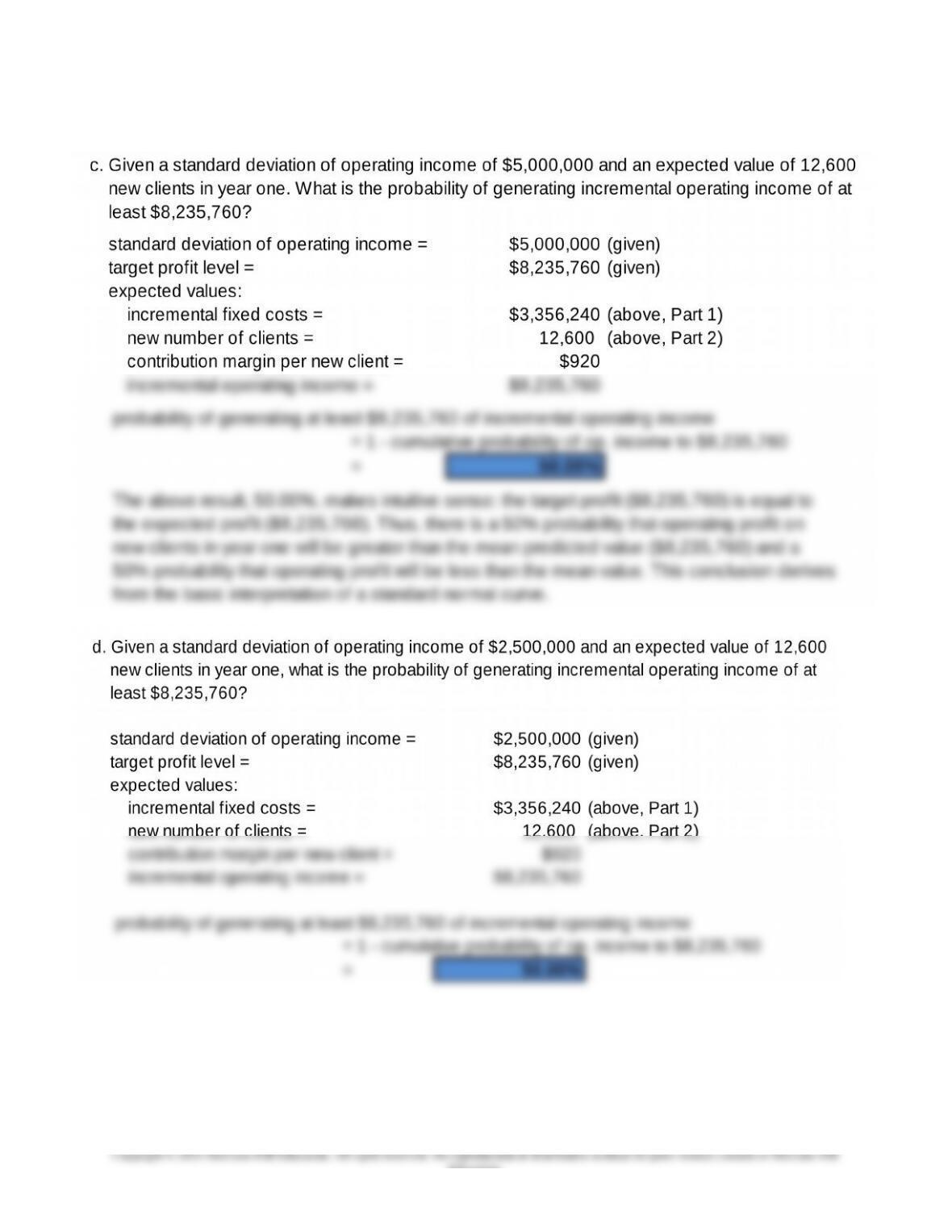

4. Basic simulation analysis using the NORMDIST function in Excel:

a. probability that the firm will at least breakeven, given normally distributed

operating income and a standard deviation of $5,000,000, is ~ 95%:

9-52

Chapter 09 - Short-Term Profit Planning: Cost-Volume-Profit (CVP) Analysis

9-44 (Continued-3)

9-53

Education.

Chapter 09 - Short-Term Profit Planning: Cost-Volume-Profit (CVP) Analysis

9-44 (Continued-4)

9-54

Education.

Chapter 09 - Short-Term Profit Planning: Cost-Volume-Profit (CVP) Analysis

9-45 CVP Analysis; Strategy; Critical Success Factors (50-60 min)

1. a. A total of 480 seminar participants would be needed for the joint

venture to break even, calculated as follows:

The break-even number of participants equals the fixed costs divided

by the contribution margin per participant

Fixed costs (F) = $318,000 from GSI + $210,000 from Eastern =

$528,000/year

b. A total of 700 seminar participants are needed for the joint venture to

earn an after-tax profit (πA) of $169,400, calculated as follows.

The target number of participants equals the fixed costs (F) plus the

Required# of participants = (F + πB) ÷ cm

= ($528,000 + $242,000)/year ÷ $1,100/participant

9-55

Education.

Chapter 09 - Short-Term Profit Planning: Cost-Volume-Profit (CVP) Analysis

9-45 (Continued-1)

2. A minimum of 1,055 participants is needed in order for GSI to prefer the

40 percent fee option rather than the flat fee, calculated as follows

(where Q = number of seminar participants):

GSI fees for flat fee option

= $9,500/seminar × 40 seminars/year = $380,000/year

GSI fees for 40% of Eastern's profit-before-tax option

Pre-tax profit (operating income) would be equal for the two options

when total revenue is equal (since fixed costs of GSI are being ignored

for the present analysis) at the following number of participants, Q.

Therefore, GSI will earn more revenue and prefer the 40 percent

option when the number of participants is 1,055 or higher.

3. Some of the strategic and implementation issues facing GSI in this

decision are the following:

Are the CVP assumptions satisfied? That is, total costs can be

divided into a fixed component and a component that is variable

with respect to volume. Total costs and total revenues have a

9-56

Education.

Chapter 09 - Short-Term Profit Planning: Cost-Volume-Profit (CVP) Analysis

9-45 (Continued-2)

Alternative uses of capacity? Since the Eastern U seminars would

occupy all GSI’s available capacity, GSI should consider whether

there might be more profitable uses for that capacity before

Has GSI considered the uncertainty in the situation? What

happens if the breakeven level of participants is not met? GSI and

Does the collaboration make sense strategically? Are Eastern and

GSI likely to enhance each other’s reputation and to provide

operating synergies and efficiencies that will make the alliance a

9-57

Education.

Chapter 09 - Short-Term Profit Planning: Cost-Volume-Profit (CVP) Analysis

9-46 CVP Analysis; Strategy; Uncertainty (60-75 min)

1. Total variable costs per unit for the current plan are $6 + $12.50 + $25

+ $10 = $53.50, and $15 + $13.75 + $30 + $10 = $68.75 under the

proposed plan. Thus, the contribution margin per unit and breakeven

point (in units) for each of the two plans are as follows:

Current Plan Proposed Plan

Contributio

$100 − $53.50 = $46.50 $100 − $68.75 = $31.25

*Fixed manufacturing overhead costs are determined from the fixed

overhead rates:

2. To determine the sales volume (in units) at which CG would be

indifferent between the current manufacturing plan and the proposed

plan, solve for the point, Q, in which total relevant cost is the same for

the two decision alternatives. (Revenue from sales is unaffected by

choice of production method. Hence, the point of operating profit

The indifference point, Q, can be found at the point of cost equality, as

follows:

9-58

Education.

Chapter 09 - Short-Term Profit Planning: Cost-Volume-Profit (CVP) Analysis

9-59

Education.