Chapter 16 – Operational Performance Measurement: Further Analysis of Productivity and Sales

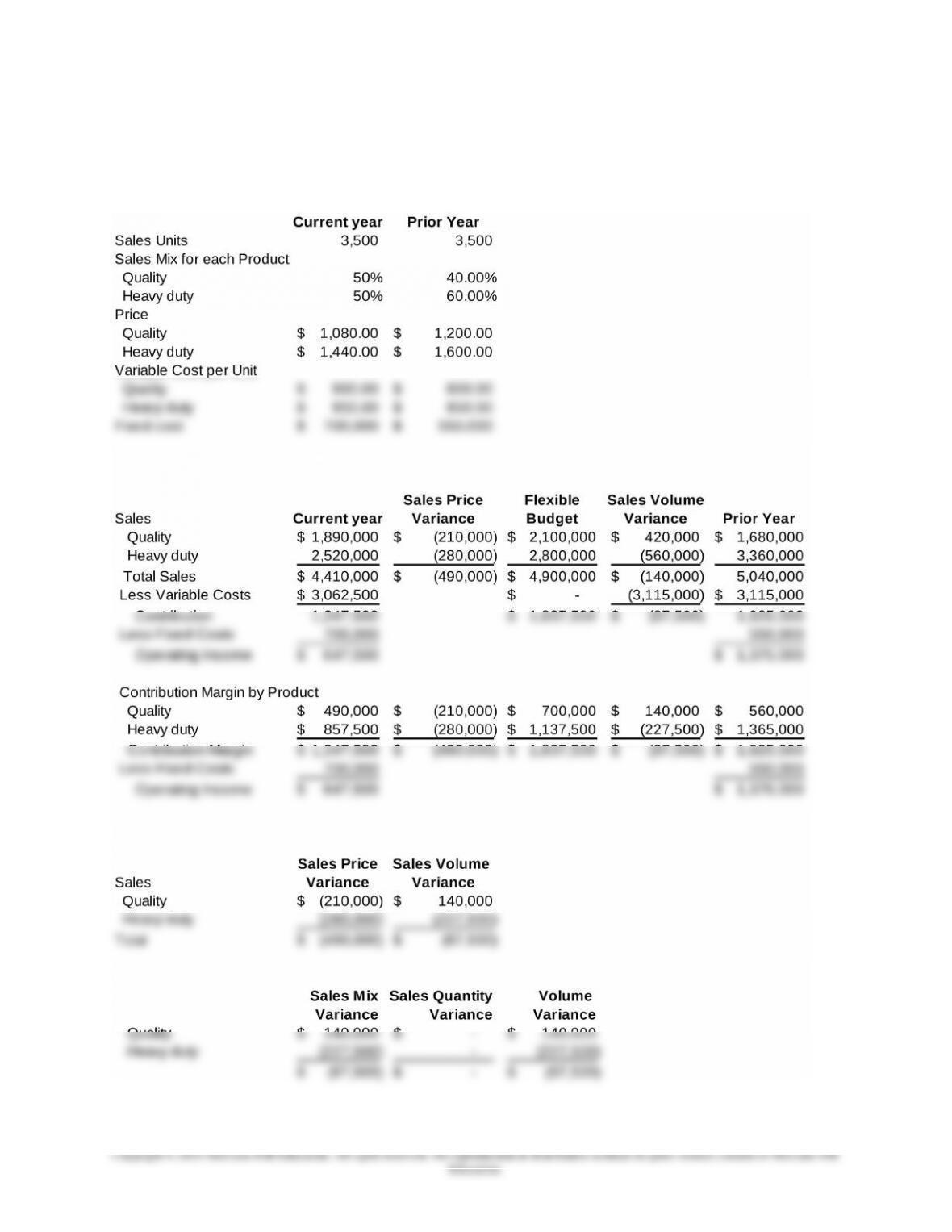

16-57 Comparative Income Statements and Sales Performance

Variances; Current to Prior Year (25 min)

1.

16-58

Chapter 16 – Operational Performance Measurement: Further Analysis of Productivity and Sales

16-57 (continued -1)

The selling price variances and volume variances based on

contribution are summarized as follows:

2. Sales mix and quantity variances

Sales Mix Variances

Quality: $140,000 (F) = (.5 – .4) x 3,500 x ($1,200 – 800)

16-59

Education.

Chapter 16 – Operational Performance Measurement: Further Analysis of Productivity and Sales

16-57 (continued -2)

3.

As expected, there were significant losses reflected in the large selling

price variances, a total unfavorable variance of $490,000. There was a

large unfavorable volume variance as well, an unfavorable variance of

$87,500, which is due entirely to the change in product mix, since there

was no change in sales quantity. Note that the volume variance is a

combination of the mix and quantity variances. There was a favorable mix

variance for the Quality product of $140,000 due to its increase from 40%

to 50% of total sales. However, there was also an unfavorable mix

16-60

Education.

Chapter 16 – Operational Performance Measurement: Further Analysis of Productivity and Sales

16-57 (continued -3)

4.

The decrease in operating income from $1,375,000 to $647,500 from the

prior to the current year is a major concern. As indicated in the problem,

the firm is starting to study ways to reduce variable costs for the coming

year. A useful way to start this planning is to use target costing and

continuous improvement, as explained in chapter 13. Target costing looks

at ways to redesign the product or manufacturing process to reduce

Another approach would be to use the productivity analyses introduced in

this chapter to determine financial and operational partial productivity

measures for the key manufacturing cost factors, and to monitor these

measures to seek improvement.

Another approach a student might suggest is to use ABC costing to better

($550,000/3,500 = $157.14 per unit).

Finally, standard costing and the flexible budget as explained in chapter 14

would be an approach to consider. Standard costing sets standard usage

and prices for the key manufacturing inputs, and determines variances from

these inputs. The six variable cost variances are usage and price for

materials, usage and rate for labor, and usage and spending variances for

variable overhead.

16-61

Education.

Chapter 16 – Operational Performance Measurement: Further Analysis of Productivity and Sales

16-58 Sales and Variable Cost Variances; Current to Prior Year; Review

of Chapter 14 (30 min)

1.

The flexible budget, the center column, is determined as follows:

Current sales at prior year prices and unit variable costs

Volume Variance

Based on sales dollars: ($176,337) = (39,200-45,500) × $27.99

Based on contribution:

= $(176,337)

16-58 (continued -1)

16-62

Education.

Chapter 16 – Operational Performance Measurement: Further Analysis of Productivity and Sales

2.

3.

The analysis above shows that RJM has succeeded in returning to

profitability, despite the falling sales and sales prices. RJM has

accomplished this through reductions in materials price and usage

and reductions in labor rate and usage. The single strongest effect

on the company was the $4.14 drop in price (from $27.99 to

16-63

Education.