Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

Chapter 7 - Cost Allocation: Departments, Joint Products, and By-Products

Chapter 7

Cost Allocation: Departments, Joint Products, and By-

Products

Teaching Notes for Cases

7-1. Revenue Allocation; Utility Industry; Strategy

This case concerns the process used in the state of Texas to subsidize companies in the heavily

regulated telecommunications industry so that the historical goal of providing universal telephone service

at reasonable rates may be achieved in the state. The subsidization of local service, particularly in high

cost rural areas, by long distance and other more profitable services, is a cornerstone of telephone

regulation. Prior to its 1984 breakup, AT&T made enough profit from the long distance market it

dominated to subsidize local service throughout the country. Since divestiture of the seven regional

telephone companies, local exchange carriers (LECs) in Texas have been subsidized by not only

interexchange carriers (IXCs) such as AT&T, MCI, and Sprint but also by the state’s largest LEC,

Southwestern Bell Telephone Company (SWBT).

The Texas Public Utilities Commission (PUC) sets telephone rates for individual LECs based on

projections of revenues needed by them to earn target rates of return. These rates are functions of

investment community requirements. In addition to settlement payments from SWBT, LECs receive

access payments from other carriers for use of their facilities in the completion of calls. They also earn

revenues from intraLATA roll calls and local telephone service.

When a telephone company predicts its revenues will be insufficient to achieve its allowable rate

of return, it may petition the PUC for a rate increase. The commission then must decide how much

additional revenue, if any, to allow the company, and from what category(s) of service. If, for example,

the PUC decides to allow an LEC to bill its customers an additional $100,000 for local telephone service,

it will adjust the company’s rate structure to provide the increase. Due to the size of SWBT (it has

approximately 80% of the telephones in Texas), its intraLATA toll rates are assigned to all local exchange

carriers in the state; consequently, a toll rate increase granted to SWBT improves the earnings and rates of

return of all 59 companies.

The PUC monitors the earnings of LECs. It may take action against those whose rates of return

exceed their allowable rates. Thus, if a company is successful in efforts to substantially reduce operating

costs it may find itself in the odd position of being called before the PUC to justify the “excess” earnings

that result.

The case questions relate to the perceived need of Southwestern Bell managers to either change

the process by which the company subsidizes the other Texas LECs or replace it with procedures which

would result in a more equitable distribution of revenues. Instead of trying to provide the correct answer

to each question, students should focus on the relative merits of alternative courses of action. Also, they

should recognize that what has been labeled “the accountant’s creed” a more complex solution is a

better solutionis not necessarily true in this situation. The FCC’s process is very complex; students may

recommend simpler procedures which they believe would be preferable.

7-1

Education.

Chapter 7 - Cost Allocation: Departments, Joint Products, and By-Products

Answers to Questions

1. For the perspective of SW Bell management accountants, the separation of non-traffic-sensitive (NTS)

costs by the frozen 1982 intrastate toll factor of 20% is the primary source of inequities in the current

pooling procedures. This factor greatly understates the current portion of SWBT’s expense and

revenues.

Some students may suggest identifying and excluding from the pooling process the revenues,

expenses, and investments associated with the non-joint provided toll calls. This change would be

welcomed by SW Bell managers because it would reduce the subsidies paid to the other carriers.

However, many of those managers believe the entire separations process is a “dinosaur” from the pre-

divestiture era that should not be refined but replaced by other arrangements for subsidizing LECs. Others

2. SW Bell officials could go to the PUC and ask for additional supervision and regulation to correct the

perceived inequities in the current system. They could point out that although the costs of telephone

technology have been declining steadily in recent years, the poolable expenses of the other LECs have

been increasing. SWBT representatives could argue that the relatively high costs of those companies may

be explained to some extent by the toll revenue sharing arrangement, which gives them little incentive to

improve operating efficiency. As implied above, unnecessarily high costs could be used by the LECs to

justify unnecessary rate increases, which are contrary to the public’s interest. One of SW Bell’s strategies

is to work for less, and more flexible regulation of the telephone industry in Texas. SWBT managers want

the PUC to adjust to the dynamic nature of the industry in the 1990s, including its rapidly changing

7-2

Education.

Chapter 7 - Cost Allocation: Departments, Joint Products, and By-Products

3. The students’ answers to this question could vary as their attitudes toward governmental versus free

market solutions, big versus small companies, gradual versus rapid change, and the rights of a company’s

shareholders versus the rights of the customers. The focus of the case and wording of the questions

probably will lead many students to recommend some change that would reduce the subsidies SWBT

pays to the other LECs but stop short of immediately discontinuing them. Students should expect the

actual solution to be a compromise that is not entirely satisfactory to any of the affected parties.

SW Bell and several of the other large LECs recently informed the TECA and the PUC that they were

withdrawing from the pool. SWBT then reached separate agreements with the larger and smaller

companies. Its negotiators agreed to pay fixed monthly support payments over a four-year period to the

other LECs which left the pool. After that time, the companies will pay each other access charges for

SWBT will provide them, again for four years.

These agreements address most of SWBT’s concerns expressed in the case. By removing itself

from the pooling process, the company eliminated the two concerns over what amounts are pooled and

how expense and investment amounts recoverable through the process are calculated. Also, analyses of

PUC data indicate that the reduced subsidies to be paid under the new arrangement are sufficient to

maintain universal service in the state. Finally, the large companies now have additional incentives to

7-3

Education.

Chapter 7 - Cost Allocation: Departments, Joint Products, and By-Products

7-2. Brookwood Medical Center

The Brookwood Medical Center (BMC) case focuses on the new TSI accounting system. Concepts such

as direct and indirect costs and simultaneous algebraic allocations are addressed in a strategic context.

Look at the quote from Carolyn Johnson at the beginning of the case. She states that upon losing

the bid for open hear surgeries, she did not know whether to be disappointed or relieved.

Ask the students to explain the basis for her reaction. Link the discussion to the Introduction case, CCR,

cost averaging. Managers at Brookwood did not have a clue about the cost of procedures. Ask the

students to think about the implications of long-term contracts. What if Brookwood acquires a contract at

a price below cost because the cost system is inadequate to help them accurately determine procedure

costs?

Answers to Questions

1. Costs were evaluated in aggregate. Also, the system focused on “charges” (a meaningless concept for

2. Consider the impact of variation in practice patterns across individual physicians. The managers at

Brookwood also were concerned with the cost of appropriate care. For example, some physicians ordered

an entire blood profile on each patient upon entering the hospital. Other physicians ordered only specific

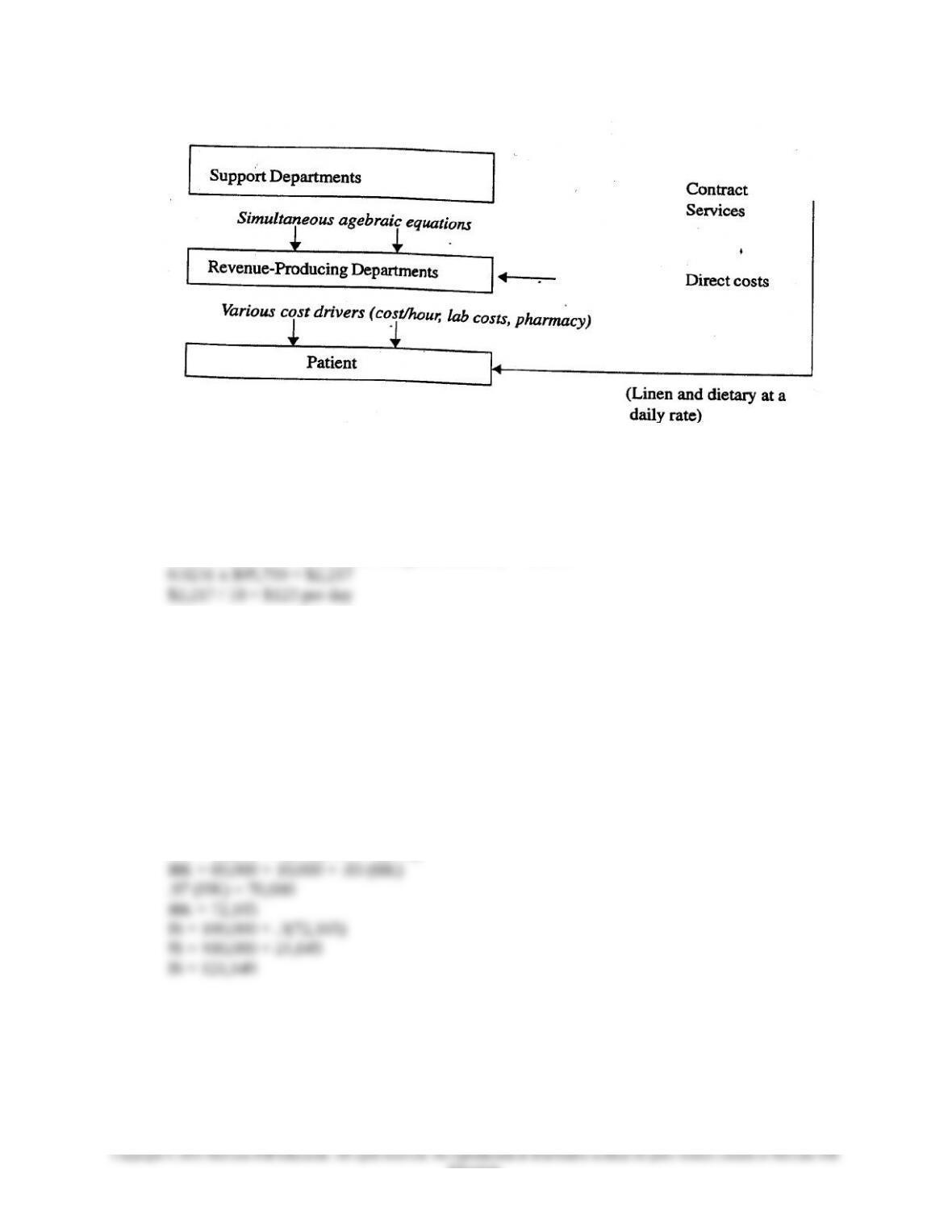

3. Draw a chart of the TSI system and point out the key principles as in the schematic below. The major

point is to stress that the indirect costs are allocated to revenue-producing departments using simultaneous

algebraic equations. In the second stage, both indirect and direct costs are applied to the patient using a

7-4

Chapter 7 - Cost Allocation: Departments, Joint Products, and By-Products

4. Consider how the daily rate (case Table 2) is determined for the Nursing Med/Surg department acuity

level 1 (based on information in case Table 3).

18 days x 346 minutes per day = 6,228 minutes

6,228 minutes / 269,045 (total budgeted minutes) = 0.0231

Acuity level 2 ($140) is calculated in an identical manner.

Why do we adjust for minutes of care? This captures the level of care required by different acuity levels.

Discuss intensive care with around the clock attention versus a step-down level of care with periodic

nursing visits. Consider the different rates at which resources are consumed.

5. At this point, you can begin the analysis by discussing the logic of the simultaneous algebraic equation

method. Case Table 4 illustrates an example of an iteration from the accounting system. Also, you can

work a simple manual example as follows:

HK = 60,000 + .10 (IS)

IS = 100,000 + .3 (HK)

HK = 60,000+.10(100,000 + .3(HK))

7-5

Education.

Chapter 7 - Cost Allocation: Departments, Joint Products, and By-Products

Solve the allocation using the allocation percentages as follows:

IS HK OR ER

100,000 60,000 -0- -0-

(121,649) 12,165 60,824 46,660

21,649 (72,165) 28,866 21,650

-0- -0- 89,690 70,310

Case Table 5 is a printout from Brookwood's TSI system. Notice that both revenue-producing and service

departments are included in the list. Education costs are allocated to the emergency room as follows: ER

Iterations such as this would continue until all service department costs were allocated to revenue-

producing departments.

6. This question permits a discussion of the key elements found in ABC systems according to Cooper's

hierarchy (unit level, batch level, product sustaining, and facility sustaining). Interestingly, we observed

few batch-level activities in the health care environment. Most costs were unit level or facility sustaining.

As a result, the cost system developed by Brookwood probably is not an ABC system. This question also

permits a discussion of the differences between service and manufacturing organizations. For example,

how do you separate the customer from the product in a health care environment?

7-6

Education.