Chapter 04 – Job Costing

4-31 Cost Flows; Applying Overhead (20 min)

1. Predetermined Overhead Rate = $1,980,000 ÷ 66,000 machine hours

2. Journal Entries:

a. Materials Inventory 900,000

Accounts Payable 900,000

180,000 lbs x $5 = $900,000

b. Work-in-Process Inventory 525,000

c. Work-in-Process Inventory 240,000

Factory Overhead 40,000

Accrued Payroll 280,000

d. Factory Overhead 75,700

Accumulated Depreciation 75,700

e. Factory Overhead 3,500

Prepaid Insurance 3,500

f. Factory Overhead 8,500

Cash 8,500

4-11

Chapter 04 – Job Costing

4-31 (continued -1)

i. Work-in-Process Inventory 231,000

Factory Overhead 231,000

$30 per machine hour x 7,700 machine hours = $231,000

3. Actual factory overhead:

4-32 Application of Overhead (20 min)

1. Calculation for Job G15: $6,000 ÷ $10,000 = 0.6 per direct labor dollar

= overhead rate

2. Applied Overhead for Job B10: $34,000 x 0.6= $20,400

Total applied overhead:

B10 $20,400

C44 20,750

G15 6,000

$47,150

4-12

Education.

Chapter 04 – Job Costing

4-33 Application of Overhead (30 min)

1. Total cost of Job A:

Sept. Direct materials requisitioned $65,000

Sept. Direct labor cost: 4,200 hours x $8.50/hour 35,700

Sept. Applied overhead: 4,200 hours x $6.50/hour* 27,300

Sept. 1 Work-in-process 31,200

Total cost of Job A $ 159,200

*predetermined OH rate = $617,500 ÷ 95,000 direct labor hours

= $6.50

2. Total overhead cost applied during September:

Applied Overhead = total direct labor-hours x overhead rate

= (4,200 + 3,500) x $6.50 per hour = $50,050

3. Overapplied overhead for September:

Actual Overhead = $13,500 + $6,000 + $7,000 + $7,500 + $12,000

4-13

Education.

Chapter 04 – Job Costing

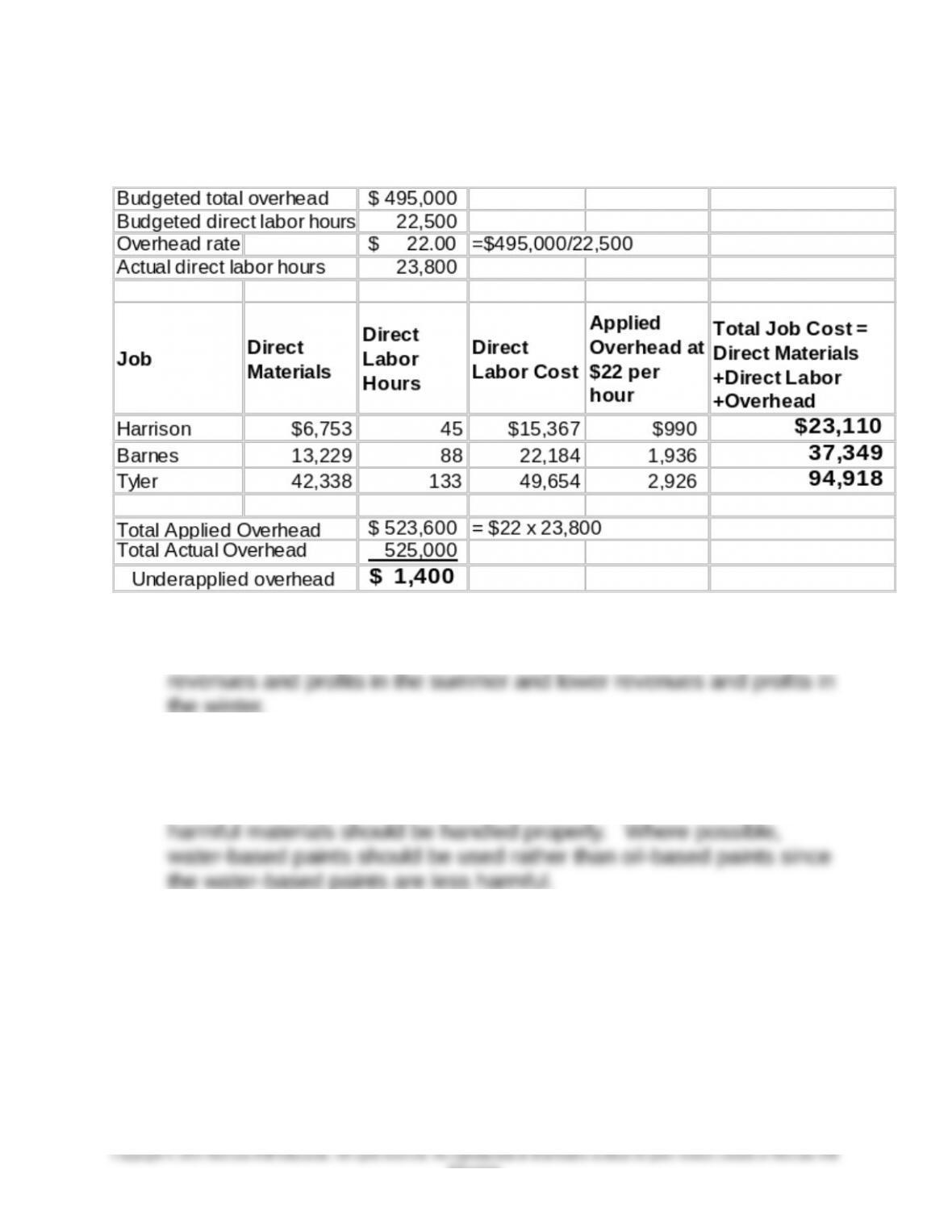

4-34 Application of Overhead (20 min)

1., 2.

3. The seasonality should not affect Whitley’s job costs because Whitley

is using an annual overhead rate; the $22 rate would be used for

each job throughout the year The effect would be for higher

the winter.

4. As a construction company, Whitley has a lot of waste to dispose of,

most of which will end up in the local landfill. Whitley can reduce the

environmental effects of waste disposal by careful use of materials so

as to minimize the waste that occurs in the jobs. Environmentally

4-14

Education.

Chapter 04 – Job Costing

4-34 (continued -1)

5. The possible cost drivers in this case include direct labor hours (used

by Whitley), direct labor cost, and materials cost. There is not likely

to be much difference between the rates based on direct labor hours

and dollars, but there could be a significant difference if there were a

change to materials cost as the cost driver. Materials cost might

associated with materials usage than labor usage.

4-35 Application of Overhead (20 min)

1. Predetermined Factory Overhead Rate

2. Applied Overhead = $8 x 71,500 = $572,000

Underapplied Overhead $10,250

3. Journal entry to transfer underapplied overhead to Cost of Goods Sold

4-36 Overhead Rate; Pricing (20 min)

1. Predetermined Overhead Rate = $325,000 ÷ 25,000 hours

= $13 per professional hour

2. Total Cost = $32,000 + ($50 x 1,200) + ($13 x 1,200)

= $32,000 + $60,000 + $15,600 = $107,600

Total billing for Central Texas Bank = $107,600 x 150% = $161,400

4-15

Education.

Chapter 04 – Job Costing

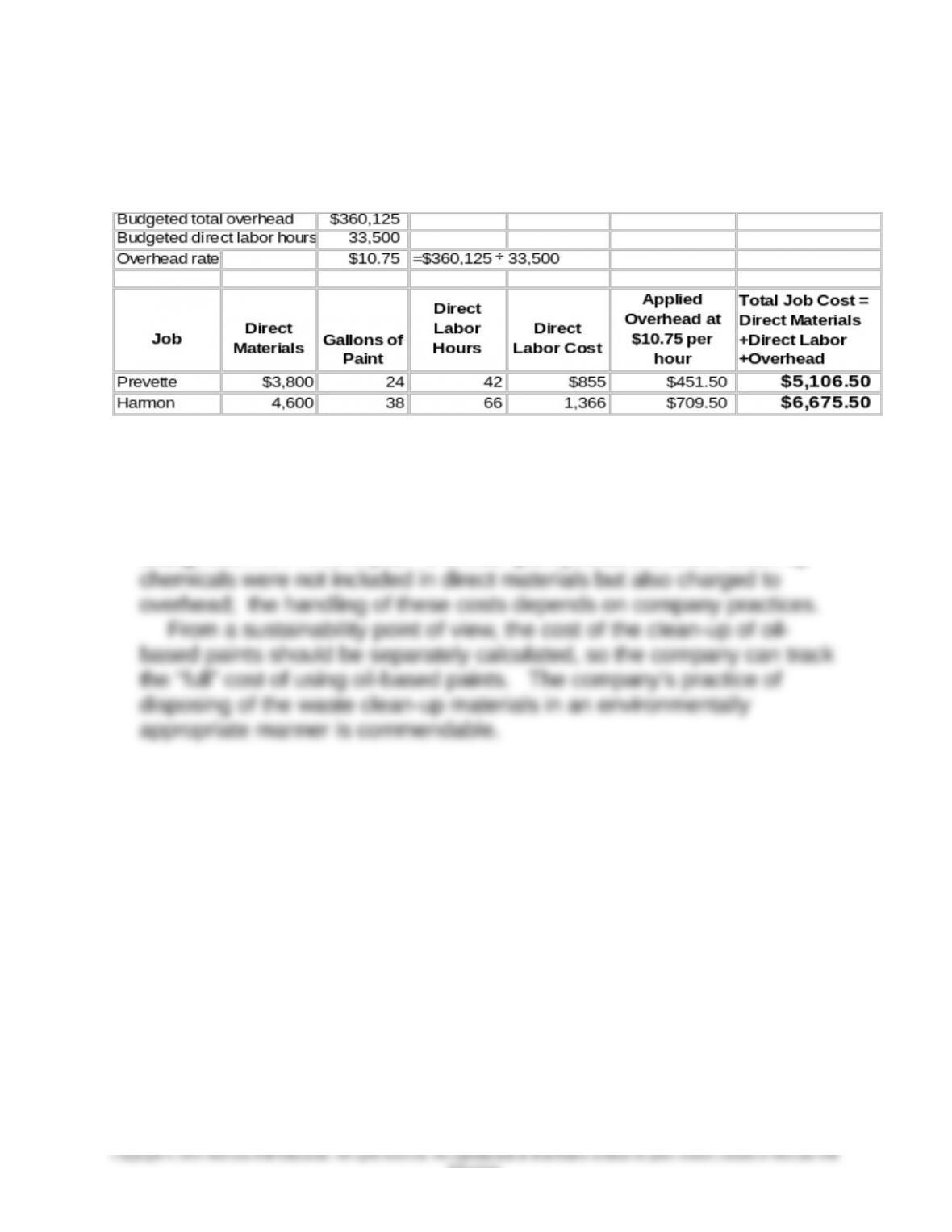

4-37 Application of Overhead (15 min)

1.

2. The oil-based paint, because it required more clean-up time and

materials (harmful chemicals), increased direct labor hours and

increased materials costs (due to the purchase of the clean-up

chemicals), both of which are included in job cost. The disposal of the

clean-up waste is likely to be included in overhead and therefore not

charged to the Prevette job; it is also quite possible that the clean-up

4-16

Education.

Chapter 04 – Job Costing

4-38 Spoilage and Scrap (20 Min)

Background Information:

Job X12 (specific normal spoilage for a particular job)

Cost of spoiled units $600

Disposal value of spoiled unit 300

Job Y34 (common normal spoilage, abnormal spoilage, and scrap)

Cost of spoiled units

Common normal spoilage $400

1. Journal entries to record spoilage costs:

a. To record the normal spoilage attributable to Job X12

Materials Inventory (disposal price of the spoiled goods) 300

Work-in-Process Inventory: Job X12 300

b. To record the normal and abnormal spoilages incurred in Job Y34

2. Journal entries to record scrap sold:

a. To record the scrap sold attributable to a specific job

Cash 80

Work-in-Process Inventory: Job Y34 80

b. To record the scrap sold common to all jobs

PROBLEMS

4-39 Overhead Rates Used for Each Machine in a Printing Plant

(Note: See also the Comments on Cost Management in Action at the end of the chapter regarding a similar costing situation)

This short case is intended as a basis for class discussion that could initiate the following topics and questions: application of job costing in the

printing industry; what are the factors driving the accuracy of product costing; how does the choice of job costing method affect pricing; what is

the effect of cost allocation methods on management behavior, performance evaluation, and how does a chosen cost method advance or hinder

the firm’s progress to its strategic goals? Some observations that I would bring out in this discussion include:

EFS uses a job costing system in which materials and direct labor are traced to the job, and overhead is traced to each machine and then applied

to the jobs based on machine usage

A strength would be that EFS has put a lot of effort into tracing the printing costs accurately and using an overhead allocation approach that

attempts to trace the costs of the machinery to the jobs that used that machinery

I would begin a discussion of the EFS approach to allocating other overhead costs – insurance, supervision, and office salaries – to the jobs based

on the capacity of the machines. That is, machines with more printing capacity (where capacity is the number of feet of forms produced per

minute of machine time) will receive a larger portion of this portion of overhead. This is very much like a volume based rate, which is OK, but

does not reflect the actual behavior of these costs. Suppose the total of other overhead is significant. Then small jobs on high capacity (fast)

4-39 (continued -1)

The strategic issue is the unknown impact of cost calculations on

competitive pricing, and therefore on the company’s competitiveness. The

success of the company depends on its ability to set a competitive price,

recognizing that the company has unused capacity (in a seasonal

business) in some periods of the year.

Source: Lisa Cross, “Benefiting from Costing and Pricing Tools,” Graphic

Arts Monthly, July 2004, pp 32-34.

4-40 Plantwide vs. Departmental Overhead Rate (30 Min)

1. Empco Inc. is currently using a plantwide overhead rate that is

applied on the basis of direct labor dollars. In general, a

plantwide factory overhead rate is acceptable only if a similar

relationship between overhead and direct labor exists in all

departments, or the company manufactures products, which

receive proportional services from each department.

In most cases, departmental overhead rates are

preferable to plantwide overhead rates because plantwide

overhead rates do not provide:

a framework for reviewing overhead costs on a

departmental basis, identifying departmental cost

4-19

Education.

Chapter 04 – Job Costing

4-40 (continued -1)

2. Because Empco uses a plantwide overhead rate applied on the

basis of direct labor dollars, the elimination of direct labor in the

Drilling Department through the introduction of robots may

appear to reduce the overhead cost of the Drilling Department

to zero. However, this change will not reduce fixed factory

3. In order to improve the allocation of overhead costs ,Empco should:

establish separate overhead accounts (pools) and rates

for the Drilling Department.

4-20

Education.