Chapter 13 – Cost Planning for the Product Life Cycle: Target Costing, Theory of Constraints, and Strategic Pricing

Let’s discuss the elements of the target costing model and how these elements are developed.

At this point in the discussion I usually write the target costing formula on the board and ask students to

consider sources of various inputs:

What are the sources of input for the projected selling price?

Students will most likely identify the following sources of information:

Stress the broad, cross-functional aspects of acquiring consumer information. To compare products, the

company had to evaluate existing competitive vehicles as well as vehicles under development.

What factors are considered when developing the required margin?

This question provides a link to finance classes. Most students have studied the concepts of weighted-

average cost of capital. I recommend spending a few minutes reviewing these concepts and linking cost of

capital to net present value (NPV) analysis. Because of the capital-intensive structure of automobile

The MB case suggests the target cost is “alive.” Is this consistent with the ideals of target costing?

I generally emphasize that Mercedes did not consider the target cost to be locked in. It was a

moving target. As engineering changes became necessary, the target cost was allowed to move. However,

before making a change, market forces were considered. For example, changes included the addition of

side airbags. In addition, the European press was critical of a simulated wood-grain part. Management

5. Explain the process of developing a component importance index. How can such an index guide

managers in making cost reduction decisions?

The index development process has five steps, as follows:

consumer importance category rankings;

I recommend making slides of Tables 1-5 to facilitate discussion. Index development is an important

element in the early conceptualization phase of the AAV. The indexes help to quantify some very abstract

concepts.

Table 1. From conversations with potential consumer groups, a list of key categories was

developed. Next, potential customers were asked to rate the importance of each category. Their responses

were computed as a percentage. Thus, safety and comfort of the AAV were viewed as significantly more

important than economy and styling.

13-8

Education.

Chapter 13 – Cost Planning for the Product Life Cycle: Target Costing, Theory of Constraints, and Strategic Pricing

Table 2 represents a rough estimate of the cost by function group and the relative percentage. The

information is used later to create a target cost index.

Table 3 is best understood by reading each category as a column. The rows explain the relative

importance of each function group to satisfying each category defined by customers. An interesting aspect

of this table is that the link between consumer preferences and engineering components is made explicit.

Table 4 builds on Table 3 by weighting the percentages computed in Table 3 by the importance

percentage calculated in Table 1. The key point is to understand which function groups contribute the

most (least) to important (less important) consumer categories.

Table 5 results in a target cost index that attempts to capture cost and benefit trade-offs. As

discussed in the case, this index may indicate a cost in excess of the perceived value of a function group.

Thus, opportunities for cost reduction (aligned with customer requirements) may be identified.

6. How does MB approach cost reduction to achieve target costs?

At this point, ask students to identify various value-engineering strategies. At Mercedes, reducing

7. How do suppliers factor into the target costing process? Why are they so critically important to the

success of the MB AAV?

From the conceptual phase through the production phase, the suppliers of systems for the AAV

truly were partners. Suppliers attended regular meetings with the cost planners throughout the entire

Why is the relationship with suppliers a crucial element in the success of the AAV?

Suppliers provide entire systems for the AAV.

The facility uses a JIT production system. In fact, many suppliers deliver directly to the assembly

line, rather than to a small warehouse.

8. What role does the accounting department play in the target costing process?

Stress the fact that accountants were watchdogs in the target costing process. Their primary

responsibility was to ensure costs did not exceed targets during the production phase. Thus, the

accountants’ role was as follows:

cost control;

What are some of the organizational barriers that may challenge managers attempting to introduce TC

systems?

Try to get students to identify various impediments to target costing systems in the United States.

Examples may include:

Teaching Strategies for Readings

13-9

Education.

Chapter 13 – Cost Planning for the Product Life Cycle: Target Costing, Theory of Constraints, and Strategic Pricing

13-1: “Target Costing at a Consumer Products Company”

This article looks at target costing, a process driven by the market. It goes through the five main steps in

target costing and then applies these steps through a consumer products example. Target costing works

best when fully integrated into the pre-existing product development process.

Discussion Questions:

1. How does target costing differ from cost plus pricing and what key elements does it incorporate?

It differs from cost-plus pricing in that it’s a way of managing the product-development process. The

target-costing process focuses on six key principles: price-led costing, customer focus, focus on

2. Explain how fixed costs are handled in the calculation of a target cost.

The fixed costs include not only fixed manufacturing costs, but also selling, general, and administrative

costs. Unlike at Boeing, Caterpillar, and other large manufacturers, new-product-development costs are

3. Where do opportunities to reduce costs occur?

13-10

Chapter 13 – Cost Planning for the Product Life Cycle: Target Costing, Theory of Constraints, and Strategic Pricing

13-2 “Integrating Activity-Based Costing and The Theory of Constraints”

The authors of this article show how ABC costing and the Theory of Constraints (TOC) methods

can be compared and used in a complementary fashion.

Discussion Question: Explain how ABC and TOC can be viewed as complementary methods.

The ABC costing approach provides accurate information for product costing and evaluating

the relative profitability of different products, especially when the mix of required

manufacturing activities differs significantly between products. However, as the authors

point out, the ABC method takes a “resource usage” approach to determining product

amounts of the supplied capacity. In essence, the ABC method, by assuming the equivalence

of resource supply and resource usage, provides a useful long-term measure of product

profitability, one wherein the short-term availabilities and limitations of supply are not

considered.

In contrast, the theory of constraints enables the manager to consider the short-term

allows effective short-term decision making when resource supplies and bottlenecks are

present.

13-11

Education.

Chapter 13 – Cost Planning for the Product Life Cycle: Target Costing, Theory of Constraints, and Strategic Pricing

13-3: “Is TOC for You?”

This article gives a good introduction to the objectives and techniques of the theory of constraints (TOC).

There is also a discussion of key performance measures related to to the application of TOC in

management accounting.

Discussion Questions:

1. What is meant by throughput?

2. What are the five steps of TOC?

The five steps of TOC are:

3. List some ways to increase the capacity on a constraint.

4. What are the five management accounting truths related to TOC?

Management Accounting Truth #1: Process improvements work together to speed up the whole operation..

Management Accounting Truth #2: You have to spend money to make money.

Management Accounting Truth #3: Operations can be made more efficient by improving labor efficiency

Chapter 13 – Cost Planning for the Product Life Cycle: Target Costing, Theory of Constraints, and Strategic Pricing

13-4: “Environmental Considerations in Product Mix”

With pressures from stakeholders, government and the public, companies often feel the pressure to

balance making profits with achieving environmental responsibility as well. This article looks at two

different methods to account for environmental costs: ABC costing method and TOC. It shows

calculations of both while also offering the positives and negatives to each method.

Discussion Questions:

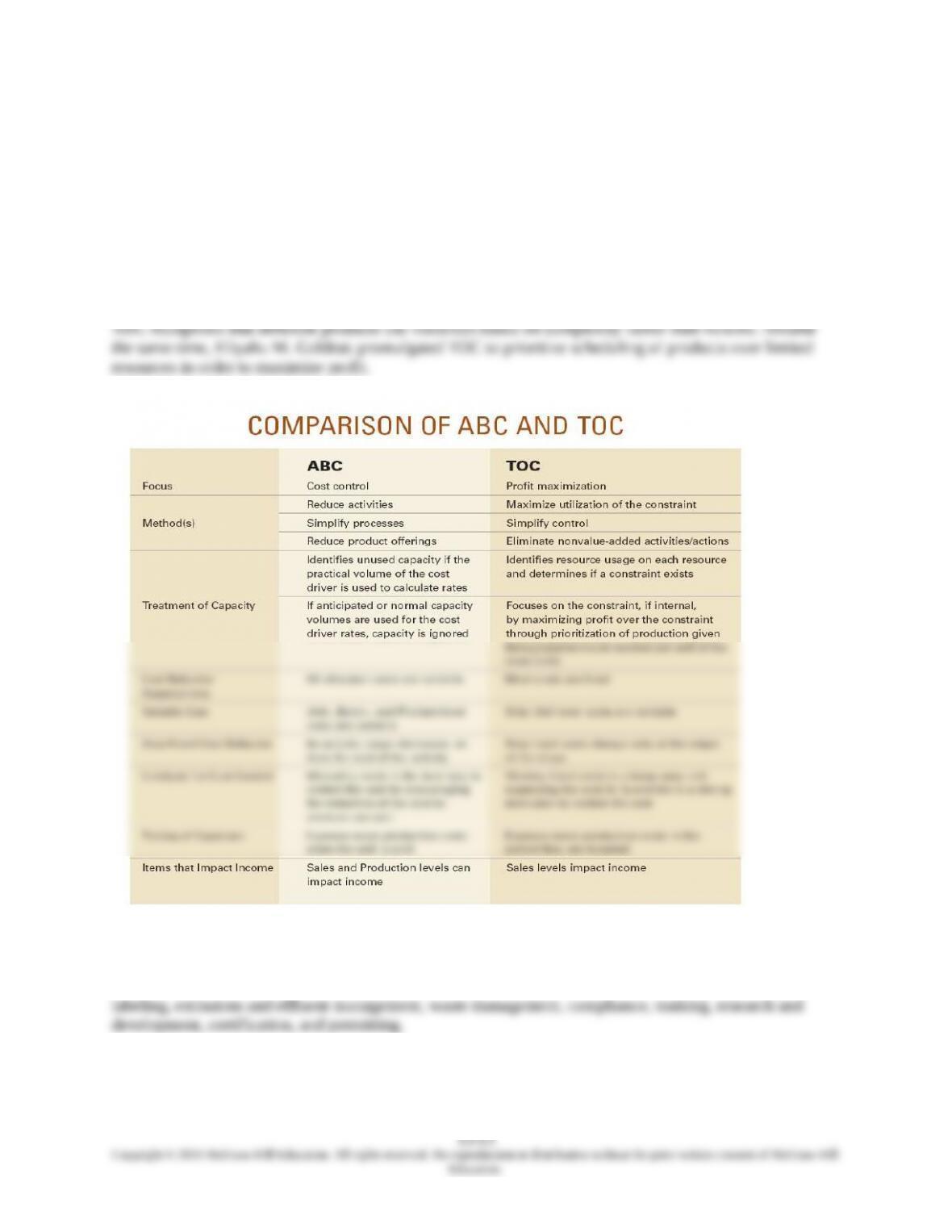

1. What are some of the main differences between TOC and ABC?

2. What are the common internal environmental costs companies face, according to the article?

Internal environmental costs when regulations are imposed may include record keeping, reporting,

3. Explain several scenarios where using TOC is always the best choice.

TOC is always the best choice given the following conditions:

Chapter 13 – Cost Planning for the Product Life Cycle: Target Costing, Theory of Constraints, and Strategic Pricing

1. Products use shared resources.

2. Demand for all of the products sharing those

solidified.

7. The creation of certain toxins is of concern to the

company, and there is a desire to determine the

product mix that generates the fewest toxins.

13-14

Education.