Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

Chapter 15 - Operational Performance Measurement: Indirect-Cost Variances and Resource-Capacity Management

efficiency of the customer order-handling process. (Note: this cost might increase a

bit to cover the cost of the TQM initiative.)

15-48 (Continued-2)

Note, however, that the cost of unused capacity increases, from $72,000 (90%

capacity utilization) to $180,000 (75% capacity utilization).

Practical Capacity:

Prior to TQM Implementation = 10,000

After TQM Implementation = 12,000

Resource Cost (Handling Customer Orders) = $720,000

Budgeted # of Customer Orders = 9,000

ABC Rates--Handling a Customer Order:

After TQM Implementation = 9,000 ÷ 12,000 = 75%

Conclusion: Efficiency initiatives (e.g., TQM) will lead to reduce resource spending

only if managers eliminate or redeploy the unused resource capacity that was created

by the efficiency improvement.

5. Faced with unused capacity, for example, the company can:

6. Logically, we would assign to a given customer or market segment the cost of unused

capacity IF the associated capacity were acquired specifically to serve that customer

or market segment. IF the unused capacity is associated with a given product line,

then the cost of unused capacity should logically be assigned to that product line (but

Chapter 15 - Operational Performance Measurement: Indirect-Cost Variances and Resource-Capacity Management

15-72

Education.

Chapter 15 - Operational Performance Measurement: Indirect-Cost Variances and Resource-Capacity Management

15-49 Two-Variance Analysis: Service Company Example (30 minutes)

1. Budgeted number of letters of credit approved: $1,000,000 $2,000 = 500

Overhead application rates:

2. Actual overhead costs incurred:

Variable: ($2,000 × 600 × 0.70) × 110% = $924,000

Insurance premium 270,000 $1,194,000

Flexible Budget:

Variable: $2,000 × 600 × 0.70 = $840,000

Insurance premium =

$270,000 0.9 = 300,000 $1,140,000

Fixed ($600,000 × 0.95) 670,000

Flexible-budget: $1,810,000

Overhead applied $3,340 × 600 × 0.70 = $1,402,800

$2,700 ÷ (1 − 0.10) = 300,000 1,702,800

Education.

Chapter 15 - Operational Performance Measurement: Indirect-Cost Variances and Resource-Capacity Management

15-50 ABC versus Traditional Approaches to Control of Batch-Related Overhead

Costs (50-60 minutes)

Additional information needed to solve this problem (highlighted in bold):

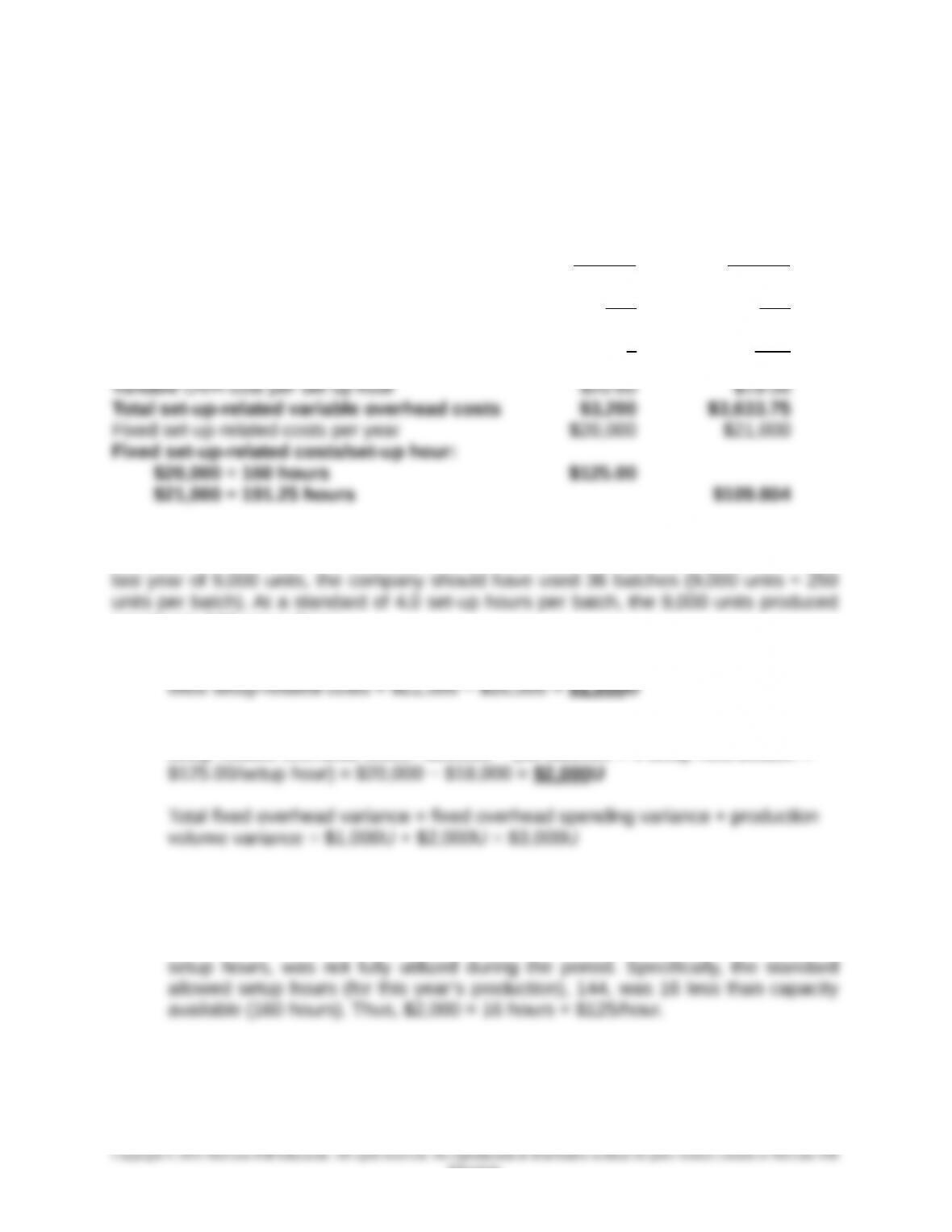

Budgeted Actual

Results Results

Units produced and sold 10,000 9,000

Batch size (units) 250 200

No. of batches 40 45

Set-up hours per batch 4 4.25

Total Set-up hours 160 191.25

Note that the control (flexible) budget for set-up-related variable overhead costs should

be based in this case on set-up hours (the controllable factor). Thus, given an output

equates to 144 set-up hours.

(1) (a) Fixed overhead spending variance = Actual fixed setup-related costs – budgeted

(b) Production volume variance = budgeted fixed setup-related costs – applied fixed

setup-related overhead costs= $20,000 − (36 batches × 4 setup-hours/batch ×

As the name implies, the fixed overhead spending variance means that last

spending on setup-related fixed overhead costs was $1,000 more than what was

envisioned when the master budget was prepared. The production volume

variance in this context means that capacity, measured in terms of budgeted

15-74

Education.

Chapter 15 - Operational Performance Measurement: Indirect-Cost Variances and Resource-Capacity Management

15-50 (Continued-1)

(2) (a) Variable setup-related overhead spending variance = actual variable setup-

related overhead costs − budgeted variable setup-related overhead costs based

on inputs (i.e., based on actual setup hours worked during the year)

= (actual batches × actual setup hours/batch × actual variable setup-related

overhead costs/setup hour) − (actual batches × actual setup hours/batch ×

(b) Variable setup-related overhead efficiency variance = FB for variable setup-

related overhead costs based on Inputs − FB for variable setup-related

overhead costs based on Outputs

batches than standard (actual # of batches = 45; standard allowed batches = 36,

as shown above); and (2) each setup took slightly more time than standard (4.25

hours/setup vs. 4.00 hours/setup). The net unfavorable variable setup-related

overhead variance indicates that the favorable spending variance was not

enough to offset the unfavorable efficiency variance.

(3) Fixed setup-related overhead costs are controlled primarily prior to the point of

operations. That is, they are controlled primarily through the planning process (for

example, the capital budgeting process or the use of zero-based budgeting). These

costs basically relate to the capacity/ability to produce.

On the other hand, variable setup-related costs, by definition, vary in response to

allocated all setup-related overhead costs by a single, volume-based activity

measure: number of machine hours. This approach (a) fails to recognize that some

15-75

Education.

Chapter 15 - Operational Performance Measurement: Indirect-Cost Variances and Resource-Capacity Management

15-50 (Continued-2)

of these overhead costs are capacity-related and therefore controlled differently,

and (b) fails to identify meaningful strategies for cost control. When machine hours

are used as the basis for cost allocation and some costs (as in this case) are not

(4) Most companies find that a comprehensive control system consists of both financial

and nonfinancial performance indicators. Thus, one would expect that operating

units in the Bangor Manufacturing Company would have timely access to

nonfinancial performance indicators such as process yields (e.g., ratio of good

outputs to inputs), manufacturing processing time, reject rates, percent first-pass

yield, defect rates (e.g., parts-per-million, ppm), etc. Such information has the

15-76

Education.