Chapter 13 – Cost Planning for the Product Life Cycle: Target Costing, Theory of Constraints, and Strategic Pricing

Chapter 13

Cost Planning for the Product Life Cycle: Target Costing,

Theory of Constraints, and Strategic Pricing

Teaching Notes for Cases

13-1. Strategy; the Theory of Constraints

1. What is the firm’s competitive strategy?

Information in the case suggests that CI is the high-cost producer that led the industry in quality,

which implies differentiation. What strategy are they pursuing now? Cost leadership, through

robotics, increasing batch sizes, reducing idle time, efforts to reduce overhead. There should be a

combined focus on customer satisfaction (differentiation) and plant reengineering (using TOC), to

improve the use of existing capacity, i.e., to improve throughput through the plant.

For example, why did they reject the Saudi offer, which would have been consistent with their

quality image? The Saudi deal should have been accepted; no reason to turn down low margin deals in a

depressed market.

Why the steep drop in price for AA knives? This simply intensified overall competition in the

industry and since competitors responded, made everyone in the industry less profitable. The steep drop

in price of AA knives is not consistent with CI’s quality image

2. What motivated the cost reduction strategy?

A depressed market for their product

Cash flow problems

Losses

Is the firm close to bankruptcy? In the actual case, the bank gave the firm 6 months or they would

enforce reorganization.

Did the cost reduction strategy work? Why?

The answer is no, because:

a. Efficiency through larger batches, less idle time, and reduced set-up time: the result was an

increase in WIP, difficulties in scheduling the large batches (less plant flexibility), and

increased overtime

b. Overhead reduction – hinged on increase in sales, which did not happen

c. The robotics did reduce labor costs of arc welding, but savings were not realized:

i.) the arc welders were not released but were reassigned

ii.) the robotics eventually caused additional labor costs necessary to manage them

3. How did the standard costs system affect the cost reduction strategy?

4. What is the role of WIP in the cost reduction strategy?

Insurance against machine or scheduling failure

Makes scheduling easier

Chapter 13 – Cost Planning for the Product Life Cycle: Target Costing, Theory of Constraints, and Strategic Pricing

5. Is the new Production Control/Inventory Control (PCIC) manager on the right track with the smaller

lot sizes?

6. What steps is the PCIC likely to take now?

The five steps of TOC are:

The binding constraints: heat treating (due to excessive overtime) and hardfacing (due to under–

utilization of capacity)

and marketing was not integrated into the effort.

7. What type of cost system should be used at CI?

Standard costing is an effective method for controlling costs in the manufacturing plant, and can

13-2

Education.

Chapter 13 – Cost Planning for the Product Life Cycle: Target Costing, Theory of Constraints, and Strategic Pricing

13-2 Blue Ridge Manufacturing (B)

Note: This case uses information from Case 5-1: Blue Ridge Manufacturing (A)

Answers to Discussion Questions:

1. What is Blue Ridge Manufacturing’s strategy now that it has developed the new products and become

a global competitor? Has the strategy changed?

Collide: Competing Through Confrontation). Firms that compete globally under this type of competition

often adopt target costing as a way to achieve the desired product enhancements at the minimum (i.e., the

“target”) cost

Note that before the introduction of the new ink, Blue Ridge’s strategy could best be described as cost

leadership based on their innovation in plant, the ABC-based costing of manufacturing cost to supply the

needed accuracy in product costs, and the “medium quality” of their product. Case (A) shows how the

ABC approach was extended to analyze more accurately the profit contribution of the three customer

groups. At this time the focus was on productivity and cost reduction. Now the firm has a broader

strategic focus, including innovation and quality. The firm’s cost management methods must also adapt,

as addressed in the following question.

2. How should Blue Ridge Manufacturing adapt to the new competitive environment?

With the change to differentiation and/or confrontation (per Robin Cooper), the role of cost

management has changed. Previously, there was a focus on cost efficiency and accuracy of cost

information, to support the previous cost leadership strategy. Consistent with this approach, the firm had

adopted ABC costing in both manufacturing and in the costing of the three major customer groups.

Moreover, the firm was committed to advanced manufacturing techniques to support the needed

manufacturing efficiency.

Now, with global competition and the manufacture of new products, the firm’s competitive

challenges have also changed. The role of cost management has now broadened, to include more

attention to the design, or “upstream” phase of product costs. While a great deal of attention has been

given, using ABC costing to develop accurate manufacturing and “downstream” costs (the analysis of

13-3

Education.

Chapter 13 – Cost Planning for the Product Life Cycle: Target Costing, Theory of Constraints, and Strategic Pricing

At the same time, target costing can help the firm know when to reject orders from customers with

poorly-developed designs, if price cannot be adjusted to cover the additional costs. For a useful

reference, John Brausch (“Target Costing for Profit Enhancement,” Management Accounting,

November 1994) explains how target costing can be used within a textile firm.

13-4

Chapter 13 – Cost Planning for the Product Life Cycle: Target Costing, Theory of Constraints, and Strategic Pricing

13-3 Nebraska Toaster

1. Calculate Product Target Cost: for the Toaster Company is $16.00

(Competitive Market Price $20 – Desired Profit $4 = Target Cost $16)

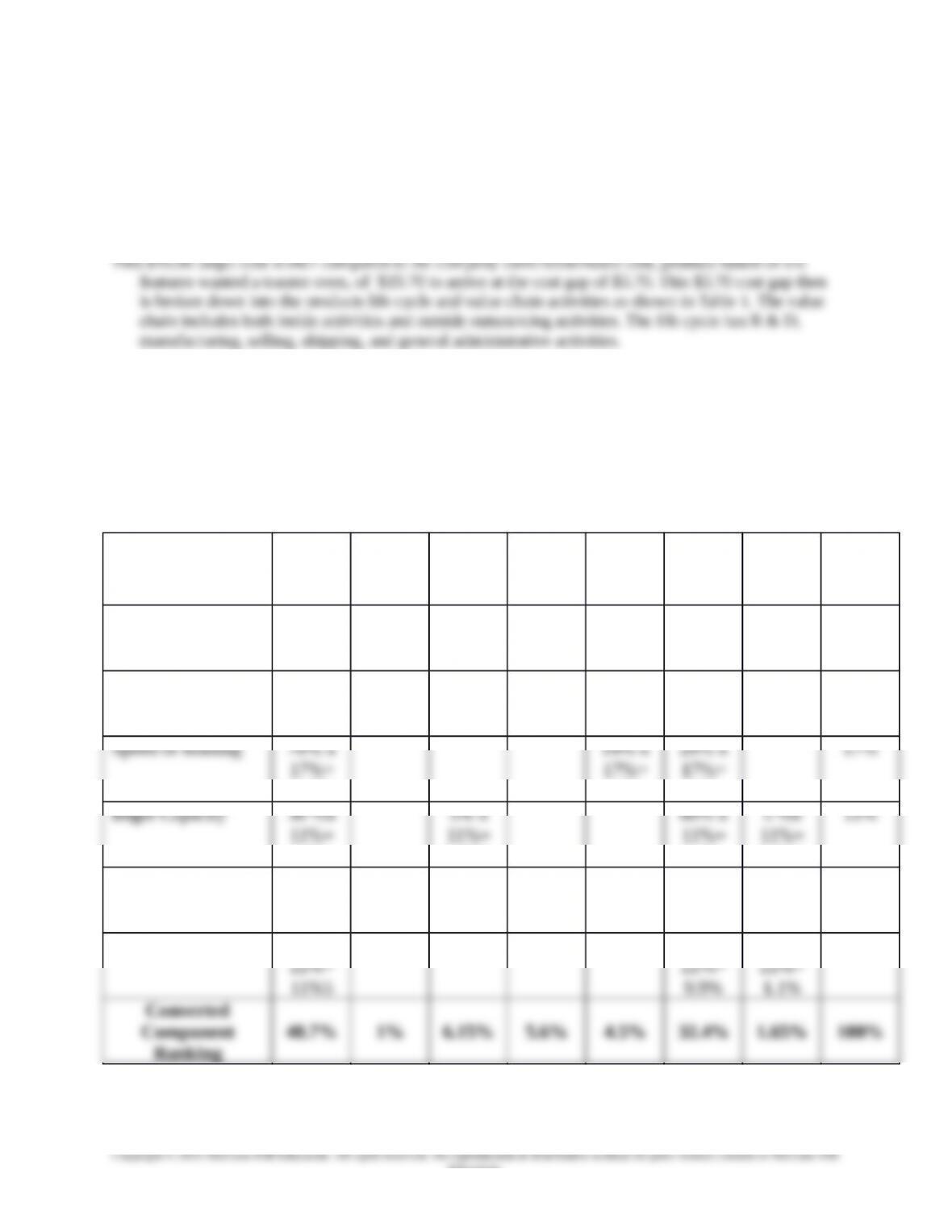

2. Combine step 2 and step 3from the case, we derive the Table 5 amounts. The “Relative Ranking”

column percentages are from Table 3.

Table 5 Quality Function Deployment Analysis

Components

or Functions

Customer

Requirements

Heating

Unit

Display

Light

Lever Spring

Coil

Temp.

Control

& Timer

Body

Design

Crumb

Catcher

Relative

Rank-

ing

Toasts and grills

properly

50% x

28% =

14%

20% x

28% =

5.6%

20% x

28% =

5.6%

10% x

28% =

2.8%

28%

Size 50% x

17% =

8.5%

50% x

17%=

8.5%

17%

3.3%

0.55%

6.6%

0.55%

Appearance 20 %x

5%=

1%

80% x

5%=

4%

5%

Easy to Clean 50 %x

45% x

5 %x

22%

Ranking

13-5

Education.

Chapter 13 – Cost Planning for the Product Life Cycle: Target Costing, Theory of Constraints, and Strategic Pricing

This gives the company the importance and value of each component relative to the features that create

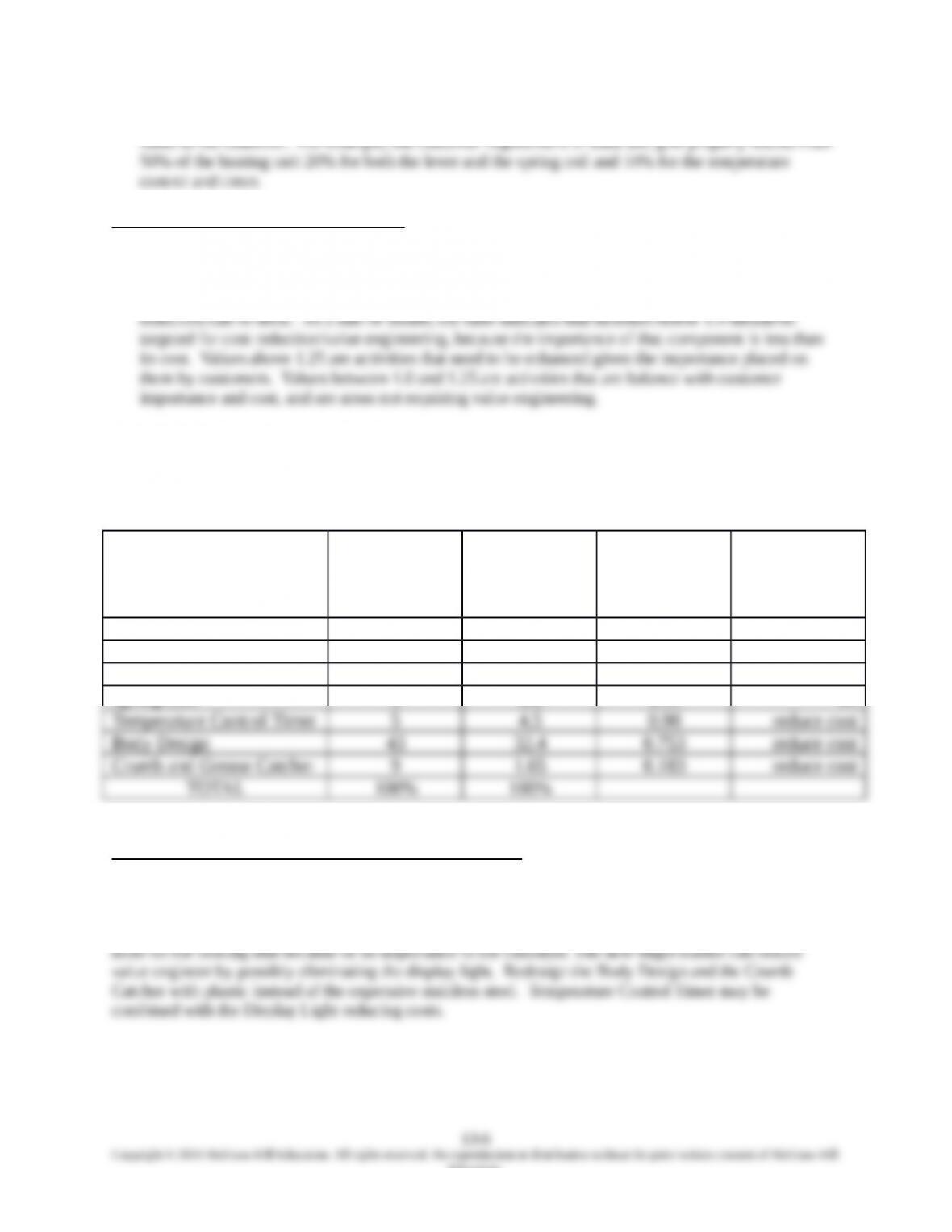

Calculating Value Index for Each Function

The next process is the value index that targets areas for value engineering. It considers the toaster oven

customer requirements at their level of importance to the amount of cost that are involved with that

component. The value index shown in Table 6 calculates a ratio that shows the areas were cost

Column 2, the “Component % of Cost” column percentages are inputted from the last column of Table 2.

Column 3, the “Relative Importance %” column percentages are inputted from the last row of Table 5.

Table 6 Value Index

(1) Component or

Function

(2)

Component %

of Cost

(3) Relative

Importance %

(4) Value

Index =

Col. 3 /

Col. 2

(5) Action

Implied

Heating Unit 20 48.7 2.435 enhance

Display Light 13 1 0.077 reduce cost

Lever 5 6.15 1.23 ok

Spring Coil 5 5.6 1.12 ok

Applying Value Engineering and Cost reduction Techniques

From the value index, Nebraska Toaster Company can see what areas to enhance and areas to apply

value engineering. At this point the entire company can generate ideas on how to accomplish these steps

of reducing costs and maintaining the level of functionality. For example, they should enhance and spend

Education.

Chapter 13 – Cost Planning for the Product Life Cycle: Target Costing, Theory of Constraints, and Strategic Pricing

13-4. Mercedes-Benz All Activity Vehicle (AAV)

The target costing case literature contains numerous examples of Japanese cost management practices;

however, few cases describe the use of target costing by large companies outside Japan. The purpose of

Student Assignment Questions

1. What is the competitive environment faced by MB?

Students will identify a number of changes, including significant market share lost to Japanese

companies such as Lexus. Stress the importance of a cultural change taking place within top management

at Mercedes. Reinforce that Mercedes is a company that had never lost money. They simply built the best

2. How has MB reacted to the changing world market for luxury automobiles?

Students should identify the following changes implemented by management at Mercedes; try to

get them to explain how different these approaches were from traditional strategies at Mercedes:

3. Using Cooper’s cost, quality, functionality chart, discuss the factors on which MB competes with other

automobile producers such as Jeep, Ford, and GM. If the instructor wishes to give a brief mini-lecture on

Robin Cooper’s survival triplet and confrontation strategy, this is a good point in the case discussion to do

so. (Robin Cooper, When Lean Enterprises Collide, Boston: Harvard Business School Press, 1995.)

The factors are:

toward the luxury end of the spectrum. Also, unlike many Japanese examples, Mercedes does not use

target costing as a strict cost control mechanism to produce the lowest priced product in its class.

4. How does the AAV project link with MB strategy in terms of market coverage?

The new introductions expand the product line of the traditionally luxury-oriented manufacturer. Recent

product introductions include the following: