Chapter 09 – Short-Term Profit Planning: Cost-Volume-Profit (CVP) Analysis

CHAPTER 9

SHORT-TERM PROFIT PLANNING:

COST-VOLUME-PROFIT (CVP) ANALYSIS

QUESTIONS

9-1 The underlying relationship depicted in a cost-volume-profit (CVP) analysis is

that costs, revenues, and operating profits (Y) all change in a predictable way as

9-2 The contribution margin ratio (CMR) is: (selling price per unit − variable cost per

unit) ÷ (selling price per unit) = p ÷ (p – v)

The contribution margin ratio (CMR) is a measure of profitability. The CMR tells

us the change in operating profit associated with a given change in sales dollars.

It is a useful measure of the relative contribution to profit of different products,

9-3 The basic assumption of the CVP model is that the behavior of revenues and

total costs is assumed to be linear over the relevant range of activity. Managers

must be careful to remember that the calculations done within the context of a

CVP model is deterministic, not stochastic), and a single cost driver: volume.

9-4 Sensitivity analysis is used to deal with uncertainties in profit planning, in two

major respects:

1. To determine which factors have the greatest influence on profit, and to assess

9-5 Sensitivity analysis deals with the risk that sales may fall short of expectations or

9-6 The issue of taxes does not affect the calculation of the breakeven point because

the breakeven point is determined at the level of zero profit and income taxes are

9-1

Education.

9-7 Margin of safety (MOS) = sales − breakeven sales, where “sales” can be either

9-8 The concept of operating leverage refers to the extent to which fixed (rather than

variable) costs characterize an organization’s cost structure. The higher the

9-9 The degree of operating leverage (DOL) is a measure, at any volume (X), of the

sensitivity of operating profit to a change in sales volume. It is measured as the

percentage change in operating profit for each percentage change in sales.

9-10 To find the breakeven point for multiple products, one must assume that the sales

of the products will continue at the present sales mix. (Each product will continue

to comprise the same proportion of total sales.) The constant sales mix permits

9-2

Education.

Chapter 09 – Short-Term Profit Planning: Cost-Volume-Profit (CVP) Analysis

BRIEF EXERCISES

9-11Contribution margin per unit = selling price per unit − variable cost per unit

9-12 Total Contribution Margin = (selling price per unit − variable cost per unit) × #units

sold

9-13 Breakeven Point—Units:

Q × p = F + (v × Q)

Q × $20 = $175,000/quarter + ($10 × Q)

9-14 Breakeven Point—Dollars:

p × Q = F + (v × Q)

Q = 500 patient-visits/month

9-15 Breakeven in Dollars: Y = [(v/p) × Y] + F

Y = [($500,000/$750,000) × Y] + $75,000/quarter

Y = [2/3 × Y] + $75,000/quarter

9-16 Unit Sales Q = (F + πB) ÷ (p – v)

Q = ($400,000 + $200,000)/quarter ÷ ($1 − $0.50)

Q = 1,200,000 bottles/quarter

9-3

Education.

Chapter 09 – Short-Term Profit Planning: Cost-Volume-Profit (CVP) Analysis

9-17 With a contribution margin (p – v) of $8 per battery, operating profit will increase

9-18 Q = F + π A/(1− t )

(p – v)

Q = $200/week + [$400/(1− 0.2)]/week

($10 − $5)/unit

9-19 Margin of Safety (MOS), in units = Planned Sales – Breakeven Sales

= 20,000 units/quarter

MOS, in $ = Planned Sales ($) − Breakeven Sales ($)

= $40,000

9-20 Degree of Operating Leverage (DOL) = Contribution Margin ÷ operating income

= [($40 − $20)/unit × 400,000 units] ÷ $2,500,000

9-4

Education.

Chapter 09 – Short-Term Profit Planning: Cost-Volume-Profit (CVP) Analysis

EXERCISES

9-21 Breakeven Planning; Profit Planning (30-40 minutes)

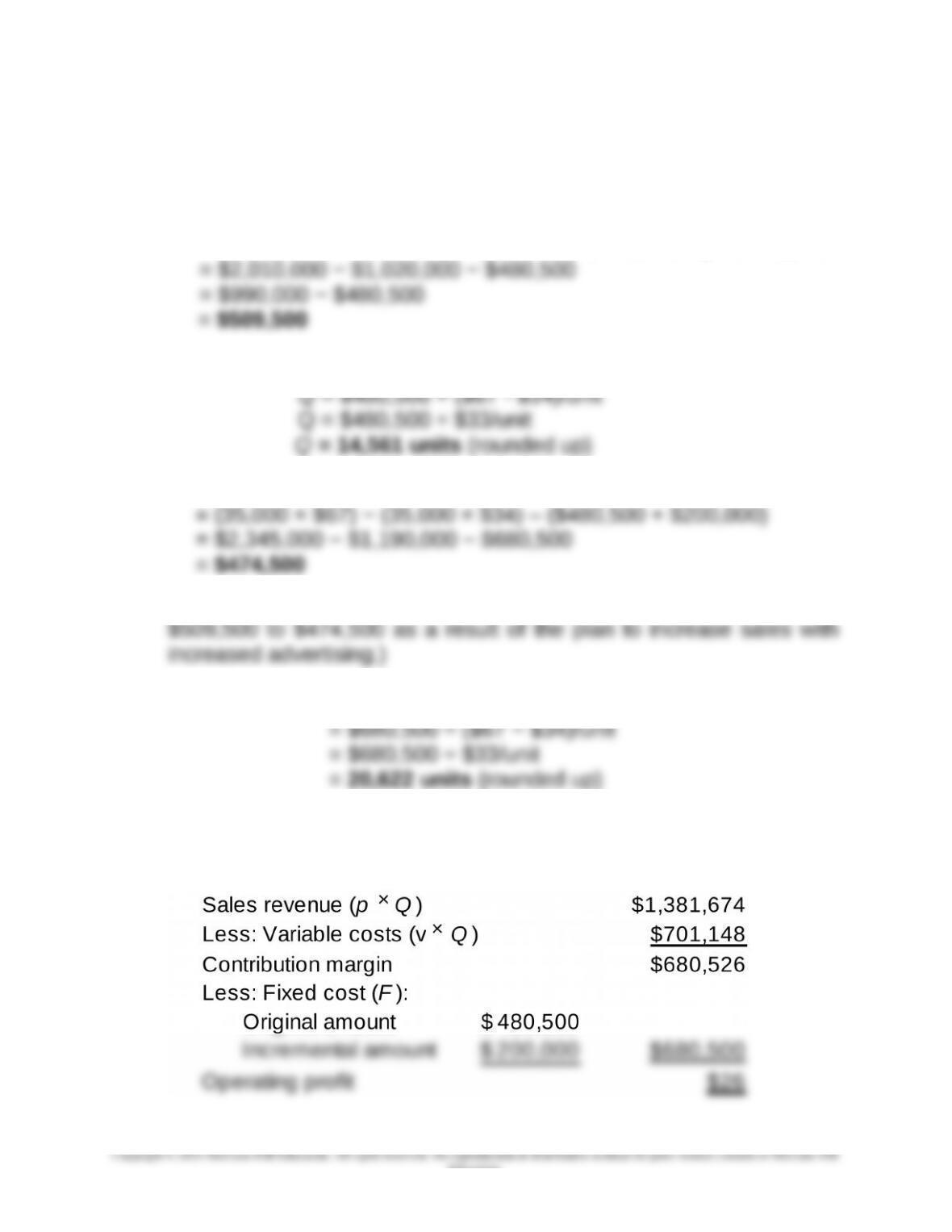

1. πB= Sales − variable costs − fixed cost

= (30,000 units × $67/unit) − (30,000 units × $34/unit) − $480,500

2. BE units: $67Q = $34Q + $480,500

3. πB = Sales – variable costs – fixed costs

(Operating profit falls by $35,000 = ($33 × 5,000) − $200,000, from

4. BE units: Q = F ÷ cm per unit

(Operating profit is lower, per part 3 above, and breakeven is higher.)

Contribution Income Statement:

9-5

Education.

Chapter 09 – Short-Term Profit Planning: Cost-Volume-Profit (CVP) Analysis

9-21 (Continued)

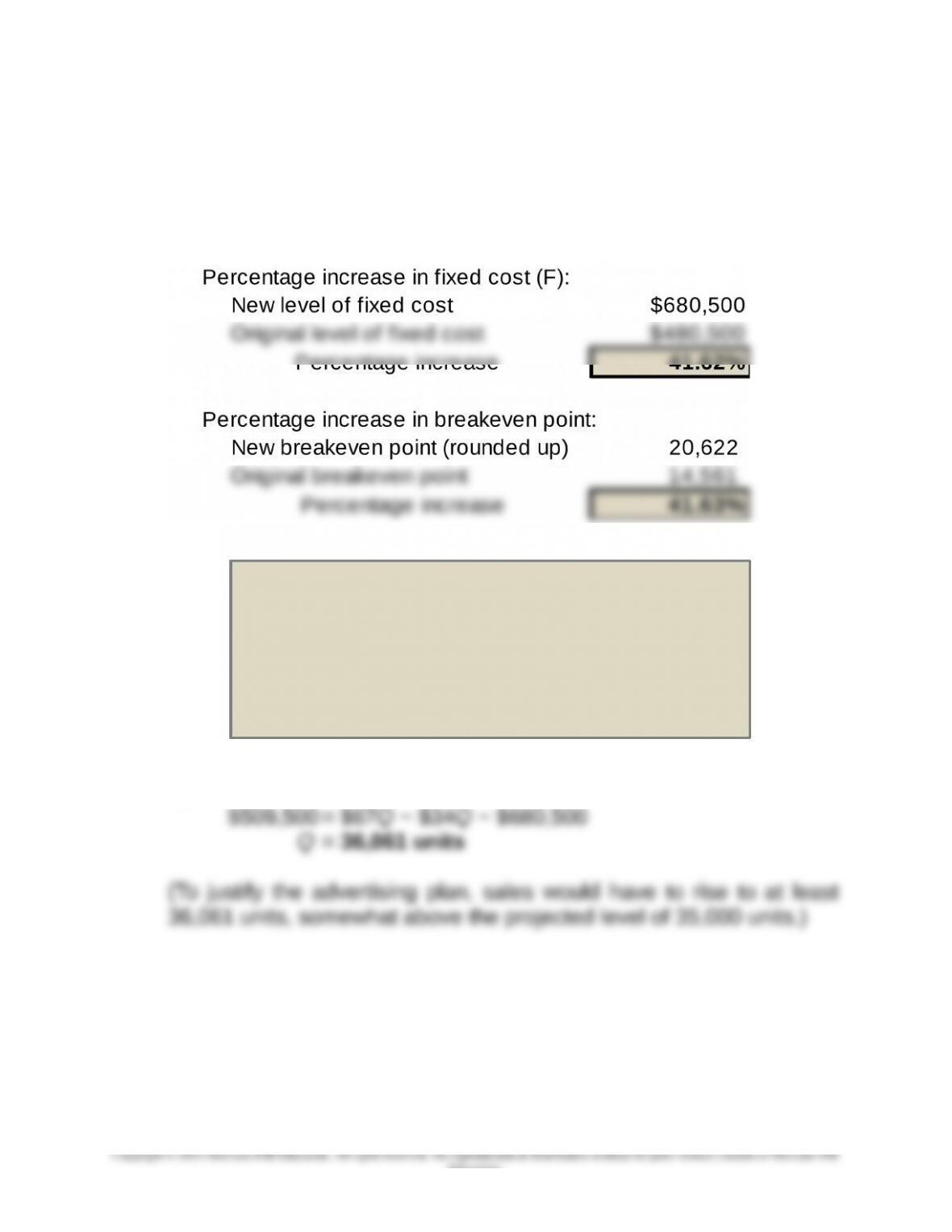

(the slight difference between the indicated operating profit,

$26, and zero is due to rounding up the breakeven point to the

nearest whole number, 20,622 units)

5. Operating profit = Sales – variable costs – fixed costs

9-6

Education.

Slight diference in the above answers is due to

rounding on sales volume, Q. The primary point,

however, is that a given percentage change in ixed cost

leads to an equivalent percentage change in the

breakeven point. (This can be conirmed precisely if the

above breakeven volumes were not rounded.)

Chapter 09 – Short-Term Profit Planning: Cost-Volume-Profit (CVP) Analysis

9-7

Education.

Chapter 09 – Short-Term Profit Planning: Cost-Volume-Profit (CVP) Analysis

9-22 Cost Planning; Machine Replacement (30-40 minutes)

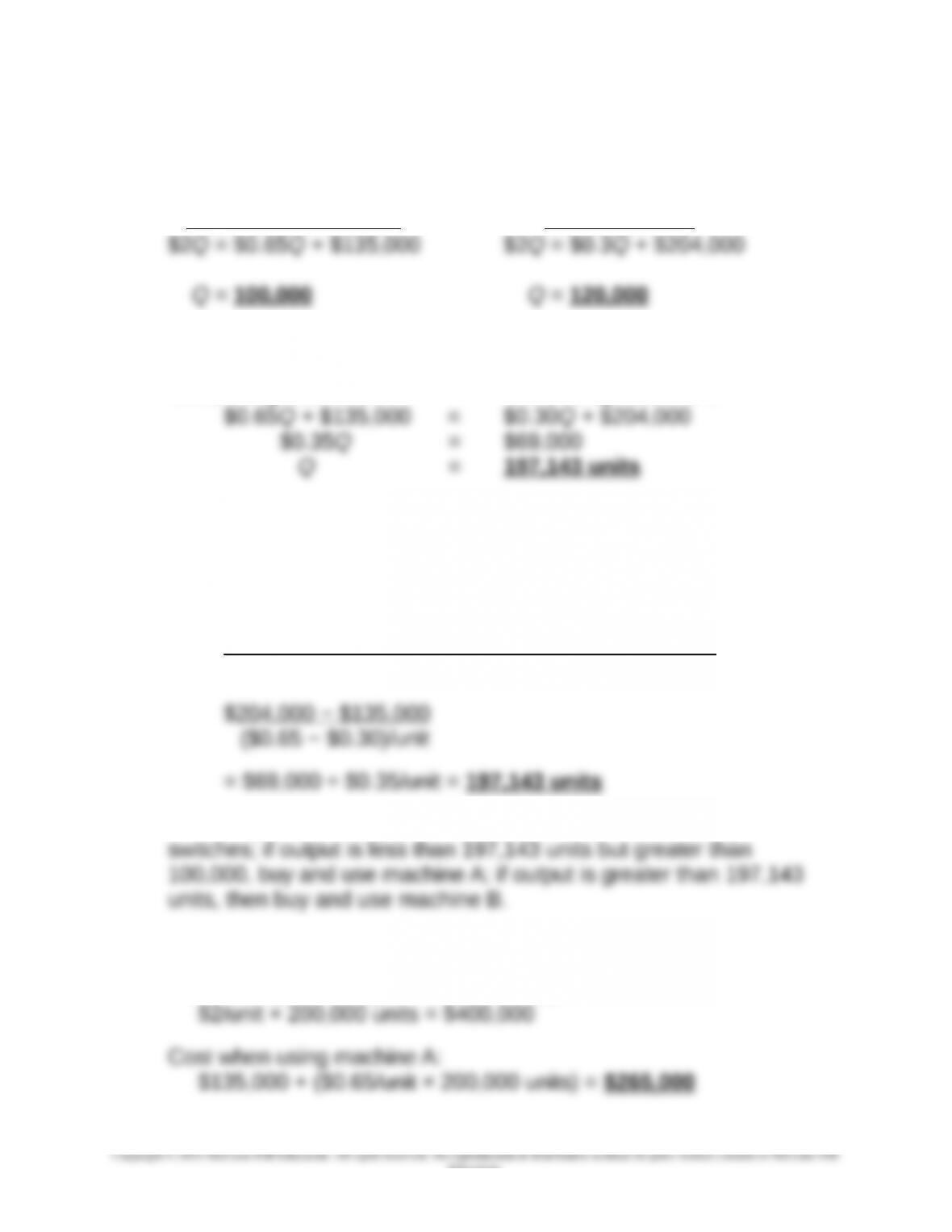

1. Breakeven volumes (total external cost/year = $2Q):

For Machine A For Machine B

2. Cost indifference point, Q:

Cost, using Machine A = Cost, using Machine B

When 197,143 switches are needed, the Vista Company is indifferent

as to which machine to use: the total cost under each of the two

decision alternatives is the same at this volume.

An alternative way to determine the indifference point is:

Fixed cost of Machine B − Fixed Cost of Machine A

Unit variable cost of A − Unit variable cost of B

Summary of (1) and (2): If output is less than 100,000, buy the

2. Total cost if volume = 200,000 units/year:

Cost when purchasing from outside supplier:

9-7

Education.

Chapter 09 – Short-Term Profit Planning: Cost-Volume-Profit (CVP) Analysis

9-22 (Continued-1)

Cost when using machine B:

4. Recommendation to management:

Considerations regarding outsourcing (rather than making

internally): what is the reliability of the existing supplier? Likely price

increases in the future from this supplier? What is the reliability of the

external supplier (delivery time, etc.)? As we’ve seen with supply

Considerations regarding insourcing (rather than purchasing

externally from the current supplier): is sufficient capital (to purchase

and install machinery) available? Are there any training-related costs

to be borne? The decision to insource increases the operating

leverage of the company, which in turn increases the business (or

operating) risk of the company. Therefore, what is the long-term

The basic point to make to students is that choice of cost structure

both reflects and influences a company’s strategy. This elevates the

9-8

Education.

9-23 Structuring Sales Commissions (15-20 min)

1. Omega–because it has the higher selling price and therefore the larger

2. From the standpoint of the company, profits may be higher if customers

purchase more units of Alpha (relative to Omega). This is because Alpha

has the higher contribution margin per unit.

To eliminate such a conflict (i.e., the goal-congruency issue), Questar

could revise its compensation plan to motivate greater sales of Alpha. It

could do this by basing sales commissions on contribution margin

generated by sales rather than sales dollars generated. If fixed costs are

not affected by the resulting shift in sales mix (toward increased sales of

Alpha), maximizing contribution margin will also maximize operating

Addendum: Bazerman, M., and A. E. Tenbrunsel. 2011. Ethical

breakdowns. Harvard Business Review (April), pp. 58-65.

Ill-Conceived Goals (p. 60)

In the above-reference article, the authors state: “In our teaching, we

often deal with sales executives. By far the most common problem they

report is that their sales forces maximize sales rather than profits. We

ask them what incentives they give their salespeople, and they confess

to actually rewarding sales rather than profits. The lesson is clear: When

employees behave in undesirable ways, it’s a good idea to look at what

you’re encouraging them to do.”

9-9

Education.