Chapter 04 – Job Costing

4-41 Plantwide vs. Departmental Overhead Rate (30 min)

1. Budgeted Overhead = ($150,000 + $94,000) + ($80,000 + $163,000)

= $487,000

Budgeted Direct Labor-hours = 1,000 units x (15 + 10) hours

2. Budgeted Machine-hours = 1,000 units x (5 + 15) hours = 20,000 hours

Predetermined Overhead Rate = $487,000 ÷ 20,000

3. Using Direct Labor-hours:

Department A Department B Total

DL-hours 1,000 x 15 1,000 x 10

= 15,000 hours = 10,000 hours 25,000 hours

Overhead applied

15,000 x $19.48 10,000 x $19.48

= $292,200 = $194,800 $487,000

Using Machine-hours:

4. If direct labor-hours are used to apply factory overhead, Department A

is assigned more than its total estimated overhead and Department B is

assigned less. Therefore, Department A will assign more overhead to

products than if a departmental rate were used and Department B will

Chapter 04 – Job Costing

4-41 (continued -1)

5. Using direct labor-hours for Department A:

Predetermined Overhead Rate = $244,000 ÷ 15,000

= $16.267 per direct labor-hour (rounded)

Applied Overhead = 1,000 units x 15 hours x $16.27 = $244,000 (rounded)

Using machine-hours for Department B:

4-22

Education.

Chapter 04 – Job Costing

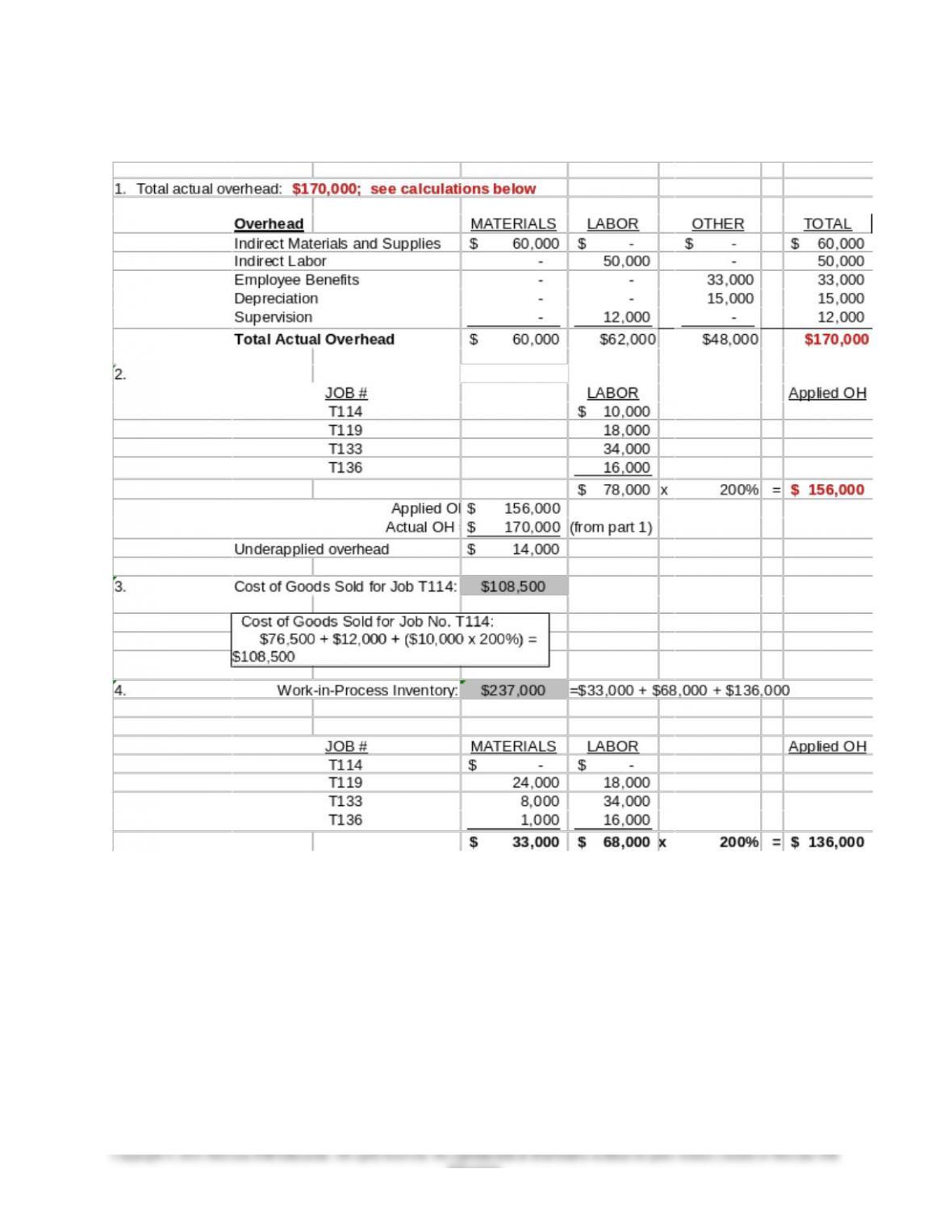

4-42 Application of Overhead (25 min)

4-23

Education.

Chapter 04 – Job Costing

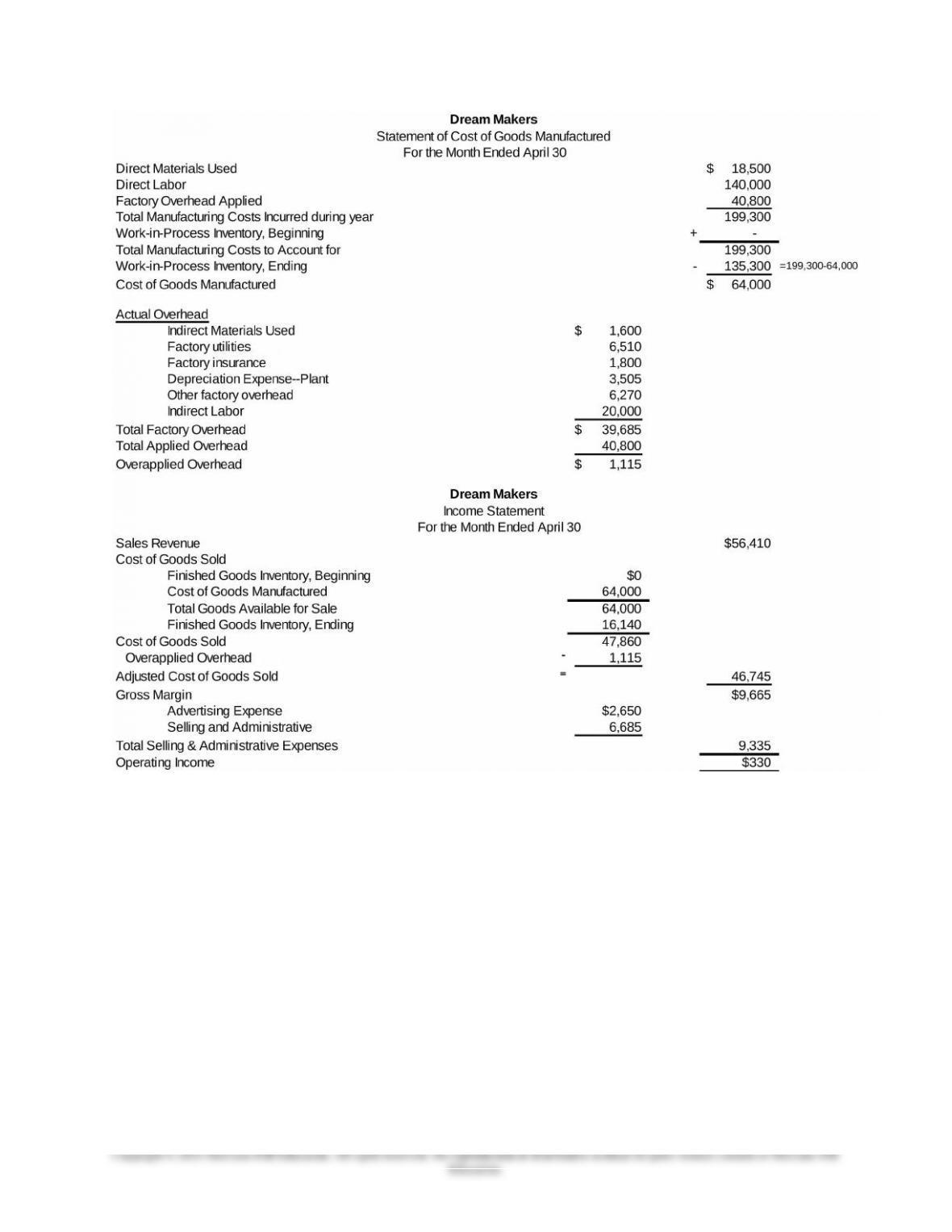

4-43 Cost Flows; Application of Overhead (40 min)

1. Predetermined Overhead Rate

= $455,600 ÷ 33,500 = $13.60 per direct labor hour

2. a. Factory Overhead 1,800

Prepaid Insurance 1,800

b. Selling& Administrative Expense 1,025

Accumulated Depreciation 1,025

e. Work-in-Process Inventory 140,000

Factory Overhead 20,000

Cash 160,000

f. Factory Overhead 6,270

Cash 6,270

g. Materials Inventory 24,500

Accounts Payable 24,500

i. Selling & Administrative Expense 5,660

Cash 5,660

j. Factory Overhead 3,505

Accumulated Depreciation 3,505

4-24

Education.

Chapter 04 – Job Costing

4-43 (continued -1)

k. Advertising Expense 2,650

Cash 2,650

l. – Direct labor hours = 4,000 total hours – 1,000 indirect labor hours

– Applied Overhead = $13.60 x 3,000 direct labor hours = $40,800

Work-in-Process Inventory 40,800

Factory Overhead 40,800

m. Finished Goods Inventory 64,000

Work-in-Process Inventory 64,000

3. Actual Overhead = $1,800(a) + $6,510(d) + $20,000(e) + $6,270(f) +

$1,600(h) + $3,505(j) = $39,685

Overapplied Overhead = $40,800 – $39,685 = $1,115

Decrease Cost of Goods Sold

4-25

Education.

Chapter 04 – Job Costing

4-43 (continued -2)

4.,5.

4-26

Chapter 04 – Job Costing

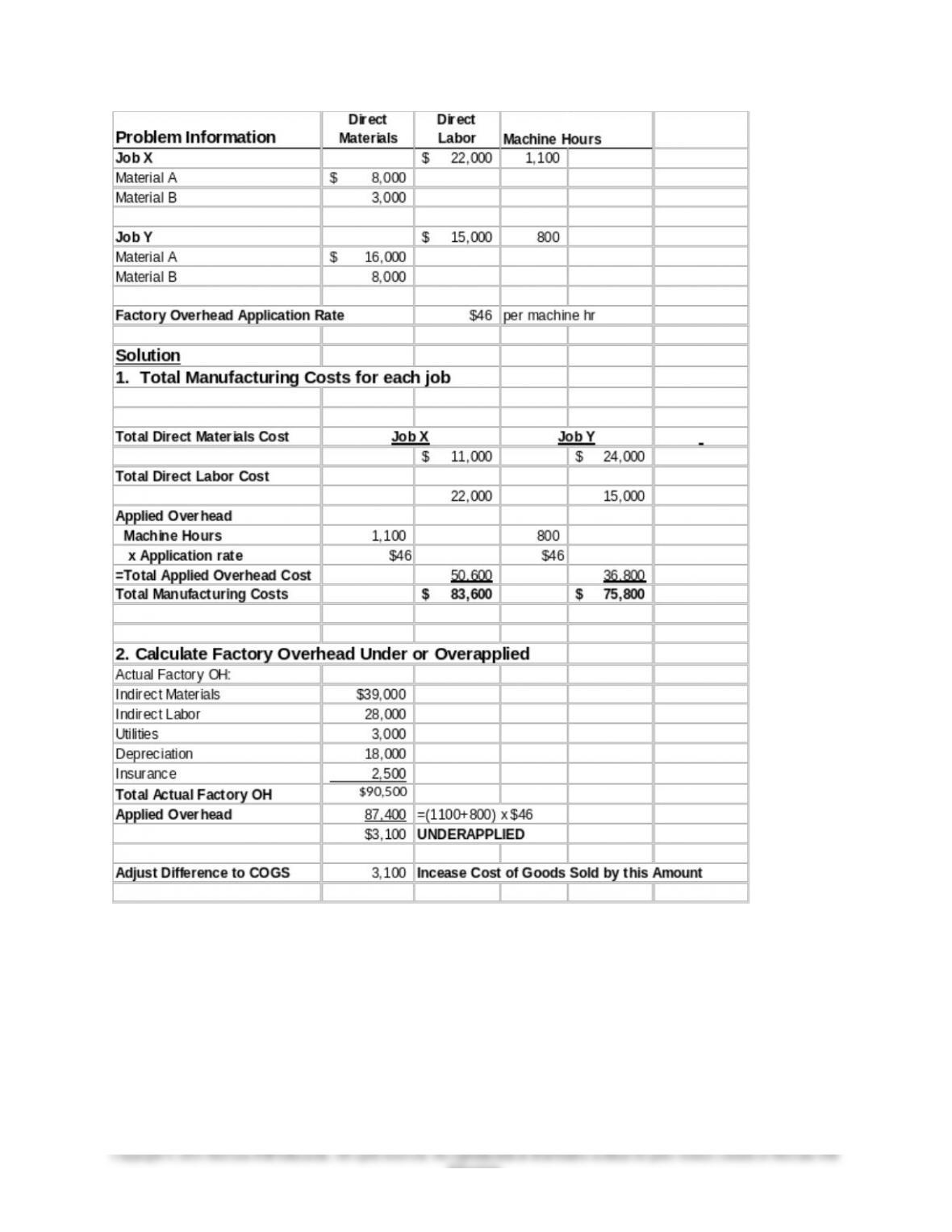

4-44 Application of Overhead (30 min)

Note: the information in part (a) is not needed for the solution.

1. Total manufacturing cost: Job X = $83,600; Job Y = $75,800

2. Underapplied overhead: $3,100; increase Cost of Goods Sold

See calculations below:

4-27

Chapter 04 – Job Costing

4-28

Education.

Chapter 04 – Job Costing

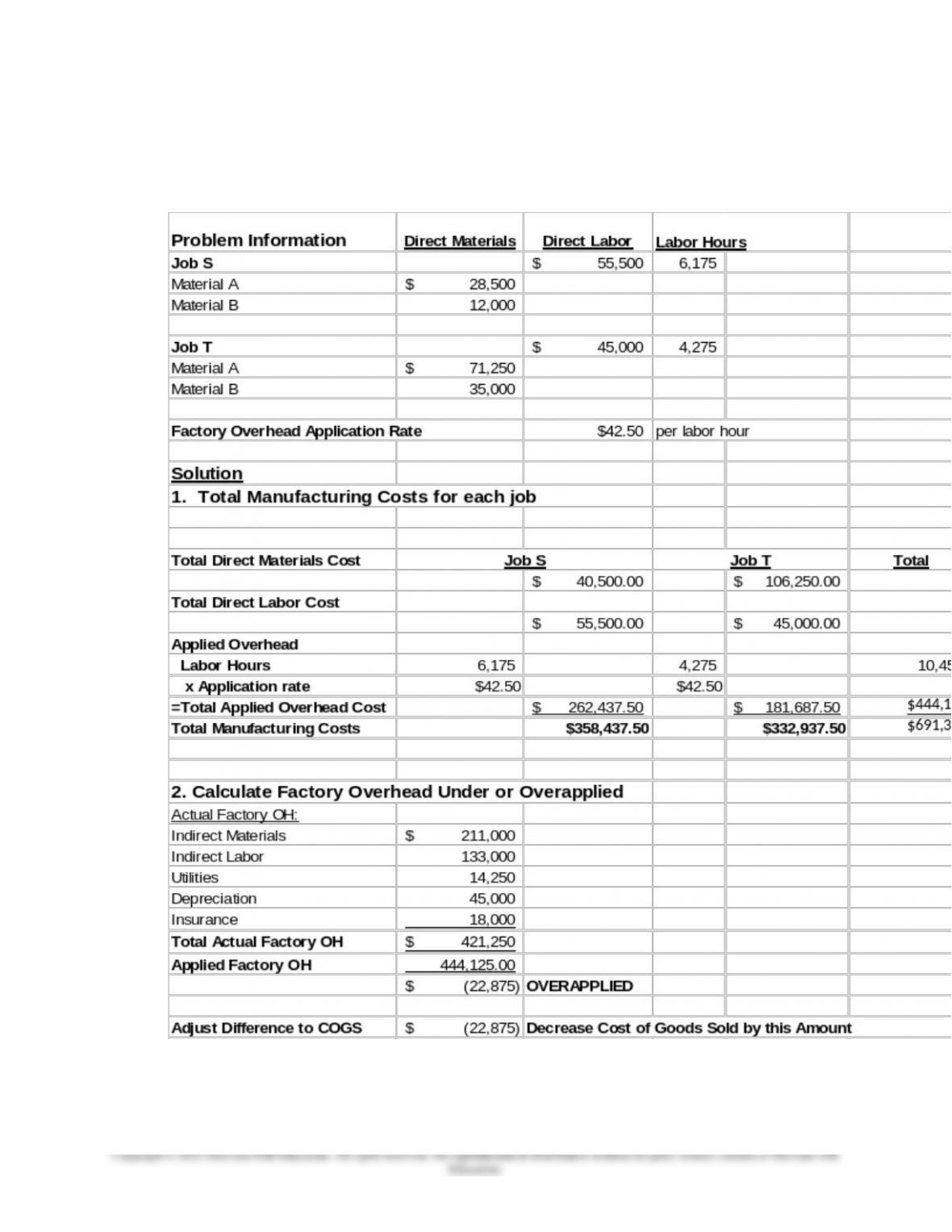

4-45 Application of Overhead (20 min)

1. Total manufacturing cost: Job S = $358,437.50; Job T= $332,937.50

2. Overapplied overhead: $22,875; decrease Cost of Goods Sold

See calculations below:

4-29

Chapter 04 – Job Costing

4-46 Cost Flows, Application of Overhead (50-60 min)

1. Predetermined Overhead Rate

= $1,261,500 ÷ 87,000 = $14.50 per direct labor-hour

2. a. Materials Inventory 130,000

Accounts Payable 130,000

$26 x 5,000 = $125,000

b. Materials Inventory 1,800

Accounts Payable 1,800

$36 x 50 = $1,800

(note that indirect materials are included in material inventory)

c. Work-in-Process Inventory 91,000

Factory Overhead 1,116

Materials Inventory (direct materials) 91,000

Materials Inventory (indirect materials) 1,116

$26 x 3,500 = $91,000

$36 x 31 = $1,116

f. Factory Overhead 3,500

Prepaid Insurance 3,500

g. Factory Overhead 8,500

Accumulated Depreciation 8,500

4-30