Chapter 17 – The Management and Control of Quality

17-37 (Continued)

The request by Sanchez is unethical because it would suppress information that

could influence an understanding of the results of operations by the company. Also,

by withholding information about the contingent liability, Sanchez is not

communicating information objectively.

2. Resolution of Ethical Conflict—the IMA Standards specify that when an individual

is faced with ethical issues, the individual should follow the policies established by

the organization to deal with (resolve) such conflicts. If these policies do not resolve

the ethical conflict, then the following courses of action are recommended:

The individual should discuss the issue with his/her immediate supervisor (except

If Stein is not able to achieve a satisfactory resolution of the matter, she should

submit the issue to the next management level. (Note: contact with levels above

Chapter 17 – The Management and Control of Quality

17-12

Education.

Chapter 17 – The Management and Control of Quality

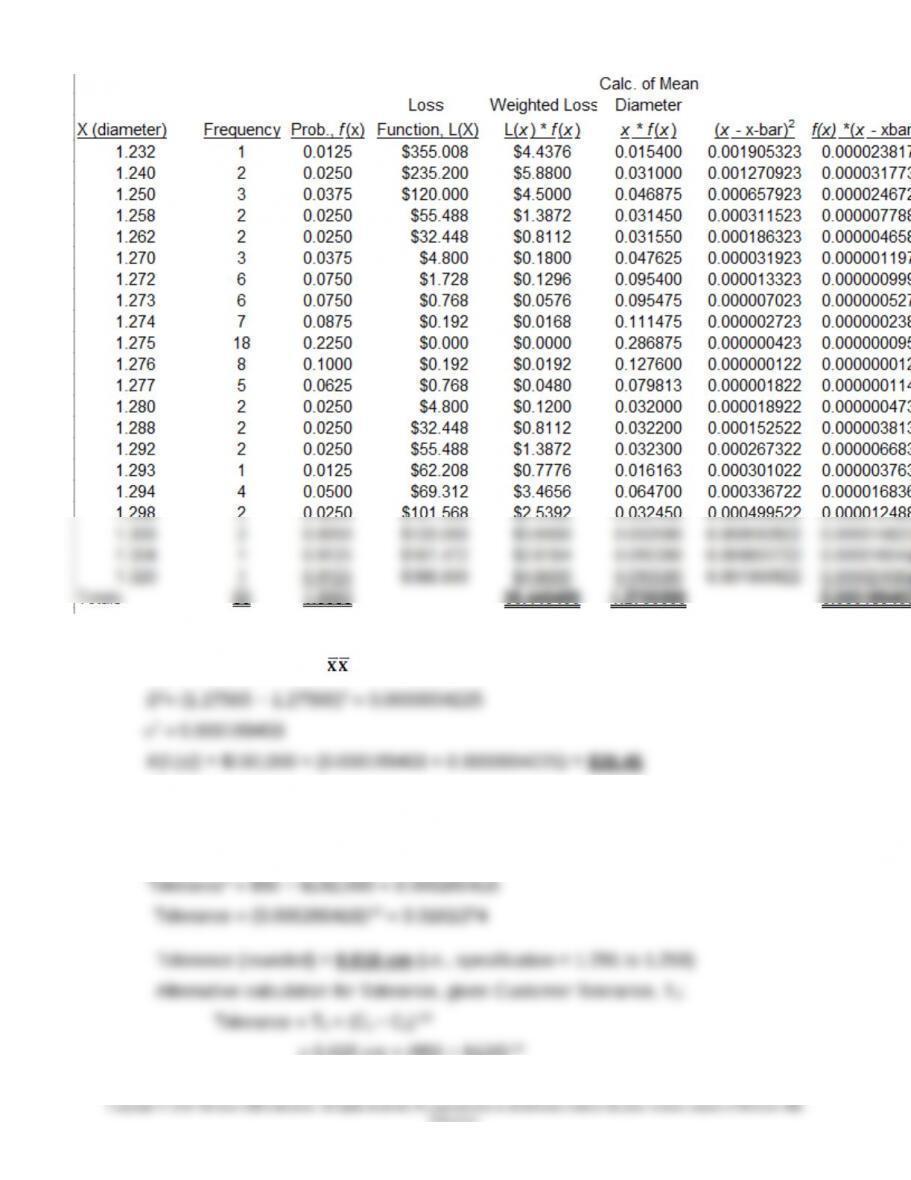

17-38 Taguchi Loss Function Analysis; Spreadsheet Application (50 Minutes)

1. k = Total quality cost ÷ (Tolerance allowed)2 = ($50 + $70) ÷ (0.025)2 = $192,000

17-13

Chapter 17 – The Management and Control of Quality

17-38 (Continued)

Mean actual diameter, = 1.2756500

2. Allowed diameter tolerance:

Repair Cost = k × (Tolerance) 2

$50 = $192,000 × (Tolerance)2

= 0.025 cm × ($50 ÷ $120)1/2

17-15

Education.

Chapter 17 – The Management and Control of Quality

= 0.025 cm × 0.645497 = 0.016 cm (rounded)

Note: An Excel spreadsheet solution file for this Problem is embedded in this document.

You can open the spreadsheet “object” that follows by doing the following:

1. Right click anywhere in the worksheet area below.

2. Select “worksheet object” and then select “Open.”

3. To return to the Word document, select “File” and then “Close and return to…”

while you are in the spreadsheet mode. The screen should then return you to the

Word document.

Ex. 17-38 7e.xlsx

Chapter 17 – The Management and Control of Quality

17-39 Six-Sigma Interpretation; Spreadsheet Application (20 minutes)

Sigma One-Tailed Two-Tailed Errors (Defects)

Level Area 1

Area Per Million

1 0.158655254 0.317310508 317,310.51

1Excel formula: = 1 − NORMSDIST(n), where n = sigma level (1, 2, …)

The preceding data indicate suggest a common misconception regarding the quality

level assumed under Six Sigma. Only when a defect is defined as any deviation from

the targeted level of the attribute (i.e., only when the “tolerance” is zero) will the

above approach represent the maximum number of defects per million opportunities

for error. Note, for example, that the expected number of errors (defects) under Six

Sigma is approximately 2 per billion (when any deviation from target is considered a

defect).

In actual practice, based on initial experience by Motorola, the application of Six

Sigma allows some variation (drift) around the target value. That is, there is an

assumption that no process can be maintained in perfect control (i.e., no “drift” at

all). Thus, in practice, a drift of 1.5 standard deviations around the target value is

“allowed.” Any deviation beyond this allowable “drift” would be considered a defect or

out-of-control process.

What this means is that a revised formula is needed to calculate the defects per

million as the Six-Sigma methodology is applied in practice. According to Pyxdek

(http://www.qualitydigest.com/may01/html/sixsigma.html) the Excel formula (under

the assumption of an allowable drift of 1.5 sigma) is: 1000000*(1 − NORMSDIST(Z-

1.5)), where 1.5 = allowable drift (in standard deviations) and Z = Sigma level. For Z

= 6.0, the Excel formula returns: 3.398, the defect-per-million figure commonly, but

perhaps mistakenly, reported in the literature. (Also see, J. R. Evans and W. M.

Lindsay, The Management and Control of Quality, 6th ed. (South-Western, 2005),

Chapter 10.)

17-17

Education.

Chapter 17 – The Management and Control of Quality

17-40 Management Accounting’s Role in Six-Sigma (25 Minutes)

At the most general level, the management accountant (because of expertise in the

measurement process) should be included as a member of the cross-functional Six–

Sigma project team whose responsibility it is to focus on a particular business

process, improve that process, and then move on to another project. The role of the

management accountant on the project team can perhaps best be described within

the context of the five phases of the DMAIC approach to process improvement:

Define, Measure, Analyze, Improve, and Control.

In the define phase, management accountants, because they are in the best

position to observe and document waste and excessive costs, can help identify

opportunities that warrant Six–Sigma-type projects. As a follow-up, management

accountants can help in the project selection process by providing reliable data

regarding estimated costs (e.g., required resources degree of difficulty, chance of

success) and benefits (e.g., cost savings, customer impact, expected time for project

completion) associated with alternative projects under review. In other words, they

the project helps define and measure the factors that have the most influence on

process performance.

actually occur.

Finally, in the control phase, the management accountant can help in the

development of control tools such as audits and check sheets that can be used to

ensure sustainability of the process improvements implemented in the preceding

stage.

Source: F. Rudisill and D. Clary, “The Management Accountant’s Role in Six Sigma,”

Strategic Finance (November 2004), pp. 35-39.

17-18

Education.

Chapter 17 – The Management and Control of Quality

17-41 Applying Six–Sigma Principles to the Accounting Function (30 Minutes)

Perhaps the most fundamental step in the project is selection of an appropriate

cross-functional team, including a project champion (in this case, it was the CFO of

the organization) and a project leader (usually either a Green Belt or Black Belt).

One framework for the project management process is DMAIC (Design, Measure,

Analyze, Improve, and Control). In the present example, the DMAIC phases

consisted of the following stages:

The Define Stage—the project team developed a statement of the problem (“Too

many hours are being spent preparing quarter-end financial statements.”) and a

goals statement (“Reduce direct hours worked for 18 schedules from over 100 hours

to 26 hours.”). The latter was determined in consultation with the person primarily

schedules, 28 hours. Thus, the overall cycle-time reduction goal was approximately

84 hours!

The Analyze Stage—in this stage, the team created a “fish-bone” (i.e., “cause-and-

effect”) diagram to identify possible root causes of the excessive cycle time for

quarterly closings. Four primary causes were identified: (1) a high number of hours

were spent on the balance sheet schedules, (2) the E-Trans submissions were

compiled a list of actions that addressed the causes of the potential failure modes.

Implementing these actions resulted in substantial process improvements: in the first

quarter alone, the total cycle time of the process was reduced to 32 hours, slightly

above the 26-hour goal.

17-19

Education.

Chapter 17 – The Management and Control of Quality

17-41 (Continued)

The Control Stage—in a sense, the most important control-related decision

17-20

Education.

Chapter 17 – The Management and Control of Quality

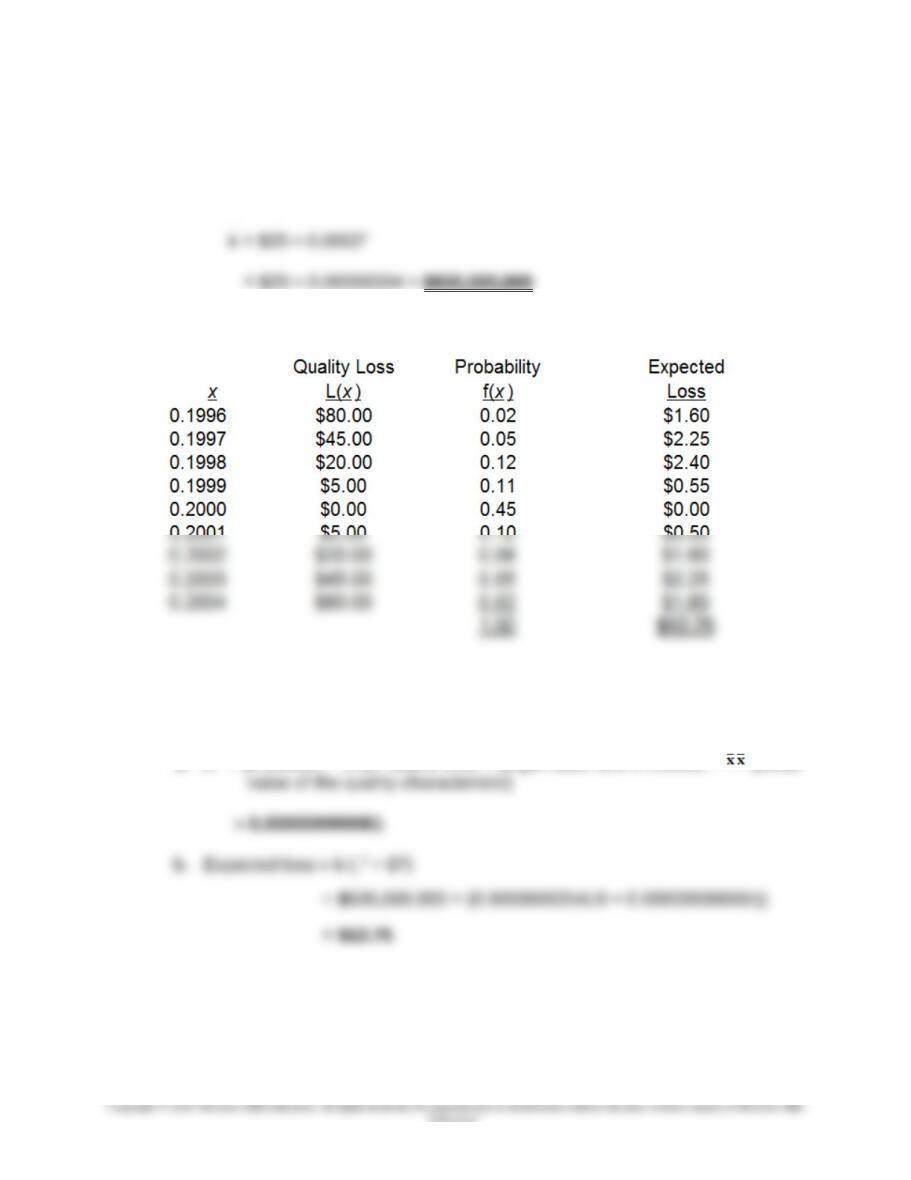

17-42 Taguchi Loss Function Analysis (50 Minutes)

1. Value of k, the cost coefficient, in the Taguchi Loss Function, L(x):

L(x) = k(x − T)2

2a & b. Expected Loss Using Taguchi Loss Function:

3. Expected Loss Using Variance Data (see table below), per Albrecht and Roth, “The

Measurement of Quality Costs: An Alternative Paradigm,” Accounting Horizons

(June 1992), pp. 15–27:

a. D2 = (0.199991 − 0.2)2, where 0.20 = target value and 0.199991 = (mean

17-21

Education.