11-39 (continued-2)

and long-term pricing strategy to make sure it is consistent with

long-term strategy with established profit targets.

Hillside should evaluate the effectiveness of its advertising and

promotional efforts. Are the targeted customers being reached?

An unintended effect of the sales contests is that certain retail

customers might buy unusually large orders, at the urging of

11-40 Profitability Analysis; Pro Forma Income Statement (60-75 min)

1. The dollar value of DimLok’s present annual fixed costs is calculated

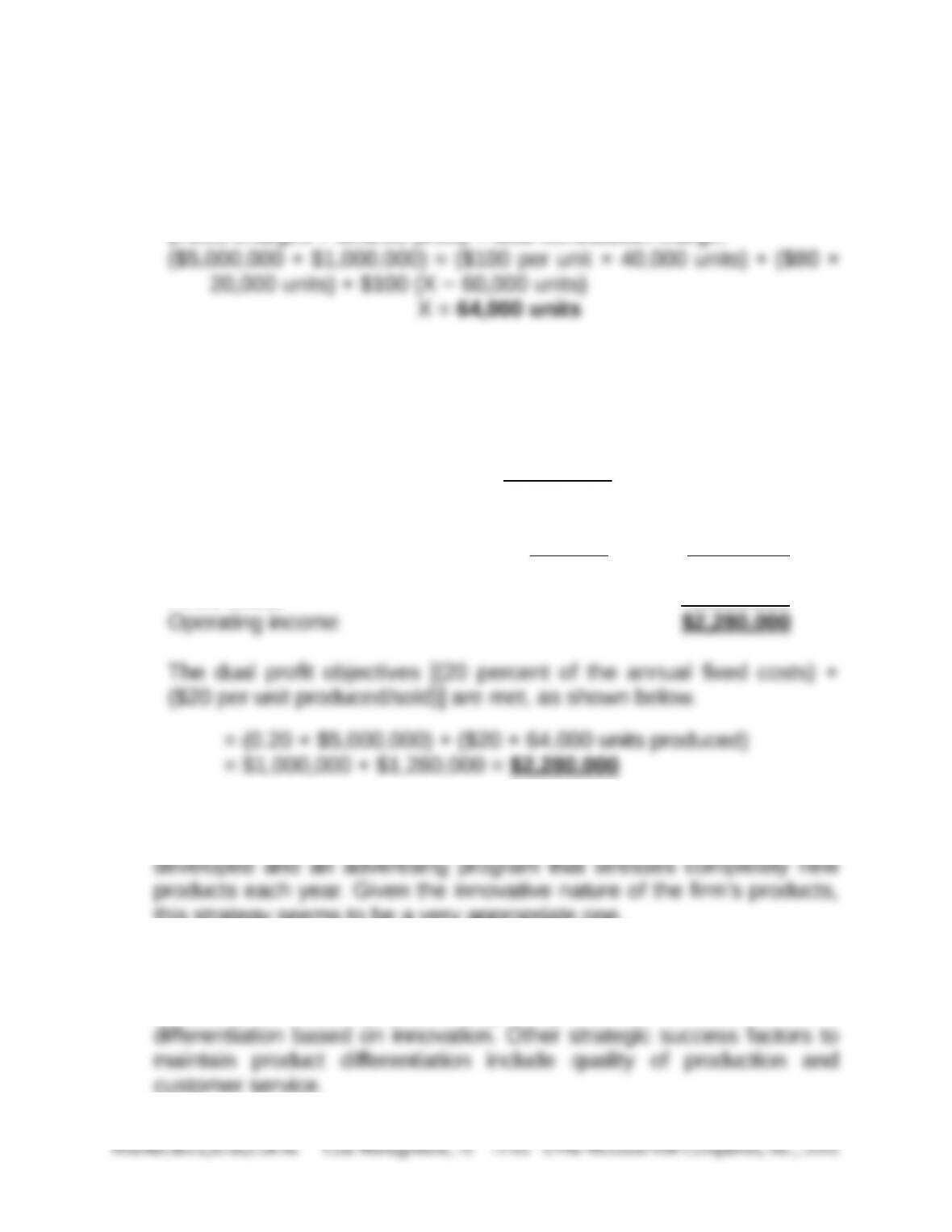

2. DimLok must sell 64,000 units in order to achieve both profit

objectives of 20 percent return on fixed costs and $20 per unit sold.

Supporting Calculations

First: The solution must consider the following constraints:

40,000 unit capacity for the current facility.

Second: The calculation of profit with the current facility at the

capacity level of 40,000 units will not meet the profit objectives, as

demonstrated by the following calculations:

Contribution margin per unit below the 40,001 unit level

= $200 selling price per unit − ($80 variable cost per unit + $20

Note: 48,000 units exceeds current capacity (40,000 units) by

8,000 units.

11-40 (continued-1)

Third: Thus, in order to achieve the profit targets, DimLok must

increase plant capacity, thus incurring an additional $1,000,000 in

fixed costs. This, in turn, increases the profit target based on fixed

costs to a total of $1,000,000 (i.e., 0.20 × [$4,000,000 + $1,000,000]),

as follows:

The per-unit contribution margin for production in the 40,001 to

60,000 units range, with the selling price reduced to $180 per unit, is

$80, as follows:

65,000 units exceeds the 60,000-unit critical level

(supplier’s contract); variable costs are reduced by

$20 per unit for production in excess of 60,000 units.

Fourth: The contribution margin per unit for production in the 60,000

to 80,000 unit range, with the variable cost per unit reduced to $60

per unit, is determined as follows:

11-40 (continued-2)

Finally, the calculation of the number of units (X) needed to achieve

overall profit objectives

(Fixed charges + desired profit) = total contribution margin

3. DimLok Division

Pro Forma Income Statement

Revenue

40,000 units × $200/unit = $8,000,000

24,000 units × $180/unit = 4,320,000 $12,320,000

Variable costs

60,000 units × $80/unit = 4,800,000

4,000 units × $60/unit = 240,000 5,040,000

Contribution Margin 7,280,000

Fixed Costs 5,000,000

4. DimLok has a competitive strategy based on differentiation. The

differentiation is based on the secret process that DimLok has

this strategy seems to be a very appropriate one.

5. Critical success factors for DimLok include research and development

(R&D) to maintain the technological advantage of their unique

products, and strong advertising programs to stress the firm’s

11-41 Product-Profitability Analysis, Scarce Resources (60 min)

1. Fixed manufacturing overhead costs, in total, are by definition

capacity-related costs and as such are not expected to change in the

short run. Thus, in total, short-term fixed costs should be independent

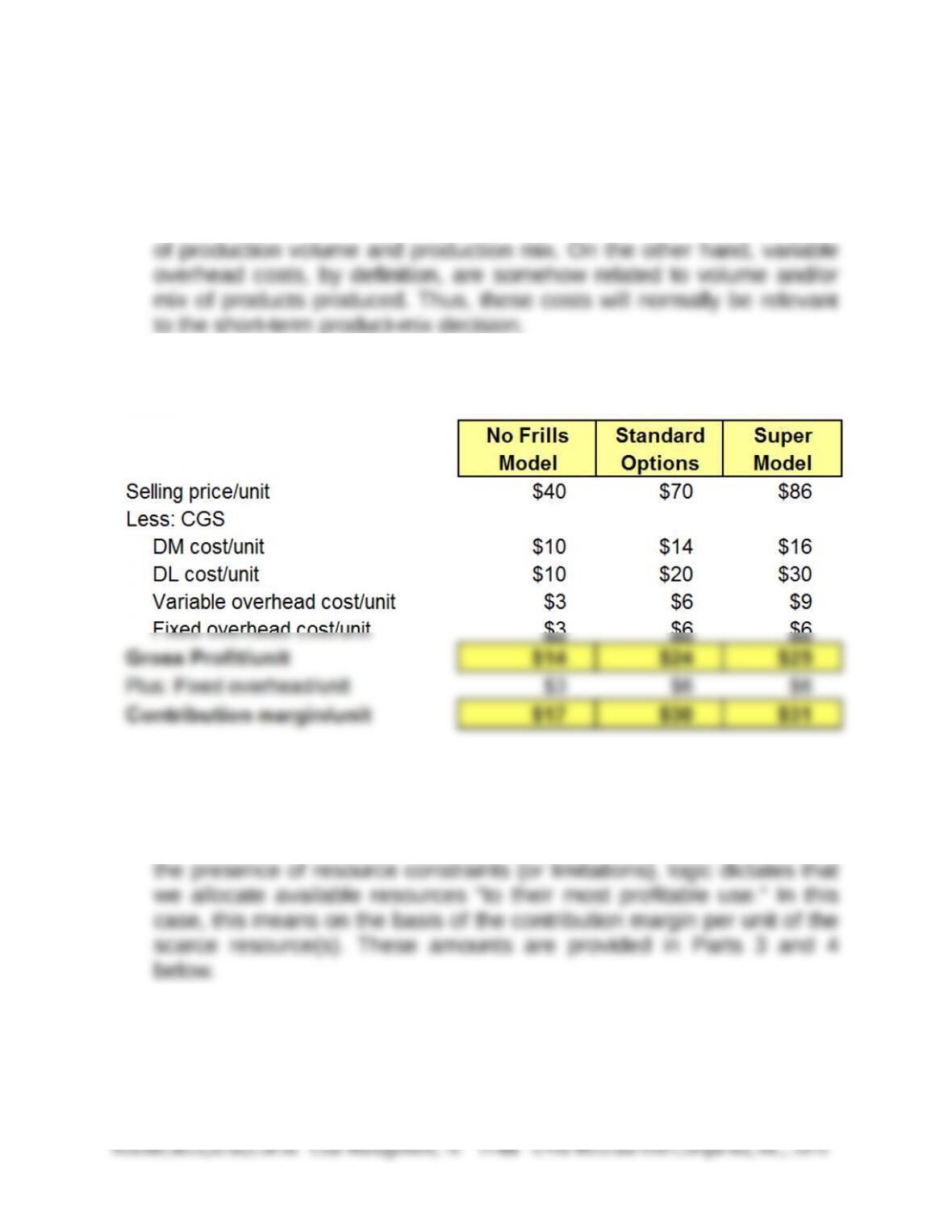

2. Gross profit per unit and contribution margin per-unit figures:

Neither of the above profit figures is useful in terms of determining the

optimum short-term product mix. In the absence of production

constraints, and assuming all per-unit contribution margins are

positive, we should produce each product up to its level of demand. In

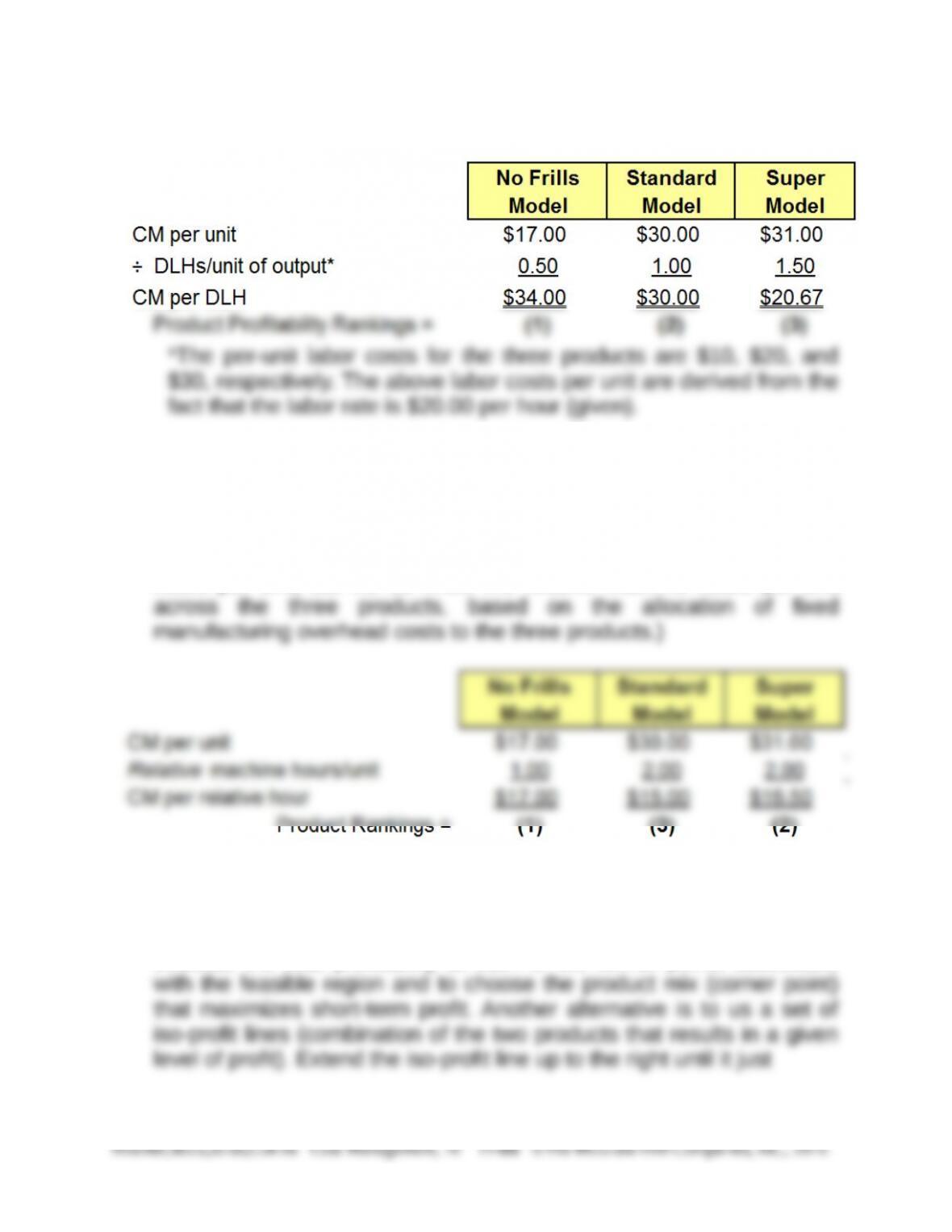

3. In the presence of a single resource constraint, we should focus on

those products that provide the greatest contribution margin per unit of

the scare resource, in this situation, labor time. The calculations follow.

11-41 (Continued-1)

4. If machine hours represent the scarce resource, then the allocation of

machine hours to products should be based on the contribution margin

per machine hour. As seen from the calculations below, the product

profitability rankings differ from those determined in Part 3 above.

(Note that in the present case we do not know the actual machine

hours per unit, but we do know the relative machine hours per unit

5. If there are only two products (and one or more constraints), we could

solve the product-mix problem using the graphical approach presented

in the chapter (see Exhibits 11.19 and 11.21). One alternative is to

evaluate the total profitability at each of the corner points associated

11-41 (Continued-2)

touches a point in the feasible set (region): this point (mix of the two

products) defines the optimum product mix.

6. In the case where there are more than two products (and one or more

constraints), the graphical approach is not practical. In this case, the

7. The primary role of the management accountant in terms of short-term

profit planning is to generate accurate estimates of the contribution

margins for each product (or service). Whether a simple or a complex

11-42 (Also Problem 9-50): CVP Analysis; Sustainability; Uncertainty;

Decision Tables (75-90 min)

1. Lifetime cost functions: let Y = lifetime cost, and v = cost per gallon of

gas

Regular model:

Lifetime Cost (Y) = Fixed Cost + Variable Cost

2. Breakeven gas price (point of cost indifference): let “v” = breakeven price

per gallon

Lifetime Cost–Gas Model = Lifetime Cost–Hybrid Model

$17,000 + (2,608.7 gals. × v) = $18,500 + (2,222.2 gals. × v)

3. Graph of Lifetime Cost Function–Regular and Hybrid Models

X (price Lifetime Cost

per gal.) Gas Model Hybrid

$2.750 $24,174 $24,611

$3.000 $24,826 $25,167