Chapter 09 – Short-Term Profit Planning: Cost-Volume-Profit (CVP) Analysis

9-37 (Continued-1)

4. BE units = F ÷ contribution margin per unit

= ($500,000 + $160,000) ÷ ($80.00 − $41.50)/unit

= $660,000 ÷ $38.50/unit = 17,143 units

πB= Sales − variable costs − fixed costs

= [Q × (unit contribution margin)] − F

5. A key strategic issue is that Hank’s sales staff is a critical success

factor for the business, especially in the growing and competitive

environment of Hank’s business. His knowledgeable and courteous

staff help to bring in and retain customers. If the salary/commissions

plan would alienate his sales staff, the plan could be a big mistake.

Finally, there is the issue of operating risk associated with moving to

a cost structure characterized by relatively higher fixed costs (traded-

off against lower variable costs).

Possible benefits:

oIf variable costs (such as variable labor costs) are high, this

9-30

Education.

Chapter 09 – Short-Term Profit Planning: Cost-Volume-Profit (CVP) Analysis

9-37 (Continued-2)

Possible costs/disadvantages:

oIncreased operating (business) risk (e.g., generally

speaking, there will be a higher breakeven point)

oIf sales volume recedes, these reductions are magnified in

costs can dramatically increase operating risk.

oIncreased fixed costs (e.g., those associated with insourcing)

may expose the company to increased risk or exposure to

production slow-downs or stoppages, as experienced in

2011 in Japan as a consequence of the earthquake/tsunami

that hit the country).

There are two additional points worth making:

1. Ultimately, the decision to increase operating leverage is affected

by some of the following considerations: year-to-year fluctuations in

sales—that is, uncertainty (the greater the uncertainty, the greater the

attractiveness of lower operating leverage, due to the increased

2. Without knowing the future, it is impossible to specify which of the

two strategies (cost structures) is more desirable.

9-31

Chapter 09 – Short-Term Profit Planning: Cost-Volume-Profit (CVP) Analysis

9-38 Profit Planning: Multiple Products (50-60 min)

1. Break-even in units: weighted-average contribution margin approach

a. Overall breakeven point = F ÷ weighted-average contribution

margin/unit

Weighted-average unit contribution per unit

b. Breakdown of breakeven units:

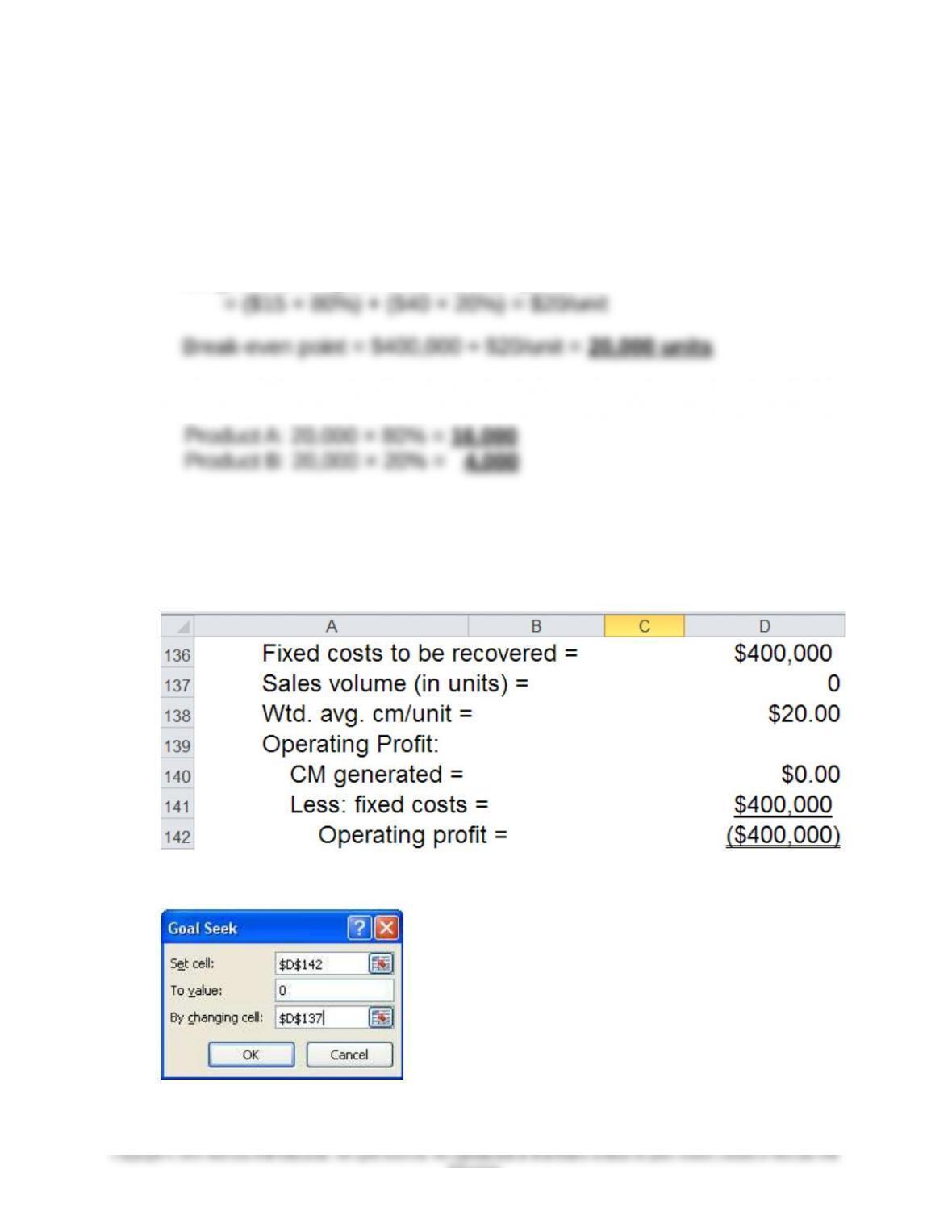

2. Use Goal Seek (in Excel) to calculate the breakeven point, in terms of

total units:

Step One: Set Up the Equation for Operating Income

Step Two: Run Goal Seek

9-32

Education.

Chapter 09 – Short-Term Profit Planning: Cost-Volume-Profit (CVP) Analysis

9-38 (Continued-1)

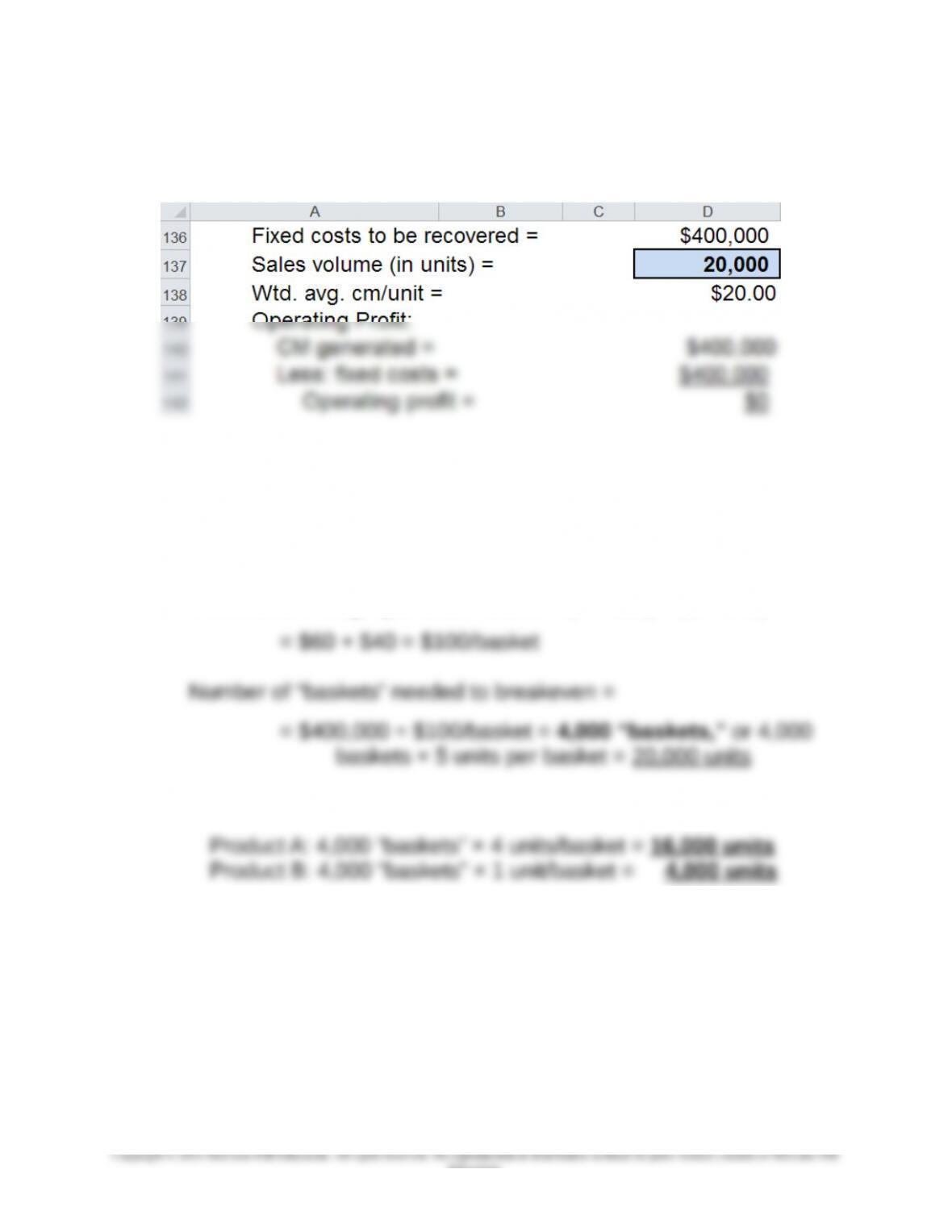

Step Three: Results (after running Goal Seek)

3. Breakeven point in units: “Sales basket” approach (assume that each

basket consists of 4 units of Product A and 1 unit of Product B).

a. Overall breakeven point (in baskets) = F ÷ contribution

margin/basket

Contribution margin per sales basket = (4 × $15) + (1 × $40)

b. Breakdown of breakeven units:

4. Distribution of breakeven point in terms of sales dollars (based on

weighted-average contribution margin ratio, where the individual

product weights are based on relative sales dollars, not physical unit,

of each product in the standard sales mix).

a. Breakeven ($) = F ÷ weighted-average cm ratio

Relative sales dollars (not units), based on standard sales mix:

9-33

Education.

Chapter 09 – Short-Term Profit Planning: Cost-Volume-Profit (CVP) Analysis

Problem 9-38 (Continued-2)

Product A: 18,000 units × $80/unit = $1,440,000

Product B: 4,500 units × $140/unit = $630,000

Weights:

Product A: $1,440,000 ÷ $2,070,000 = 0.6956522

Weighted-average contribution margin ratio:

A: 0.69565 × ($15/$80) = 0.6956522 × 0.1875 = 0.13043479

Breakeven point in overall dollars ($) = F ÷ wtd. avg. cm ratio

b. breakdown of total breakeven sales dollars, by product:

Product A: mix % × breakeven sales, in $

5. For the multiproduct firm, there is no breakeven point independent of

the sales mix assumption. For the multiproduct firm, we typically

assume that the outputs are sold in some standard mix, based either

on relative physical units or relative sales dollars. If the individual

products differ in terms of their contribution margin per unit (or

contribution margin ratio), then the weighted-average contribution

9-34

Education.

Chapter 09 – Short-Term Profit Planning: Cost-Volume-Profit (CVP) Analysis

Problem 9-38 (Continued-3)

6. Change in the breakeven point (in total units) in response to a 10%

change in fixed costs:

New level of fixed costs = $400,000 + $40,000 = $440,000

Original level of fixed costs = $400,000

Percentage change in breakeven point = 2,000 ÷ 20,000 = 10.00%

As seen from the above, the percentage change in fixed cost (here

10%) led to an identical percentage change in the breakeven point.

Because of the linear cost functions assumed in a conventional CVP

model, this finding can be generalized: with everything else held

9-35

Education.

Chapter 09 – Short-Term Profit Planning: Cost-Volume-Profit (CVP) Analysis

9-39 CVP Analysis/Profit Planning (45-60 min)

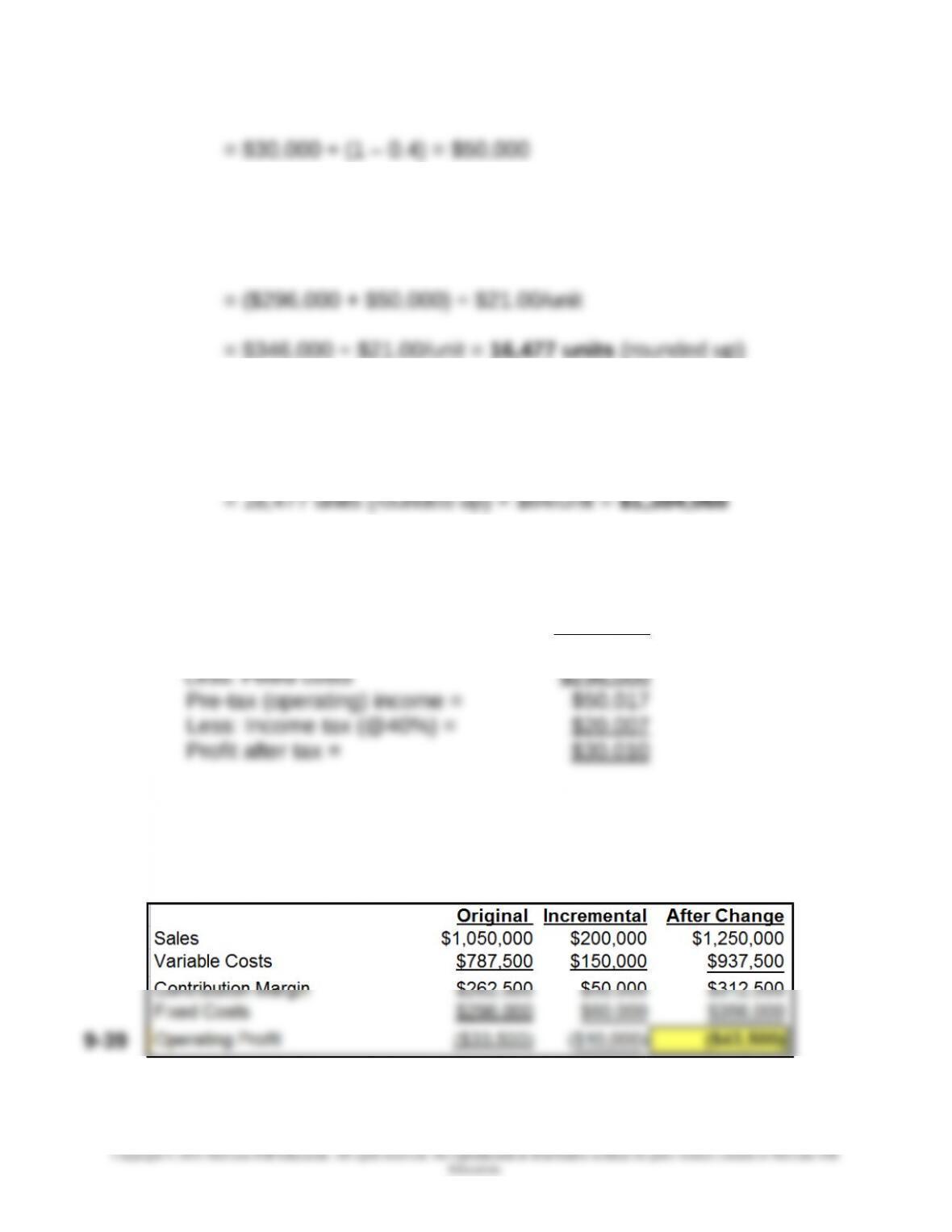

1. BE in units = F ÷ (p − v) = $296,000 ÷ ($84 − $63)/unit = 14,095.24

units (14,096 rounded up)

Contribution margin ratio = (p – v) ÷ p

rounded up)

2. Required sales, in units and in dollars, to achieve pre-tax profit goal of

$30,000:

# units = (F + πB) ÷ cm per unit = ($296,000 + $30,000) ÷ $21/unit

OR,

Required sales in $ = (F + πB) ÷ cm ratio

3. Required sales to achieve after-tax profit goal:

After-tax profit goal = $30,000

Conversion of after-tax profit goal into pre-tax dollar equivalent:

$30,000 ÷ (1 – t), where t = combined income tax rate

9-39 (Continued-1)

9-36

Education.

Chapter 09 – Short-Term Profit Planning: Cost-Volume-Profit (CVP) Analysis

Required sales (in units) to achieve after-tax profit target

= (F + targeted pre-tax profit) ÷ cm per unit

Required sales, in $, to achieve after-tax profit target

= required sales volume, in units × selling price/unit

4. Contribution income statement:

Sales (16,477 units × $84/unit) = $1,384,068

Less: Variable cost (@ $63/unit) = 1,038,051

Contribution margin (@ $21/unit) = $346,017

Note: Difference of $10 is due to rounding up in terms of the required

sales volume in units.

5. Profits will decrease by $10,000, from ($33,500) to ($43,500)

(Continued-2)

9-37

Chapter 09 – Short-Term Profit Planning: Cost-Volume-Profit (CVP) Analysis

Or,

= Increase in CM – Increase in Fixed Costs

6. Operating Profit will decrease $105,625, from a loss of $33,500 to a

loss of $139,125:

Planned reduction in selling price/unit = 10%

Estimated increase in sales volume (units) = 25%

Estimated increase in fixed costs = $40,000

7. Yes, the proposed change is desirable. The total reduction in variable

9-38

Education.

Chapter 09 – Short-Term Profit Planning: Cost-Volume-Profit (CVP) Analysis

9-40 CVP Analysis (45-50 min)

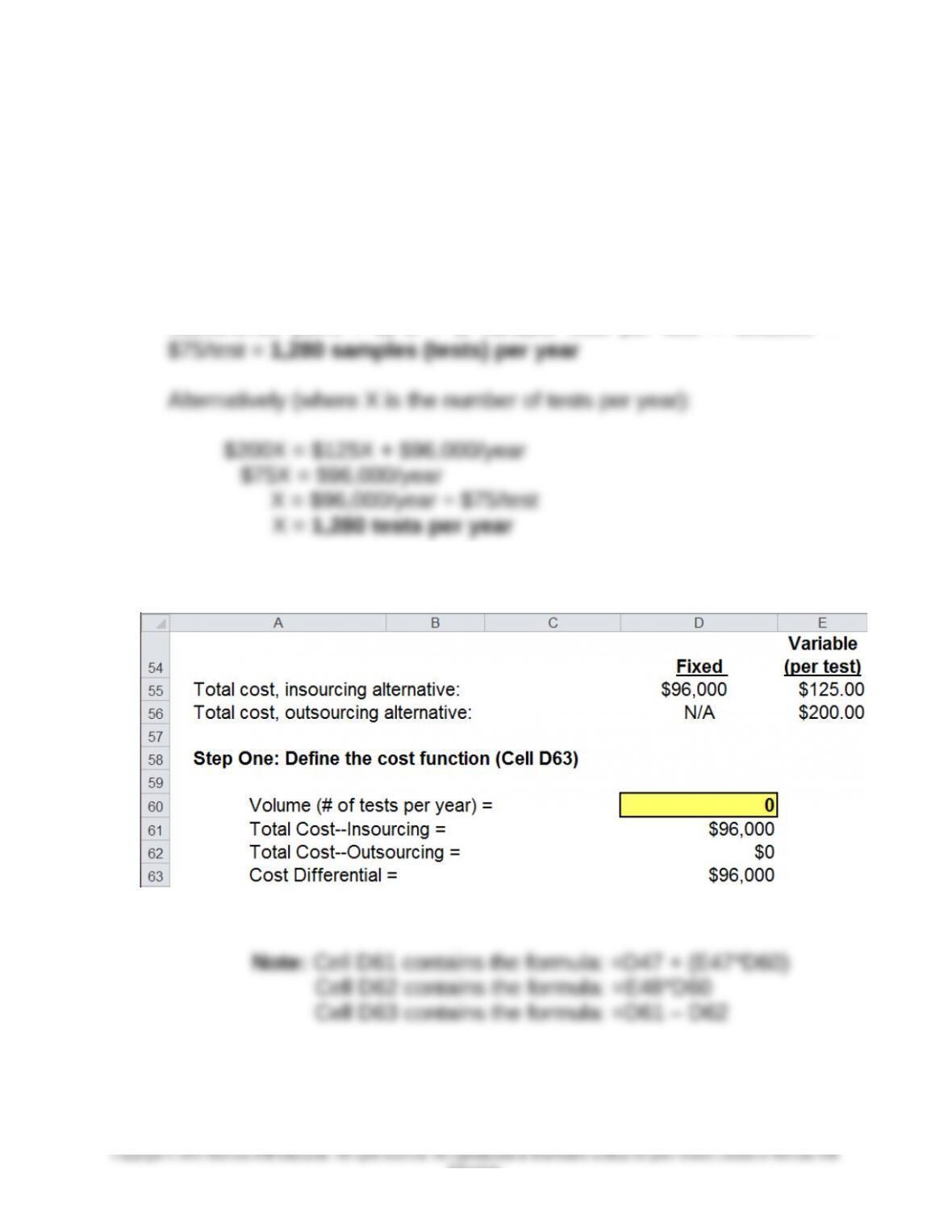

1. Pro-rated per-year fixed cost of blood gas analysis machine =

$960,000 ÷ 10 years = $96,000/year

Savings per sample in direct costs if a blood gas analysis machine is

purchased: $200 − $125 = $75/test

Indifference point = ∆FC ÷ ∆ variable cost per test = $96,000 ÷

2. Using Goal Seek to determine the indifference point:

9-39

Education.