43. Garrison Co. produces three products — X, Y, and Z — from a joint process. Each product

may be sold at the split-off point or processed further. Additional processing requires no special

facilities, and production costs of further processing are entirely variable and traceable to the

products involved. Last year all three products were processed beyond split-off. Joint production

costs for the year were $120,000. Sales values and costs needed to evaluate Garrison’s

production policy follow.

Units Sales Value at If Processed Further

Product Produced Split Off Sales Value Additional Costs

X 6,000 $40,000 $80,000 $1,200

Y 3,000 15,000 40,000 3,000

Z 1,000 16,000 30,000 1,500

The amount of joint costs allocated to product Z using the sales value at split-off method is

(calculate all ratios and percentages to 4 decimal places, for example 33.3333%, and round all

dollar amounts to the nearest whole dollar):

44. Garrison Co. produces three products — X, Y, and Z — from a joint process. Each product

may be sold at the split-off point or processed further. Additional processing requires no special

facilities, and production costs of further processing are entirely variable and traceable to the

products involved. Last year all three products were processed beyond split-off. Joint production

costs for the year were $120,000. Sales values and costs needed to evaluate Garrison’s

production policy follow.

Units Sales Value at If Processed Further

Product Produced Split Off Sales Value Additional Costs

X 6,000 $40,000 $80,000 $1,200

Y 3,000 15,000 40,000 3,000

Z 1,000 16,000 30,000 1,500

The amount of joint costs allocated to product X using the net realizable value method is

(calculate all ratios and percentages to 4 decimal places, for example 33.3333%, and round all

dollar amounts to the nearest whole dollar):

45. Garrison Co. produces three products — X, Y, and Z — from a joint process. Each product

may be sold at the split-off point or processed further. Additional processing requires no special

facilities, and production costs of further processing are entirely variable and traceable to the

products involved. Last year all three products were processed beyond split-off. Joint production

costs for the year were $120,000. Sales values and costs needed to evaluate Garrison’s

production policy follow.

Units Sales Value at If Processed Further

Product Produced Split Off Sales Value Additional Costs

X 6,000 $40,000 $80,000 $1,200

Y 3,000 15,000 40,000 3,000

Z 1,000 16,000 30,000 1,500

The amount of joint costs allocated to product Y using the net realizable value method is

(calculate all ratios and percentages to 4 decimal places, for example 33.3333%, and round all

dollar amounts to the nearest whole dollar):

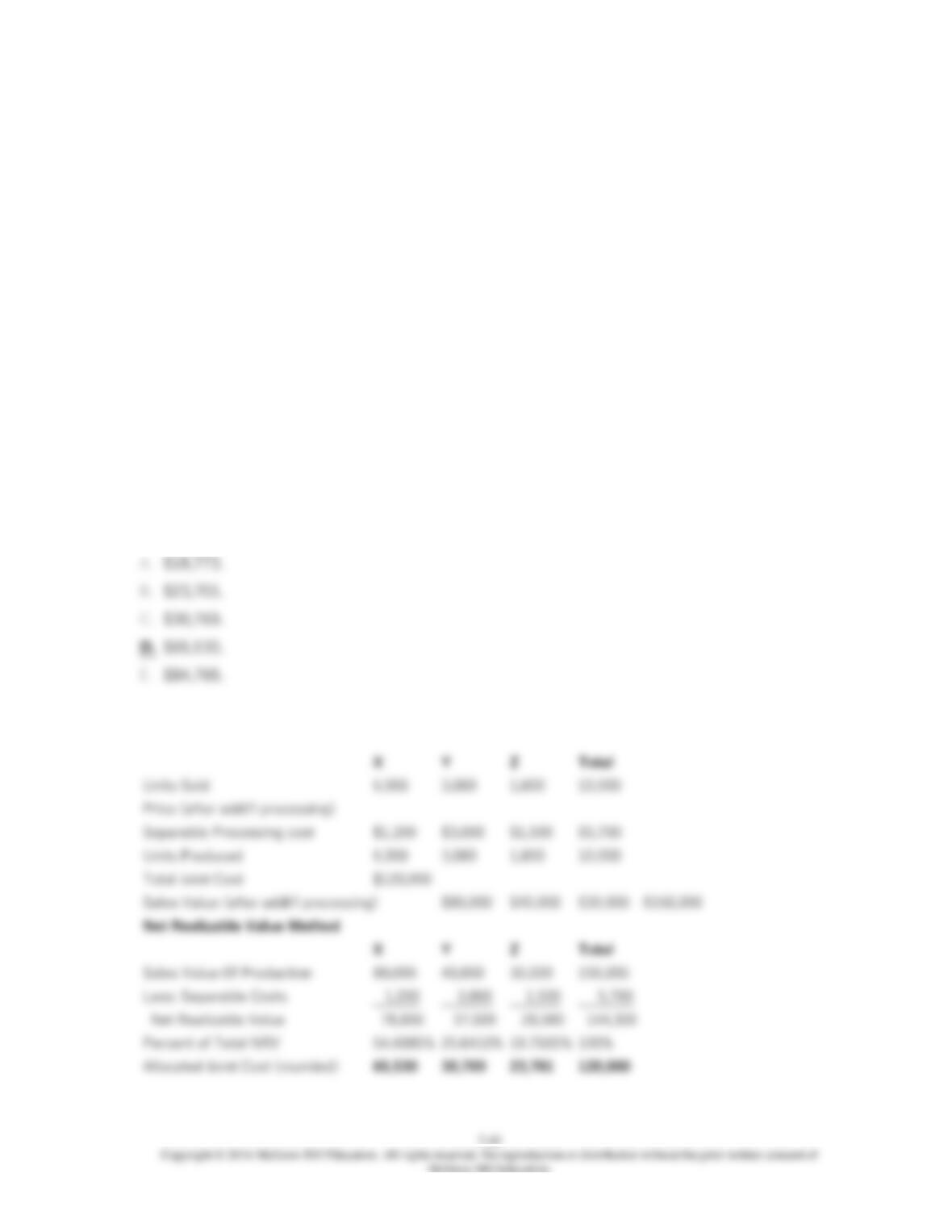

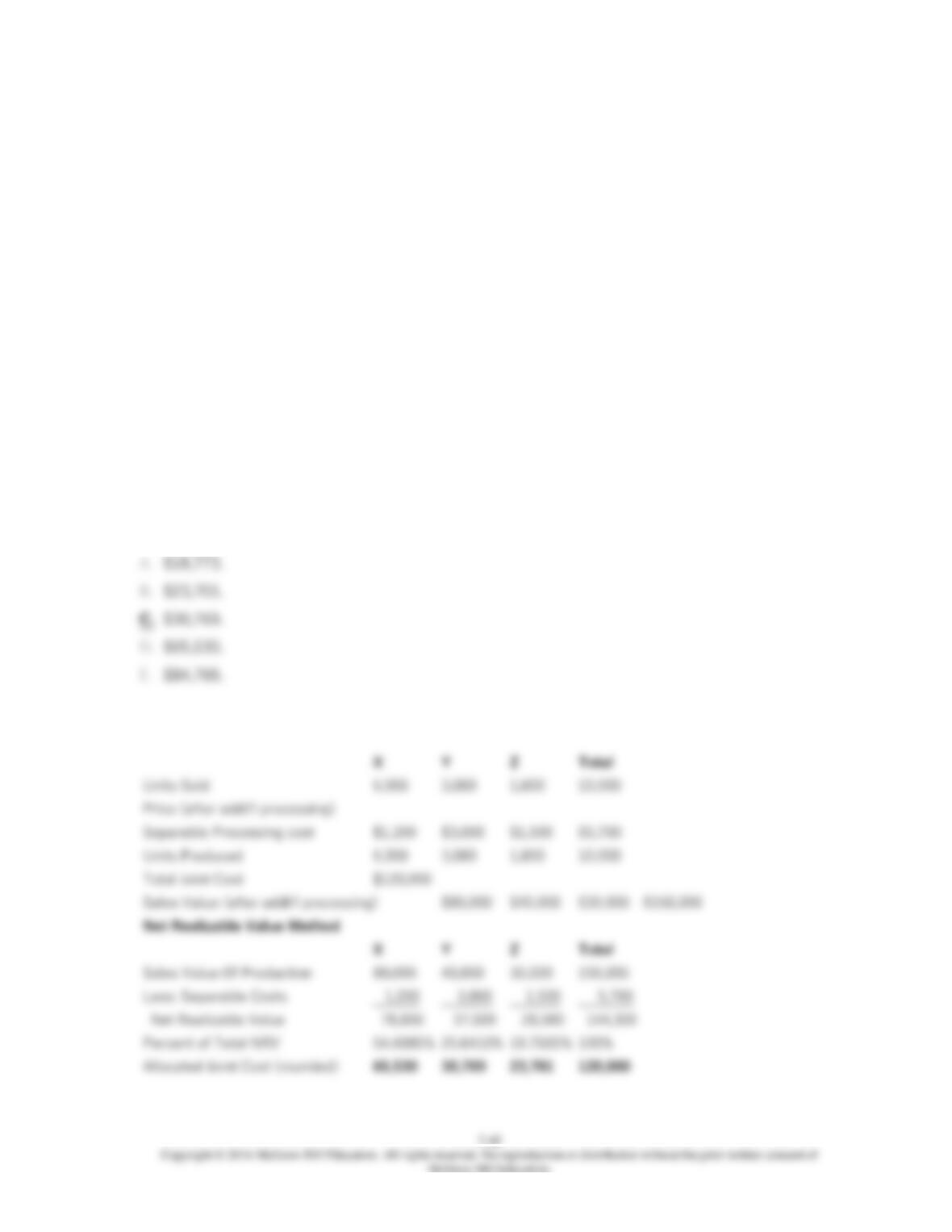

46. Garrison Co. produces three products — X, Y, and Z — from a joint process. Each product

may be sold at the split-off point or processed further. Additional processing requires no special

facilities, and production costs of further processing are entirely variable and traceable to the

products involved. Last year all three products were processed beyond split-off. Joint production

costs for the year were $120,000. Sales values and costs needed to evaluate Garrison’s

production policy follow.

Units Sales Value at If Processed Further

Product Produced Split Off Sales Value Additional Costs

X 6,000 $40,000 $80,000 $1,200

Y 3,000 15,000 40,000 3,000

Z 1,000 16,000 30,000 1,500

The amount of joint costs allocated to product Z using the net realizable value method is

(calculate all ratios and percentages to 4 decimal places, for example 33.3333%, and round all

dollar amounts to the nearest whole dollar):

47. Which of the following statements best describes a by-product?

48. For the purposes of cost accumulation, which of the following are identifiable as different

individual products before the split-off point?

By-products Joint products

A) No No

B) Yes No

C) Yes Yes

D) No Yes

49. Relative sales value at split-off is used to allocate:

Cost Beyond

Split-Off Joint Costs

A) Yes Yes

B) Yes No

C) No No

D) No Yes

50. Which of the following is not one of the objectives of cost allocation?

51. The cost allocation method most widely used because of its accuracy and ability to

provide a detailed level of analysis is:

52. The departmental approach of cost allocation recognizes that the typical manufacturing

operation involves which type(s) of departments?

53. Place the following phases of the departmental approach in the correct order.

1. Allocate the production department costs to products.

2. Allocate service costs to the overhead costs.

3. Allocate the service department costs to the production department.

4. Trace all direct costs and allocate overhead costs to both the service and production

departments.

54. Which of the following is an example of a physical measure used in the physical measure

method?

55. Which is not a common method used to allocate costs under the departmental

approach?

56. A key disincentive effect of departmental cost allocation can occur when:

57. Net Realizable Value (NRV) of a product is:

58. By-product costing approaches include:

59. Johns Company manufactures products R, S, and T from a joint process. The following

information is available:

Product

R S T Total

Units produced 12,000 ? ? 24,000

Sales value at split-off ? ? $50,000 $200,000

Joint costs $48,000 ? ? $120,000

Sales value if processed further $110,000 $90,000 $60,000 $260,000

Additional costs if processed further $18,000 $14,000 $10,000 $42,000

Assuming that joint product costs are allocated using the relative–sales-value at split-off

approach, what was the sales value at split-off for products R and S?

Product R Product S

A) $55,000 $75,000

B) $63,000 $81,000

C) $80,000 $70,000

D) $91,000 $83,000

E) $101,000 $92,000

60. The Long Term Care Plus Company has two service departments — actuarial and

premium rating, and two operations departments — marketing and sales. The distribution of each

service department’s efforts to the other departments is shown below:

FROM TO

Actuarial Rating Marketing Sales

Actuarial 0% 40% 20% 40%

Rating 25% 0% 37.5% 37.5%

The direct operating costs of the departments (including both variable and fixed costs) were as

follows:

Actuarial $60,000

Premium Rating $40,000

Marketing $60,000

Sales $70,000

The total cost accumulated in the marketing department using the direct method is (calculate all

ratios and percentages to 2 decimal places, for example 33.33%, and round all dollar amounts to

the nearest whole dollar):

61. The Long Term Care Plus Company has two service departments — actuarial and

premium rating, and two operations departments — marketing and sales. The distribution of each

service department’s efforts to the other departments is shown below:

FROM TO

Actuarial Rating Marketing Sales

Actuarial 0% 40% 20% 40%

Rating 25% 0% 37.5% 37.5%

The direct operating costs of the departments (including both variable and fixed costs) were as

follows:

Actuarial $60,000

Premium Rating $40,000

Marketing $60,000

Sales $70,000

The total cost accumulated in the sales department using the direct method is (calculate all

ratios and percentages to 2 decimal places, for example 33.33%, and round all dollar amounts to

the nearest whole dollar):

62. The Long Term Care Plus Company has two service departments — actuarial and

premium rating, and two operations departments — marketing and sales. The distribution of each

service department’s efforts to the other departments is shown below:

FROM TO

Actuarial Rating Marketing Sales

Actuarial 0% 40% 20% 40%

Rating 25% 0% 37.5% 37.5%

The direct operating costs of the departments (including both variable and fixed costs) were as

follows:

Actuarial $60,000

Premium Rating $40,000

Marketing $60,000

Sales $70,000

The total cost accumulated in the marketing department using the step method is (calculate all

ratios and percentages to 4 decimal places, for example 33.3333%, and round all dollar amounts

to the nearest whole dollar; assume the actuarial department goes first):