Chapter 14 – Operational Performance Measurement: Sales, Direct-Cost Variances, and the Role of Nonfinancial

Performance Measures

14-37 Standard Costing and Journal Entries (40 minutes)

1. Materials Inventory (6,000 gals. × $10.00/gal.) 60,000

Materials Purchase-Price Variance 2,700

2. WIP Inventory (2,500 × 2 gals. × $10/gal.) 50,000

Materials Usage Variance (100 gals. × $10/gal.) 1,000

3. WIP Inventory (2,500 units × 2 hrs./unit × $25/hr.) 125,000

Labor Rate Variance ($5.50/hr. × 4,900 hrs.) 26,950

4. Finished Goods Inventory ($70/unit × 2,500 units) 175,000

5. CGS ($70/unit × 2,000 units) 140,000

6. Accounts Receivable ($150/unit × 2,000 units) 300,000

Sales Revenue 300,000

To record sales revenue and associated accounts receivable for the period.

Chapter 14 – Operational Performance Measurement: Sales, Direct-Cost Variances, and the Role of Nonfinancial

Performance Measures

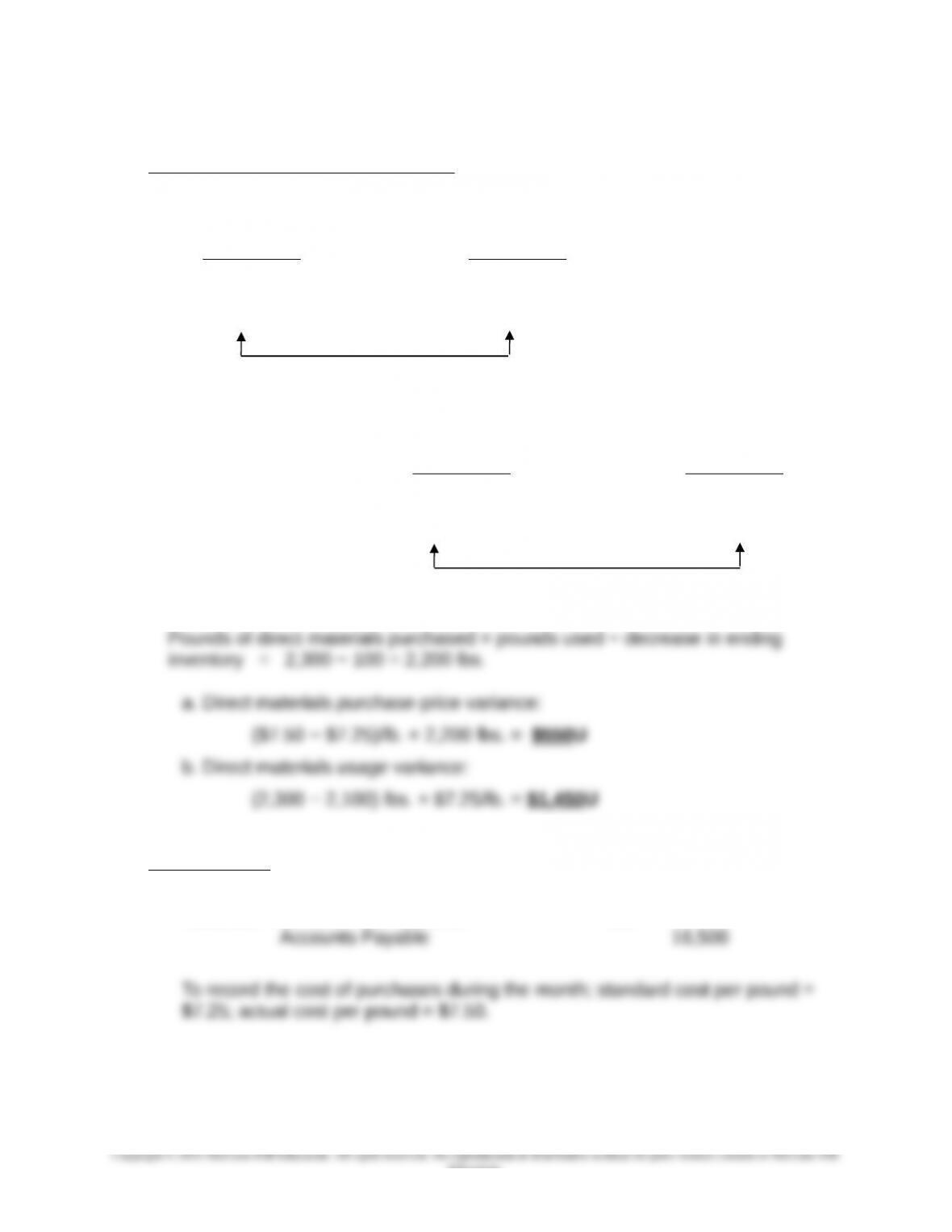

14-38 Direct Materials Variances—Journal Entries (30 minutes)

1. Determination of variances for March:

Actual Purchases Actual Purchases

at Actual Cost at Standard Cost

(AQ) × (AP) (AQ) × (SP)

(AQ) × $7.50/lb. (AQ) × $7.25/lb.

= ? = ?

Purchase-Price Variance = ?

Actual Usage at Flexible-Budget

Standard Cost Amount

(AQ) × (SP) (SQ) × (SP)

2,300 lbs. × $7.25/lb. 2,100 lbs. × $7.25/lb.

= $16,675 = $15,225

Usage Variance = ?

2. Journal entries:

Materials Inventory 15,950

Materials Purchase-Price Variance 550

14-32

Education.

Chapter 14 – Operational Performance Measurement: Sales, Direct-Cost Variances, and the Role of Nonfinancial

Performance Measures

14-38 (Continued)

WIP Inventory 15,225

Materials Usage Variance 1,450

To record the standard direct materials cost for this period’s production.

14-33

Education.

Chapter 14 – Operational Performance Measurement: Sales, Direct-Cost Variances, and the Role of Nonfinancial

Performance Measures

14-39 Financial versus Nonfinancial Performance Indicators for Operational Control

(15 minutes)

Repetitive operations, such as consumption of power (or direct materials) in an

automated manufacturing facility, require constant feedback and data to ensure that

the underlying process is “in control.” That is, the managers of such operations

cannot wait for financial reports in order to correct (put back into control) a

malfunctioning process. In this context, real-time nonfinancial performance indicators

On the other hand, managers are likely to be more interested in financial operating

results, for several reasons. One, the performance of managers is often judged on

the basis of financial results. Two, financial metrics provide decision-makers with a

common unit that can be used to evaluate the economic effects of different courses

14-34

Chapter 14 – Operational Performance Measurement: Sales, Direct-Cost Variances, and the Role of Nonfinancial

Performance Measures

14-40 Behavioral Considerations (40-45 minutes)

1. Managerial time can be considered a scare resource. Time spent in terms of

securing operational control detracts from time spent dealing with issues of a more

strategic (or long-term) nature. For this reason, many managers embrace a

managerial philosophy known as “management by exception.” When variances

(e.g., labor cost variances) are considered immaterial, no intervention on the part

of management is required: the underlying system is considered to be “in control.”

2. A standard cost system can have a negative impact on worker motivation if the

standards are too “loose” (i.e., too easily attainable) or too “tight” (i.e., too difficult

to attain). In the former case, the standards tend to reduce productivity; in the latter

case, in the extreme, employees simply ignore the standards—that is, they do not

3. The purpose of this question is to get students to think about the strategic role of

standard costs and flexible budgets in a comprehensive management accounting

and control system. In this regard, students should think about both the costs and

benefits of using these elements of a traditional financial control mechanism.

Criticisms/Limitations of Conventional Standard Cost Variance Analysis

1. Variances are too aggregated and concentrate on consequences rather than

2. Traditional standard cost variance reports are too late to be useful. In order to

14-35

Chapter 14 – Operational Performance Measurement: Sales, Direct-Cost Variances, and the Role of Nonfinancial

Performance Measures

14-40 (Continued-1)

real time the consumption of resources (e.g., labor and materials). Traditional

standard cost systems provide variance information only infrequently, e.g., at

the end of each month. Thus, the relevance of this information can be called

into question.

3. Standard costing systems tend to focus too heavily on cost minimization. For

companies competing on the basis of cost (i.e., those pursuing a cost–

4. Standard costing systems take a departmental perspective rather than a

process perspective. The point here is that traditional standard costing systems

are not “integrated.” As such, each department or cost center tends to focus on

5. Too much emphasis is placed on the cost and efficiency of direct labor.

Traditional systems focus on the analysis of labor and material cost variances,

in spite of the fact that labor, as a percentage of total manufacturing cost, is

6. JIT Manufacturing: JIT is a strategy that requires continuous working to improve

quality and reduce costs. Some question whether traditional standard cost

systems motivate continuous improvement that is at the heart of a JIT system.

7. Standard costs become out-dated quickly due to shorter product life cycles.

8. Some critics maintain that the use of standard costs and variances (via flexible

budgets) is misplaced in terms of securing operational control. These critics

maintain that operating personnel perform or participate in one or more

Benefits/Advantages of Using a Standard Cost System

1. Provides a good basis for cost comparisons. To the extent that “cost” is a

critical variable on which the organization competes, a standard cost system

14-36

Education.

Chapter 14 – Operational Performance Measurement: Sales, Direct-Cost Variances, and the Role of Nonfinancial

Performance Measures

14-40 (Continued-2)

2. Enables managers to use management by exception. As noted above, a

3. Provides a basis for performance evaluation and determining bonuses. Again,

the key here is that managers who decide to use standard costs and variances

14-37

Chapter 14 – Operational Performance Measurement: Sales, Direct-Cost Variances, and the Role of Nonfinancial

Performance Measures

14-41 Control of Operating Processes/Non-financial Performance Indicators (45

minutes)

1. Organizations engage in a variety of processes in order to deliver the stated value

proposition to its targeted customers and in order to achieve its stated financial

objectives. These processes, for expository purposes, might be grouped into the

Operating processes might be defined as what the organization does, on a day-to-

day basis, to produce and deliver to customers its outputs (services and/or products).

Thus, operating processes include activities such as: acquiring raw materials from

supplier firms; producing finished goods and services; and, distributing the finished

product to customers. Customer-management processes relate to activities designed to

strengthen and expand relationships with the organization’s targeted customers. More

specifically, customer-management processes included the following activities:

customer selection (i.e., specification of targeted customers), customer acquisition

(everything from generate leads to closing the sale), customer retention (e.g., through

the use of customer-service units and call centers), and customer growth (e.g., through

cross-selling activities). Growth and innovation processes relate to the development of

new products, services, and processes that allow the firm to penetrate new markets or

market segments. (Without growth and innovation the firm risks losing its competitive

employment practices, and investment in the community.

2. The following are examples of possible objectives and associated performance

indicators for two operating processes: production, and distribution.

Production Process

(1) Achieve Reduction in the Cost of Outputs (Products and/or Services)

(2) Achieve Continuous Improvement in Key Processes

14-38

Education.

Chapter 14 – Operational Performance Measurement: Sales, Direct-Cost Variances, and the Role of Nonfinancial

Performance Measures

14-41 (Continued-1)

Total Cost of Quality (COQ), over time

Ratio of Prevention + Appraisal Costs to Internal + External Failure Costs

(3) Increase the Responsiveness of the Manufacturing Process

Process Cycle Efficiency (PCE) (i.e., ratio of value-added time to total

up time)

(4) Improve the Utilization of Capital (Fixed) Assets

Number and % of machine breakdowns

Distribution Process

(1) Reduce Cost of Servicing Customers

Activity-based costs associated with key activities (e.g., storage and

(2) Improve Delivery Process:

% of on-time deliveries

14-39

Education.

Chapter 14 – Operational Performance Measurement: Sales, Direct-Cost Variances, and the Role of Nonfinancial

Performance Measures

14-41 (Continued-2)

Enhance Quality of the Distribution Process

14-40

Education.