Chapter 7 – Cost Allocation: Departments, Joint Products, and By-Products

7-38 (continued -2)

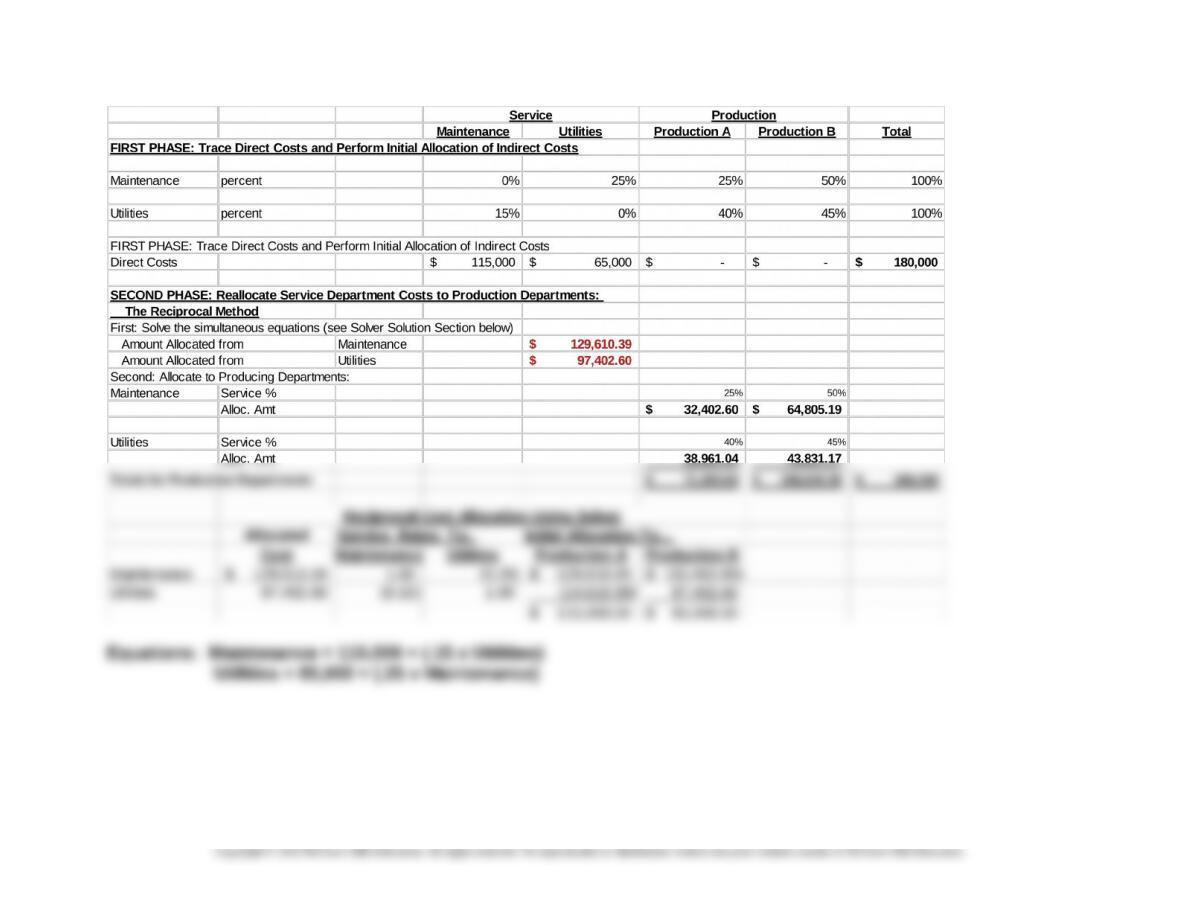

The Reciprocal Method

7-41

Chapter 7 – Cost Allocation: Departments, Joint Products, and By-Products

7-42

Chapter 7 – Cost Allocation: Departments, Joint Products, and By-Products

7-39 Departmental Cost Allocation (50 Min)

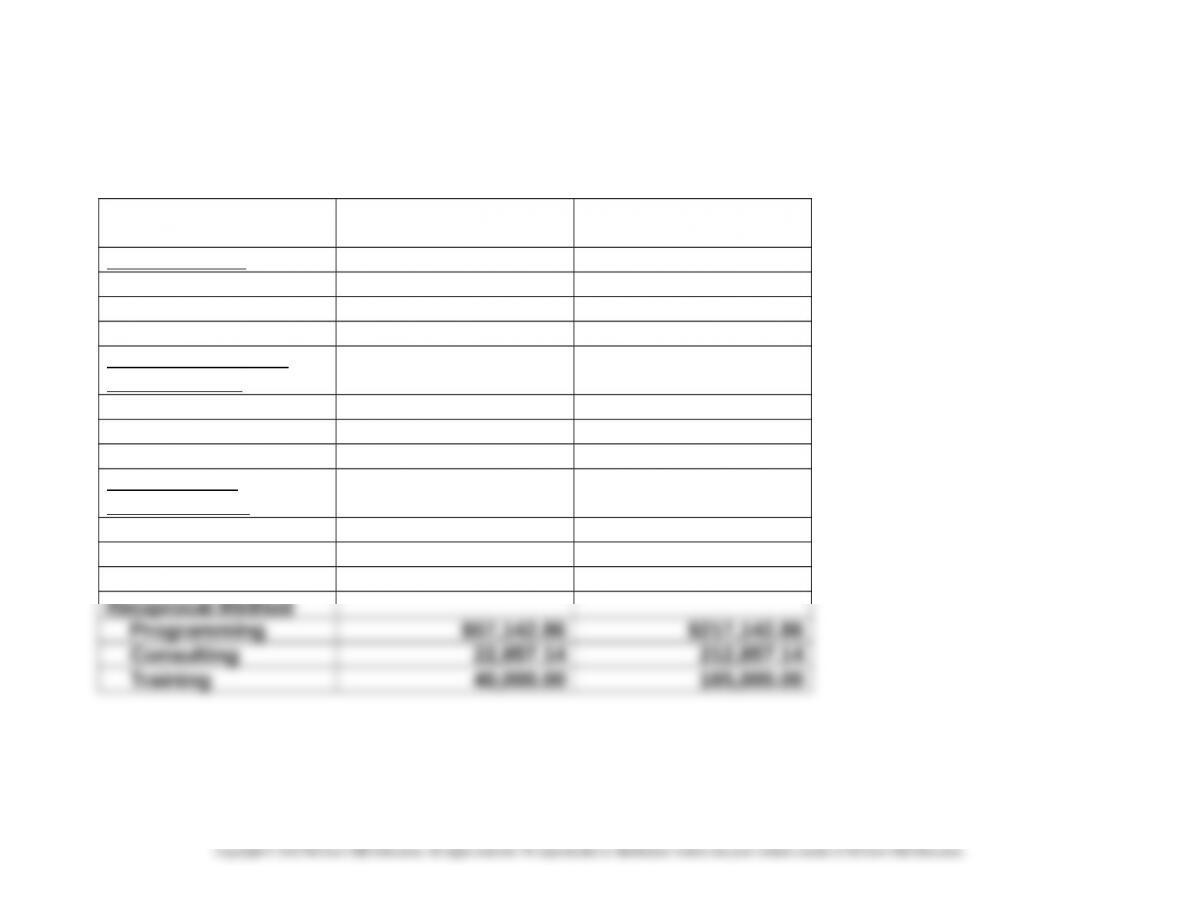

Total Service Dept.

Cost Allocated

Total Production Cost

Direct Method

Programming $57,777.78 $217,777.78

Consulting 21,111.77 211,111.11

Training 41,111.77 166,111.11

Step Method (info

systems first)

Programming $56,888.89 $216,888.89

Consulting 23,555.56 213,555.56

Training 39,555.56 164,555.56

Step Method

(facilities first)

Programming $58,000 $218,000

Consulting 20,500 210,500

Training 41,500 166,500

7-43

Chapter 7 – Cost Allocation: Departments, Joint Products, and By-Products

7-39 (continued -1)

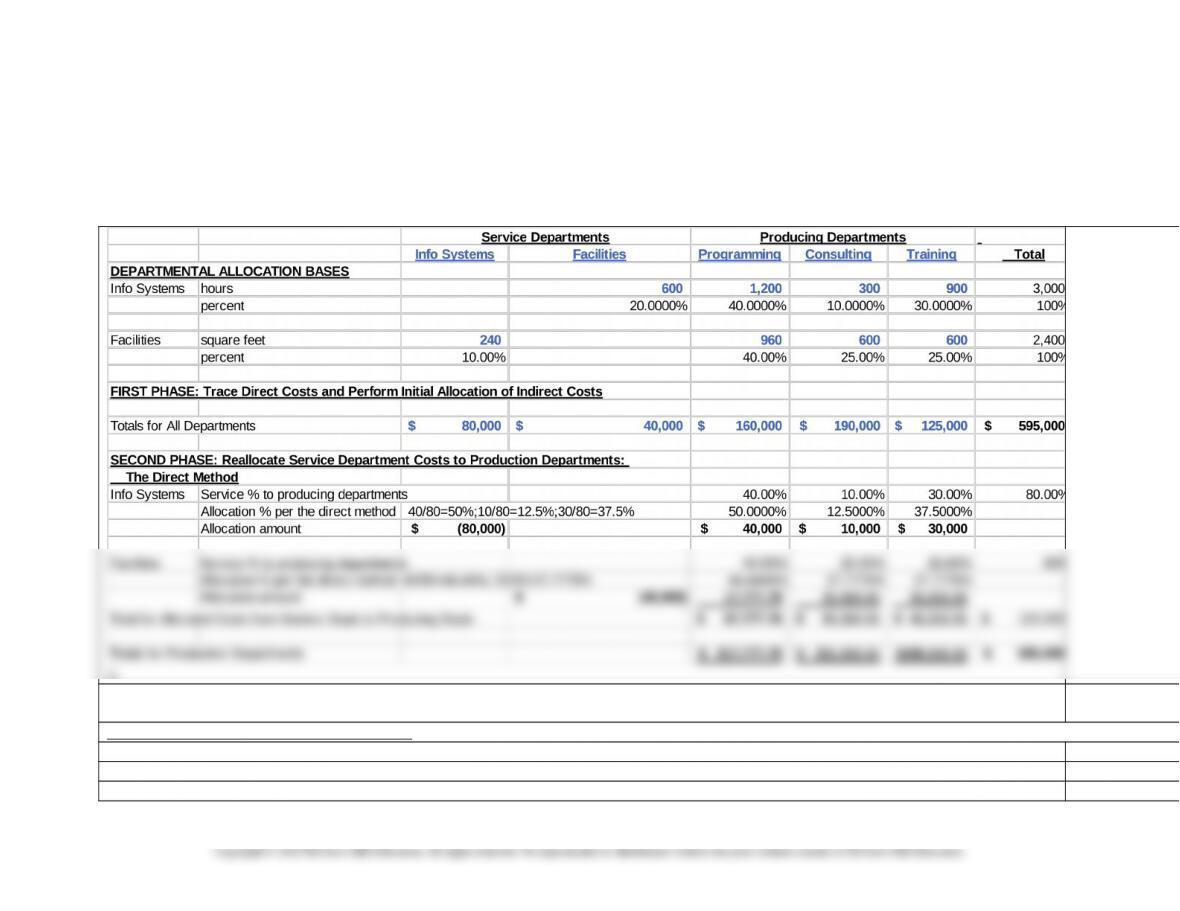

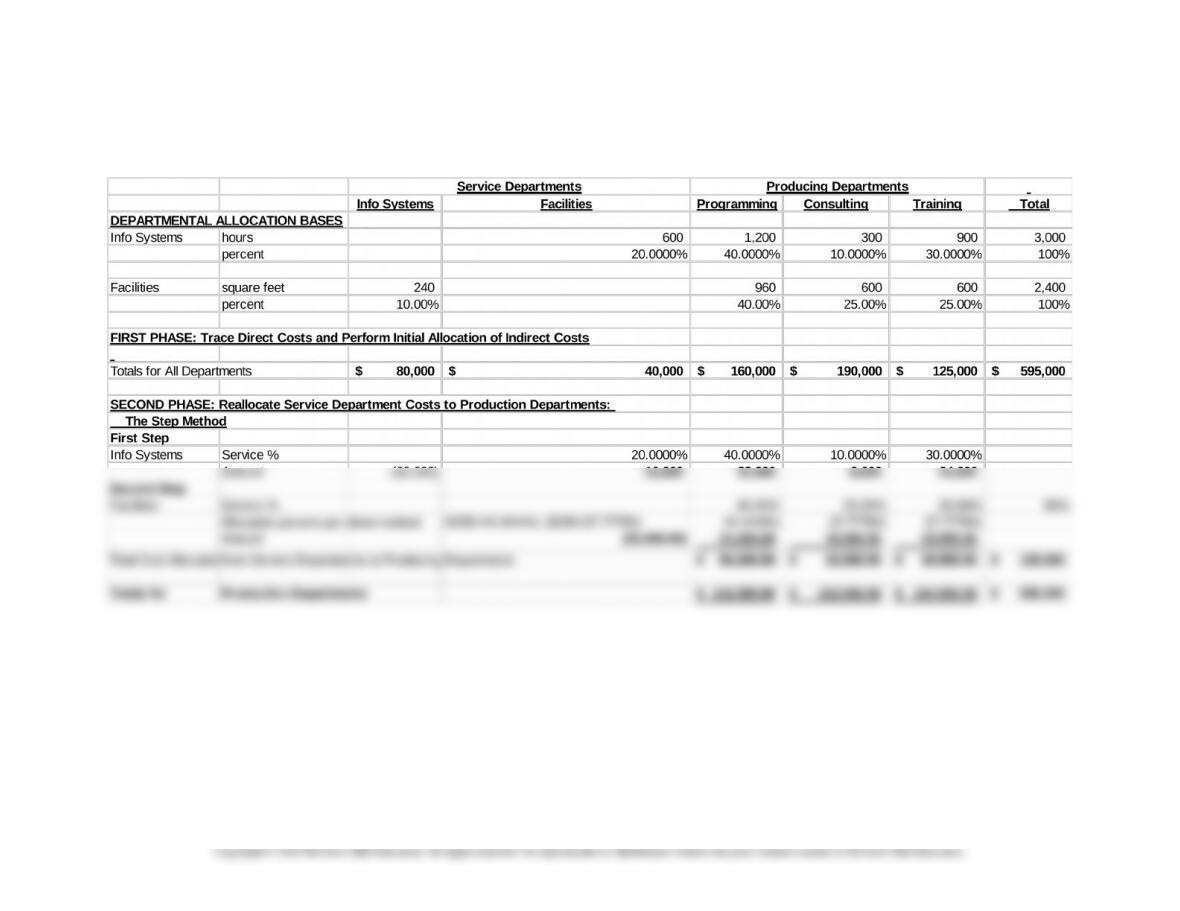

1.a. The Direct Method

X

DEPARTMENTAL ALLOCATION BASES

Info Systems

percent

7-44

Chapter 7 – Cost Allocation: Departments, Joint Products, and By-Products

Facilities

percent

FIRST PHASE: Trace Direct Costs and Perform Initial Allocation of Indirect Costs

Totals for All Departments

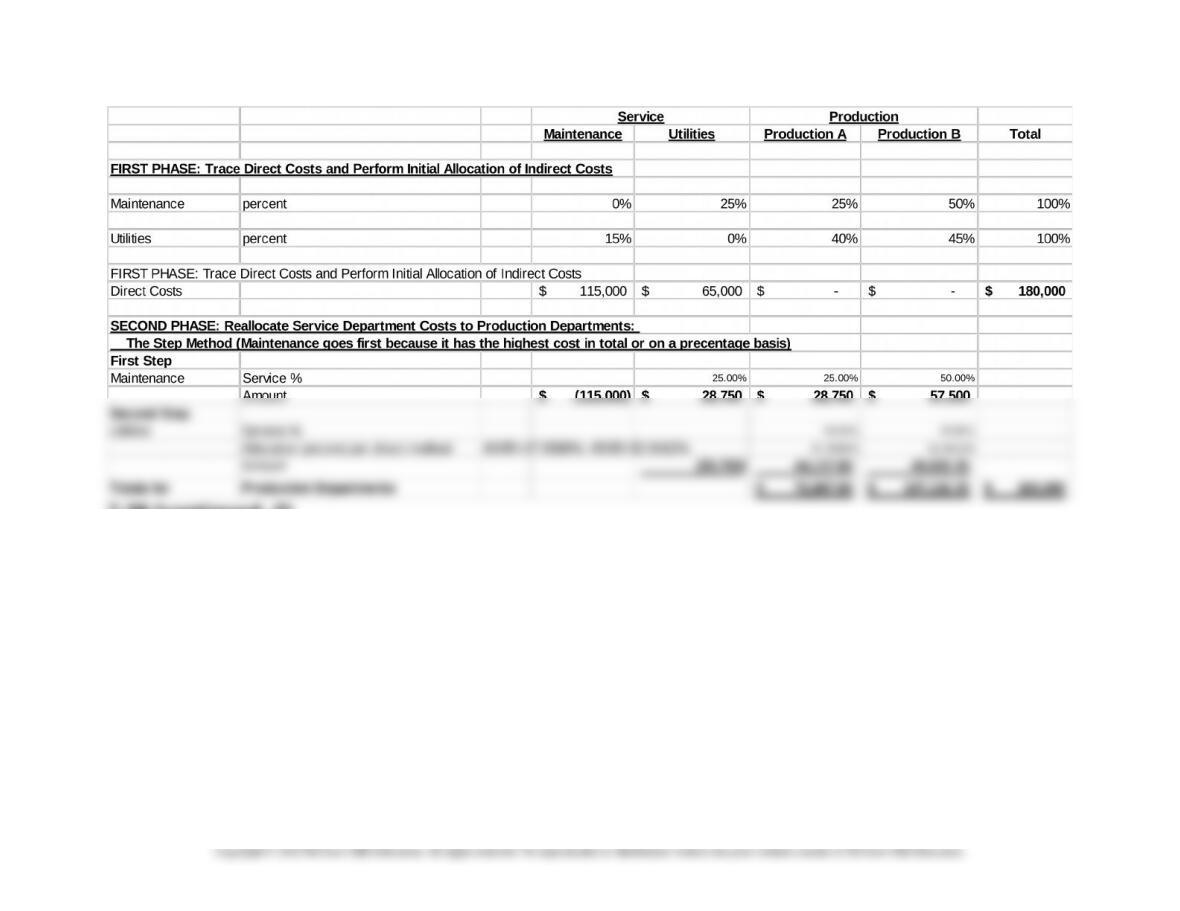

SECOND PHASE: Reallocate Service Department Costs to Production Departments:

The Direct Method

Info Systems Service % to produ

Allocation %

method

Allocation amoun

Facilities Service % to produ

Allocation %

method

Allocation amoun

Total for Allocated Costs from Service Depts to Producing Depts

Totals for Production Departments

7-45

Chapter 7 – Cost Allocation: Departments, Joint Products, and By-Products

7-39 (continued -2)

1.b The Step Method (Information Systems Goes First)

7-46

Chapter 7 – Cost Allocation: Departments, Joint Products, and By-Products

7-39 (continued -3)

1.b The Step Method (Facilities Goes First)

7-47

Chapter 7 – Cost Allocation: Departments, Joint Products, and By-Products

7-39 (continued -4)

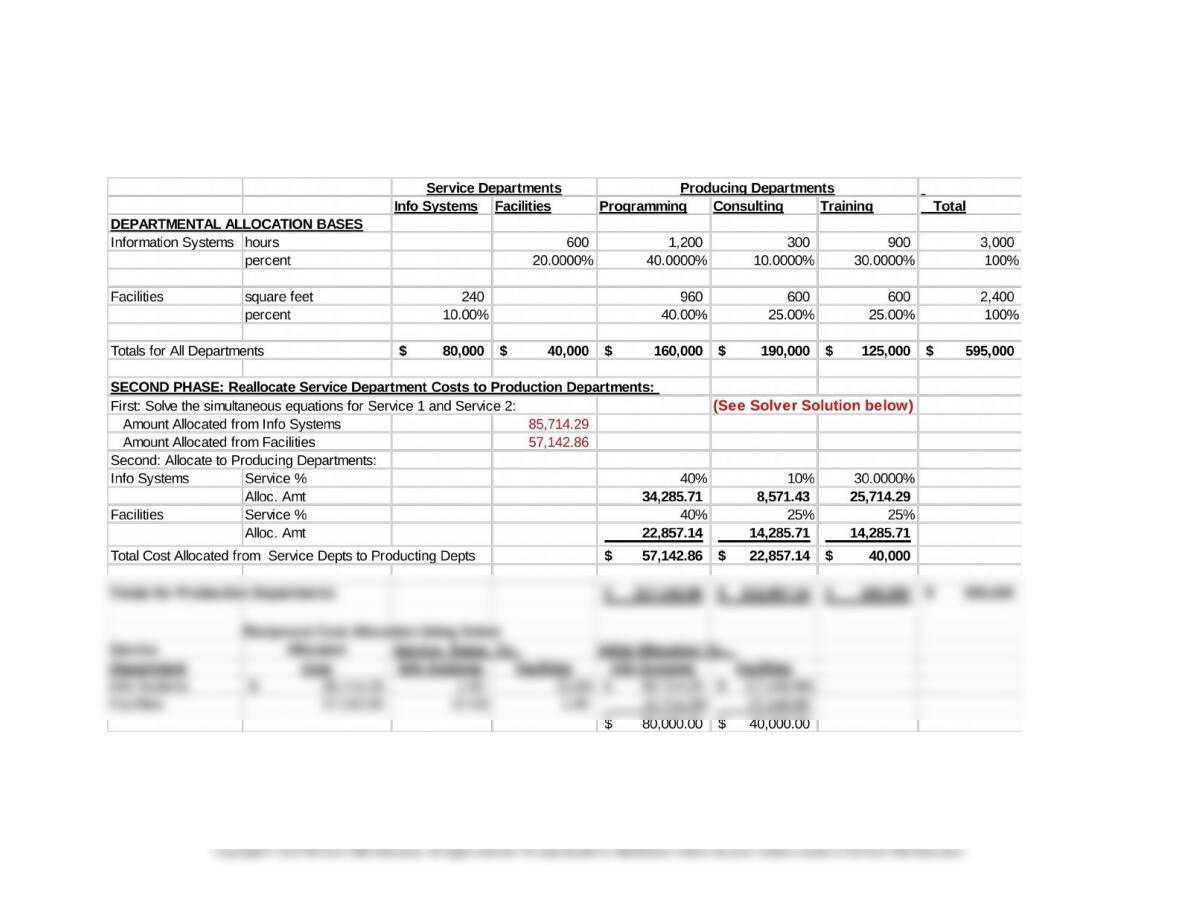

1.c. The Reciprocal Method

7-48

Chapter 7 – Cost Allocation: Departments, Joint Products, and By-Products

7-39 (continued -5)

2. Rather than to allocate costs, Data Performance might consider

using the market prices for these services. The use of market prices

would force the service departments to be competitive with outside

suppliers of the services.

7-49

Education.

Chapter 7 – Cost Allocation: Departments, Joint Products, and By-Products

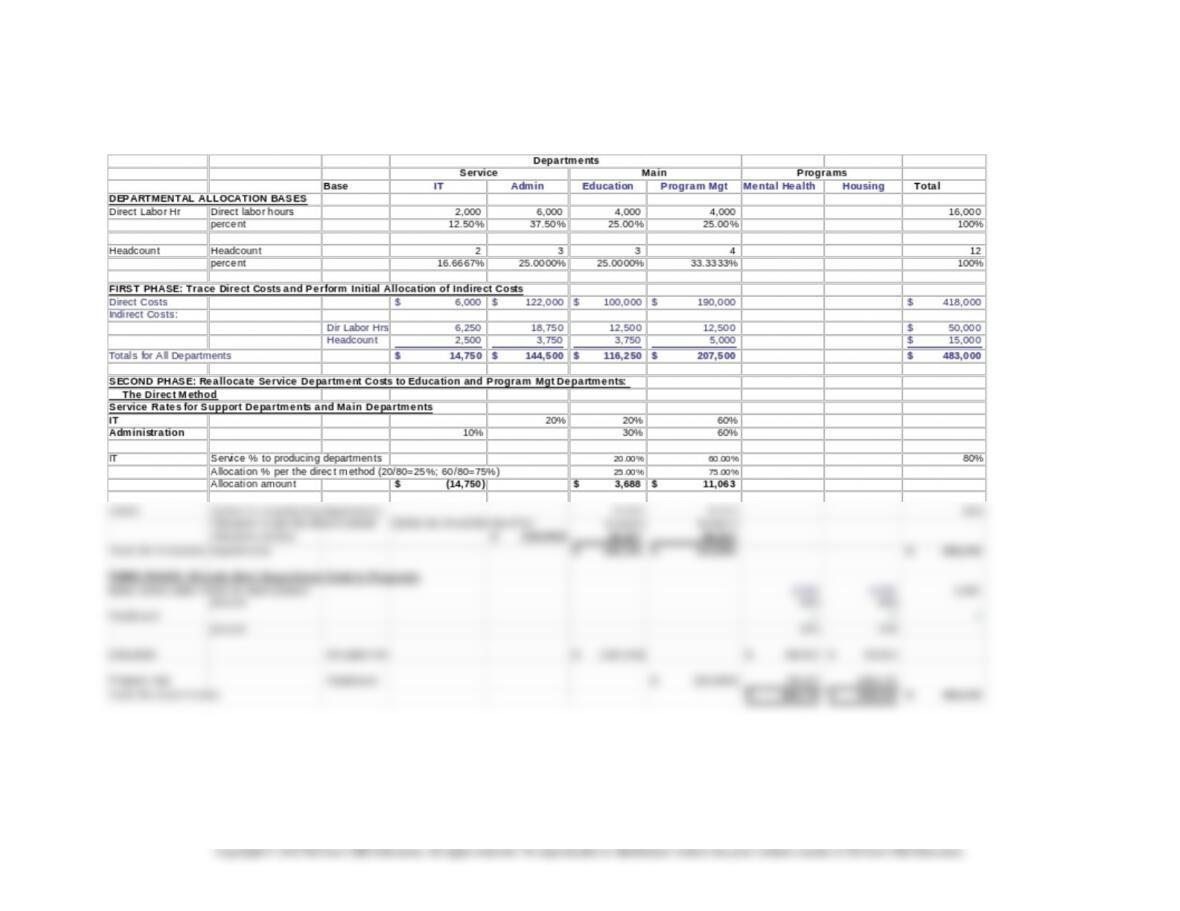

7-40 Departmental Cost Allocation (50 min)

The Direct Method

7-40 (continued -1) The Step Method

7-50