Chapter 8 – Cost Estimation

Chapter 8

Cost Estimation

Teaching Notes for Cases

8-1. High-Low Method and Regression Analysis

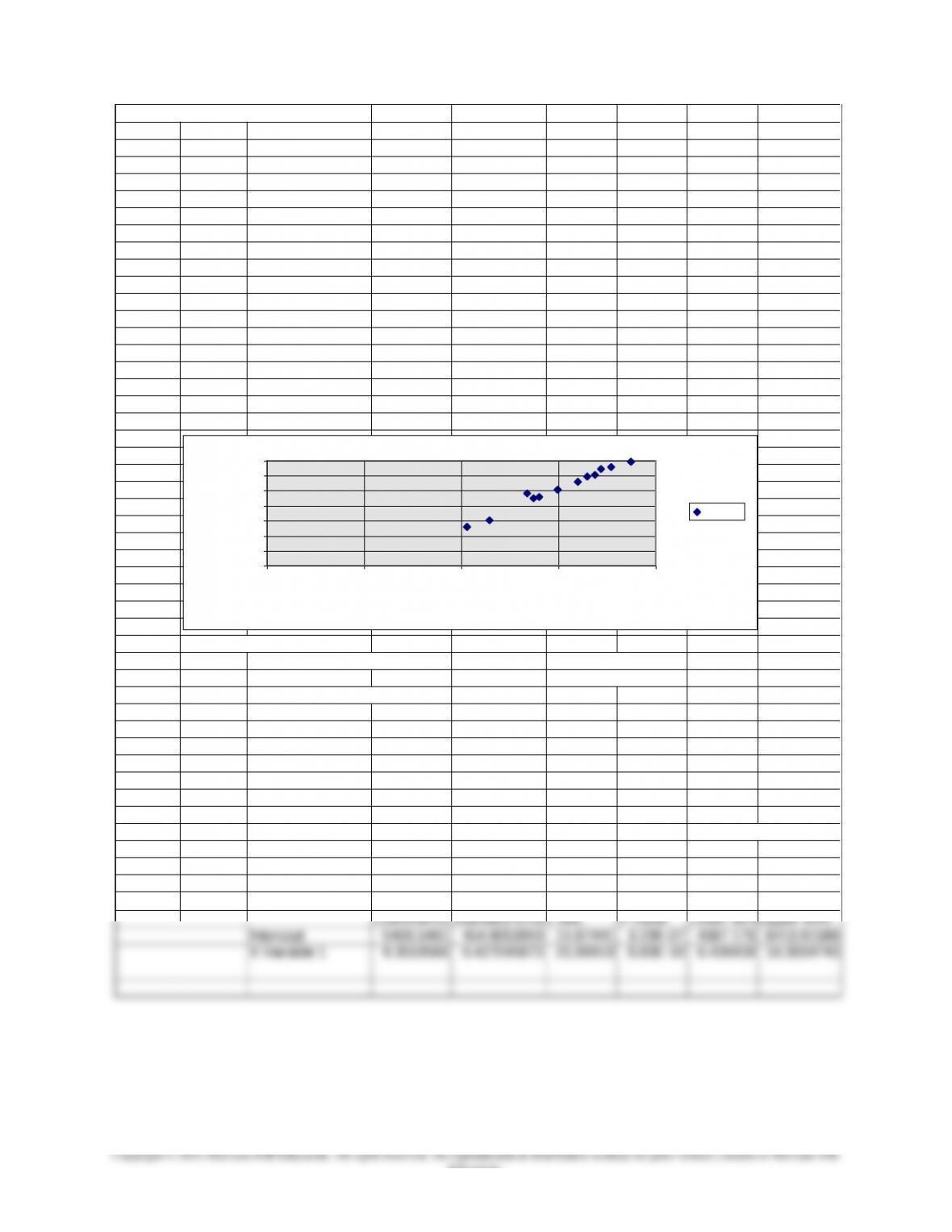

1, 2. The spreadsheet below shows the analysis of the Brenham Hospital data using both regression and

high-low methods. Before either method is applied, a scattergraph is prepared, as shown in the middle of

the spreadsheet; there are no apparent outliers or nonlinear patterns. The unit variable cost and fixed cost

for the high-low method are calculated, in the cells immediately below the figure, from the data in the

upper right hand corner of the spreadsheetunit variable cost is $9.73 and fixed cost is $5,264. The

regression analysis is shown at the bottom of the spreadsheetunit variable cost is similar to the high-low

regression results are better, we would choose the regression model for the most accurate predictions.

3. Since unit variable cost is apparently less than $10, from both the regression and high-low results, and

since the fixed costs are unlikely to change (in fact the hospital says it plans to keep the dietician and

equipment), the best plan would be to keep the kitchen open, since the variable cost of the kitchen

(approximately $9.50) is less than the outside price of $11.50.

8-1

Chapter 8 – Cost Estimation

8-2

Brenham General Hospital

High Low

Other Food Total Patient Prediction

Dietician Staff Costs Maint. Equip. Cost Days Error

JAN 2,875 3,122 9,674 1,401 1,649 18,721 1,382 –

FEB 2,875 2,908 9,184 1,322 1,415 17,704 1,312 112,513

MAR 2,875 2,655 8,302 1,322 1,313 16,467 1,186 119,441

APR 2,875 2,600 7,084 1,288 1,105 14,952 1,012 27,693

MAY 2,875 2,433 6,398 1,200 1,089 13,995 914 28,634

JUN 2,875 2,083 4,338 1,133 1,011 11,440 604 86,535

JUL 2,875 1,809 3,612 1,093 900 10,289 516 –

AUG 2,875 2,322 6,275 1,122 1,112 13,706 896 80,063

SEP 2,875 1,434 6,734 1,235 1,103 13,381 962 1,563,944

OCT 2,875 2,700 9,002 1,302 1,300 17,179 1,286 368,783

NOV 2,875 2,798 8,456 1,300 1,442 16,871 1,208 24,277

DEC 2,875 2,600 7,798 1,322 1,396 15,991 1,114 14,534

34,500 29,464 86,857 15,040 14,835 180,696 12,392 2,426,417

Regression High Low:

SUMMARY OUTPUT Unit Variable cost 9.736721

Fixed Cost 5264.852

Regression Statistics

Multiple R 0.9897344

R Square 0.9795741

Adjusted R Square 0.9775315

Standard Error 385.28595

Observations 12

ANOVA

df SS MS F Significance F

Regression 1 71,190,535 71190535 479.5743 8.83E-10

Residual 10 1,484,453 148445.3

Total 11 72,674,988

Coefficients

Standard Error

t Stat P-value

Lower 95%

Upper 95%

Intercept 5400.5461 454.8053919 11.87441 3.23E-07 4387.176 6413.91586

X Variable 1 9.3519566 0.427045873 21.89919 8.83E-10 8.400439 10.3034743

–

200

400

600

800

1,000

1,200

1,400

– 5,000 10,000 15,000 20,000

Cost

Patient Days

Series1

8-2. Cost Estimation; Implementation

Background for the Case Answers:

Students will find it helpful if you go through the computations in the example in the case for job

1. This will also assure that they understand the nature of the adjustment that is being made. As you go

through the exhibit, emphasize that these adjustments are made only once a year even though many of the

jobs are in process for two and three years.

In the example in the case, the original cost estimate given on the first line is for reference only. It

is not used in the adjustment calculation. The second section calculates the costs incurred to date plus the

estimated costs to complete the job, yielding a new estimate for the total cost that will be required to

complete the job.

The third portion of the exhibit is the market value computation using the net realizable value less

a normal profit margin approach. The last line is the amount of the adjustment required to bring the

inventory carrying value (cost) down to lower of cost of market (LCM) .

For job 1, the LCM value of inventory will be ($2,100 + $373) – $572 = $1,901, while for job 2

the inventory value is $100 – $800 = $(700). Although this latter value may seem strange, the firm is

properly recognizing its loss on the job as soon as they become aware of it.

Next, you may wish to begin the discussion of the case by asking students to identify the major

problem areas that affect profitability. Then proceed to a discussion of the two specific questions.

The class discussion of the problem areas should reveal:

1. It appears that some jobs are accepted at unprofitable prices due to faulty cost-estimate

analysis (e.g., job 2 in the exhibit).

2. There is likely to be pressure put on the cost-estimate analysts by sales to keep estimates

low so as to generate additional sales. The analysts report to sales.

3. Feedback is slow. Problems are identified only when a job is complete or at the year-end

review of inventory. This makes it difficult to pinpoint responsibility and makes the taking

of timely corrective action nearly impossible.

4. The long production cycle exposes the firm to considerable risk due to inflation.

5. The large overhead rates suggest that the firm is not doing a very good job of tracing direct

costs to products. This, in turn, makes it difficult to have much confidence in the

cost/profitability figures.

Answers to Questions

1. (a) The cost-estimate analysts should not report to sales. It is likely that more realistic cost estimates

would result if this unit reported to a production manager.

In addition, a performance report should be devised for each cost-estimate analyst. This report

should routinely compare original cost estimates to actual costs incurred. If an analyst consistently over or

under estimates costs, corrective action can be taken. To be useful, such a report must be generated on a

timely basis. A monthly report comparing actual costs incurred-to-date with the estimate should provide

the needed information.

The accounting system should be adjusted to treat more costs as direct costs. This should help the

8-3

Education.

Chapter 8 – Cost Estimation

(b) Currently, the LCM review comes too late for effective control. The analysis should be made

much more frequently. A monthly analysis would provide the basis for the cost analyst’s performance

2. Because of the very large dollar investment in these products and the long in-process production times,

the carrying costs for inventory are substantial. Progress payments and advance payments shift a good

portion of the carrying costs (the cost of capital) to the customer.

With a fixed price contract the inflation risk is borne entirely by the company. Inserting estimates

What the Firm Actually Did

The firm recognized the critical role played by the cost analyst. Errors here could doom the firm

to unprofitable contract even before work had begun. The firm changed the reporting relationship of the

analysts to report directly to the plant manager. In addition, the firm upgraded the quality of the analysts

by requiring more professional training.

The original cost analysis for each job became a standard. Monthly reports of actual costs

compared to this standard are now prepared for each job. Thus production and estimation problems can

now be more quickly identified. To assure that personnel do not attempt to “manage” earnings through the

8-4

Chapter 8 – Cost Estimation

8-3. Regression Analysis; Activity Based Costing; Strategy; International

Note to instructor: A variation on this case, shorter, with a focus on correlation analysis rather

than regression, is in the text, problem 8-47.

The firm is a large manufacturer of soap products for the hospitality industry. While the data is

real, the locations and descriptions are disguised. The firm has a goal of growth in sales, and has adopted

a marketing strategy of differentiation to achieve this. The result is a significant growth in the number and

variety of productssizes, fragrances, moisturizers, and packaging.

The firm operates in two marketing segmentsthe large hotel chain market, and the small

independent hotel market (that purchase from wholesalers). HPI’s success has been in the large chain

market, where HPI introduced an attractive and appealing product. At the time of the case, HPI is

contemplating a significant expansion into the wholesale segment. A consequence of this strategy will be

an increased variety of products.

Teaching Objectives:

The case is very useful for an illustration of the potential application of ABC costing, because of

the firm’s diverse product line (packaging, soap fragrance, etc). A key result of the strategy conflict

identified above is that product diversity increases rapidly (as a result of the marketing strategy) while the

manufacturing strategy has been to invest in plants oriented to high-volume, low-cost production. ABC

can play a key role in developing a better understanding of the cost implications of the marketing strategy.

The regression exercise is useful in three ways. First, it shows the students that a regression tool

within Excel can help provide useful information about cost drivers. Second, it gives the students an

opportunity to work with actual data in identifying cost driver relationships. Third, it illustrates the

complex inter-relationships among cost drivers.

The case was originally used in the manufacturing strategy course to illustrate the conflict

between manufacturing strategy (cost leadership) and marketing strategy (differentiation) in the case. The

case has been adapted to deal with cost drivers and strategic issues.

Main Points:

Discussion Questions:

1. What is HPI’s competitive strategy? How does HPI deal effectively with global competition in its

business?

HPI has built its business on differentiation, in the large hotel chain market. The attractive and

appealing soap products have developed this differentiation and given HPI a competitive advantage. As

other manufacturers are catching up in this segment, HPI is moving to the wholesale segment of the

8-5

Chapter 8 – Cost Estimation

An important feature of competition in the soap product business is cost leadership, as noted

above. By locating its plants near to its major markets and customers, HPI has located plants and

schedules production so as to minimize transportation costs. There are a large number of global issues

2. What are the implications of the marketing and manufacturing initiatives undertaken by HPI?

The point should be made that the new marketing focus, involving increased product variety (and

built upon a cost leadership (large order sizes, low variety).

3. Using the data in Table 1 and appropriate methods of analysis such as regression or correlation

analysis, analyze the effect of order size and product variety on the productivity and cost structure of the

Paris plant.

The case is a good illustration of the value of ABC costing, to help measure product profitability

in a firm experiencing increased product variety. This is well illustrated in the regression/correlation

The solutions for the subtotal approach and graphical approach are not illustrated here but the

regression approach is shown below.

There are two regressions. Each of the two have the same three independent variables:

a) machine type

b) order size

c) a code for complexity (see the key at the bottom of Table 1 for an explanation)

The two regression each have a different dependent variable:

Regression One: per unit setup time + downtime

Regression Two: per unit runtime

The students will likely make a variety of inferences from their individual analyses of the data.

After some discussion, make sure that the following points are made:

a. Assess the statistical measures for the regressions the students present, and/or for the regressions

attached. Make sure that the students understand the importance of evaluating the regressions:

b. The regression results show clearly that:

a) larger orders have lower per unit set up time and per unit runtime (i.e., better productivity)

per both Regressions, the sign of the quantity independent variable is negative and significant (p<.05)

8-6

Education.

Chapter 8 – Cost Estimation

(Note however, that these regressions are weak with low R-squares. However, since our focus is

Regression One

Dependent Variable: Per unit set-up time plus downtime

Regression Statistics

Multiple R 0.603189

R Square 0.363837

Adjusted R Square 0.327828

Standard Error 0.014407

Observations 57

ANOVA

df SS MS F

Significance F

Regression 3 0.006291226 0.002097 10.10399 2.28E-05

Residual 53 0.011000104 0.000208

Total 56 0.01729133

Coefficients

Standard Error

t Stat P-value

Lower 95%

Intercept -0.0032 0.007375574 -0.43452 0.665672 -0.018

Number 0.000667 0.000671082 0.993887 0.324794 -0.00068

Quantity -8.7E-06 3.27751E-06 -2.65008 0.010585 -1.5E-05

Complexity 0.010325 0.002377343 4.343194 6.37E-05 0.005557

Chapter 8 – Cost Estimation

Regression Two

8.4 Custom Photography

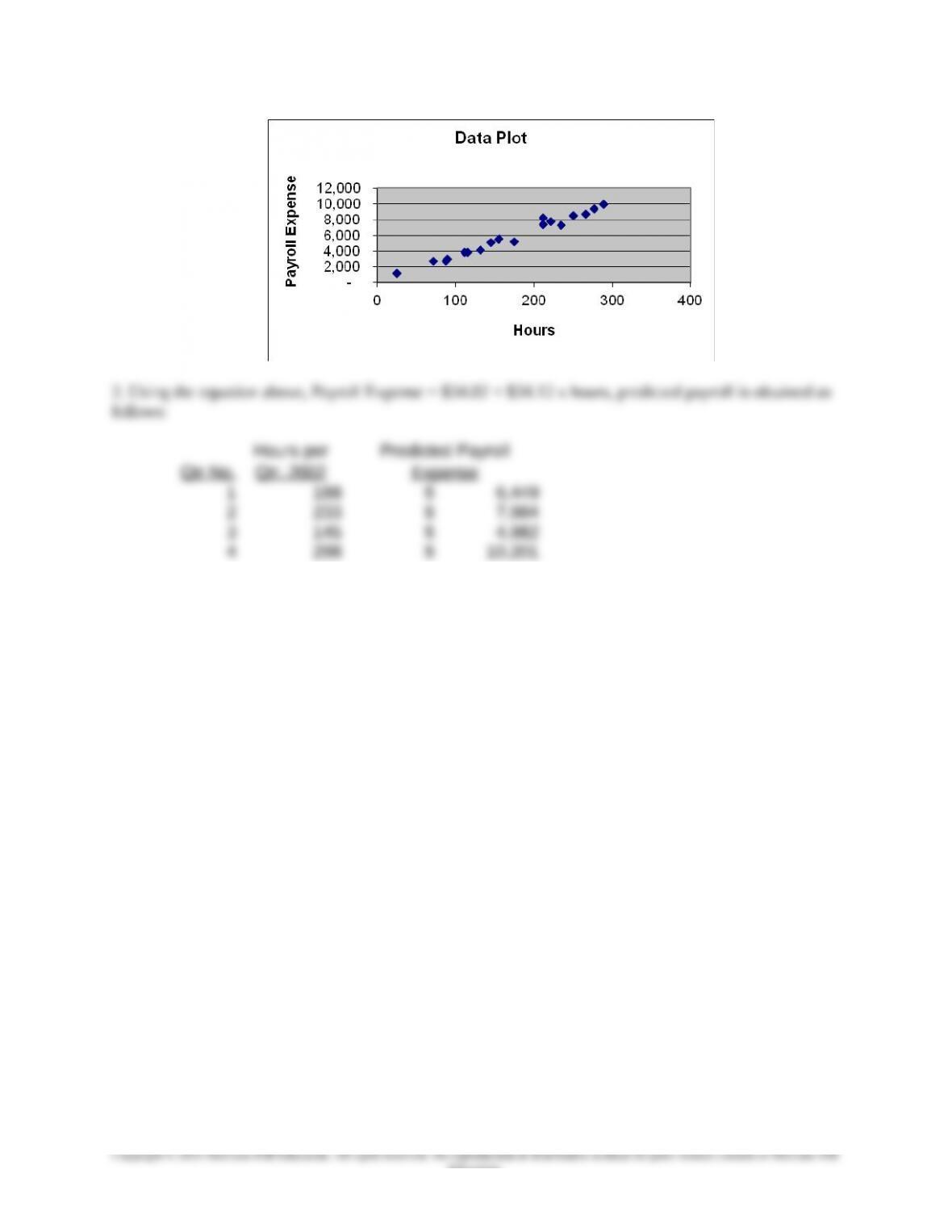

1. The Excel regression analysis for Custom Photography is shown below. Note that all the statistical

measures are excellent. The R-squared is very high, the standard error of the estimate is relatively low at

Note: While the regression is a very good fit, the management accountant should also check to see if

there are any potential outliers or non-linearity to the data, by studying the graph of residuals, checking

the Durbin-Watson statistics, and similar statistical measures. Graphs shown below of the residuals and

of the data do not appear to show any signs of outliers or non-linearity, so that the management

accountant can reasonably rely on the results.

8-8

Dependent Variable: Per unit runtime

Regression Statistics

Multiple R 0.58985361

R Square 0.34792728

Adjusted R Square

0.31101751

Standard Error 0.0034273

Observations 57

ANOVA

df SS MS F

Significance F

Regression 3 0.00033218 0.00011073 9.4264263 4.304E-05

Residual 53 0.00062256 1.1746E-05

Total 56 0.00095474

Coefficients

Standard Error

t Stat P-value Lower 95%

Intercept 0.04555712 0.00175464 25.9638504 8.209E-32 0.0420378

Number 2.3785E-05 0.00015965 0.14898304 0.8821325 -0.0002964

Quantity –4.096E-06 7.7971E-07 -5.25336231 2.705E-06 -5.66E-06

Complexity -0.0008911 0.00056557 -1.5755149 0.1210886 -0.0020254

Chapter 8 – Cost Estimation

Regression Statistics

Multiple R 0.988

R Square 0.977

Adjusted R

Square

0.975

Standard Error 431.538

Observations 20

ANOVA

df SS MS F Significance F

Regression 1 140804738.725 140804738.725 756.101 0.000

Residual 18 3352047.475 186224.860

Education.

Chapter 8 – Cost Estimation

8-10

Education.