Chapter 14 – Operational Performance Measurement: Sales, Direct Cost Variances, and the Role of Nonfinancial

Performance Measures

Chapter 14

Operational Performance Measurement: Sales, Direct Cost

Variances, and the Role of Nonfinancial Performance Measures

Teaching Notes for Case

Case 14-1: Pet Groom & Clean Case

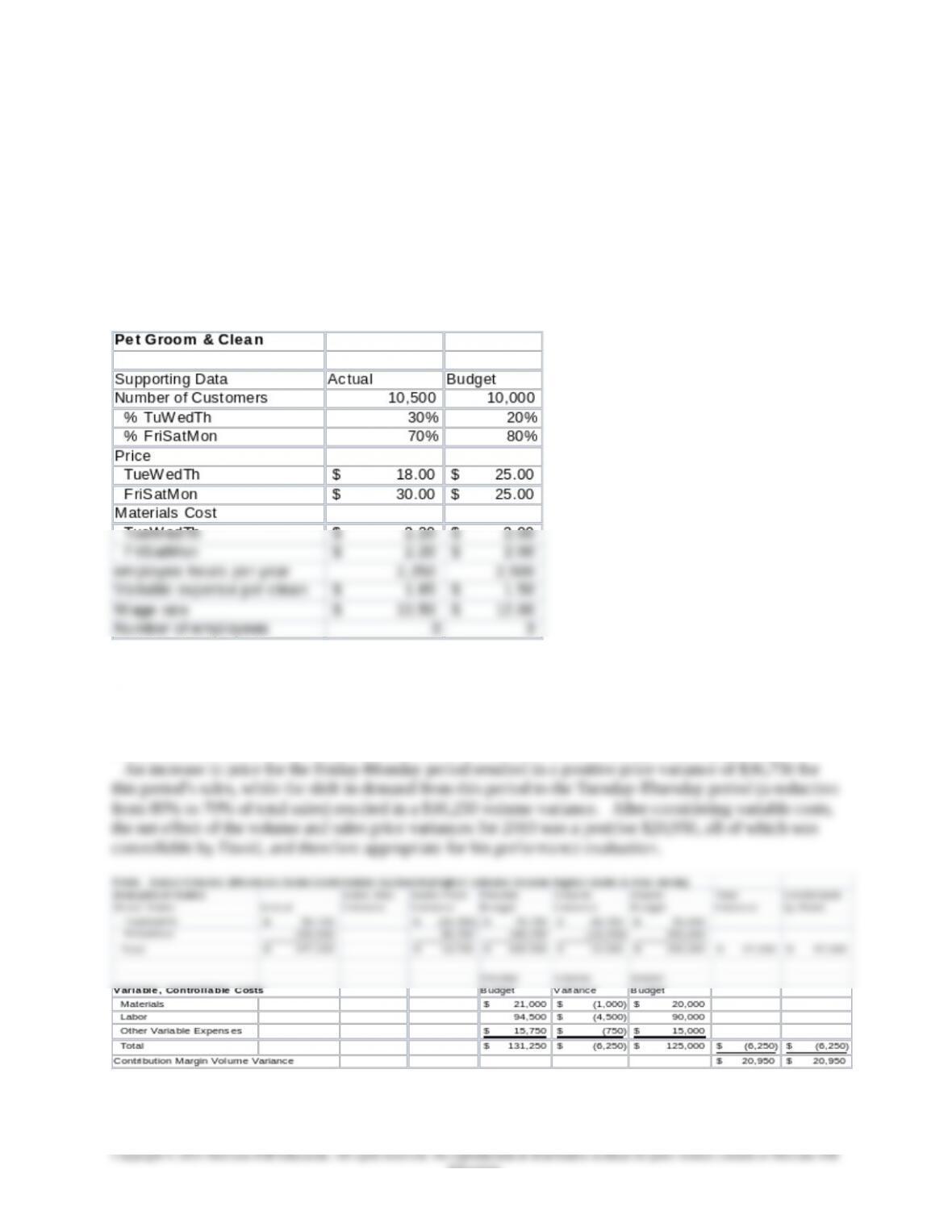

Summary of Key Data for the analysis

First step: Analyze Total Sales and the effect of price and volume changes for both the Tuesday-

Thursday and the Friday-Monday periods. The results show that the decrease in price for the Tuesday-

Thursday period was a net advantage: the price reduction caused a negative price variance of $22,050,

but the volume variance was greater, at $28,750 (this takes into account both the increase in total number

of service units sold and the shift in demand from 20% to 30% for the Tuesday-Thursday period).

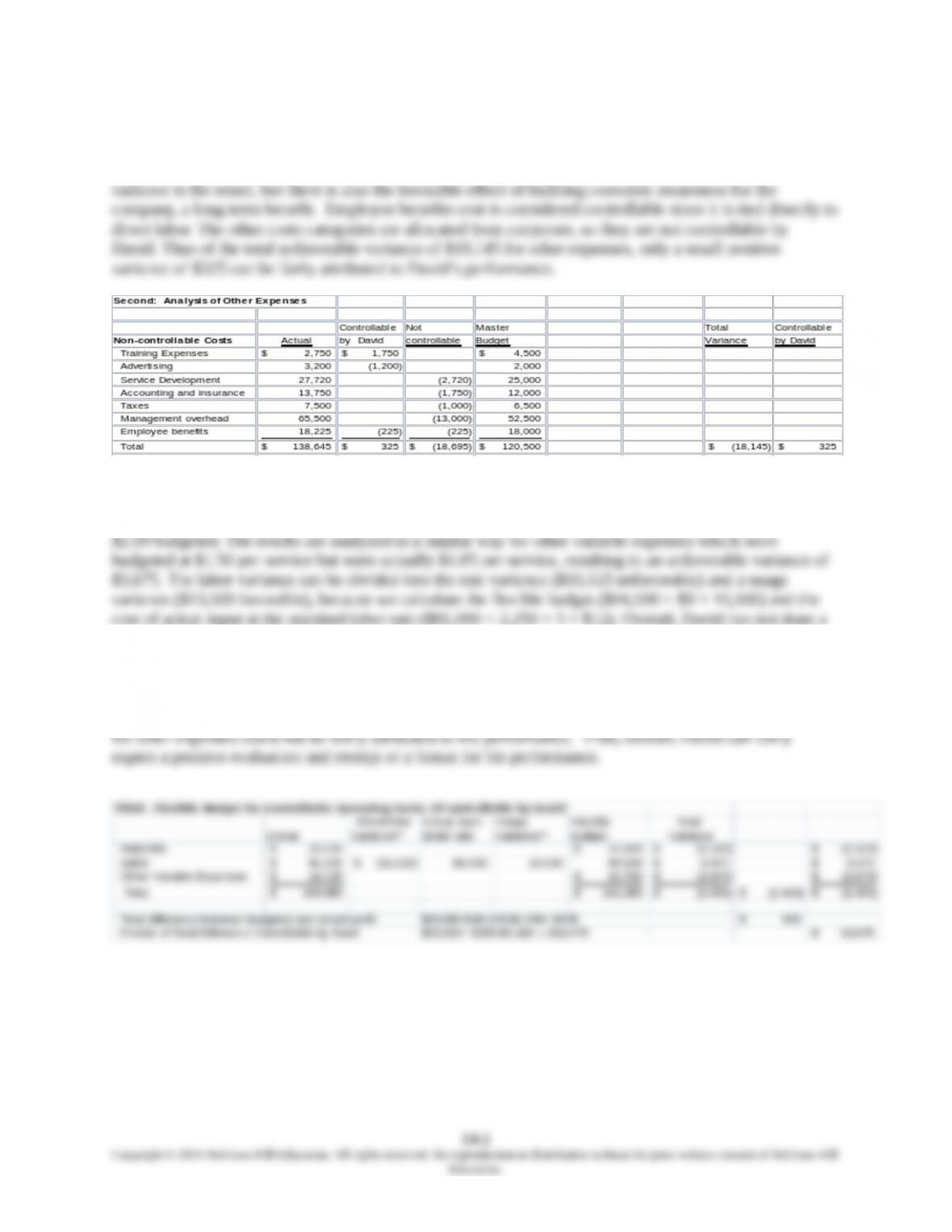

Second step: Analyze other expenses, some of which are controllable by David and others are not.

Training expenses are controllable by David since he chooses how much time each of his staff spends in

14-1

Education.

Chapter 14 – Operational Performance Measurement: Sales, Direct Cost Variances, and the Role of Nonfinancial

Performance Measures

training. Note that the amount of training cost is below budget, thus saving costs for David, but the

downside is that David has not met the expected amount of training time per staff (6 hours per staff), and

training is important for the long-term success of the company. This favorable cost variance also has that

negative impact. In contrast, David chose to spend over the budget on advertising. The unfavorable cost

The third and final step is to analyze the variable costs, all of which are controllable by David. The

following shows that the materials variance is unfavorable at $2,100, when the flexible budget is

compared to the actual costs for materials. The actual cost of materials is $2.20 per service rather than the

very good job of controlling variable costs, and the net unfavorable variance of $2,400 illustrates this.

Note that the difference between the actual net income and budgeted net income of $405 can be

determined by adding the three variances in each of the three steps. The total variance controllable by

David is a favorable amount of $18,875 because such a large portion of the $18,145 unfavorable variance

Chapter 14 – Operational Performance Measurement: Sales, Direct Cost Variances, and the Role of Nonfinancial

Performance Measures

Teaching Notes for Readings

Reading 14-1: D. Johnsen and P. Sopariwala, “Standard costing is alive and Well at Parker

Brass,” Management Accounting Quarterly (Winter 2000), pp. 12-20.

The Brass Products Division at Parker Hannifin Corporation is a world-class manufactures of tube and

brass fittings, valves, hose, and hose fittings. Despite the introduction of popular new costing systems, the

Brass Product Division at Parker Hannifin Corporation is still using a traditional standard costing system

and making it work.

Discussion Questions:

1. What features in the firm’s standard costing that make it a success?

Among features that the Brass Products Division at Parker Hannifin Corporation introduced into its

standard costing systems and variance analyses are:

Disaggregated product line information – Earnings statements are prepared for each product line.

Product line managers are required to provide an explanation for variances exceeding 5% of sales

variances by part number, by job, or by high dollar volume.

Employee training and empowerment – Meetings are held with the hourly employees to explain

variances and earnings statements for their product lines.

2. In addition to variances seen in the textbook Parker Brass created several new variances.

Describe these variances. Why are these variance added at Parker Brass?

The firm has created three new variances to adapt its standard costing system to its particular business

environment:

Chapter 14 – Operational Performance Measurement: Sales, Direct Cost Variances, and the Role of Nonfinancial

Performance Measures

Reading 14-2: C. B. Cheatham and L. R. Cheatham, “Redesigning Cost Systems: Is Standard

Costing Obsolete?” Accounting Horizons (December 1996), pp. 23-31.

The article shows some new ways to analyze standard cost data, going beyond the traditional emphasis on

production costs variances that focus on price and efficiency. Variances for product quality are developed

and explained, as well as sales variances based on sales orders received and orders actually shipped.

There is also a discussion of how to incorporate activity-based costing, and continuous standard

improvement, including benchmarking and target costing.

The main premise of the article is that standard cost systems are the most common cost systems in

use, and while there are a number of limitations to these systems, a careful and creative effort can

transform them into more useful cost systems.

Discussion Questions:

1. What are the main criticisms of traditional standard cost systems?

The main criticisms mentioned in the article include an over-emphasis on price and efficiency to the

exclusion of other CSFs such as quality, timeliness, and customer satisfaction. Other criticisms include

2. What is meant by “push through” production? Is it preferred to “pull through” production, and

why?

Push-through production is associated with plants that work from large amounts of raw materials and

work-in-process to move work from operation to operation, with specialized work roles. The objective

3. What are the best ways to make standard cost systems more dynamic?

The article suggests that standard cost systems can be made more dynamic through regular review and

4. Should a firm follow the suggestions make in this article to add additional variances to its

standard costing system?

The article makes some good suggestions for expanding the role and use of standard costing, to

include new variances such as the raw materials and finished goods inventory variances, the quality

variance, and the sales order variance. Each of the variances provides potentially useful additional

information for the user of a standard costing system. For example, the quality variance can be used

14-4

Education.

Chapter 14 – Operational Performance Measurement: Sales, Direct Cost Variances, and the Role of Nonfinancial

Performance Measures

Reading 14-3: T. Mitchell and M. Thomas, “Can Variance Analysis Make Media Marketing

Managers More Accountable?” Management Accounting Quarterly (Fall 2005), pp. 51-61.

This article discusses, within the context of a marketing application, an alternative method for

decomposing a total standard cost variance. The authors posit that in such applications the joint variance

(that in conventional practice is assumed to be small) can be significant in amount and therefore

invalidate conventional methods that include the joint price-cost variance as part of the price variance.

However, the treatment proposed by the authors for the joint price-quantity variance differs from the

“three-variance” solution found in some cost/managerial accounting texts.

Discussion Questions:

1. Explain what is meant by the term “joint variance” as this term is used in standard cost systems

used for control purposes.

Any variable cost (e.g., labor) is a function of two factors: price (p) and quantity (q). Thus, if during a

given period there is a flexible-budget variance for a given variable cost, that variance can

theoretically be decomposed into a price and quantity variance, thereby attributing a portion of the

variance to each of the two input factors: price paid for labor (p) and quantity of labor hours used (q)

2. Explain what the authors of this article mean when they describe their proposed approach for

standard cost variance decomposition as a “geometric solution.”

The authors argue that even the three-variance approach discussed in some textbooks (see (1) above)

is fundamentally flawed in the sense that does not consistently produce accurate results. As a practical

matter, however, the authors admit that this issue is of practical importance only when standards are

“loose” and so-called joint variances are large.

As noted by the authors, the “joint price-quantity” variance is sometimes called the “unexplained

14-5

Education.

3. Explain the term “Minimum Potential Performance Budget” model. How is this concept

employed in the variance decomposition process recommended by the authors?

The “minimum potential performance budget” is a concept that can be used to implement the

“geometric solution” presented by the authors (see (2) above). That is, it is proposed as a method to

correct the calculation errors associated with either the two-variance or the three-variance approaches

used in practice.

The model proposed by the authors changes the manner in which the two primary (price and quantity)

4. What are the primary advantages and primary disadvantages of the variance-decomposition

model recommended by the authors of this paper?

These are listed in the article (see Case/Readings Supplement, page 14-30):

Advantages

Disadvantages

the underlying concept, based on geometric relationships, may not be intuitive to some

14-6

Education.

Chapter 14 – Operational Performance Measurement: Sales, Direct Cost Variances, and the Role of Nonfinancial

Performance Measures

Reading 14-4: Helping Students See the ‘Big Picture of Variance Analysis by Neal VanZante,

Management Accounting Quarterly, Vol. 8, No. 3 (Spring 2007), pp. 39-47.

This paper presents two examples that can be used to reinforce concepts and procedures students learn in

text Chapters 14 through 16. The first example, Fernandez Company, can be used as a comprehensive

review of all three chapters; the second example, Roger Company, can be used in conjunction with

Chapter 14 if additional coverage of the joint price-quantity variance for direct materials (DM) is desired.

The Fernandez Company example requires students to first calculate the total flexible budget variance (in

operating income) for a period and then breakdown this variance into its constituent parts (selling price

variance, various cost variances, etc.).

Discussion Questions:

1. What is meant by the total operating-income variance for a given accounting period? What

alternative names are there to describe this variance?

As described both in the text (Chapter 14) and this article, the total operating income variance for any

given period is the difference between actual operating income and the operating income reflected in

the master (static) budget for the same period. This variance is also referred to as the master budget

2. What would be a first-level breakdown of the total variance described above in (1)?

As implied by this question, the total operating-income variance for a period can be broken down into

finer and finer components. A first-level breakdown of the total variance would be to calculate a sales

3. How can the total flexible-budget variance be broken down (i.e., what are the constituent parts

of this total variance)?

As illustrated in the article and in the text (viz., Exhibits 14.2 and 14.4), the total flexible-budget

variance for a period is equal to the difference between actual results (revenue, variable costs, and

fixed costs) and flexible-budget results. As such, volume is held constant while we let selling price

14-7

Education.

Chapter 14 – Operational Performance Measurement: Sales, Direct Cost Variances, and the Role of Nonfinancial

Performance Measures

4. Explain the total sales volume variance for a period. How can this total variance be

decomposed?

As indicated both in the article and the textbook, the sales volume variance for a single-product firm

represents the effect on operating income of selling more or fewer units than was envisioned when the

master budget was prepared. Because this variance is basically calculated as the difference between

5. Explain the meaning of the joint price-quantity variance that is the basis for the discussion in

the Roger Company case.

When there is a mix of resource inputs (e.g., labor and materials) and the actual mix of resources

consumed differs from the budgeted mix, it is possible to further breakdown the quantity (efficiency)

14-8

Education.