Chapter 19 – Strategic Performance Measurement—Investment Centers

19-36 (Continued-1)

Further, such differences likely have incentive effects. For example, if the

division in question currently generates an ROI greater than, say, 15% (or

even 11%), it is not clear that the manager of the division would be

motivated to accept the proposed investment, in spite of the fact that the

proposed investment is justified on a present-value (i.e., discounted cash

flow) basis.

In summary, this question ultimately deals with the incentive effects of using

one method for making long-term investment decisions (DCF, as

discussed in Chapter 12) and a different method for evaluating the

subsequent financial performance of the decision-maker and operating unit

(e.g., ROI based on accrual-accounting data). If NBV is used as the basis

for measuring the level of invested capital for ROI calculations, there will be

(2) this negative incentive effect can, to some extent, be ameliorated

through the use of gross book values when measuring the investment base

in the ROI calculation. The important point, however, is the ability to identify

incentive effects associated with different implementation options of the

ROI performance metric.

4. Year-by-Year ROIs, based on average NBV of the investment and accelerated

(DDB) depreciation:

Year

Income Prior

to Deprec.

DDB

Depreciation

Charge

Operating

Income After

Depreciation

Average

NBV of

Asset

ROI

Based on

NBV

1 $360,000 $480,000 ($120,000) $960,000 (12.50%)

2 $360,000 $288,000 $72,000 $576,000 12.50%

3 $360,000 $172,800 $187,200 $345,600 54.17%

19-31

Education.

Chapter 19 – Strategic Performance Measurement—Investment Centers

19-36 (Continued-2)

Year-by-year ROIs, based on GBV of the investment and DDB depreciation

(with a switch to SL depreciation in year 4):

DDB Operating Average

ROI Based

on

Income Prior Depreciation Income After Gross Book on Gross

Year to Deprec. Charge Depreciation Value Book Value

1 $360,000 $480,000 ($120,000) $1,200,000 (10.00%)

2 $360,000 $288,000 $72,000 $1,200,000 6.00%

Summary: the above results demonstrate that the bias associated with

the use of NBV versus GBV of the asset (investment) base is even more

5. Year-by-Year Financial Results: Residual Income (RI)

a. Using average NBV of long-lived assets as the investment base, and SL

depreciation (per requirement 1 above):

Income

Operating

Income

Less: 8%

Imputed

Year

Prior to

Deprec.

Depreciation

Charge

After

Depreciation

Capital

Charge

Residual

Income (RI)

1 $360,000 $240,000 $120,000 $86,400 $33,600

2 $360,000 $240,000 $120,000 $67,200 $52,800

19-32

Chapter 19 – Strategic Performance Measurement—Investment Centers

19-36 (Continued-3)

b. Using GBV of long-lived assets as the investment base, and SL

depreciation (per requirement 2 above):

Income

Operating

Income

Less: 8%

Imputed

Year

Prior to

Deprec.

Depreciatio

n Charge

After

Depreciation

Capital

Charge

Residual

Income

1 $360,000 $240,000 $120,000 $96,000 $24,000

2 $360,000 $240,000 $120,000 $96,000 $24,000

c. Using NBV as the investment base and DDB depreciation (per

requirement 4(1) above):

Year

Income

Prior to

Deprec.

Depreciation

Charge

Operating

Income After

Depreciation

Less: 8%

Imputed

Capital

Charge

Residual

Income

1 $360,000 $480,000 ($120,000) $76,800 ($196,800)

2 $360,000 $288,000 $72,000 $46,080 $4,800

3 $360,000 $172,800 $187,200 $27,648 $139,200

19-33

Chapter 19 – Strategic Performance Measurement—Investment Centers

19-36 (Continued-4)

d. Using GBV as the investment base and DDB depreciation (per

requirement 4(2) above):

Year

Income

Prior to

Deprec.

Depreciation

Charge

Operating

Income After

Depreciation

Less: 8%

Imputed

Capital

Charge

Residual

Income

1 $360,000 $480,000 ($120,000) $96,000 ($216,000)

2 $360,000 $288,000 $72,000 $96,000 ($24,000)

The preceding results show that, as in the case with ROI, there is no

unambiguous way to calculate the residual income (RI) financial

performance indicator. Differences exist as to how RI is calculated.

These differences cause year-to-year differences in RI amounts, as

demonstrated by the calculations in (a) through (d) above. Note that the

differences observed in requirement 5 are attributable both to the

depreciation method chosen and to how the level of investment was

defined (operationalized). As shown above, these differences can result

Again, the basic issue is the existence of a disconnect between the

model used for long-term decision-making (i.e., DCF) and the model

used subsequently for assessing financial performance. One possibility,

subsequently evaluating actual performance.

19-34

Education.

Chapter 19 – Strategic Performance Measurement—Investment Centers

19-36 (Continued-5)

An Excel file solution for this assignment is embedded (below) into this

Word solution file. To access the Excel file solution, place the cursor

anywhere over the object, right-click, choose “Worksheet Object,” then

choose “open.”

Pr. 19-36 7e.xlsx

19-35

Education.

Chapter 19 – Strategic Performance Measurement—Investment Centers

19-37 Return on Investment (ROI), Present-Value Depreciation;

Spreadsheet Application (60 Minutes)

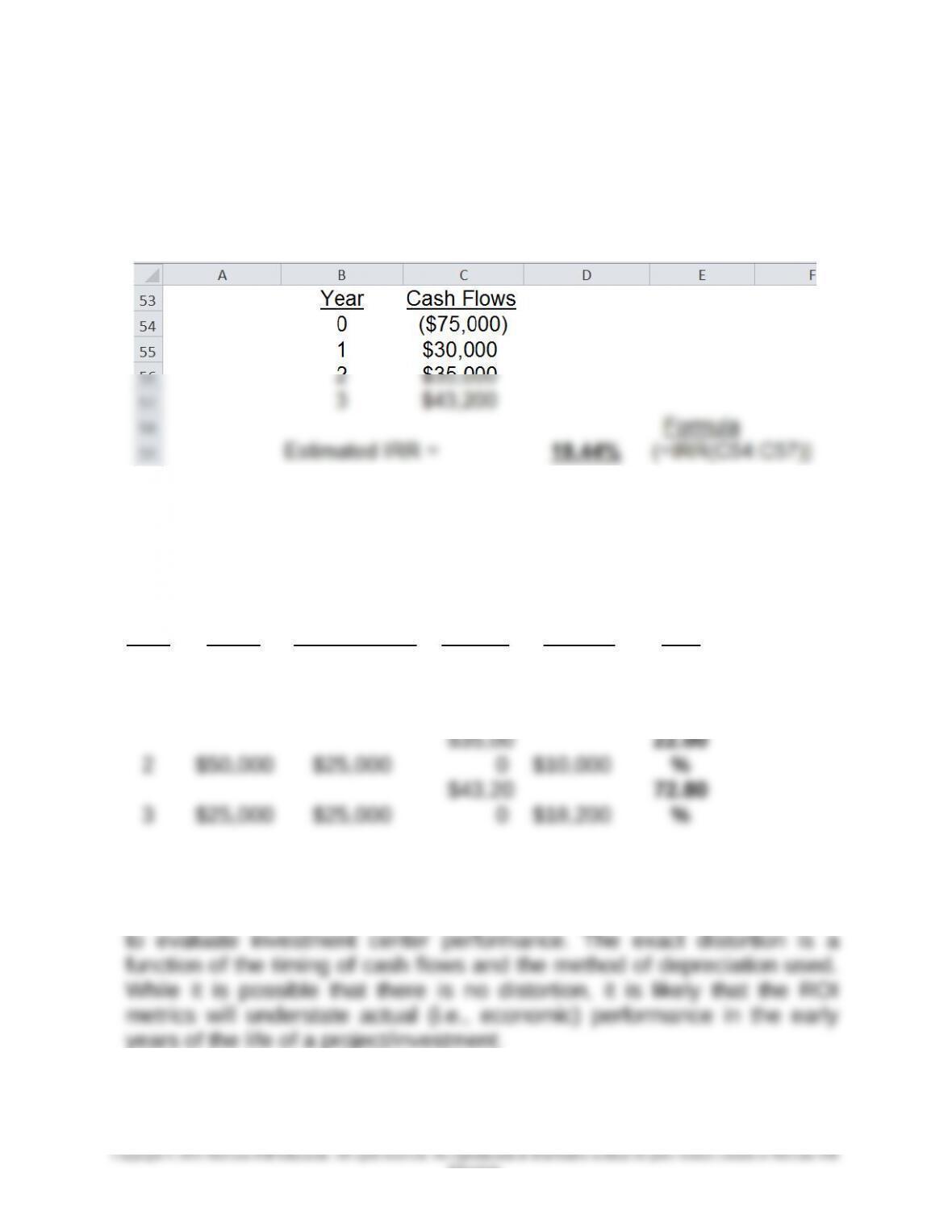

1. Determining the IRR of the proposed investment (using the built-in

function in Excel):

2. Year-by-Year Accounting Rate of Return (SL depreciation);

Investment measured as beginning-of-year book value

BOY

Book SL Cash Operating

Year Value Depreciation Inflows Income ROI

0

1 $75,000 $25,000

$30,00

0 $5,000 6.67%

$35,00

22.00

Given the required rate of return for this company (15%), this project will

appear unsatisfactory in Year 1. The point of this example is to illustrate

the bias for new investment that exists when accrual-based data are used

19-36

Education.

Chapter 19 – Strategic Performance Measurement—Investment Centers

19-37 (Continued-1)

3. Year-by-Year ROI, Present-Value Depreciation:

PV of Cash Decrease

Cash Inflows (@ in PV of

Year Flows 19.44%) the Asset

0($75,000) $75,000

$15,41

BOY Book PV Cash

Operatin

g

Year Value

Depreciatio

n Inflows Income ROI

Summary: The use of present-value (i.e., “economic”) depreciation

reduces the negative incentive effects illustrated above in part 2.

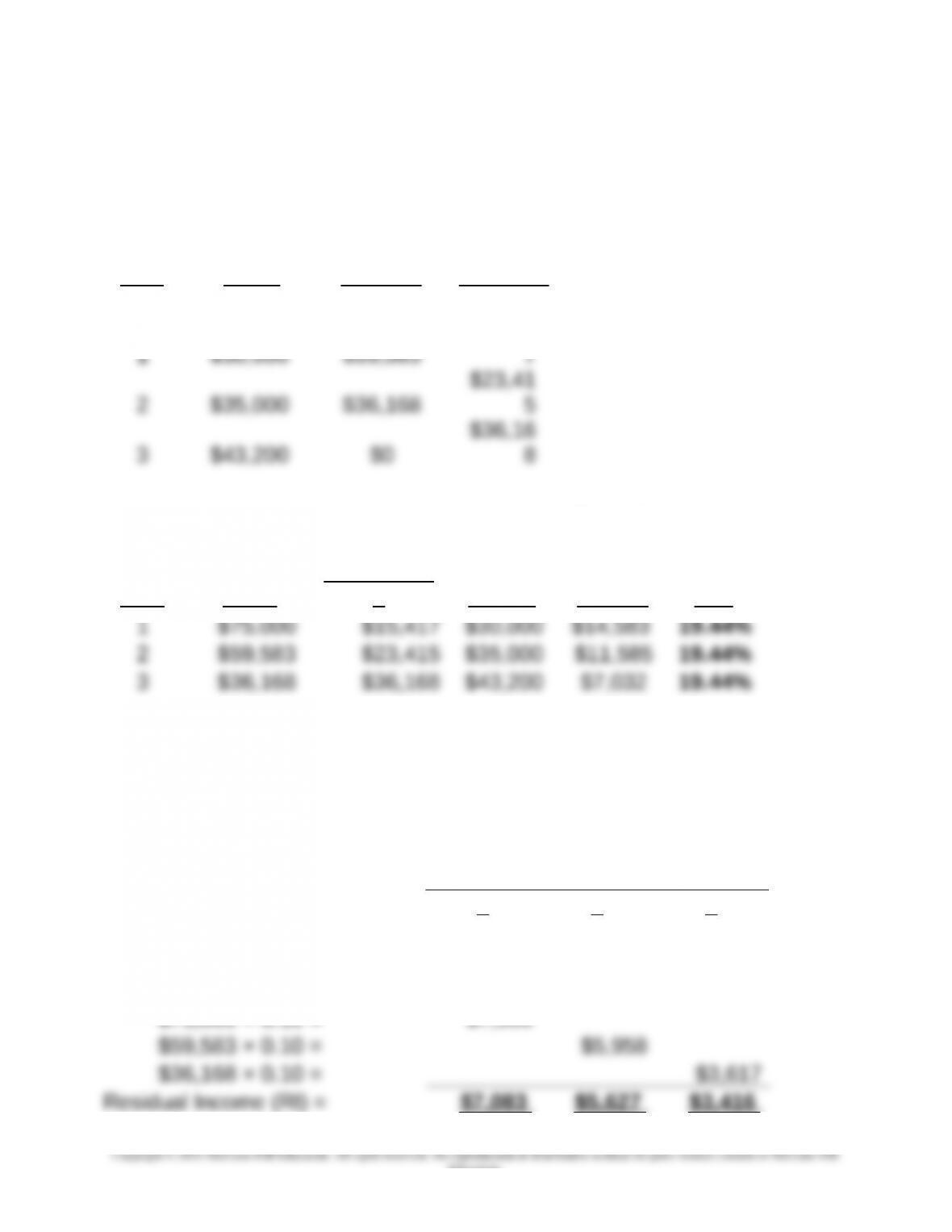

4. Estimated Year-by-Year Residual Income (RI), Present-Value

Depreciation:

Year

123

Cash Inflows $30,000 $35,000 $43,200

Present Value Depreciation $15,417 $23,415 $36,168

Imputed Capital Charge:

$75,000 × 0.10 = $7,500

19-37

Education.

Chapter 19 – Strategic Performance Measurement—Investment Centers

19-38

Chapter 19 – Strategic Performance Measurement—Investment Centers

19-37 (Continued-2)

Using the built-in function (NPV) in Excel, we estimate the following:

Estimated NPV of RIs, at 10% =

$13,65

5

Summary: For an economically desirable project (as in the case here:

IRR > 10%), the RI for each year of a project’s life will be positive so

long as present-value depreciation is used in the calculations. That is, if

(NPV), and the other for evaluating subsequent performance (RI, with

PV depreciation).

An Excel file solution for this assignment is embedded (below) into this

Word solution file. To access the Excel file solution, place the cursor

anywhere over the object, right-click, choose “Worksheet Object,” then

choose “open.”

19-39

Education.

Pr. 19-37 7e.xlsx

Chapter 19 – Strategic Performance Measurement—Investment Centers

19-38 Research Assignment, Strategy (60 minutes, including reading time)

1. As the authors note on page 123 of their article, “Globalization has left

only one true path to profitability for firms operating in high-wage,

developed nations: to base their competitive strategy on exceptional

human capital management (HCM).” In the past, these same firms may

have been able to secure sustainable competitive advantage by

managing their financial or physical capital. Performance-measurement

systems for managing such assets are well-developed and key to

traditional management accounting and control systems. The

2. The overall purpose of the framework proposed by the authors is to

establish empirical linkages between “people” (or, the quality of HCM)

and organizational performance (e.g., sales revenue, factory safety,

student scores on standardized tests, or stock-market returns).

Conceptually, the authors are trying to model key HCM drivers of

five major categories.

From the standpoint of a management accounting and control system,

the key imperative is to focus, for the given organization, on the most

important HCM drivers of organizational success. This requires a

statistical analysis between HCM scores over time (or across

organizational units) and key organizational outcomes (such as

19-40

Education.