Chapter 18 – Strategic Performance Measurement: Cost Centers, Profit Centers, and the Balanced Scorecard

18-62 Contribution Income Statement for Profit Centers (40 min)

1.

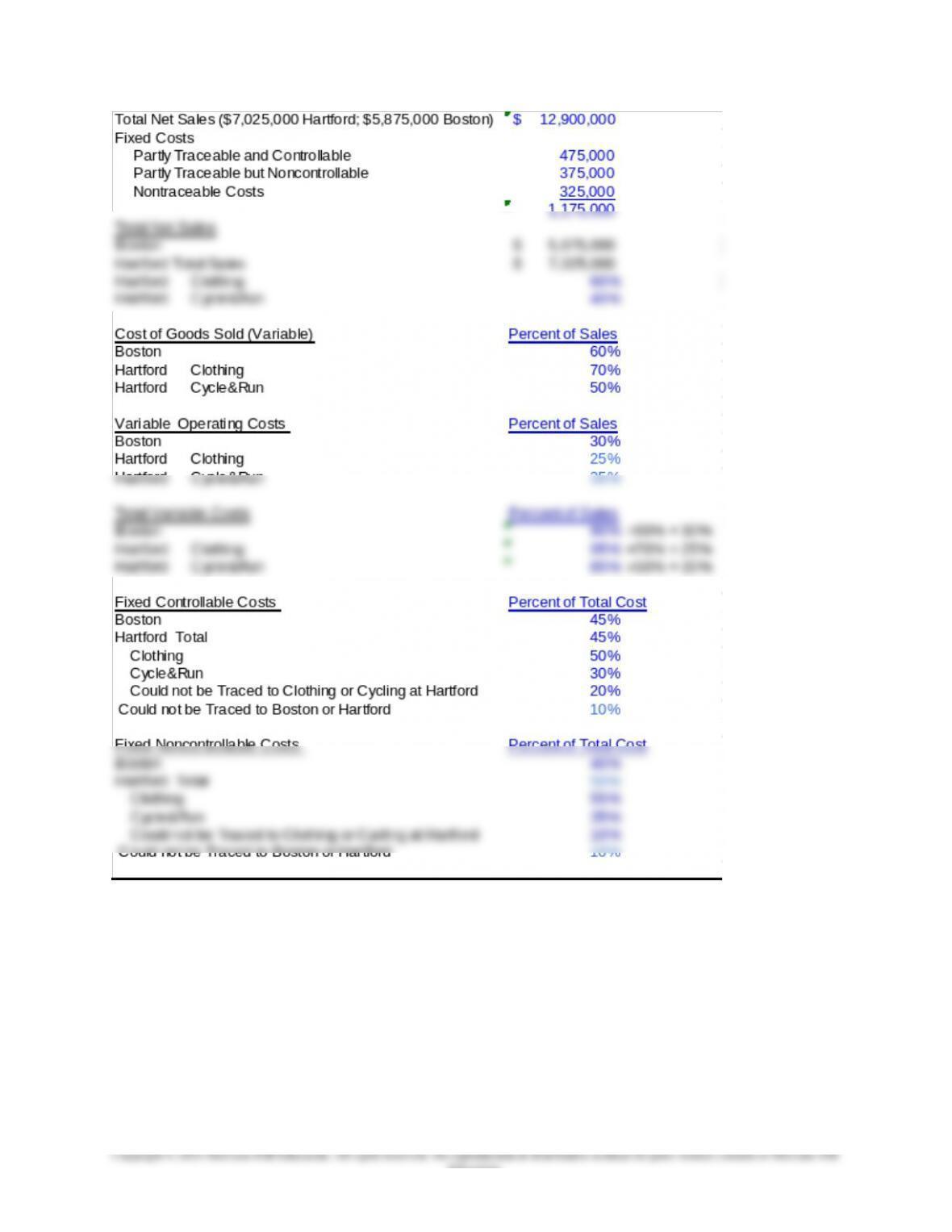

Data Summary:

18-81

Education.

Chapter 18 – Strategic Performance Measurement: Cost Centers, Profit Centers, and the Balanced Scorecard

18-62

(continued -1)

18-82

Education.

Chapter 18 – Strategic Performance Measurement: Cost Centers, Profit Centers, and the Balanced Scorecard

18-83

Education.

Chapter 18 – Strategic Performance Measurement: Cost Centers, Profit Centers, and the Balanced Scorecard

18-62 (continued -2)

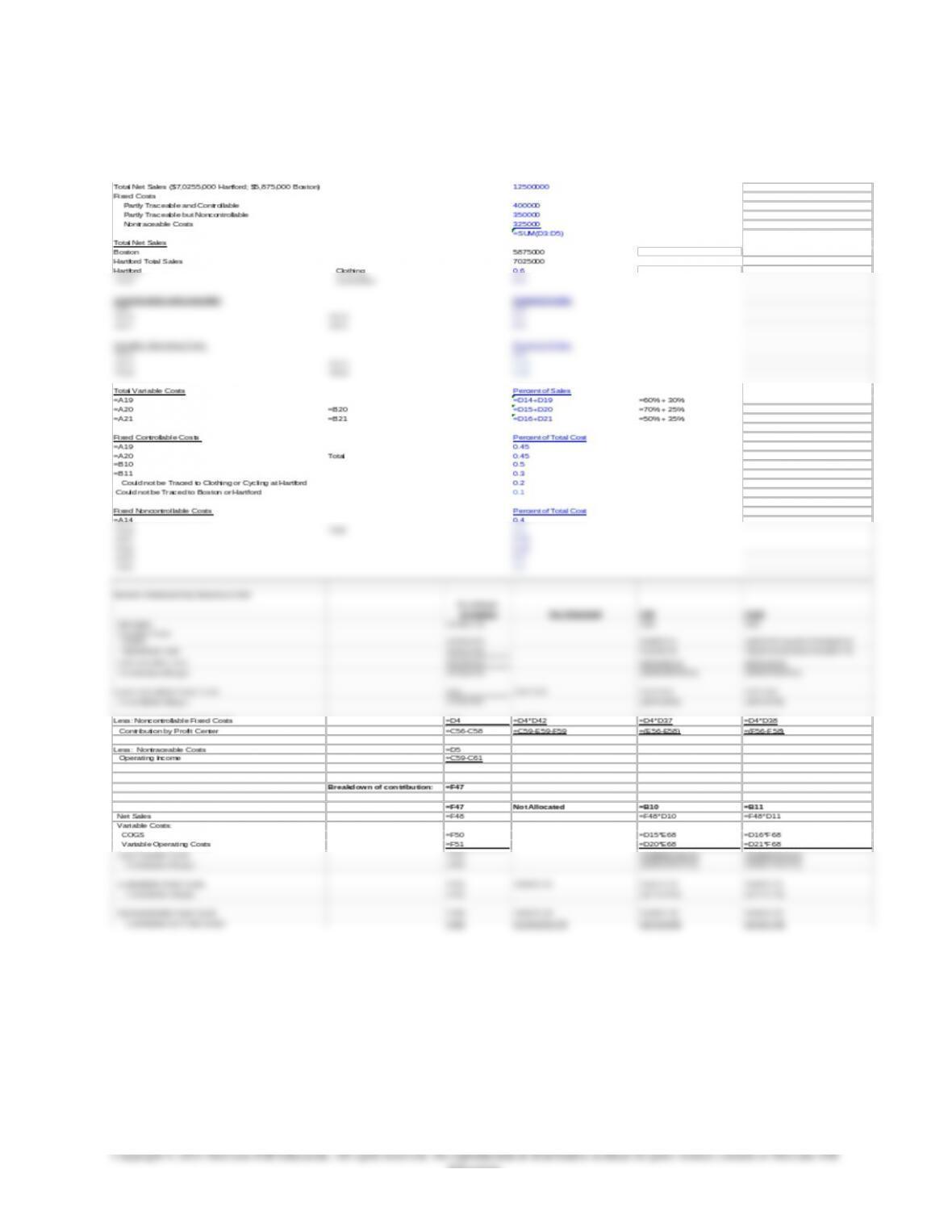

The formulas for the above spreadsheet are as follows:

18-84

Education.

Chapter 18 – Strategic Performance Measurement: Cost Centers, Profit Centers, and the Balanced Scorecard

18-62 (continued -3)

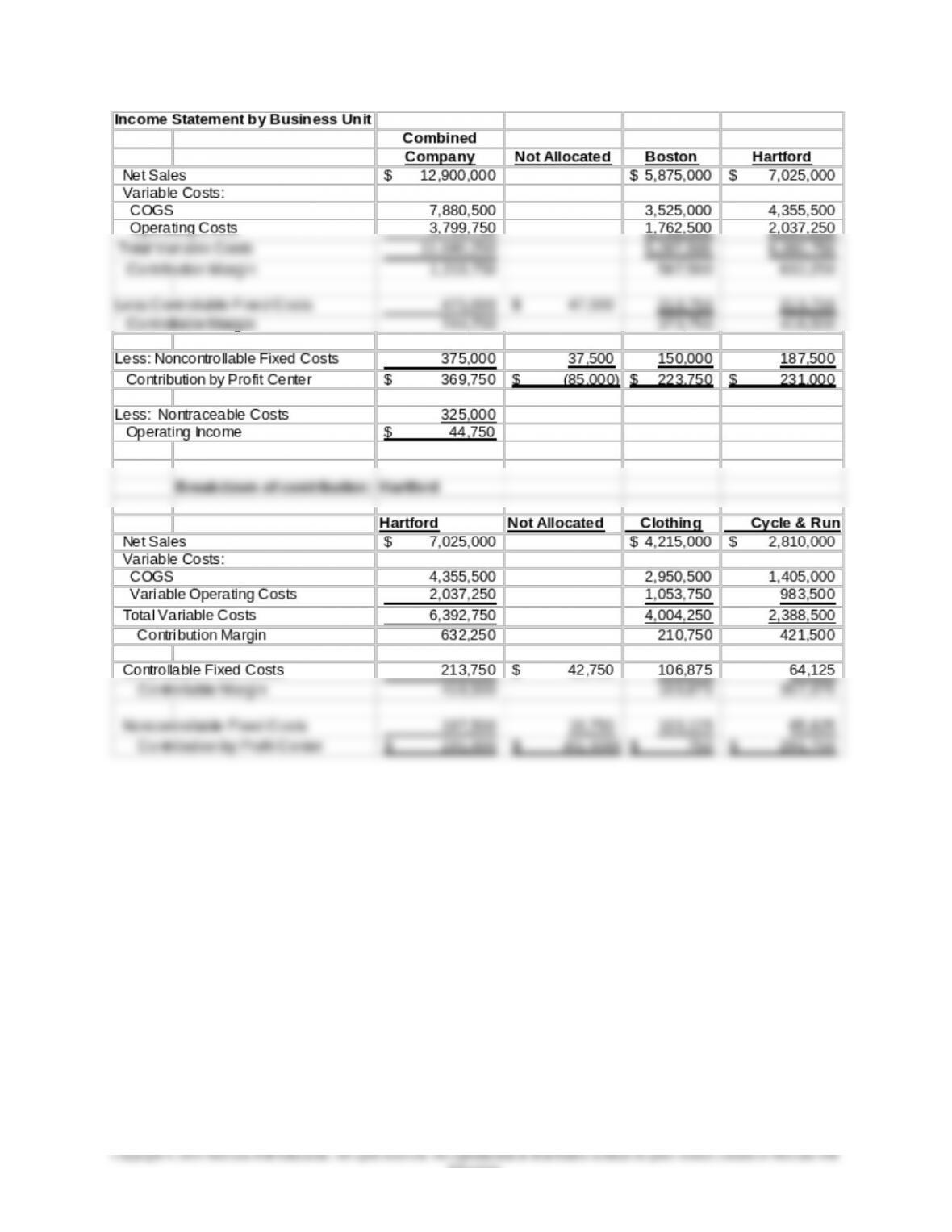

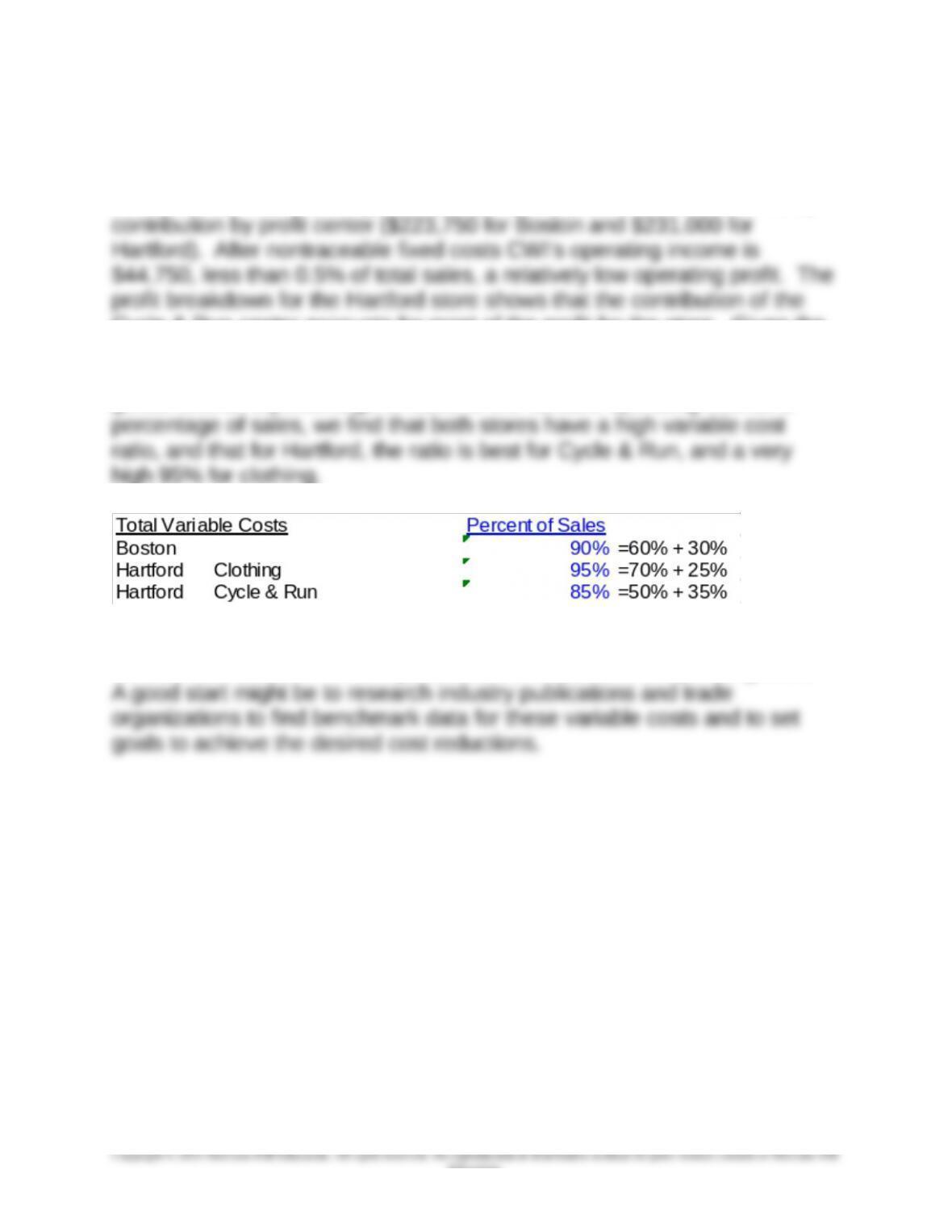

The results of the contribution income statement analysis shows that both

stores are profitable and approximately equally profitable as measured by

Cycle & Run center accounts for most of the profit for the store. Given the

cost estimates, this is not surprising. Note that the variable cost

percentages for the two stores is as follows. Adding the variable cost of

goods sold as a percentage of sales to the variable operating cost as a

The analysis shows that management needs to look for ways to control

variable costs, both in cost of purchases for resale and in operating costs.

18-85

Education.

Chapter 18 – Strategic Performance Measurement: Cost Centers, Profit Centers, and the Balanced Scorecard

18-63 Choice of Strategic Business Unit (20 min)

1. The new office of sustainability is a support department and as such

should be evaluated as a cost center, and since the outputs of the

department will be difficult to measure, at least initially, it should be

established as a discretionary cost center. The department would likely

search for alternatives in the size and type of engines in the trucks that are

used, as well as a new system to schedule routes so as to minimize miles

traveled. Ultimately, as the department begins to realize consistent

success in reducing fuel costs, the evaluation may be changed to some

2. This new department would best be evaluated as a profit center since

its mission is to develop new products and to refine existing products in

order to attract new customers and increase sales. The costs of new

3. This department is best evaluated as a discretionary cost center. The

goal of the department is to identify risk and to make plans accordingly. It

would be difficult to tie this activity to revenues. However, to the extent

18-86

Education.