92. Stulce Inc. produces joint products A, B, and C from a joint process. Information

concerning a batch produced in May at a joint cost of $120,000 was as follows:

A B C Total

Units Sold 2,500 4,000 1,500 8,000

Price (after addt’l processing) $35 $22 $15

Separable Processing cost $35,000 $12,000 $16,000 $63,000

Units Produced 2,500 4,000 1,500 8,000

Total Joint Cost $120,000

Sales Price at Split-off $25 $12 $13

Required:

(Calculate all ratios, percentages, and unit costs to 4 decimal places, for example 33.3333%, and

round all dollar amounts to the nearest whole dollar.):

1. Allocate the joint costs to the joint products using the physical measure method.

2. Calculate the gross margin for each of the three products using the cost allocation for the

physical measure method in part (1) above.

3. Allocate the joint costs to the joint products using the net realizable method.

4. Calculate the gross margin for each of the three products using the cost allocation for the net

realizable value method in part (3) above.

93. The following data on overhead apply to the Acme Manufacturing Company that

manufactures frames for large trucks in three production departments (J-122, J-123, and J-125).

There are two service departments, the Human Resources Department and the Facilities

Department.

Service Departments Production Department

Human Resources

Facilities

J-122

J-123

J-125

Total

Budgeted Overhead $16,000 $35,000 $28,000 $145,000 $185,000 $409,000

Human Resources*

(hours)

400

800

1,200

1,600

4,000

Facilities**

(thousand square feet)

600

400

1,200

1,800

4,000

*Allocated on the basis of hours of usage in the HR department.

**Allocated on the basis of floor space.

Required:

Using hours as the application base for the Human Resources Department and square feet of

floor space for the Facilities Department, apply overhead from these service departments to the

production departments, using the following two methods. Calculate all ratios and percentages to

4 decimal places, for example 33.3333%, and round all dollar amounts to the nearest whole dollar.

(1) Direct method.

(2) Step method (assume the human resources department is allocated first).

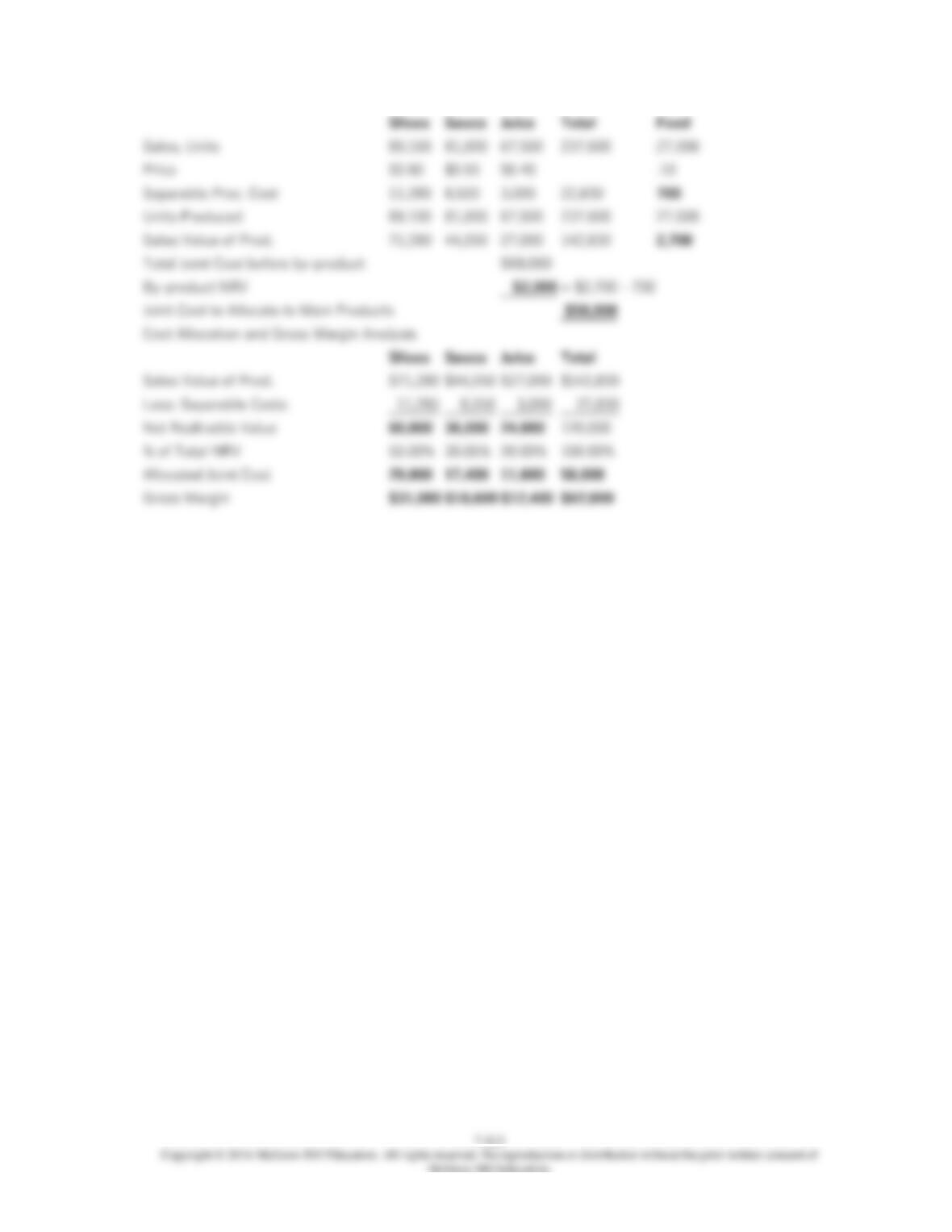

94. Lond Company produces joint products Jana and Reta, and by-product Bynd. Jana is sold

at split-off; Reta and Bynd undergo additional processing. Production data pertaining to these

products for the year ended December 31 were as follows:

Jana Reta Bynd Total

Joint costs

Variable $88,000

Fixed 148,000

Separable costs

Variable $120,000 $3,000 123,000

Fixed 90,000 2,000 92,000

Production in pounds 50,000 40,000 10,000 100,000

Sales price per pound $4.00 $7.50 $1.10

Lond had no beginning or ending inventories and no materials were spoiled in production. Bynd’s

net realizable value is deducted from joint costs. Joint costs are allocated to joint products to

achieve the same gross margin percentage for each joint product.

Required:

Prepare the following information for Lond Company for the year ended December 31, 2013:

1. Total gross margin.

2. Allocation of joint costs to Jana and Reta.

3. Separate gross margins for Jana and Reta.

95. Princess Corporation grows, processes, packages, and sells three apple products: slices

that are used in frozen pies, applesauce, and apple juice. The outside skin of the apple, which is

removed in the cutting department and processed as animal feed, is treated as a by-product.

Princess uses the net realizable value method to assign costs of the joint process to its main

products. The apple skin by-product net realizable value is used to reduce the joint production

costs prior to allocation to the main products. Details of Princess’ production process follow:

• The cutting department washes the apples and removes the outside skin. The department then

cores and trims the apples for slicing. At this point, each of the three main products and the by–

product are recognizable. Each product is then transferred to the next department for final

processing.

• The slicing department receives the trimmed apples and slices and freezes them. Any juice

generated during the slicing operation is frozen with the slices.

• The crushing department trims pieces of apple and processes them into applesauce. The juice

generated during this operation is used in the applesauce.

• The juicing department pulverizes the core and any surplus apple from the cutting department

into a liquid. This department experiences a loss equal to 8 percent of the weight of the good

output produced.

• The feed department chops the outside skin into animal food and packages it. A total of

270,000 pounds of apples entered the cutting department during November. The following

information shows the costs incurred in each department, the proportion by weight (based on

pounds) transferred to the four final processing departments, and the selling price of each end

product. Assume no beginning or ending inventory of apple slices, applesauce, or juice.

Department

Costs

Incurred Proportion of Product by

Weight

Transferred to Departments

Selling Price

per Pound of

Final Product

Cutting $60,000 – –

Slicing 11,280 33% $0.80

Crushing 8,550 30% 0.55

Juicing 3,000 27% 0.40

Feed 700 10% 0.10

Total $83,530 100%

Required:

1. Princess Corporation uses the net realizable value method to determine inventory values for

its main products and by-products. For the month of November, calculate each of the following:

a. Output in pounds for apple slices, applesauce, apple juice, and animal feed.

b. Net realizable value at the split-off point for each of the three main products.

c. Cutting department cost assigned to each of the three main products and to the by-product in

accordance with corporate policy.

d. Gross margin in dollars for each of the three main products.

2. Comment on the significance to management of the gross margin dollar information by main

product for planning and control purposes as opposed to inventory valuation.

3. List the important issues that Princess faces as a global company. What are its critical

success factors? Which key issues arise because Princess operates in several countries? Should

any of these issues affect the way Princess allocates costs, as determined in requirement 1?

96. Ted Brown is the chief financial officer of Haywood Inc., a large manufacturer of

cosmetics and other personal care products. Ted is conducting a financial analysis of the firm’s

line of hand lotions which consists of three products: SkinSalve, SkinCream, and SkinBalm. Total

sales for the three products in the recent year were $400,000, $250,000 and $500,000,

respectively. Because there is a small amount of additional processing cost for each of the three

products, which differs between the products ($20,000, $50,000 and $30,000, respectively), Ted

has been using the net realizable value method for allocating the joint production cost of

$500,000. However, he is not satisfied with the result of somewhat different gross margin

percentage ratios (gross margin/sales) for the three products when using this approach. He

knows only of the physical measure method, the sales value at split-off method, and the net

realizable value method for allocating joint cost.

Required:

Prepare a new cost allocation for Ted so that after allocation of joint costs and separable costs,

the gross margin percentage is the same for all three products.