11-30 (continued-5)

Note that the products have the same per unit profit, but Flash has

the higher contribution margin per unit, and Clash has the higher

contribution per direct labor hour (DLH). Thus, Flash would be the

more profitable product without a labor constraint, while Clash is the

DLHs would then be devoted to the production of Flash.

g. Special-Order Pricing

on each meal. However, in a special-order situation the fixed costs

are irrelevant, and Barry should be willing to do business for any price

above variable cost of $2.00. Thus, the tour operator’s deal is a good

one for Barry. As long as there is space for the additional meals, and

since daily fixed costs are unaffected by the additional patrons, any

price above $2.00 should be acceptable.

More generally, the minimum selling price per unit = incremental

costs (variable + fixed + opportunity):

Out-of-pocket costs:

Variable out-of-pocket costs per meal $2.00

business.

11-30 (continued-6)

The idea of agreeing to serve 200 patrons on any given day presents

a problem with limited capacity. In this case, 100 of the regular

The above can be reflected in a general reporting framework, as

follows:

Number of patrons per month 200

Special-order price offered by tour company $3.00 (given)

Incremental costs per tour-bus meal:

Variable out-of-pocket costs per meal $2.00

Fixed out-of-pocket costs per meal $0.00

Opportunity cost per meal:

PROBLEMS

11-31 Budgeting and Sustainability (75-90 minutes) (note: this is Pr. 10-58)

Requirement 1: Short-Term Financial Analysis

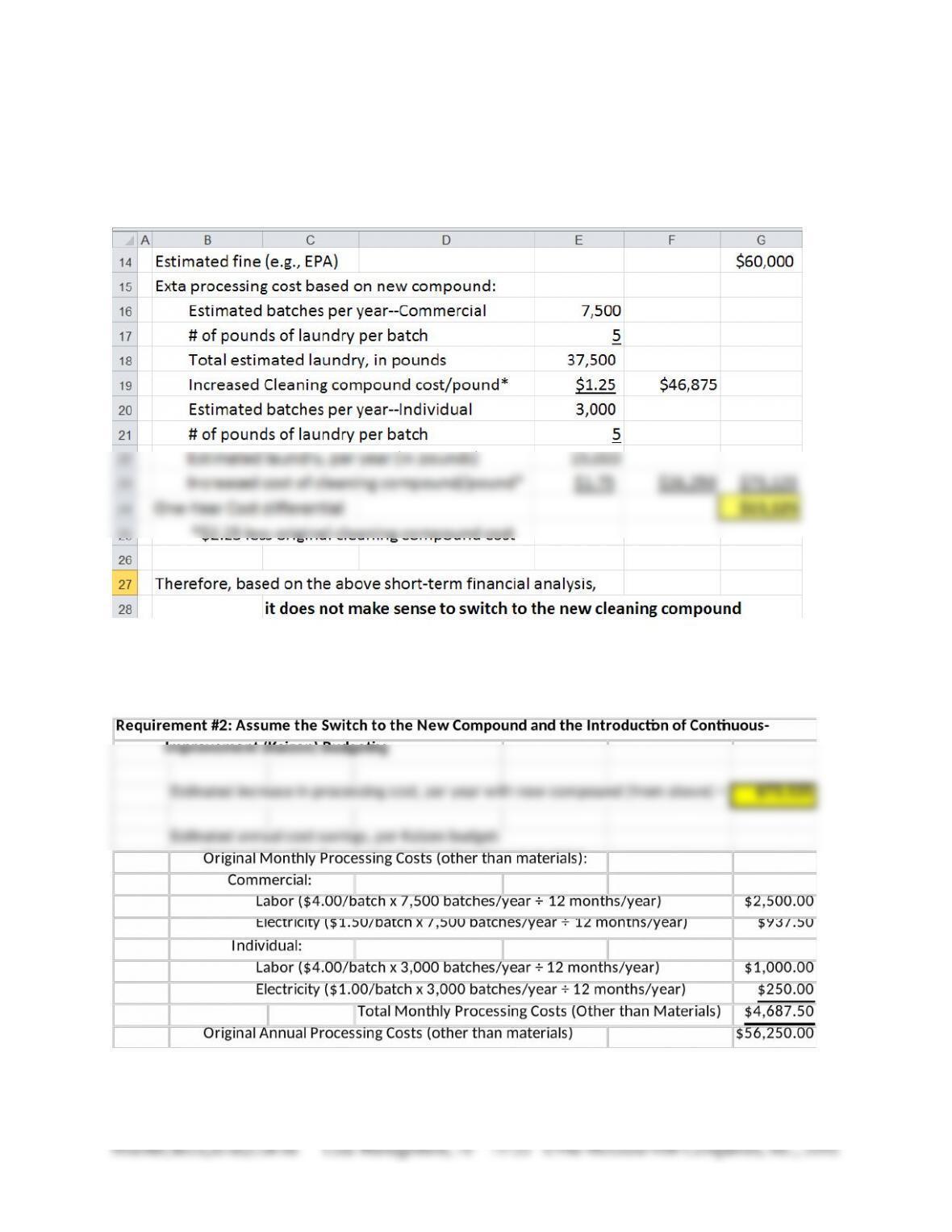

For purposes of illustration (and for Requirement 3 below), the cell

reference for $13,125 (above) is G24; the cell reference for $60,000

(above) is G14.

Cell references: $73,125 = cell G32 (=G23); $4,687.50 = cell G42 (=SUM(G37:G41));

$56,250.00 = cell G43.

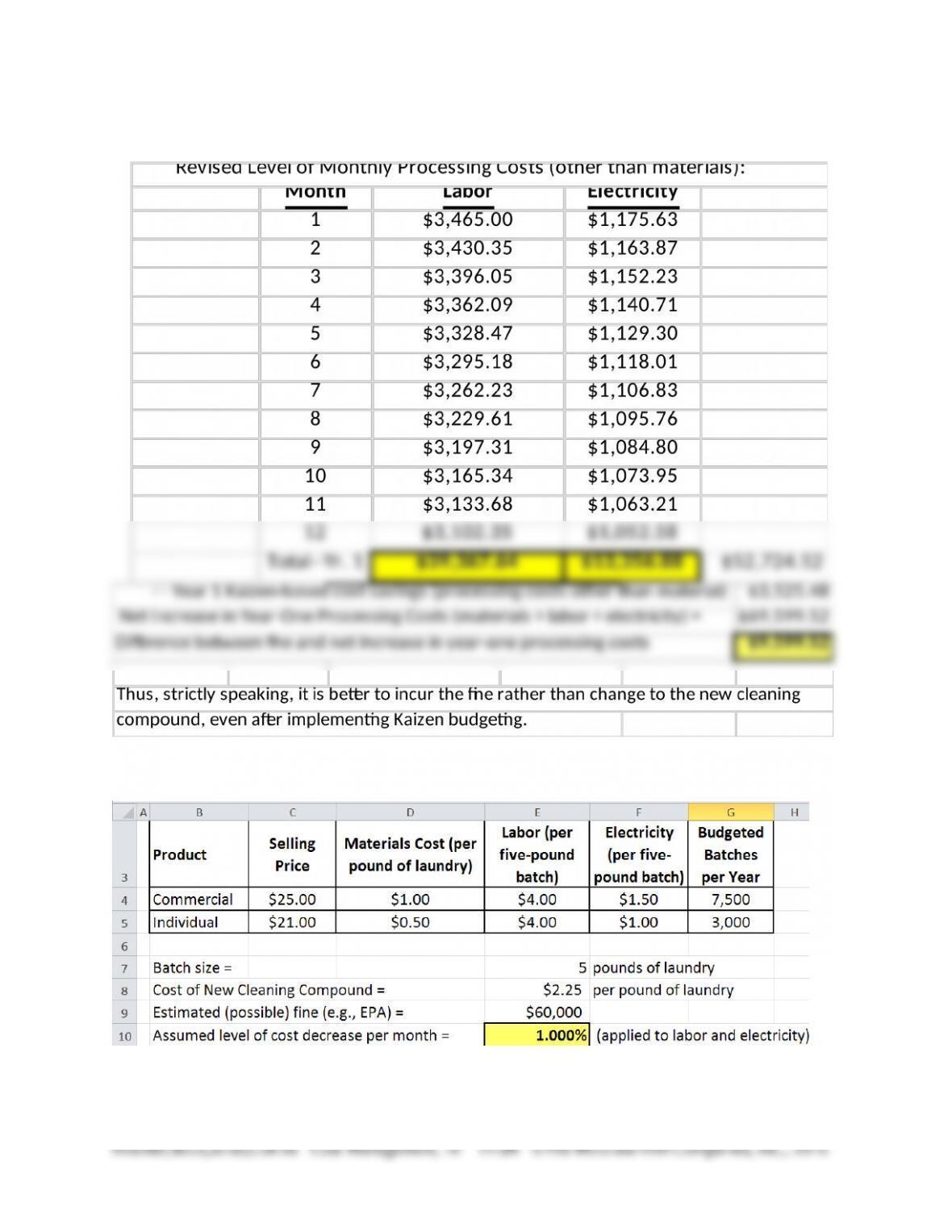

11-31 (Continued-1)

For requirement 3 (below), assume the following input data:

11-31 (Continued-2)

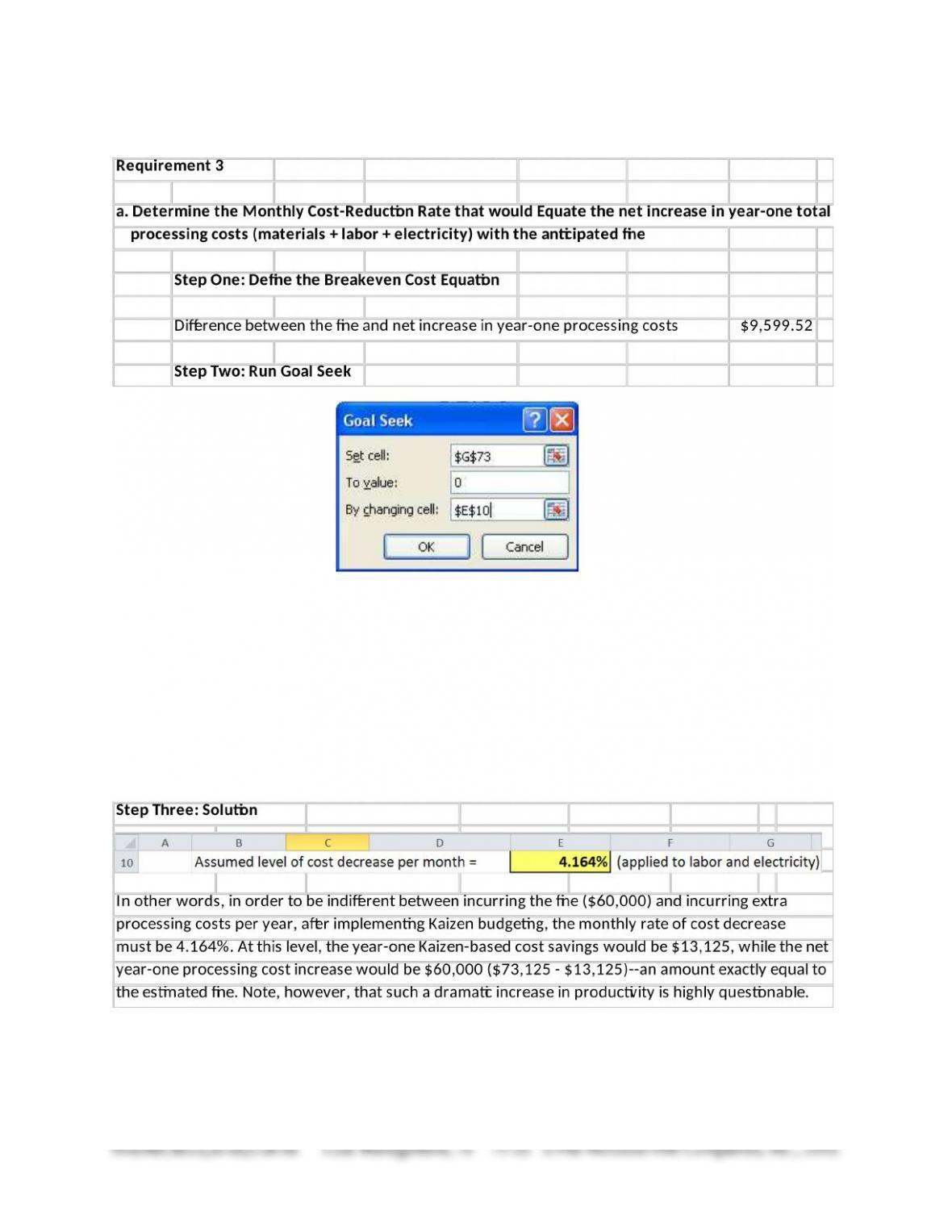

Note: cell E10 contains the assumed monthly rate of cost decrease; cell G73

contains arithmetic difference between the cost of the fine and the net increase in

processing costs—other than materials cost, and after implementing Kaizen

budgeting. The value “0” in the above formulation essentially solves for the

breakeven level: that is, the rate of monthly cost savings needed to equate the

value of the fine and the increased processing costs due to the new compound, but

after implementing Kaizen. As shown below, Goal Seek provides the answer:

4.164% per month.

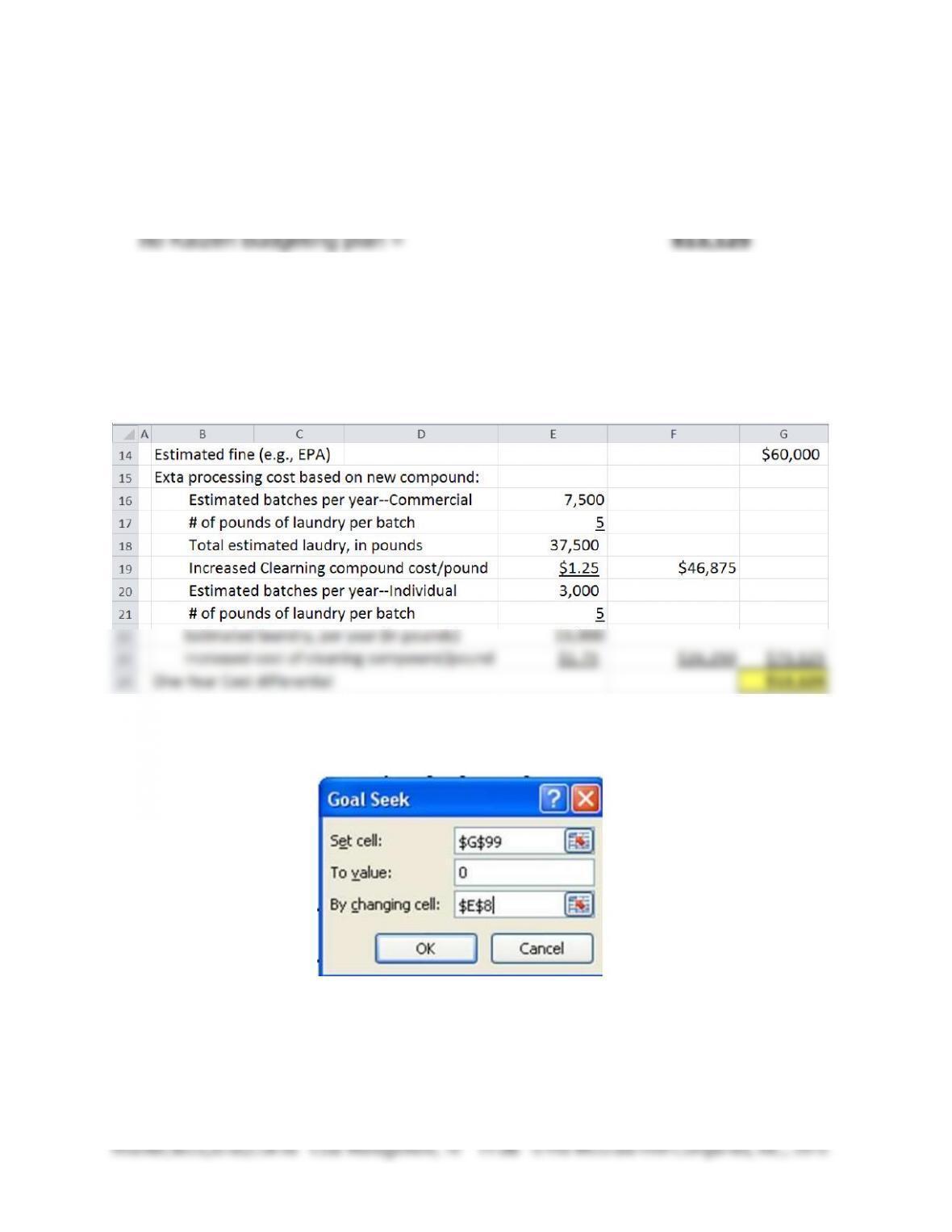

b. The cost per pound for the new compound that would equate the anticipated fine with

the net year-one costs, assuming no Kaizen budgeting plan (i.e., no reduction per

month in processing costs):

11-31 (Continued-3)

Step One: Set Up the Cost Equation

Cost differential: anticipated fine and net one-year processing costs, with

Note: the above value is contained (in this example) in cell G99, which

in turn is defined as the contents from cell G24. G24 contains the

difference between the anticipated cost of the fine, $60,000 (entered in

cell G14) and the expected increase in material cost associated with the

use of the new compound (G23), as shown below:

Step Two: Run Goal Seek

Cell E8 contains the cost of the new compound, per pound of laundry; cell

G99 contains the cost difference: the anticipated fine versus the increased

processing cost attributable to the use of the new compound.

11-31 (Continued-4)

Step 3: Results

course, other considerations may affect the ultimate decision.

4. Operational Changes Needed to Ensure Kaizen Cost Savings

The reduction in labor time might be realized by improving the efficiency

of operations, including a decrease in machine downtime. It is probably

the case that line employees (i.e., operating personnel) would have

suggestions for ways to improve operational efficiency (e.g., changes

that would reduce idle time as well as processing time).

To achieve aggressive cost reductions in labor, however, it might be

necessary to institute some type of employee incentive program.

Savings in electricity consumption may be more difficult to achieve.

Some reduction would likely accompany any planned-for reductions in

labor cost. However, ultimately it may be necessary to invest in more

modern technology to improve electricity consumption. This is

particularly true given recent (and anticipated) increases in utility rates.

Finally, as the present example shows, effective Kaizen budgeting may

require collaborative work with individuals/companies across the value

chain. David Duncan is more likely to achieve his cost-reduction goals

by working with his suppliers. As indicated above, if the cost of the new

compound can be decreased by only $0.25 per pound of laundry

processed, David would be indifferent (solely on an expected cost basis)

11-31 (Continued-5)

between incurring the fine ($60,000) and the increased processing cost

associated with the use of the new compound ($60,000 as well).

5. Other (qualitative) Considerations that Might Affect the Ultimate

Decision:

What impact, perhaps negative, will the Kaizen budgeting approach

have on employee morale?

Will the quest to achieve aggressive levels of cost reduction have a

negative effect on service quality?

Will the use of the new, environmentally friendly cleaning compound

have a beneficial effect on the image of the business and therefore

on sales?

Would the use of the new cleaning compound have a beneficial

impact on employee health/working conditions?

If the existing cleaning compound were to continue to be used, would

it require any special handling costs/preventative measures (e.g.,

employee health and safety)?

Would incurring a fine (rather than incurring increased operating

costs) negatively affect the image of the business, and therefore

future service demand? (Would negative media coverage reduce

demand?)

Does the existing cleaning compound create a hazardous work

environment for employees (the problem is silent on this issue)?

If the existing cleaning compound is considered hazardous to

employee well-being, is there an effect on employee absenteeism?

Duncan’s business essentially consists of two service lines/segments:

commercial and individual. Is there a differential effect on marketing

activity for these two groups? (That is, do these groups differ in their

response to either positive or negative media coverage?)

Would it make more sense for Duncan to invest in new technology,

which might bring the company into full compliance with current

emission requirements?

11-32 Special Order (45 min)

1. Average cost-per-unit calculations, with and without the special sales

order:

Old (prior to special order) average cost per unit:

Total Cost/month $1,362,500

Total Output/month 7,500

Recalculated Average Cost, including Special Sales Order:

Direct labor cost per unit = $375,000 ÷ 7,500 = $50 per unit;

Direct material cost per unit = $300,000 ÷ 7,500 = $40 per unit

Old Total Cost per month $1,362,500

Special-Order Costs:

Direct labor $125,000

Direct material $100,000

Neither of the above two average cost figures is relevant to the decision

at hand: both include sunk costs in the form of fixed manufacturing

overhead and fixed marketing costs, both of which are “sunk” with

2. Short-term profit effect of accepting the special sales order:

Price of special order $115

Relevant Cost = Incremental Cost per Unit:

= (Direct labor, $50 per unit

+ Direct Material, $40 per unit) = 90

3. Breakeven selling price per unit on the special sales order:

The breakeven selling price is the price that would leave the operating

profit for the company unchanged. Alternatively, this can be defined as

the sum of “relevant costs,” that is, incremental variable costs,

incremental fixed costs (if any), and opportunity cost (if any).

In the present case, relevant cost includes only incremental variable cost

(i.e., there is no opportunity cost and there are no incremental fixed

costs):

Relevant Costs:

Incremental direct labor $125,000

4. Other considerations:

a. Is the order likely to lead to further regular business with this

customer?

b. Is the order in the strategic best interest of the firm, for example,

will it support or undermine Award Plus’ desired image in the

market?

c. While Award Plus has just enough capacity to complete the

special order, will there be other costs in addition to the variable

manufacturing costs in order to complete the order, that is, special

tooling or set up costs, etc.

d. See part 5 below.

5. The controller, LePenn, has a conflict of interest in the sourcing of raw

materials for the firm. Cathy has the ethical responsibility under the IMA

Statement of Ethical Professional Practice to bring this matter to the