Chapter 05 – Activity-Based Costing and Customer Profitability Analysis

Chapter 5

Activity-Based Costing and Customer Profitability Analysis

Learning Objectives

LO 5-1 Explain the strategic role of activity-based costing.

LO 5-2 Describe activity-based costing (ABC), the steps in developing an ABC system, and the

benefits and limitations of an ABC system.

LO 5-3 Determine product costs under both the volume-based method and the activity-based

method and contrast the two.

LO 5-4 Explain activity-based management (ABM).

LO 5-5 Describe how ABC/M is used in manufacturing companies, service companies, and

governmental organizations.

LO 5-6 Use an activity-based approach to analyze customer profitability.

LO 5-7 Identify key factors for successful ABC/M implementation.

New in this Edition

Two new “Real World Focus” items; one on ABC to support sustainability initiatives and the

other on the use of TDABC.

Five revised end-of-chapter research problems

Teaching Suggestions

A thorough coverage of activity-based costing and activity-based management is an important

part of the development of strategic cost management. Knowing the “true” costs is critical to attain a

better result for all firms and organizations. It is particularly important for firms with complex operations,

where analysis of cost flows and product profitability are important. Moreover, the concept of activity

analysis has important implications for many cost management methods. For these reasons, we have put

the coverage of ABC very early in the book. This allows us to include activity-based concepts when other

topics are covered in later chapters.

Our teaching plan for ABC costing is to begin with a thorough coverage of the benefits and

limitations of ABC systems, including a discussion of why and when they are preferred to other cost

systems. The coverage focuses on the comparison of the volume-based and ABC systems, looking

particularly at the effects of the systems on such strategic decisions as product line additions or deletions.

5-1

Education.

Chapter 05 – Activity-Based Costing and Customer Profitability Analysis

Assignment Matrix

End-of-Chapter Exercises & Problems Learning Objectives Text Features

7e

EOC

6e

EOC

Transition

6e to 7e

X = included in Connect

Time

1. Strategic Role /objectives of ABC

2. Describe ABC and its steps

3. Volume based and ABC costs

4. Explain ABM

5. Describe how ABM is used

6. Customer profitability

7. ABC/M implementation factors

Strategy

Service

International

Ethics

Sustainability

Brief exercises

5-16 5-16 X 05 min. X

5-17 5-17 X 05 min. X

5-18 5-18 X 05 min. X

5-19 5-19 X 05 min. X

5-20 5-20 X 05 min. X

5-21 5-21 X 05 min. X

5-22 5-22 X 05 min. X

5-23 5-23 X 05 min. X

Exercises

5-24 5-24 – 25 min X X

5-25 Moved to 5-27

5-25 5-27 X 05 min X

5-26 5-26 X 05 min X

5-27 Moved to 5-25

5-27 5-25 X 20 min X X X

5-28 5-28 X 25 min X

5-29 5-29 X 15 min X

5-30 5-30 X 05 min X X

5-31 5-31 20 min X X

5-32 5-32 X 25 min X X X X

5-33 5-33 X 25 min X X X

5-34 5-34 – 15 min X X X X X

Continued on next page …

5-2

Education.

Chapter 5 assignment matrix continued

End-of-Chapter Exercises & Problems Learning Objectives Text Features

7e

EOC

6e

EOC

Transition

6e to 7e

X = included in Connect

Time

1. Strategic Role /objectives of ABC

2. Describe ABC and its steps

3. Volume based and ABC costs

4. Explain ABM

5. Describe how ABM is used

6. Customer profitability

7. ABC/M implementation factors

Strategy

Service

International

Ethics

Sustainability

5-35 5-35 X 25 min X

5-36 5-36 X 25 min X

5-37 5-37 – 10 min X X

Problems

5-38 5-38 Revised – 25 min X X X

5-39 5-39 –25 min X X X

5-40 5-40 Revised – 40 min X X X

5-41 5-41 Revised – 35 min X X X X

5-42 Moved to 5-44

5-42 5-43 Moved to 5-42 – 40 min X X X

5-43 5-44 Moved to 5-43 – 25 min X X X X

5-45 Moved to 5-50

5-44 5-42 –35 min X X X

5-45 5-50 – 30 min X X X X X

5-46 5-46 Revised – 20 min X X X

5-47 5-47 Revised – 20 min X X X X

5-48 5-48 –30 min X X X X

5-49 5-49 –45 min X X

5-50 5-45 – 5 min X X X

5-50 Moved to 5-45

5-51 5-51 –30 min X X X

5-3

Chapter 05 – Activity-Based Costing and Customer Profitability Analysis

Lecture Notes

A. Volume-based Costing. Volume-based costing can be a good strategic choice for some firms. It is

generally appropriate when common costs are relatively small or when activities supporting the

production of the product or service are relatively homogenous across different product lines.

Volume-based overhead rate

1. Plantwide overhead rate

Budgeted (total) overhead

Budgeted (total) direct labor or machine hours

2. Departmental overhead rate

Budgeted departmental overhead

Budgeted departmental direct labor or machine hours

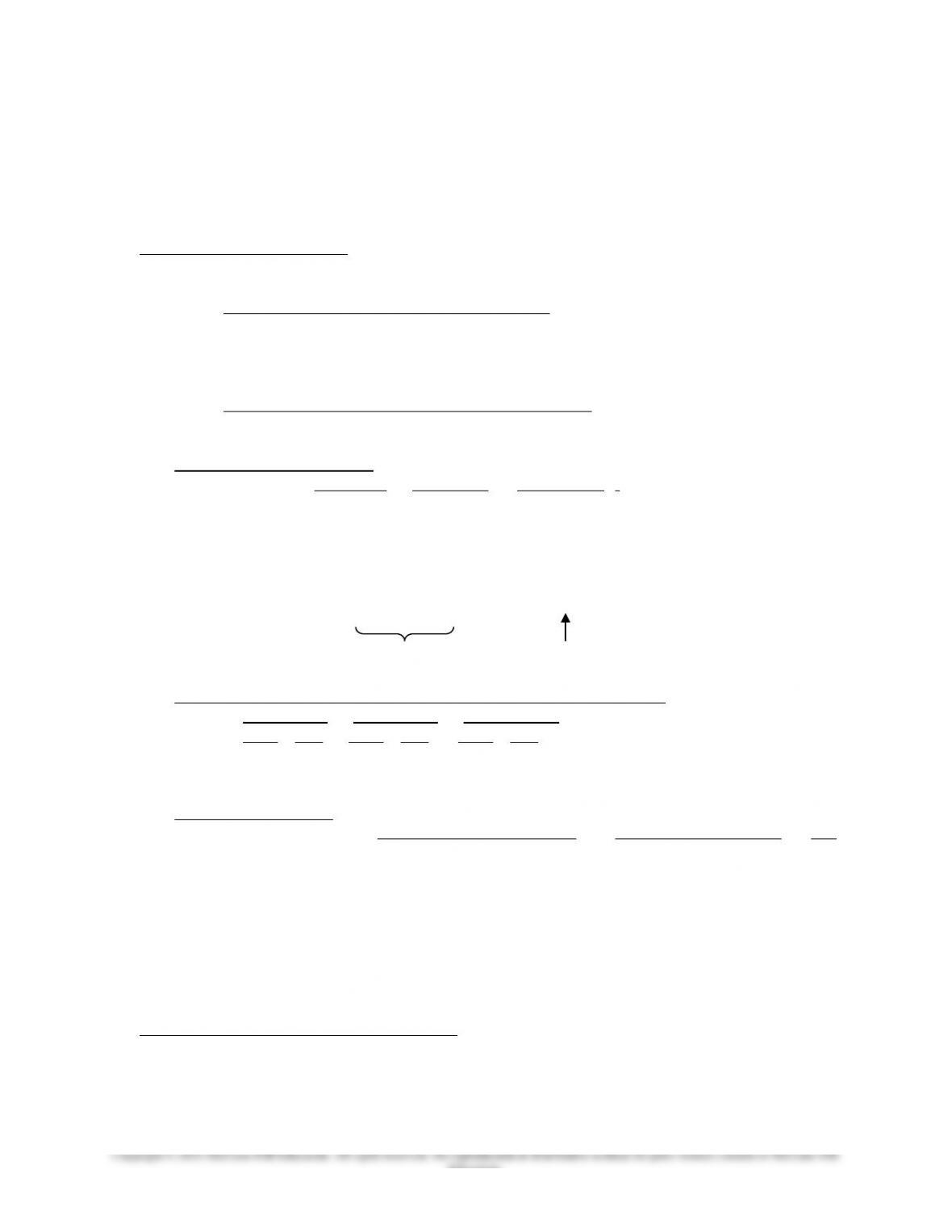

Example:

Volume-based overhead rate:

Division 1 Division 2 Plant Total

DLH 1,000 200 1,200

MH 400 2,000 2,400

Budget $OH $5,000 $7,000 $12,000

Overhead rate:

Per DLH $ 5.00 $35.00 $10.00

Per MH $12.50 $ 3.50 $ 5.00

Departmental Rates Plantwide Rates

Required resources to manufacture one unit each of Widget and Gidget:

Division 1 Division 2 Total

DLH MH DLH MH DLH MH

Widget 20 1 10 5 30 6

Gidget 2 10 6 20 8 30

Factory OH applied to:

Widget Gidget

Using Plantwide rate:

Based on DLH rate $10 x 30 = $300 $10 x 8 = $ 80

Based on MH rate $5 x 6 = $ 30 $5 x 30 = $150

Using departmental rate:

Based on DLH $5 x 20 + $3.5 x 5 = $117.50

Based on MH $5 x 2 + $3.5 x 20 = $80

What is Widget’s “true” OH per unit? $300, $30, or $117.50?

What is Gidget’s “true” OH per unit? $80 or $150?

Limitation of volume-based costing systems

One major limitation of volume-based costing systems is the use of a single plant-wide factory

overhead rate such as direct labor hours or volume-based departmental rates such as machine hours

and direct materials cost to firms with diverse products, processes, and volume. They produce

inaccurate product costs when more factory overhead costs such as setup and materials handling costs

5-4

Education.

Chapter 05 – Activity-Based Costing and Customer Profitability Analysis

are not volume-based, and when firms produce a diverse mix of products with different volume, sizes,

and complexities. In summary, a volume-based costing system is likely to suffer from the following

weaknesses:

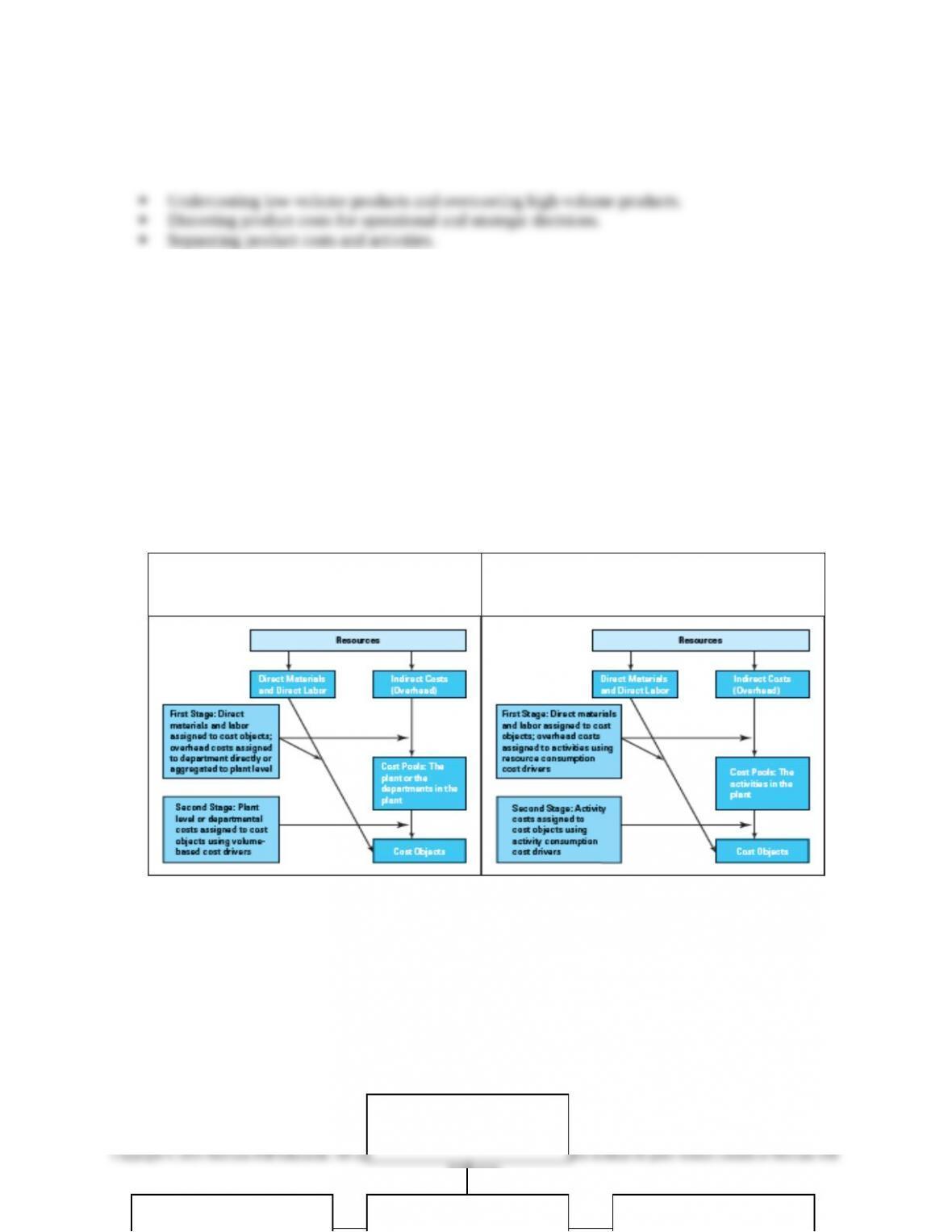

B. Comparison of Volume-based and Activity-based Costing Systems.

1. Volume-based Two-stage allocation process

a. First stage — overhead costs are assigned to cost centers (e.g. departments or individual

operations).

b. Second stage — costs are applied from departments to individual jobs or products using

volume as the main factor.

Note: Where diversity exists between products (e.g. lot size, complexity of

production), overhead costs assignments based on volume will not provide accurate

product costs. Typically high-volume products have higher and low-volume products have

lower cost than their “true” cost.

The two stage cost allocation procedures is illustrated for both the volume-based and the

activity-based methods:

2. Activity-Based Costing (ABC) is a costing approach that assigns costs to products or services

based on their consumption of resources via activities required for the manufacturing of the

products or providing services. It is based on the premise that a firm’s products or services are

performed by activities and that the required activities incur costs. Cost of resources are assigned

to activities, then activities are assigned to cost objects based on their use. ABC recognizes the

causal relationships of cost drivers to activities. ABC’s major advantage is that it improves the

traceability of overhead costs thus minimizes distortion of product costs.

5-5

Education.

EXHIBIT 5.2

The Activity-Based Two-Stage

Procedure

EXHIBIT 5.1

The Volume-Based Two-Stage

Procedure

Input Information

Resources

Performance EvaluationActivities

Chapter 05 – Activity-Based Costing and Customer Profitability Analysis

5-6

Education.

Products and Services