Chapter 5 – Activity-Based Costing and Customer Profitability Analysis

Chapter 5

Activity-Based Costing and Customer Profitability Analysis

Teaching Notes for Cases

5-1 Blue Ridge Manufacturing (Activity-Based Costing for Marketing Channels)

Case Description:

Blue Ridge Manufacturing produces and sells towels for the U.S. “sport towel” market. A “sport towel” is

a towel that has the promotion of an event or a log printed on it. Most often they are used in connection

with major sporting events such as the Super Bowl.

Case Writers: Paul E. Juras and Paul A. Dierks, Wake Forest University; written for the IMA 1994 Student

Case Competition

Teaching Objectives:

The main teaching objective of the case is to illustrate, with an extensive numerical exercise, the use of

value chain analysis for profitability analysis. The analysis follows an ABC model, in which selling and

administrative costs are allocated to customer groups for the purpose of analyzing customer profitability.

Main Points:

Activity-Based Costing

Value Chain Analysis

Customer profitability analysis

Discussion Questions:

1. What is Blue Ridge’s competitive strategy?

The current strategy appears to be a combination of focus (on the southeast states) and cost

leadership. The manufacturing is in a modern plant with upgraded facilities, including the use of ABC

costing for manufacturing costs and the commitment to introducing advanced manufacturing

to be moving to a differentiation strategy. Further evidence of this is the firm is “going national,” it will

focus more on quality, and is interested in identifying the least profitable customers. All this suggests

efforts to differentiate the firm from its competitors.

The case does not provide sufficient information for a thorough strategic analysis. However, the

student’s should be expected to identify strategic issues, as noted above, and also:

a) Is the new ink patented? How soon are competitors expected to meet this new innovation?

b) Are Blue Ridge’s licenses with the sports teams of unique value, or do competitors have the

same access as Blue Ridge?

c) How strong are Blue Ridge’s ties to its customers, especially the large customers? Are these

ties sufficiently strong to protect against competition for the next few years?

d) Has Blue Ridge integrated the marketing and manufacturing strategies, so that they are

consistent? Given the changes in both manufacturing (new ink) and marketing (going national, seeking

more profitable customers), the integration of these functions is important.

2. What type of cost system does Blue Ridge use, and is it consistent with their strategy?

The ABC costing system in use is consistent with the cost leadership strategy. It will also assist

5-1

3. What is Blue Ridge likely to gain from a value chain analysis? What are some of the opportunities for

cost reduction and for value added for the customers?

The value chain analysis can help Blue Ridge better understand its competitive advantage and to

identify opportunities for improving its competitive position.

Cost reduction:

– Can Blue Ridge obtain better terms or prices from its suppliers? Materials cost represents a large

share of total manufacturing cost.

– Use profitability analysis (as illustrated in the computer exercise below) to determine the “full”

costs of each product line and customer group as a basis for identifying and focusing on the most profitable

product lines and customers.

– Technical support requirements

(Does Blue Ridge do design or other service for any of the customers, and if so are they properly charged to

the customer?)

Value Added for Customers

– Develop service links with the larger customers, as in the case of Proctor and Gamble and Wal-Mart;

where the retailer and manufacturer share data so that the manufacturer knows when, where and what to

Computer Assignment:

Develop a spreadsheet analysis, which can be used to assess the profitability of the three customer groups

of Blue Ridge — large, medium and small customer account size. Use the information in Tables 1-4 to trace

and allocate the costs necessary for the analysis.

The solution is shown on the attached spreadsheet. The solution process involves three stages:

Stage 1: Allocate SG & A Costs to SG & A Activities.

1. Collect all SG & A costs incurred in each function (Shipping, Sales, Marketing) as showed in

Table 4A of the case.

2. For each function, collect usage % for each activity (Entering P.O., Commissions, Shipping,

Invoicing, Making Sales Calls, Checking Credit, Samples & Catalog Information, Special

Handling, Distribution Management, Marketing by Customer Type, Advertising & Promotion,

Marketing, Administrative Office Support, and Licenses & Fees) as shown in 4A.

3. Then, allocate function costs to activities by usage %.

Stage 2: Allocate activity costs to Customer Type (Large, Medium, Small).

1. Identify cost drivers (as shown in Table 4) and their consumption statistics for each customer

type (as shown in Table 1).

2. Calculate cost driver consumption % for each customer type.

3. Allocate activity costs to customer type.

5-2

Chapter 5 – Activity-Based Costing and Customer Profitability Analysis

Stage 3: Customer Profitability Analysis.

1. Calculate revenues for each customer group (sales quantities from Table 1 and unit prices

from Table 2).

2. Calculate manufacturing cost (Regular, Mid-size, Hand, Special), customizing cost (Inking,

Embroidery, Dyeing), SG & A cost and total costs for each customer group (using data from

Tables 1 & 2).

3. Calculate customer profits ($102,661, $49,742, -$4,828) and profit per customer ($12,833,

$323, -$6) for each customer type.

Note that the analysis makes it clear the group of large customers provide most of the profits for

Blue Ridge. Show how the cost of purchase orders, shipping, the medium and small customer groups

predominantly cause credit checks, advertising, and marketing. The analysis shows clearly that these two

groups, on a per customer basis, are marginally profitable. This analysis indicates that Blue Ridge should

5-3

Chapter 5 – Activity-Based Costing and Customer Profitability Analysis

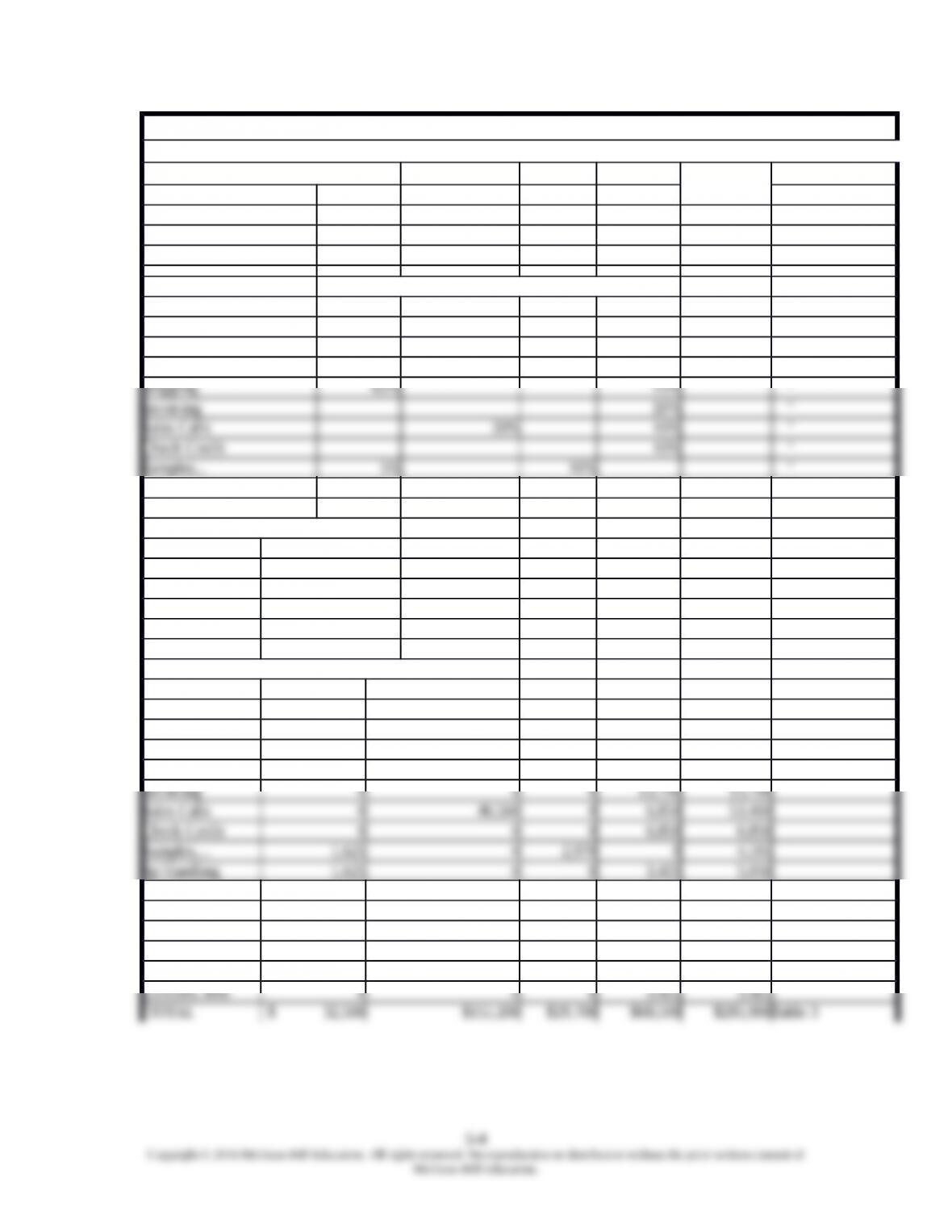

Blue Ridge Manufacturing

First Stage Allocation: Allocate SG&A Costs to SG&A Activities

First: SG&A Costs Total

Assigned

Shipping Sales Marketing Other Source

Administration 17,000 37,400 20,400 56,100 130,900Table 3

Selling 15,500 117,800 9,300 12,400 155,000Table 3

$32,500 $155,200 $29,700 $68,500 $285,900

Percentage of…

Second: SG&A Shipping Sales Marketing Other

ACTIVITIES

Enter P.O. 55% 10% Table 3

Commissions 10% “

Sp Handling 5% 5% “

Distribution 10% 10% “

Marketing, Customer 5% “

Advertising 30% “

Marketing 15% 50% 5% “

Administrative 20% “

Licenses, fees 0% 5% “

TOTAL 100% 100% 100% 100% “

Third: Allocate Costs to Activities

Shipping Sales Marketing Other Total

Assigned

ACTIVITIES

Enter P.O. 0 85,360 0 6,850 92,210

Commissions 0 15,520 0 0 15,520

Shipping 21,125 0 0 10,275 31,400

Distribution 3,250 0 2,970 0 6,220

Marketing, Cust 0 7,760 0 0 7,760

Advertising 0 0 8,910 0 8,910

Marketing 4,875 0 14,850 3,425 23,150

Administrative 0 0 0 13,700 13,700

Chapter 5 – Activity-Based Costing and Customer Profitability Analysis

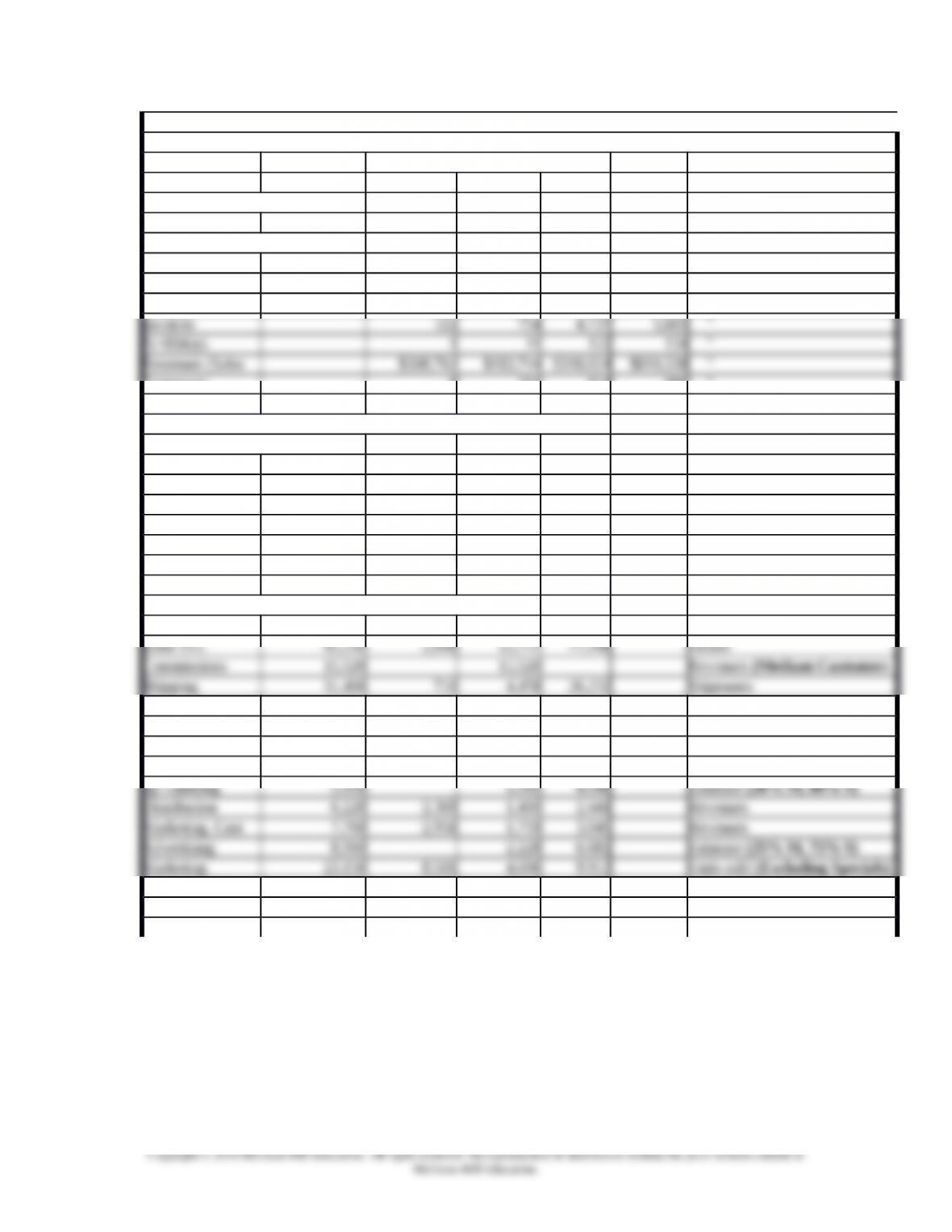

Second Stage Allocation: Allocates SA&A Activities to Customer Type (Large, Medium, Small)

First: Identify Cost Driver and Its Consumption Level or Amount

Customer Type…

COST DRIVER Large Medium Small Total

Units sold- w/o specials 99,770 55,118 116,812 271,700

Units sold-Total 100,250 58,544 117,406 276,200 Table 1

Units embroidered 5,959 6,490 29,394 41,843 “

Units dyed 20,536 9,935 12,328 42,799 “

Orders 133 845 5,130 6,108 “

Shipments 147 923 5,431 6,501 “

Value)

Customers 8 154 824 986 “

Second: Calculate Cost Driver Percentage for Each Customer Type

Units sold (excl. Special) 0.367 0.203 0.430 1.000From above

Orders 0.022 0.138 0.840 1.000From above

Shipments 0.023 0.142 0.835 1.000From above

Invoices 0.020 0.135 0.845 1.000From above

%>60days 0.007 0.082 0.910 1.000From above

Revenues 0.381 0.227 0.392 1.000From above

Customers 0.008 0.156 0.836 1.000From above

Third: Allocate Activity Costs to Customer Type Cost Driver/ Allocation Base

ACTIVITIES Total Cost Large Medium Small (Table 4)

(Medium Customers

only)

Invoicing 13,700 274 1,844 11,583 Invoices

Sales Calls 53,410 53,410 Revenues (Large

Customers only)

Check Credit 6,850 51 562 6,237 %>60days

Samples… 4,595 1,750 1,042 1,803 Revenues

Administrative 13,700 5,031 2,779 5,890 Units sold (Excluding Specials)

Licenses, fees 3,425 3,425 Revenues

(Medium Customers

only)

TOTAL 285,900 77,060 53,490 155,350 AA

5-5

Chapter 5 – Activity-Based Costing and Customer Profitability Analysis

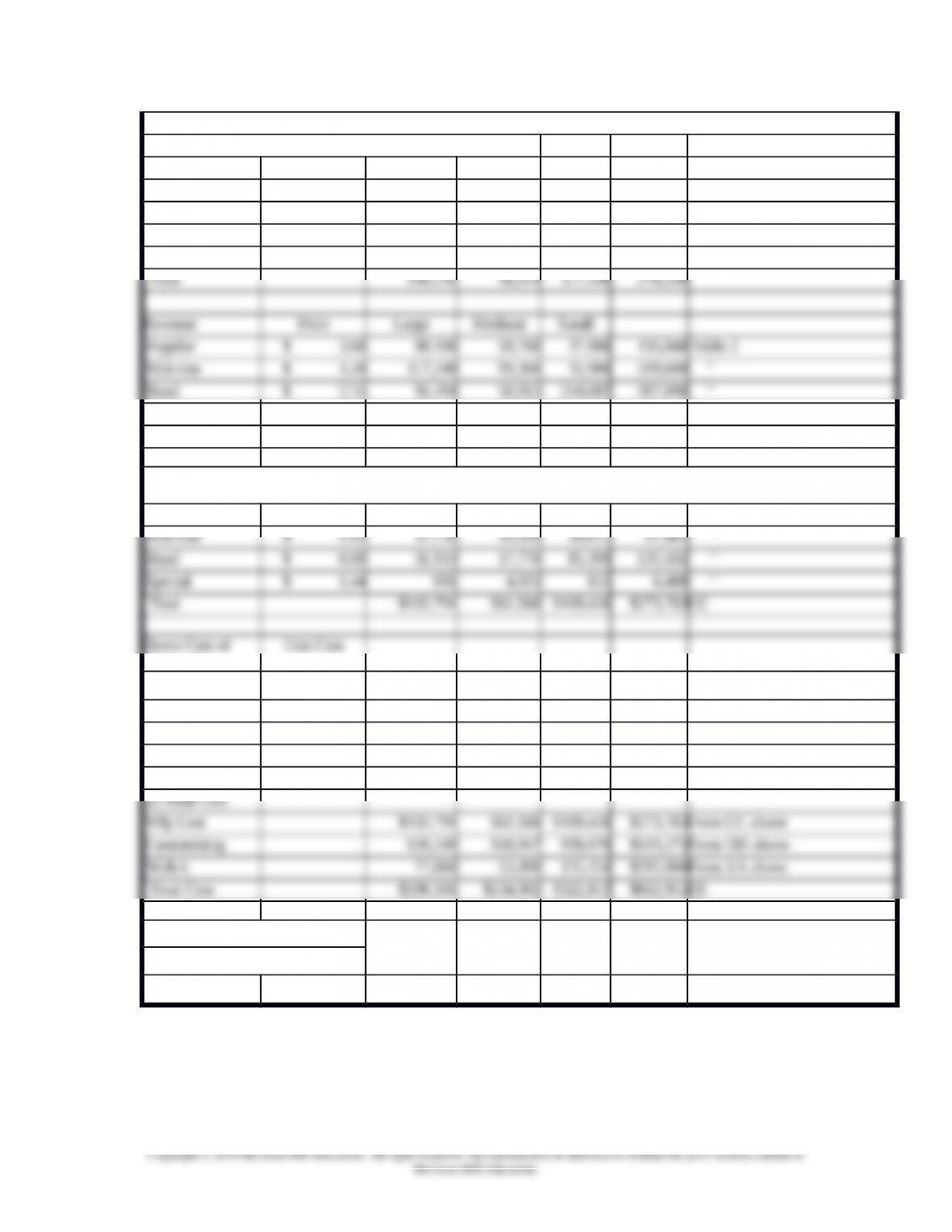

Third Stage: Customer Profitability Analysis

First: Get Revenues by Customer Group

Unit Sales Large Medium Small

Regular 27,250 16,600 10,550 54,400 Table 1

Mid-size 36,640 18,552 10,308 65,500 “

Hand 35,880 19,966 95,954 151,800 “

Special 480 3,426 594 4,500 “

Special $ 4.00 1,920 13,704 2,376 18,000 “

Total Revenue $308,762 $183,744 $318,024 $810,530BB

Second: Calculate Manufacturing Cost —

(1) Unit Cost

Regular $ 1.19 32,428 19,754 12,554 64,736Table 2 x Table 1

Customizing

Inking (Units x 2) $ 0.0817 16,381 9,566 19,184 45,131Table 2 x Table 1

Embroidery $ 1.2770 7,610 8,288 37,536 53,434

Dyeing $ 0.1100 2,259 1,093 1,356 4,708

$26,249 $18,947 $58,076 $103,272DD

Third: Calculate Customer Profit —

$102,661 $49,742 $(4,828) $147,575BB-EE

(1) Total

(2) Per Customer $12,833 $323 $(6) $150

5-6

Chapter 5 – Activity-Based Costing and Customer Profitability Analysis

5-2 Columbo Soft-Serve Frozen Yogurt

Purpose of the case:

This case illustrates the application of Activity-based costing to marketing costs in a food

manufacturer. While the purpose of analyzing product costs is to identify costs per unit of

product, the purpose of analyzing marketing costs is to identify costs per customer or customer

group. This case illustrates how cost drivers are identified and used to compare two separate

customer groups based on the channels of distribution. These cost drivers could also be used to

analyze marketing costs for individual customers. This information is very useful for

understanding profitability in the two channels and for decisions about how to service the two

channels.

Suggested Strategy for Use:

About 60 to 90 minutes are needed to discuss the case thoroughly. This fits well in a 90 minute

class with some lecture about Activity-based costing. I suggest starting with a short background

about marketing in the food business followed by a discussion of the critical issues in the case.

Then, discuss the activity-based costing analysis of the marketing costs. During this phase,

discuss the development of cost drivers, how the firm might have identified them, whether other

cost drivers might be applicable, how to measure the cost drivers and how to collect data about

the cost drivers. Finally, discuss the suggestions for changes in strategy.

Background for the Case Analysis

Food Industry Structure:

There are two distinct channels of distribution in the food business. Grocery and Foodservice.

Grocery is defined as food purchased for later assembly, preparation and consumption in the local

Grocery store. Foodservice is defined as meals prepared for the consumer away from home.

While most are familiar with the local grocery store, foodservice includes any location a

consumer may venture to purchase or eat a meal such as the corner deli, Red Lobster,

McDonald‘s or the college cafeteria. Foodservice comprises more than 52 percent of consumer‘s

food dollars and is growing at a real rate of 1.5% faster than Grocery

.

Grocery and Foodservice evolved independently due to three primary factors: Packaging

requirements, Shipping/Logistics requirements and Marketing requirements.

Packaging. The end use packaging format was the primary determinant of this

separation. Grocery stores sell relatively small package sizes whereas Foodservice uses

either single-serve packages or large, bulk packages. The large manufacturers in

foodservice are generally grocery product suppliers as well due to large capital

requirements to build manufacturing plants and relatively small capital requirements for

unique packaging. Thus, Foodservice is an excellent tool to maximize plant utilization. In

addition, consumer brands built in the Grocery channel have strong appeal in the

Foodservice channel.

5-7

Chapter 5 – Activity-Based Costing and Customer Profitability Analysis

Shipping/Logistics. There are six hundred thousand foodservice operators in the United

States and only thirty thousand grocery stores. Given similar channel sizes, the average

foodservice outlet purchases 1/20th the volume of the average grocery store.

Furthermore, foodservice operators generally have little storage room, so they tend to

order more often than grocers do. As a result, Grocery operators deal directly with

manufacturers whereas Foodservice operators deal with foodservice distributors who deal

with the manufacturers. The Foodservice distributors (such as Sysco, Alliant, US

Foodservice) carry the entire line of products their foodservice customers require

including cooking equipment, dry food, fresh food, meats, etc.

In addition, the manufacturer distribution centers differ for each subchannel because

Grocery orders are predominately full cube/full truck orders whereas Foodservice orders

are mostly part cube and less than truckload (LTL) orders. Thus, grocery distribution

centers are highly standardized with significant automation whereas foodservice

distribution centers are highly customized and manually intense operations.

Marketing. Grocery stores are very active in merchandising consumer products and

usually work in conjunction with the manufacturers to coordinate their advertising

activities. When manufacturers fund these promotions (and they generally do), they can

have tremendous influence over consumer purchase behaviors independent of the grocery

retailer. There is no similar mechanism in the foodservice industry. Instead, the few large

foodservice operators (McDonald‘s, Red Lobster, Marriott, ARAMARK, etc) enjoy

market power over the distributor who in turn wields power over the manufacturer. The

distributors control the street business (small, independent operators) through their sales

force (Distributor Sales Rep œ DSR) but remain beholden to the large foodservice

operators.

Since the large foodservice operators are few and powerful, manufacturers have found

it profitable to develop strong business ties to these operators and use those

relationships to pull product into distributor inventories. Once they have the product,

the distributor will encourage their DSR‘s to sell the product on the street in an effort

to maximize inventory turns. Less than half the 600M foodservice operators are

represented by chains, rather they are independently operated. So the decision making

in this market is quite uneven: a relatively few powerful players dominate. Yet a large

number of individual independent buyers purchase large quantities in aggregate. This

creates a window of competitive opportunity for a strong foodservice manufacturer.

General Mills has a large direct sales force of its own who call on the

restaurants and other foodservice operators. The salespeople create

demand with the operators who request the product from the distributors.

General Mills planned to use this sales force to market Colombo yogurt.

This case concentrates only on Foodservice. Within Foodservice, there are two distinct sub-

channels– Shops and Impulse locations. These sub-channels differ in marketing and shipping

requirements. Shops specialize in frozen yogurt whereas Impulse locations specialize in other

products–yogurt is an add-on.

5-8

Chapter 5 – Activity-Based Costing and Customer Profitability Analysis

1. General Mills and Colombo Competitive Environment:

General Mills focuses on high quality and high sales service. They had a large sales force

already selling to Impulse segment; Colombo offered the advantage of one more product. The

appeal was added profit for little added effort. General Mills had little experience or expertise in

selling to Shops

The market for frozen yogurt changed dramatically in the 1990‘s. In the early 1990‘s, the

market for frozen yogurt was increasing and many shops converted into franchise operations

such as TCBY, ICBY, Freshens, and Yogen-Fruz. These shops purchased their product from

their franchise operator. Meanwhile, Impulse locations started to open up. By late 1990‘s more

than 2/3 of soft-serve sales were at Impulse locations.

Sales of frozen yogurt started to drop and the company wasn‘t exactly sure why. Customers were

dissatisfied and profits were declining. General Mills used the same approach for both Impulse

and Shops. The company sensed that the two channels were different but lacked detailed

information about each channel.

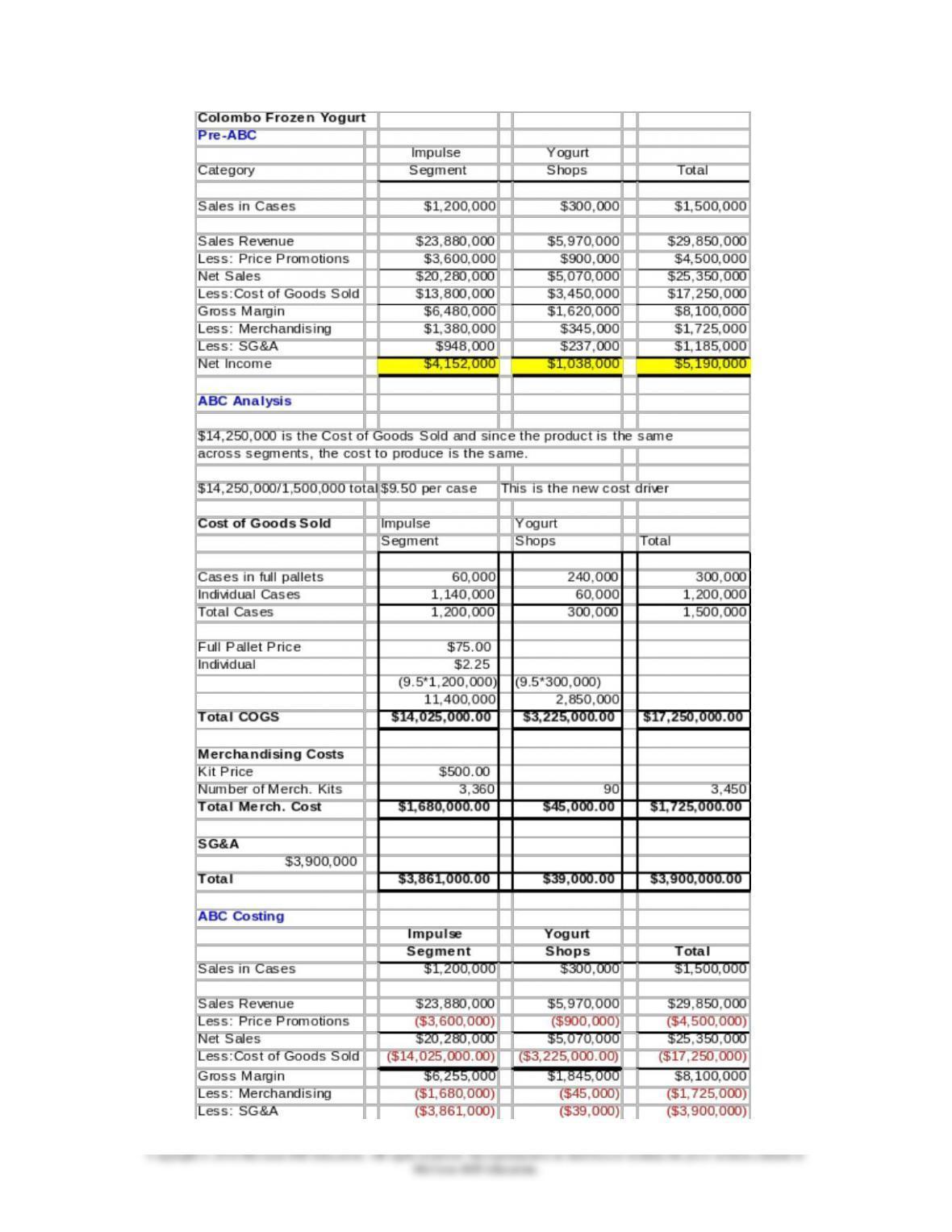

2. Activity-based costing analysis:

Cost of goods sold: – $14,250,000 (same for all cases) = $14,250,000/1,500,000 cases = $9.50 per

case

Impulse: 1,200,000 @ $9.50 = $11,400,000

Shops: 300,000 @ $9.50 = $2,850,000

Shipping: $3,000,000 varies with individual cases ($2.25/case) or with pallets ($75/pallet):

Impulse:

oPallets = 60,000/75 = 800 @ $75 = $60,000

oIndividual cases = 1,140,000 @ $2.25 = $2,565,000

oTotal = $2,625,000

Shops:

oPallets = 240,000/75 = 3200 @ $75 = $240,000

oIndividual cases = 60,000 @ $2.25 = $135,000

oTotal = $375,000

Merchandising: $500 per kit

New Net Income Analysis:

5-9

Chapter 5 – Activity-Based Costing and Customer Profitability Analysis

5-10