Chapter 12 – Strategy and the Analysis of Capital Investments

12-44 (Continued-1)

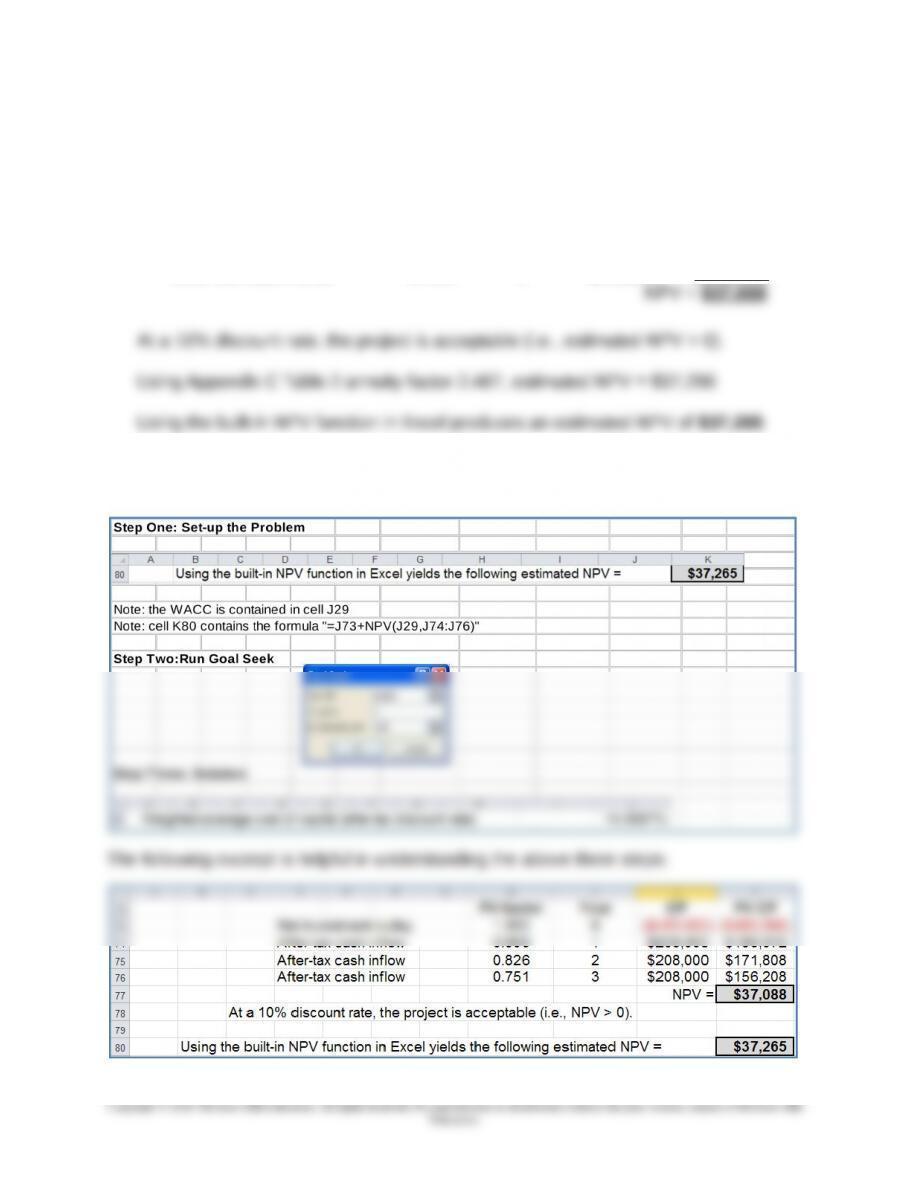

PV factor Year CF PV CF

Net investment outlay 1.000 0 ($480,000)

($480,000

)

After-tax cash inflow 0.909 1 $208,000 $189,072

After-tax cash inflow 0.826 2 $208,000 $171,808

After-tax cash inflow 0.751 3 $208,000 $156,208

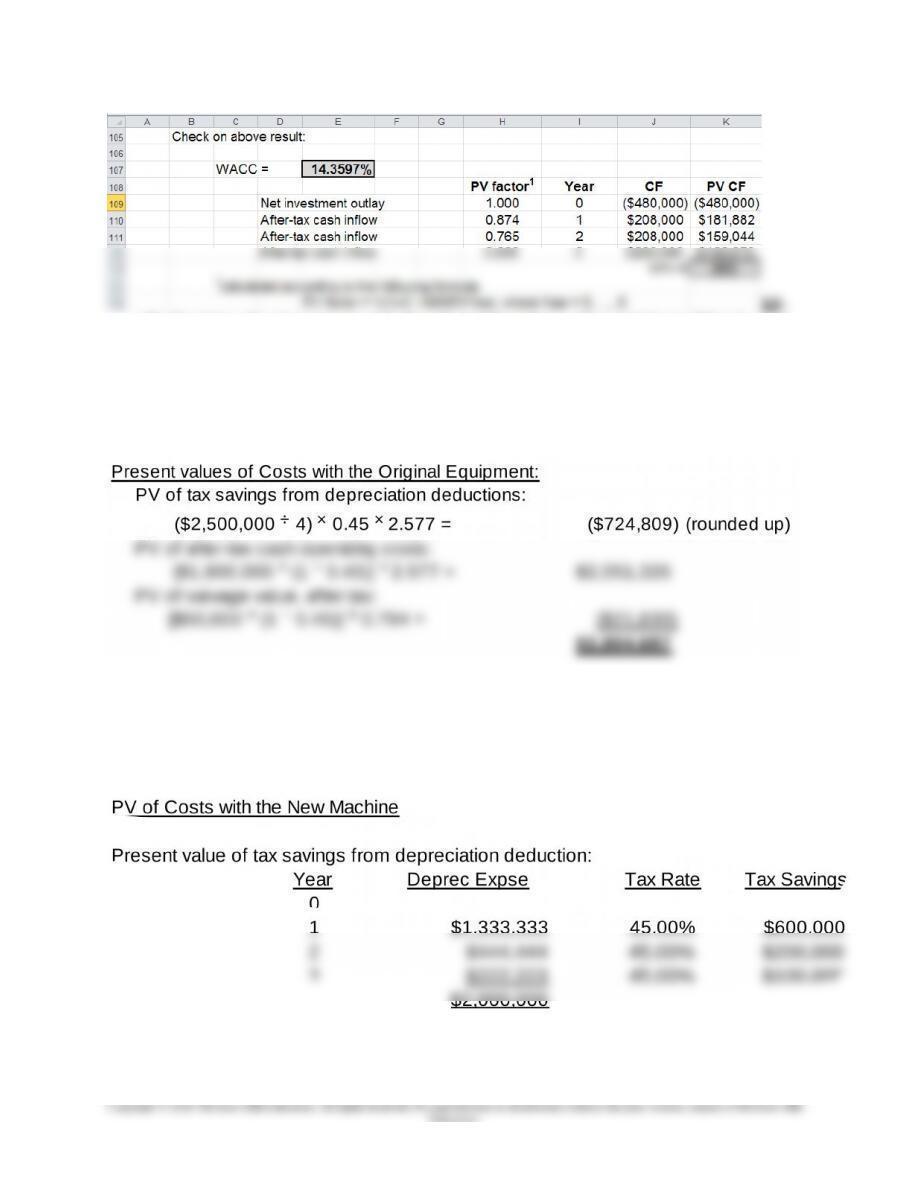

3. The weighted-average cost of capital (WACC) that would make the company

indifferent between keeping or replacing asset A is 14.3597%, as follows:

12-41

Chapter 12 – Strategy and the Analysis of Capital Investments

12-44 (Continued-2)

12-42

Education.

Chapter 12 – Strategy and the Analysis of Capital Investments

45 Machine Replacement with Tax Considerations; Spreadsheet (50 minutes)

(Note: the amounts given below are slightly different from the results obtained using the

present value factors provided in Appendix C, Tables 1 and 2. This is due to the rounding, to

three digits, in the present value factors presented in Tables 1 and 2 in the text. The solution

below is based on the use of PV and NPV functions in Excel.)

(NOTE: The present value factors listed above are taken from text Tables 1 and 2 and,

as such, have been rounded to three decimal places. However, the actual calculations

above are done using the NPV and PV built-in functions in Excel, and as such are not

rounded.)

12-43

Education.

Chapter 12 – Strategy and the Analysis of Capital Investments

12-45 (Continued)

The total cost of the new machine, including the purchase cost and the cash

operating cost in each of the three years is, in PV terms, $202,440 below the

total cost of continuing with the original equipment. Therefore, from a purely

financial standpoint, the purchase of the new machine is a good investment.

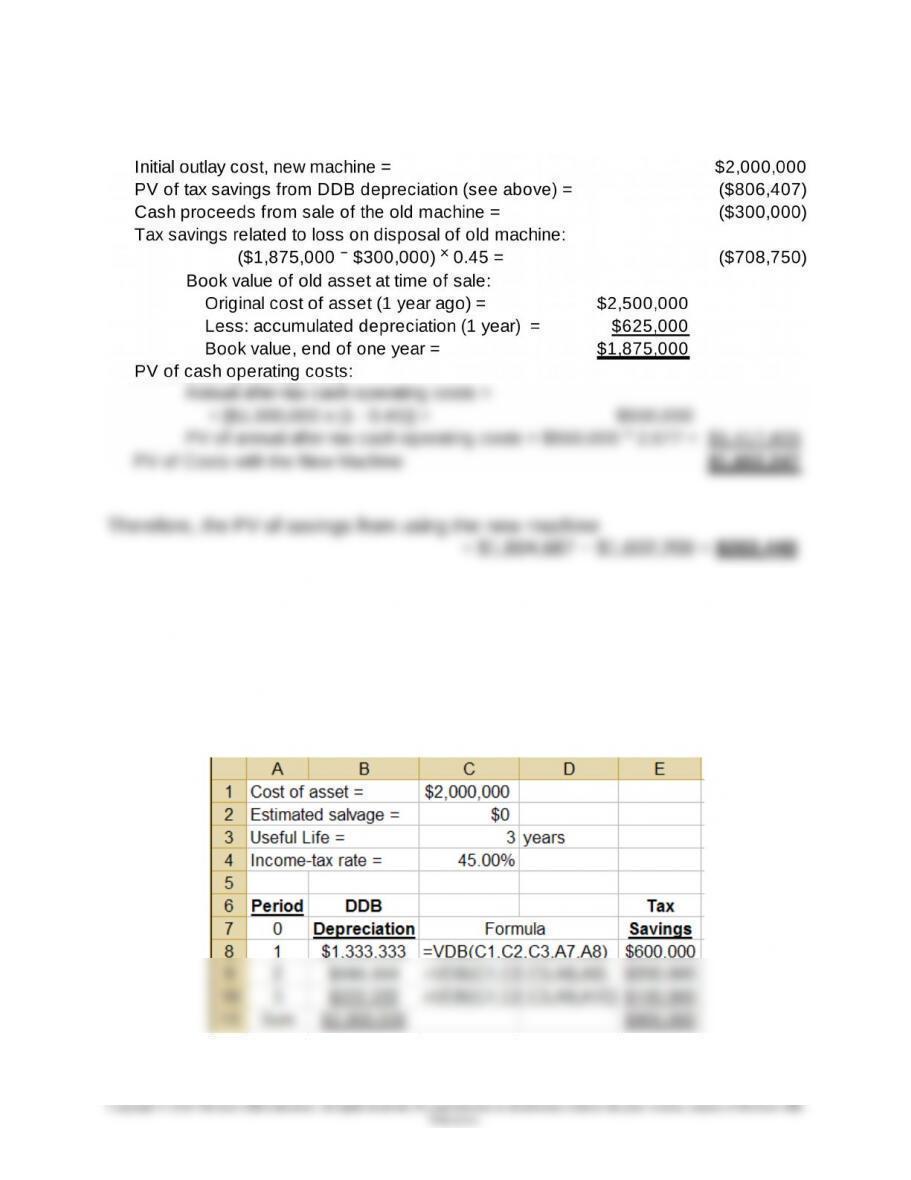

Depreciation Calculations for Replacement Machine: Using VDB Function in

Excel

12-44

Chapter 12 – Strategy and the Analysis of Capital Investments

12-46 Equipment Replacement; MACRS (50 minutes)

1. Per-unit pre-tax cash flow per unit, additional unit sales:

Sales price per unit $3,500

Current variable (cash) manufacturing cost per unit − 2,450

Current cash contribution margin per unit $1,050

Cash-based cost savings per unit with the new machine + 150

Pre-tax cash flow per unit for the additional units $1,200

After-Tax Cash Flow Analysis Present Discount

Item Description Value Factor 1

2016 2017 2018 2019

Purchase cost of the new asset ($608,000)

Capitalized installation cost of the new asset ($12,000)

After-tax proceeds from disposing old ($50,000 × (1 − t)) $30,000

Pre-tax cash flow per unit, sale of additional units (above) $1,200 $1,200 $1,200 $1,200

Additional units (given) 30 50 50 70

Pre-tax cash flow from additional units $ 36,000 $ 60,000 $ 60,000 $ 84,000

VacuTech can expect to have a negative NPV of $60,006 if it purchases the new pump.

1Note: The above PV of after-tax cash inflows ($529,994) was determined using the NPV built-in function in Excel. If,

instead, the present value factors from Appendix C, Table 1 were used, the indicated NPV would be ($59,840).

The PVs for after-tax cash flows are as follows: Year 1 = $155,243; Year 2 = $168,286; Year 3 = $97,516; Year 4 =

$109,115.

12-45

12-46 (Continued)

2. Other factors the firm needs to consider include:

Maintenance costs of the machines

Reliability of the machines

Changes and timing of newer machine

12-47

Education.

Chapter 12 – Strategy and The Analysis of Capital Investments

PROBLEMS

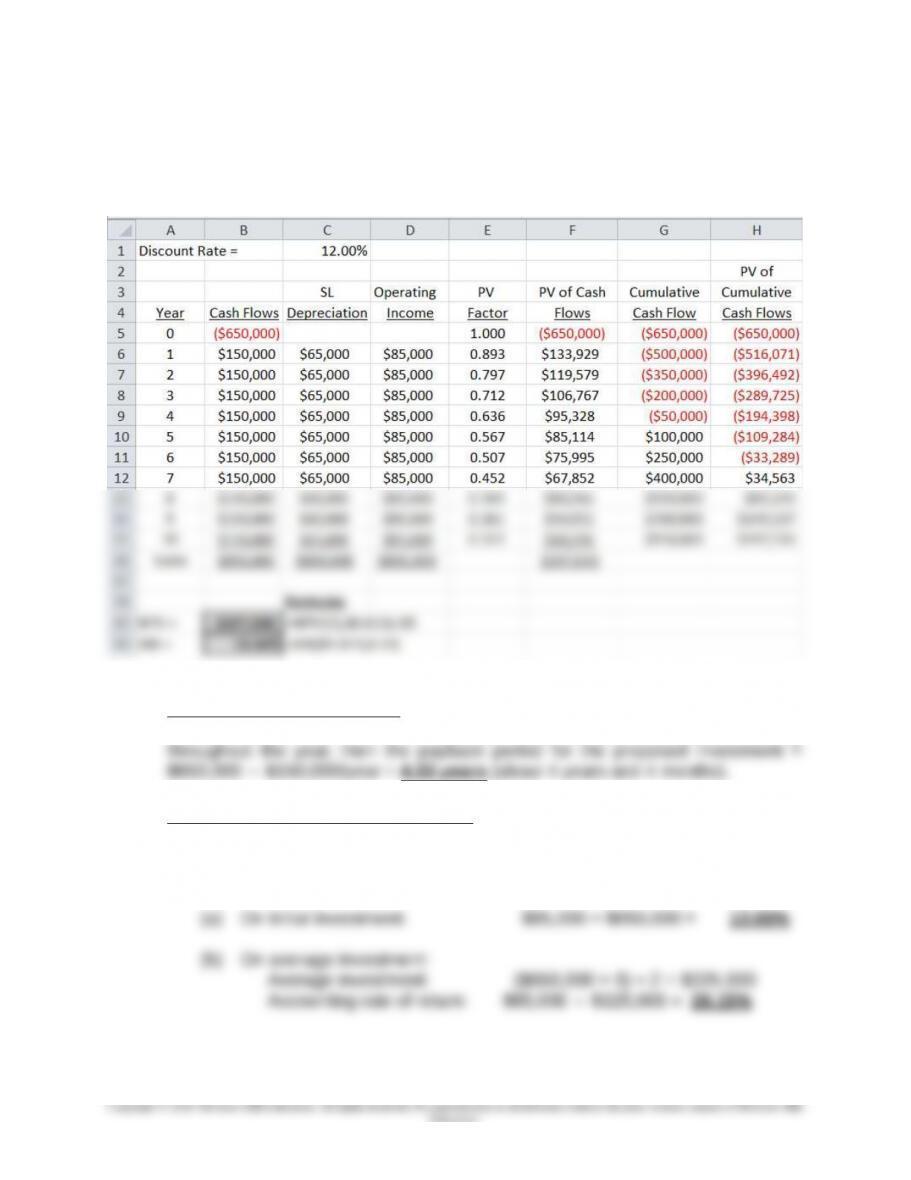

12-47 Basic Capital-Budgeting Techniques; No Taxes; Uniform Net Cash Inflows;

Spreadsheets (45-60 minutes)

1. Unadjusted Payback Period: As shown above, the payback period occurs

between years 4 and 5. If we assume that the cash inflows occur evenly

2. Accounting (book) rate of return (ARR):

From the above, the average increase in operating income over the 10-year

period = $850,000 ÷ 10 years = $85,000 ÷ year. Thus, the ARR

12-48

Education.

Chapter 12 – Strategy and the Analysis of Capital Investments

12-47 (Continued-1)

3. NPV: using the PV factors from Appendix C, Table 2, NPV =$197,500

As shown above, based on the NPV function of Excel, NPV = $197,533 (the

4. Present value payback period: as indicated in the above schedule (with PV

factors rounded to three decimal places, per Table 2), the present value

payback period is “6-plus” years; this is the time it takes for the present value

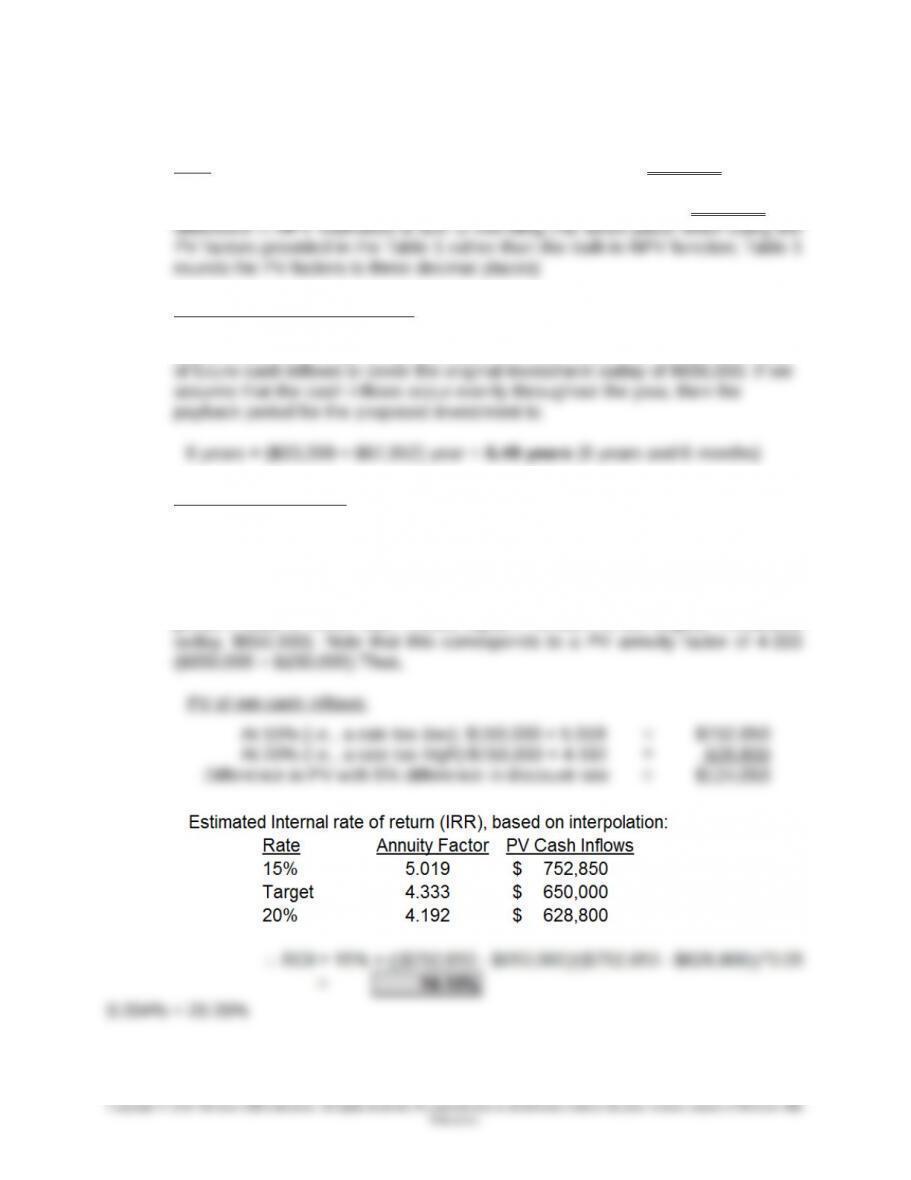

5. Internal rate of return: as indicated in the above schedule, we can use the built-

in function in Excel to estimate the IRR for this proposed investment; IRR =

19.04%.

Alternatively, we can estimate the IRR as follows. We are looking for an

interest/discount rate that provides for a NPV = $0 (i.e., a rate that provides a

present value of future cash inflows equal in amount to the original investment

IRR =

20% +

12-49

Chapter 12 – Strategy and the Analysis of Capital Investments

12-50

Education.

Chapter 12 – Strategy and the Analysis of Capital Investments

12-47 (Continued-2)

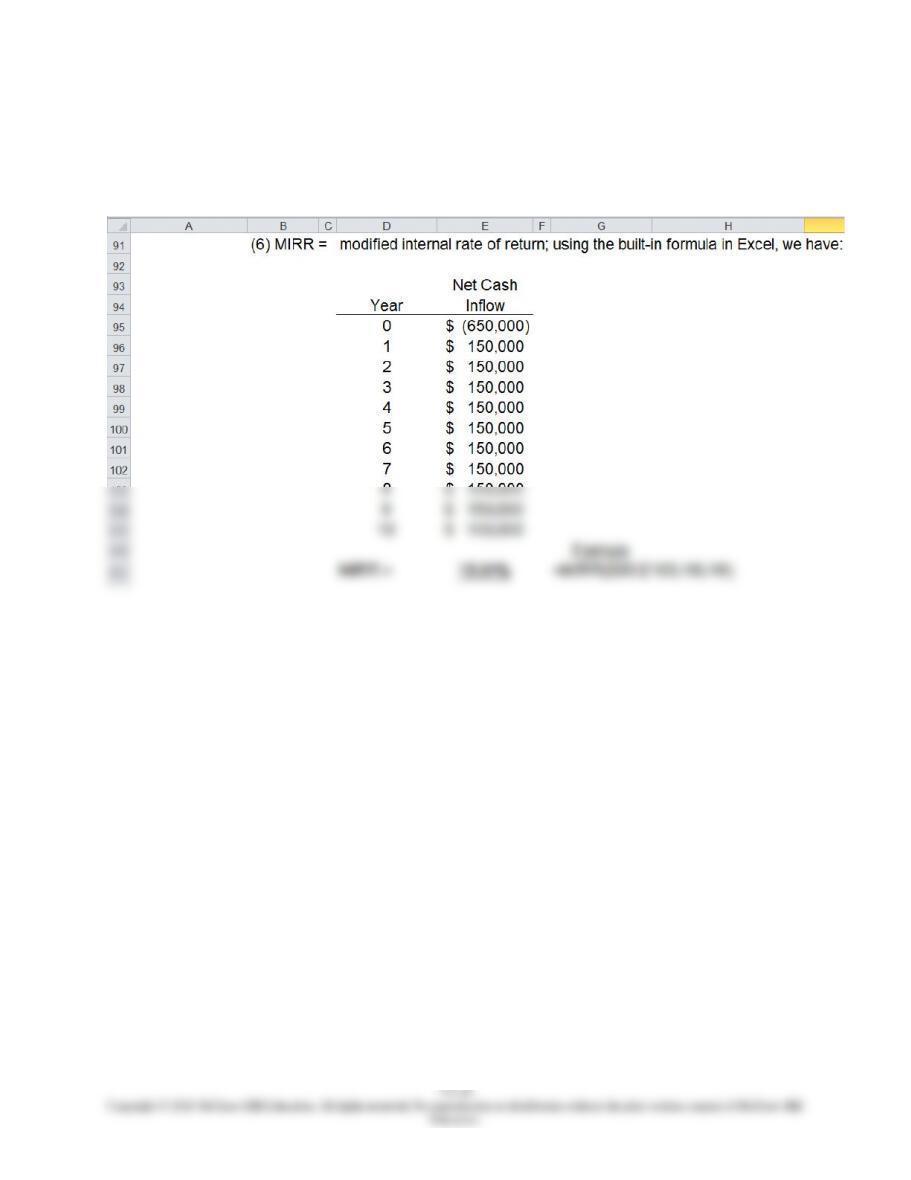

6. Modified internal rate of return (MIRR):