Chapter 07 – Cost Allocation: Departments, Joint Products, and By-Products

CHAPTER 7:

COST ALLOCATION: DEPARTMENTS, JOINT PRODUCTS,

AND BY-PRODUCTS

QUESTIONS

7-1 The four objectives in the strategic role of cost allocation are to achieve effective

cost management through methods which:

1. Determine accurate departmental and product costs as a basis for evaluation

the performance of the department or profitability of the product.

7-2 Joint products and by-products are derived from processing a single input or a

common set of inputs. Joint products are products from the same production

classified as by-products.

7-3 Reciprocal service flows are the service flows between service departments in

departmental allocation. These flows are ignored in the direct method, they are

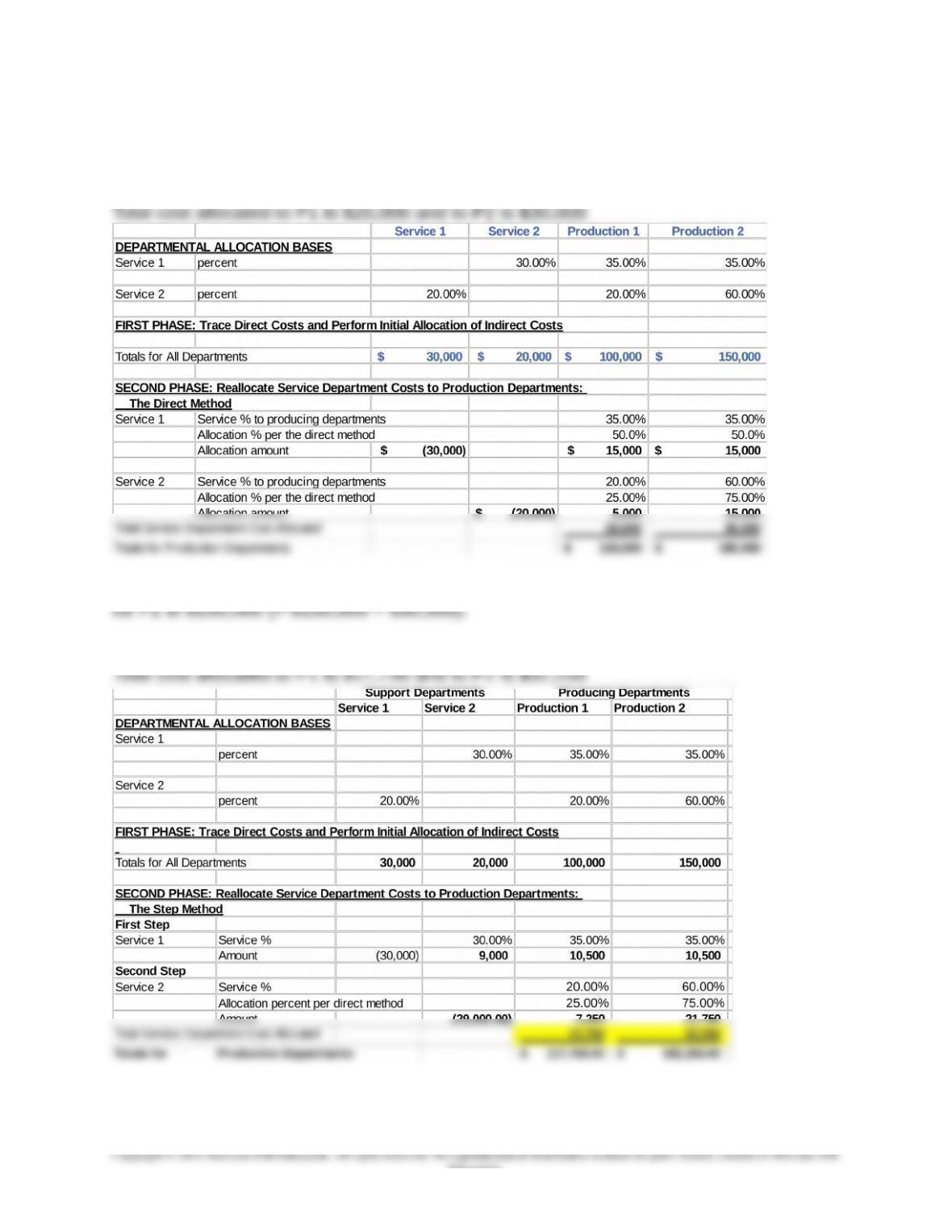

7-4 There are three methods for departmental cost allocation: the direct method, the

step method, and the reciprocal method.

The direct method of cost allocation is done by taking the service

department flows to production departments only and determining each

The reciprocal method is most preferred because it simultaneously takes

into account all the reciprocal flows among service departments.

7-1

Chapter 07 – Cost Allocation: Departments, Joint Products, and By-Products

7-5 The three phases of departmental cost allocation, which apply for each of the

three methods (Question 7-4) are:

1. The initial allocation of all production and service costs to departments

2. The allocation of service department costs to production departments

3. The allocation of costs of production departments to products

The first phase in departmental cost allocation has two parts: to trace the direct

manufacturing costs in the plant to each service and production department that

The third phase is to take the costs accumulated in the producing departments

and to allocate these costs to the final cost objectsthe products or services.

7-6 There are a number of possible answers here. The chapter gives examples of

the use of departmental cost allocation in the banking industry and in medical

care. Other examples would include cost allocation in an electric utility company

to provide a basis for rate setting for different users of the utility (telephone,

water, electricity, etc.). Also, a not-for-profit or a governmental unit such as a

7-7 There are four methods for by-product costing:

The two asset recognition methods are:

Method 1 – Net Realizable Value Method. This method shows the net

realizable value of by-products in the income statement as a deduction from the

7-2

Education.

Chapter 07 – Cost Allocation: Departments, Joint Products, and By-Products

The two revenue methods are:

Method 3 – Other Income at Selling Point Method. The net sales revenue

The preferred method depends on the circumstances. Where the amount of the

by-product cost and revenue is small, methods 3 and 4 are preferred on the

basis of convenience and cost benefit. In contrast, when the cost or revenue of

the by-product is significant, the asset recognition methods 1 and 2 are preferred.

Asset recognition methods are based on the financial accounting concepts of

7-8 and,

7-9 There are a number of limitations and implementation issues to consider when

using either joint cost allocation or departmental cost allocation.

One issue is that it is often difficult to determine an appropriate allocation

base to allocate the joint product costs or to determine a figure for percentage

service provided by the service departments. The choice of a base and a service

percentage may be subjective and prone to error.

Other issues include (a) Disincentive Effects When the Allocation Base is

7-3

Chapter 07 – Cost Allocation: Departments, Joint Products, and By-Products

7-10 A number of ethical issues are important when implementing cost allocation

methods. First, there are ethical issues when cost allocation is used in a situation

where the products or services are produced for both a competitive market and

for a public agency or government which is paying on a cost-plus basis. There is

an incentive for the provider to allocate an unfairly high portion of joint costs to

the cost-plus customer.

A second issue is the equity or “fair share” issue that arises when a

government reimburses costs of a private institution, or when government

provides a service for a fee to the public. In both cases, cost allocation methods

problem arises.

Another important ethical issue in cost allocation is the effect of the

chosen allocation method on the costs of products sold to or from foreign

subsidiaries of U.S. manufacturing firms. The cost allocation method usually

affects the cost of products traded internationally and therefore also the amount

7-4

Education.

Chapter 07 – Cost Allocation: Departments, Joint Products, and By-Products

BRIEF EXERCISES

7-11

Total cost allocated to P1 is $20,000 and to P2 is $30,000

7-12 See 7-11 above, the total for P1 is $120,000 (= $100,000+$20,000), and the total

7-13

7-5

Education.

Chapter 07 – Cost Allocation: Departments, Joint Products, and By-Products

7-14 There will be no change. The cost allocation is for service department cost (for S1

7-15, 16

Non Service % P1 P2

S1 60% 40%/60% = 2/3 20%/60% = 1/3

S2 80% 40%/80% = 1/2 40%/80% = 1/2

7-17,18

The cost allocations are shown below.

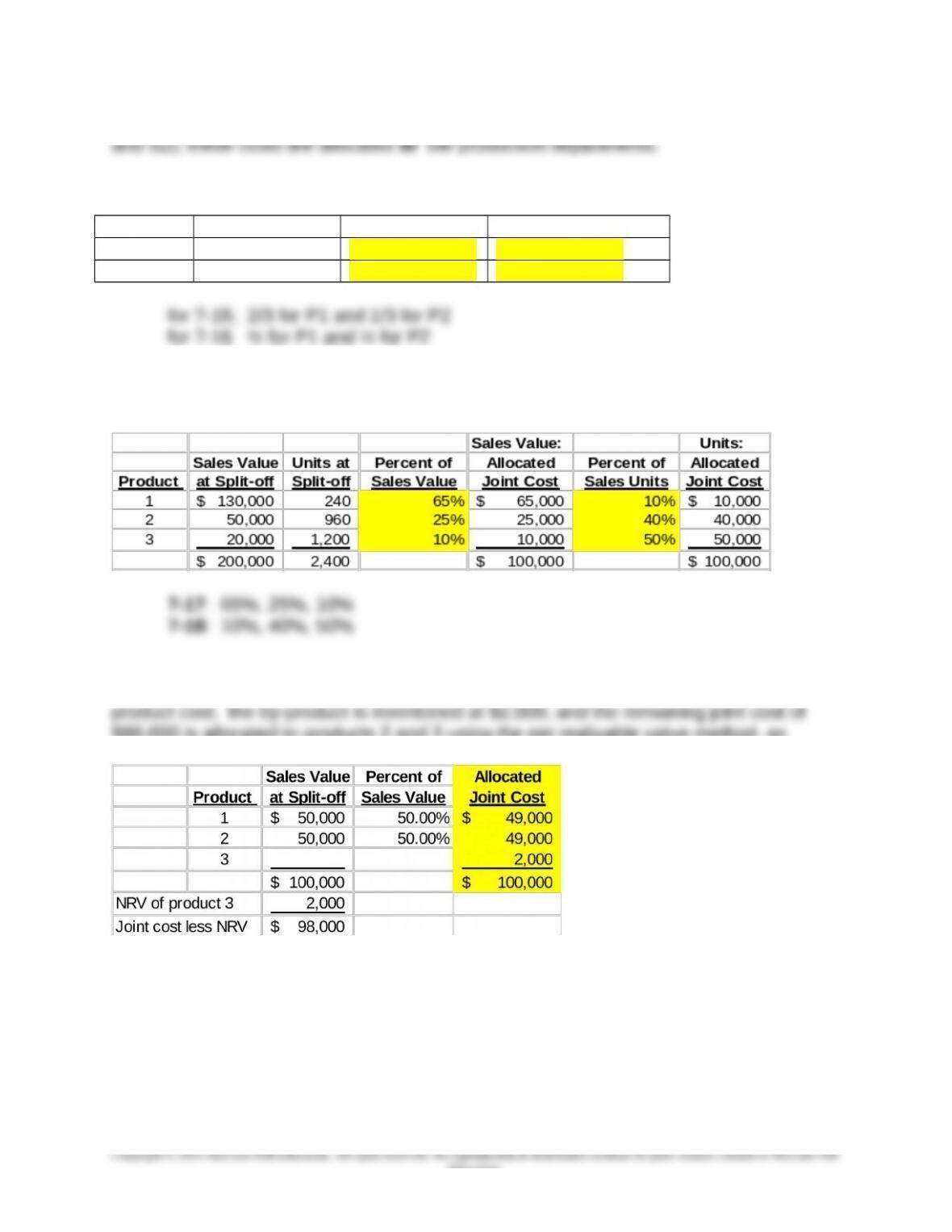

7-19

First, the net realizable value of the by-product, $2,000 is reduced from the total joint

$98,000 is allocated to products 2 and 3 using the net realizable value method, as

follows:

7-6

Education.

Chapter 07 – Cost Allocation: Departments, Joint Products, and By-Products

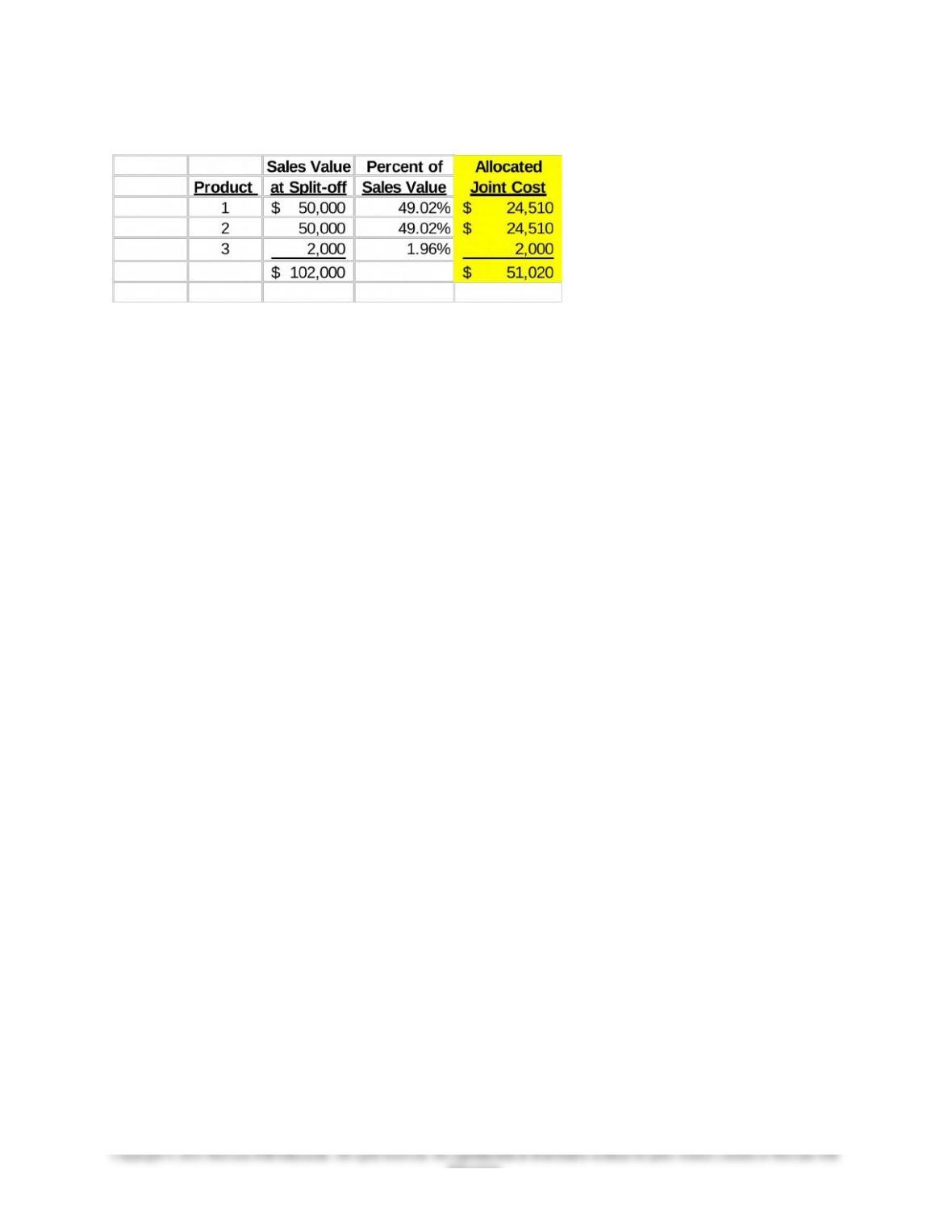

7-20

7-7

Education.

Chapter 07 – Cost Allocation: Departments, Joint Products, and By-Products

EXERCISES

7-21 Cost Allocation, General (15 min)

Cost pools are collections of costs that are similar in nature and have

a presumed causal connection. Examples of cost pools include

personnel-related costs, payroll-related costs, space-related costs,

and energy-related costs. A cost object can be any physical unit or

territories, or other organizational subdivisions.

1. The “benefit” basis, often applied to corporate administrative

costs, allocates costs according to some measure of the benefit

received by the cost object. The benefit criterion holds that cost

2. The “ability to bear” criterion, which is similar in objective to

the benefit criterion, is based on the ability of the cost objects to cover

or absorb costs and allocates costs based on the revenues or profits

of the cost objects. This allocation base does not consider the

7-8

Education.

Chapter 07 – Cost Allocation: Departments, Joint Products, and By-Products

7-22 By-products and Decision Making (15 min)

Joe is considering a fruit-liquid, which is a by-product of the

processing for his jams and jellies, to produce a new product – a

coffee flavoring to complement his line of gourmet coffees. Joe is

correct in understanding that the production cost of jams and jellies is

irrelevant, since the fruit-liquid is a necessary by-product of the

revenue from the sales to canneries – price to canneries less any

selling costs. The key to the decision is to ignore the joint costs, but

focus instead only on the separable costs and the increase in sales

value. This question is addressed further in chapter 11 under the

heading, “Decisions to Sell Before or After Additional Processing,” on

page 406.

A more critical consideration is the strategic issue: will the new

product line enhance the sales of coffees and the overall image of

Joe’s business as a high-end, quality gourmet business? Joe might

7-9

Education.

Chapter 07 – Cost Allocation: Departments, Joint Products, and By-Products

7-23 By-Products; Sustainability (15 min)

1. The wood pellets should be accounted for as a by-product since the

main product and the highest-value product of the timber industry is

lumber for construction. Since the pellet production is in total of

2. Some environmentalists have argued against the use of wood pellets

as a green source of energy. They say that it would take 54 years

for a new tree to consume the carbon emissions of a single tree

burned as pellets. Others argue that the use of timber for wood

pellets helps to preserve the forests, which would otherwise

potentially be converted to other types of agriculture or to urban

their widespread use was discouraged.

3. The issues of sustainability and climate change are global issues.

That is, emissions anywhere in the world have an effect on climate

change. One could argue that emissions in one country would most

Source: Bruce Siceloff, “Useless Wood Converted Into Cash,” Raleigh

News & Observer, August 17, 2013, section 1, p1.

7-10

Education.