Chapter 20 – Management Compensation, Business Analysis, and Business Valuation

Chapter 20

Management Compensation, Business Analysis, and Business

Valuation

Teaching Notes for Cases

20-1. Midwest Petro-Chemical Company: Evaluation of a Firm; Strategy

Adapted from teaching note provided by the case authors, David A. Kunz and Keith A. Russell

1. The case does not provide much information about the competitive environment for the firm, but we

know this is a commodity business, and the nature of the competition is therefore most likely to be cost

leadership. Appropriate compensation plans would be tied directly to managers’ ability to manage costs.

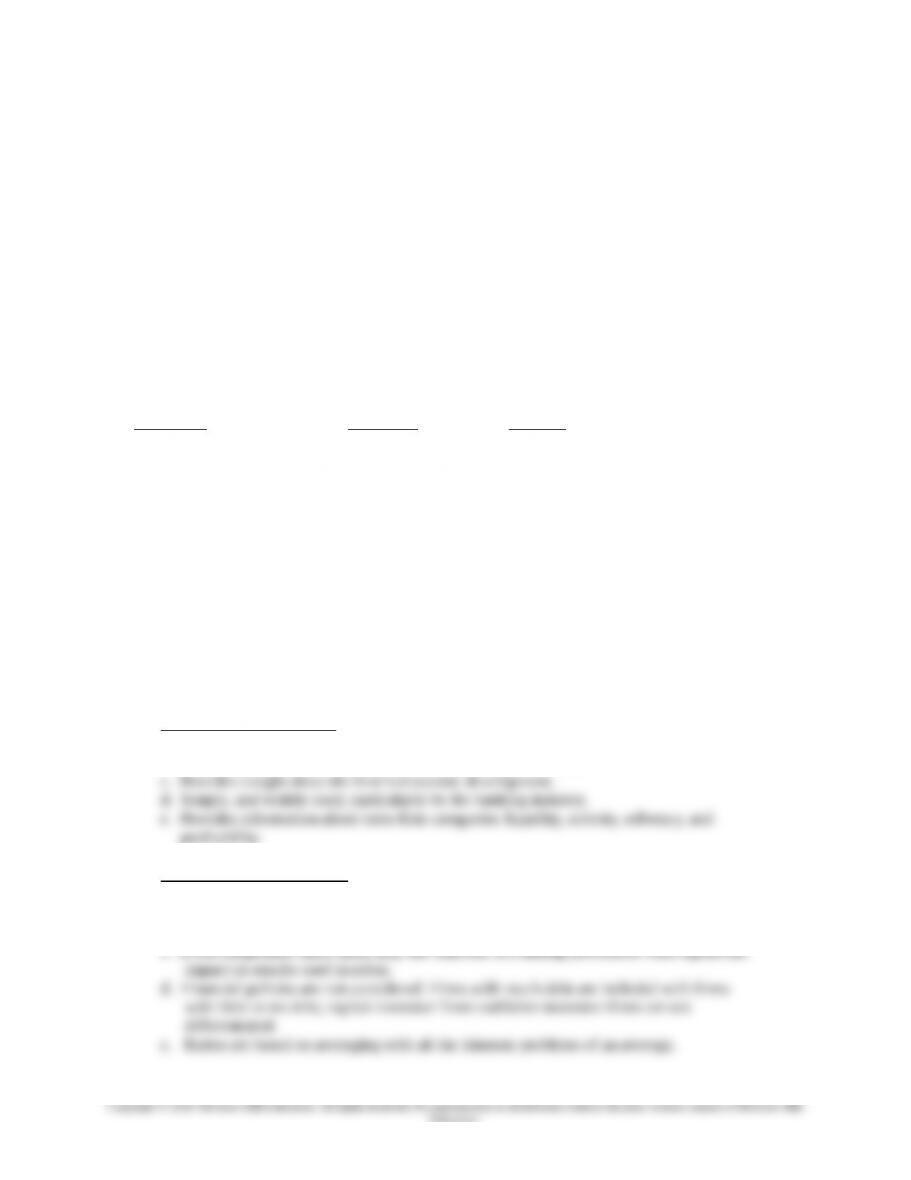

2. Analysis of company performance using ratio and industry norms as a benchmark.

Ratio/2013 Value Line Midwest

Profit margin 7.5% 2.4% ($2,315/$95,962)

Return on Assets 15.0% 5.3% ($2,315/$44,006)

(% earned total capital)

Return on Equity 17.5% 12.4% ($2,315/$18,657)

(% earned net worth)

Price Earning Ratio 18.5 7.3 ($22.50/$3.08)

Price to Book Value — .38 ($22.50/$58.74)

Operating Margin 17.0% 4.4% ($4,221/$95,962)

Income Tax Rate 35.5% 30.0% ($992/$3,307)

Per cent (%) Retained

to Common Equity 12.0% 85.0% ($16,698/$19,702)

Clearly, Midwest Petro-Chemical is a weak firm relative to industry norms, based on financial ratio

analysis.

Strengths of ratio analysis:

a. Provides an excellent historical profile of a firm.

b. Comparative information is readily available for public firms.

Weaknesses of ratio analysis:

a. Ratio analysis is an art; users have to make important judgments.

b. As firms diversify, become conglomerates, and/or multi-national, specific

industry/segment information is lost.

c. Even comparable-sized firms may use different accounting procedures with significant

20-1

Education.

Chapter 20 – Management Compensation, Business Analysis, and Business Valuation

3. Why did ratio analysis serve as an effective tool for Tom Williams?

As a banker, Williams was more concerned about loan repayment ability than about value.

4. Discuss each valuation method. What are strengths and weaknesses of each? What difficulties are

encountered when applying each method?

a. Asset-based or market value : The firm’s value can be determined by valuing the assets.

Three approaches to this method are;

Strengths of the asset method: Best used to value firms in natural resources or the securities

industry.

Weaknesses of the asset method: Not a popular method; techniques do not consider firm as a

going concern; historical or book value may bear little, if any, relationship to market value.

b. Market Comparison: Uses market values for similar forms to determine value.

Strengths: Can be useful for similar firms in terms of financial policies, if turnover ratios, profit

opportunity cost of funds by the investor. The rate typically contains two components:

1. a risk-free element equal to the rate earned on a short-term government instrument

(Treasury Bill, for example), and

2. a return premium equal to the risk factor associated with the firm being valued.

Strengths: Very popular with sophisticated investors; conceptually very strong.

Weaknesses: Complex; determination of risk premium requires a subjective judgment.

d. Capitalization of earnings: Based on the value of historical or future earnings divided by a

capitalization rate.

Historic earnings: An average of the firm’s net incomes is divided by the capitalization rate. If

1. Riskier businesses have higher capitalization rates

2. Firms with higher earnings growth rates have lower capitalization rates

20-2

Chapter 20 – Management Compensation, Business Analysis, and Business Valuation

Strengths: Used by knowledgeable investors; solid method for evaluating a low-risk firm.

Weaknesses: Capitalization rate determination is subjective (estimated); the method may be

somewhat difficult to understand.

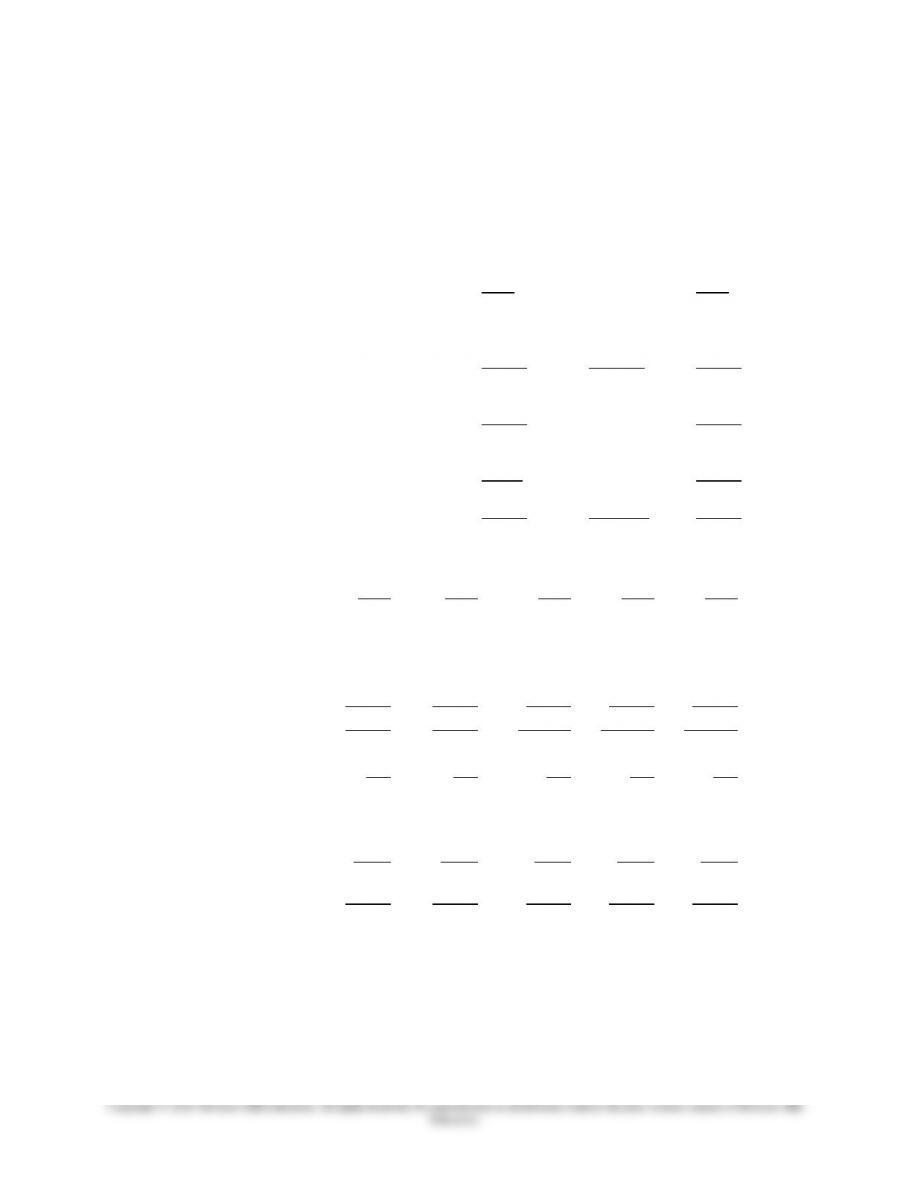

5. Develop values for Midwest’s Petro-Chemical’s stock using the methods discussed in part 4.

. Asset-based or market value (000s omitted)

Exhibit One: Appraisal Value (Replacement) for land,

plant, property, and equipment $24,335

Plus: Book value of current assets 24,490

Less: Book value of liabilities 24,408

Asset base value $24,417

$24,417/751 shares outstanding = $32.51 per share.

B. Market Comparison:

Year Earnings per share

2013 $3.08

2012 $2.66

2011 $1.08

2010 $1.15

$7.97/ 4 years = $1.99 x 16* = $31.84

* sales price x earnings for Western Solvents (given in case)

20-3

Education.

Chapter 20 – Management Compensation, Business Analysis, and Business Valuation

C: Discounted Cash Flow

First, determine the cost of sales and income as a percent of sales as a basis for projecting income

for 1996-2000.

Statement of Income

for years ending December 31

($, 000s omitted)

2013 2012

Net Sales $95,652 (100%) $92,333

Cost and Expenses

Cost of Sales 77,719 (81.2%) 74,882

Selling G & A 13,712 (14.4%) 13,388

Total cost & Exp 91,431 (95.6%) 88,270

Operating Income 4,221 ( 4.4%) 4,063

Interest Expense 914 1,214

Income before Income Tax 3,307 2,849

Income Tax Exp. 992 854

Net Income $2,315 ( 2.4%) $1,995

Second, develop the income projections based on the above percentages for 2013 and 2012:

($,000 omitted)

2014 2015 2016 2017 2018

Sales

Cost of Sales

$99,000 $102,466 $106,050 $109,764 $113,605

Costs & Expenses 80,388 83,202 86,113 89,128 92,247

Selling G & A 14,256 14,755 15,271 15,806 16,359

Total Cost & Exp 94,644 97,957 101,384 104,934 108,606

Operating Income 4,356 4,509 4,666 4,830 4,999

Interest Expense 900 850 800 750 700

Income before

Income Tax 3,456 3,659 3,866 4,080 4,299

Income Tax Exp.

(30%)

1,037 1,098 1,160 1,224 1,290

Net Income $2,419 $2,561 $2,706 $2,856 $3,009

Earnings per share 3.22 3.41 3.60 3.80 4.01

Dividends per share .35 .40 .45 .50 .55

Third, develop Cash Flow Projections:

20-4

Chapter 20 – Management Compensation, Business Analysis, and Business Valuation

Cash Flow WC Cash Cash

Year NI Depr In Flow Out* Flow Net

2014 $2,419 + $800 = $ 3,219 – $385 = $2,834

2015 2,561 + 800 = 3,361 – 398 = 2,963

2016 2,706 + 800 = 3,506 – 412 = 3,094

2017 2,856 + 800 = 3,656 – 427 = 3,229

2018 3,009 + 800 + 3,809 – 442 = 3,367

*2013 Working Capital / Sales = % of Sales

CA $24,490/$95,652 = 25.6%

CL $13,509/$95,652 = 14.1%

11.5%

Supporting data for developing the cash flow projections:

WC Cash Flow Out: Changes in Sales

2014 = 3,348 x .115 = 385

2015 = 3,465 x .115 = 398

2016 = 3,586 x .115 = 412

2017 = 3,712 x .115 = 427

2018 = 3,842 x .115 = 442

Fourth, develop the valuation based on discounted cash flow:

Present Value

Cash Flow @ 15%*

2014 $2,834 x .8696 = $2,464

2015 2,963 x .7561 = 2,240

2016 3,094 x .6575 = 2,034

2017 3,229 x .5718 = 1,846

2018 34,930** x .4972 = 17,367

$ 25,951

$25,951 / 751 = $34.55

*Discount rate: Debt cost (balance sheet) .095

+ Premium (equity) .030

+ Premium (small firm) .025

.150

** Cash Flow plus stockholder equity ($,367 + 31,563)

Supporting data for the above:

Changes in Stockholder Equity (000s omitted):

NI Dividend SE

2013 $ $ $ 19,702

2014 2,419 – 263 = 21,858

2015 2,561 – 300 = 24,119

2016 2,706 – 338 = 26,487

2017 2,856 – 376 = 28,967

2018 3,009 – 413 = 31,563

20-5

Education.

Chapter 20 – Management Compensation, Business Analysis, and Business Valuation

Dividends (rounded to nearest 000s):

2014 .35 x $751,000 = $ 263,000

2015 .40 x 751,000= 300,000

2016 .45 x 751,000= 338,000

2017 .50 x 751,000= 376,000

2018 .55 x 751,000= 413,000

D. Capitalization of Earnings (000s omitted)

Net Income Begin SE* Return on Equity

2013 $ 2,315 / $17,612 = 13.1%

2014 1,995 / 15,805 = 12.6%

2015 809 / 15,161 = 5.3%

2016 865 / 14,446 = 6.0%

37.0% / 4 = 9.25%

* Year Begin SE NI – Dividends

2013 $19,702

2012 17,612 2,315 – 225 ($.30 x 751)

2011 15,805 1,995 – 188

2010 14,446 809 – 165

2009 15,161 865 – 150

Historic EPS

2013 – $3.08

2012 – 2.66

2011 – 1.08

2010 – 1.15

$7.97 / 4 = $1.99

$1.99 / .0925 = $21.51

Projected EPS

2014 – $ 3.22

2015 – 3.41

2016 – 3.60

2017 – 3.80

2018 – 4.01

$18.04 / 5 = $3.61

$ 3.61 / .0925 = $39.03

20-6

Education.

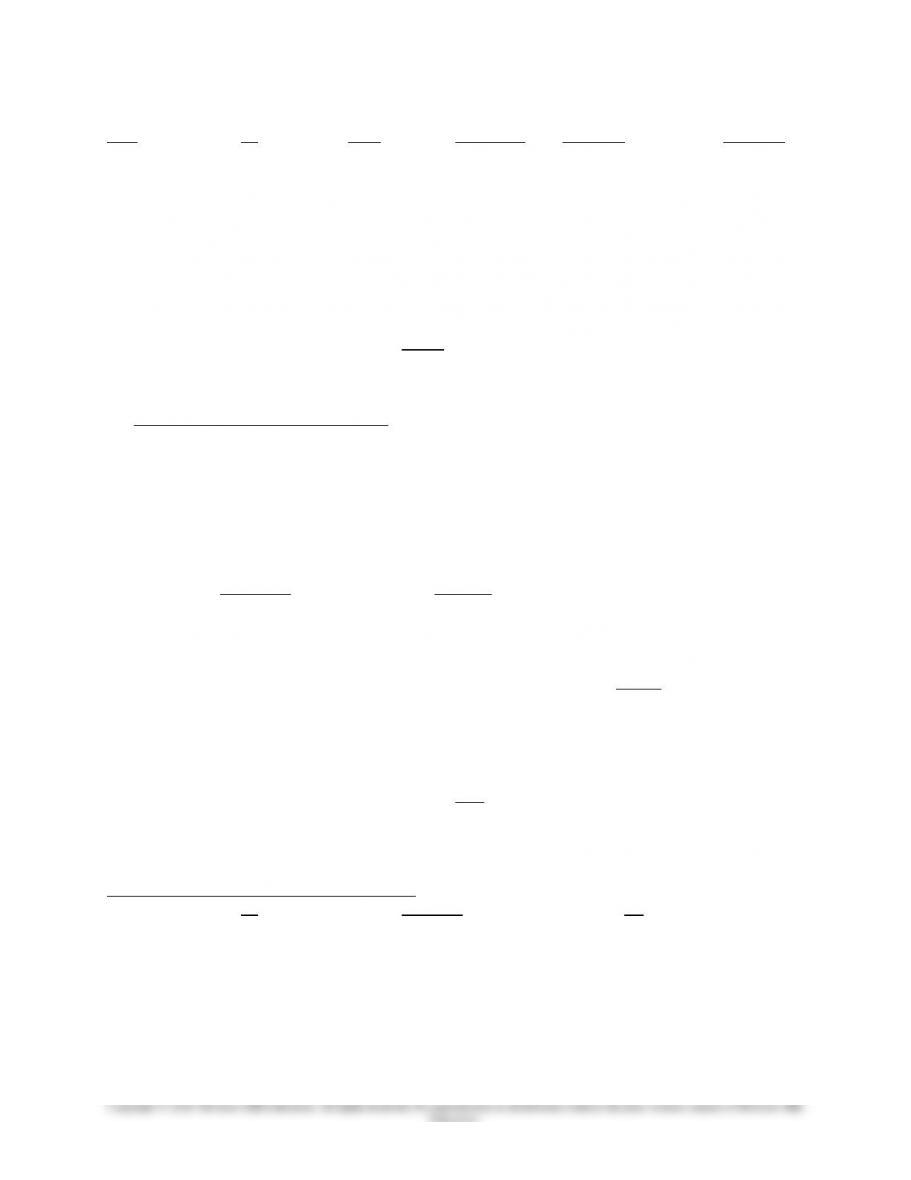

6. Based on your previous answers, develop a fair-market value for Midwest’s common stock.

Use an average for each of the values produced in part 5 above:

. Asset-based: $ 32.51

B. Market comparison: $ 31.84

C. Discounted cash flow: $ 34.55

D. Capitalization of earnings

1. Historic: $ 21.51

2. Projected: $ 39.03

$159.44 / 5 = $31.89

7. Have Frank Armstrong draft a response to Georgia Chemical in Atlanta covering the following

points:

The Board’s surprise at the purchase inquiry since Midwest has not made public an interest to

The above strategy would (1) determine the seriousness of the offer, (2) enable Allen and Warren to

complete their internal analysis of the value of Midwest, and (3) provide time for a “cooling-off” period

by the Board and provide time for reflection by Fletcher.

However, it should be noted that Fletcher owns 41.8% of Midwest shares. Also, the pension funds own

10.4% of the shares voted by Allen. These two blocks of stock give Fletcher 52.2% of the voting shares.

Allen will vote the pension fund shares the way Fletcher, his boss, tells him to vote the shares. In short,

Fletcher still controls Midwest. No sale will take place until Fletcher agrees to the sale no matter what

negotiations take place.

8. Once a price is agreed upon by a buyer and a seller, sales terms must be structured.

. Will the price be paid in cash at closing?

Rarely is the full purchase price paid in cash at closing.

As an initial cash payment plus future payments?

Yes, this is the traditional method of payment.

As stock or some combination of the aforementioned?

Possible, but not very likely. Sellers want as much cash as possible and buyers want as

much control of their new business as possible. Cash and debt instruments are the

preferred method of payment.

B. Will stock and assets be sold?

20-7

Education.

Chapter 20 – Management Compensation, Business Analysis, and Business Valuation

Either method of transfer of ownership is acceptable. Each part to the transaction needs to

address this issue in terms of tax liabilities, concern about unexpected events within the

firm, and related uncertainties.

Will the sales terms affect the price? YES.

Traditionally there is a continuum where all cash and lower sales price is at one end and

zero cash and higher sales price is at the other end. Sellers want cash, usually, and buyers,

usually, want to pay with anything but cash. The normal give and take of negotiating

works each group to a point on the continuum where each assumes they have optimized

their winning position.

20-8

Education.

20-2. Evaluating a Firm

This case describes the financial analysis of the W. T. Grant retail firm in the five years prior to its

bankruptcy in 1975. To disguise the case, the actual dates are not used in the text. The year 19X8

represents the actual year 1968, and so on. The case is useful to point out some of the limitations of

financial analysis based primarily on ratio analysis, and to point out the importance of analyzing cash

flows, especially for firms under financial stress, as was W. T Grant in the early 1970s.

The article by Largay and Stickney in the August, 1980 Financial Analysts Journal (“Cash Flows,

Ratio Analysis, and the W.T. Grant Company Bankruptcy”) is the basis for the following discussion.

“Although they surfaced as a gusher rather than a trickle, the problems that brought the W.T.

Grant Company into bankruptcy and ultimately, liquidation, did not develop overnight. Whereas

traditional ratio analysis of Grant’s financial statements would not have revealed the existence of many of

the company’s problems until 1970 or 1971, careful analysis of the company’s cash flows would have

revealed impending doom as much as a decade before the collapse.”

Grant’s continuing inability to generate cash from operations should have provided investors with

an early signal of problems. Yet as recently as 1973, Grant stock was selling at nearly 20 times earnings.

Investors placed a much higher value on Grant’s prospects than an analysis of the company’s cash flow

from operations would have warranted.” (Largay and Stickney, p51)

The analysis of liquidity and profitability ratios is shown below.

20-9

Chapter 20 – Management Compensation, Business Analysis, and Business Valuation

Liquidity

Ratios Relevance 2008 2009 2010 2011 2012 2013

A/R

Turnover

The average number of times per yr.

net receivables turn into cash.

Indicates effectiveness of credit policy

and collections. Should be compared

to prior years and to industry averages.

3.74 3.57 3.20 3.07 3.23

Ratio

(Acid Test)

ratio, but more conservative. Includes

only highly current assets-cash,

marketable securities, and receivables.

2.19 2.03 2.17 2.13 2.22 2.36

liabilities

Looks OK overall, but for recent buildup in inventory and receivables; all ratios look stable. The key is to see that the cash flow ratio is falling steadily, with a

sharp drop in the recent year. This shows that the company is beginning to fund operations through long term debt, a signal of sever liquidity problems. Note

that the conventional liquidity measures do not tend to show this, and disguise the rapid build up in receivables in inventory.

20-10