Chapter 12 – Strategy and the Analysis of Capital Investments

2. Perform a detailed financial analysis of the Park Hill Acres superstore option assuming the

Webster Street store remains open. In your analysis include your judgments and rationale for

dealing with the ‘sales erosion’ from the Webster Street store.

Answer: In preparing this question, students will need to initially develop three sets of pro forma

spreadsheets. Students will need one spreadsheet that projects the Park Hill Acres store without the

superstore investment. Case Exhibits 1 and 4 provide students the basic information and assumptions to

develop this spreadsheet. Appendix I and Table 1 provide this set of pro formas and assumptions.

In order to consider the profitability of a superstore for the Park Hill Acres location, students will need to

develop a second spreadsheet that reflects the projections with this new facility. The data to develop this

spreadsheet is included in Exhibits 1, 4, and 5. In this spreadsheet, students need to calculate incremental

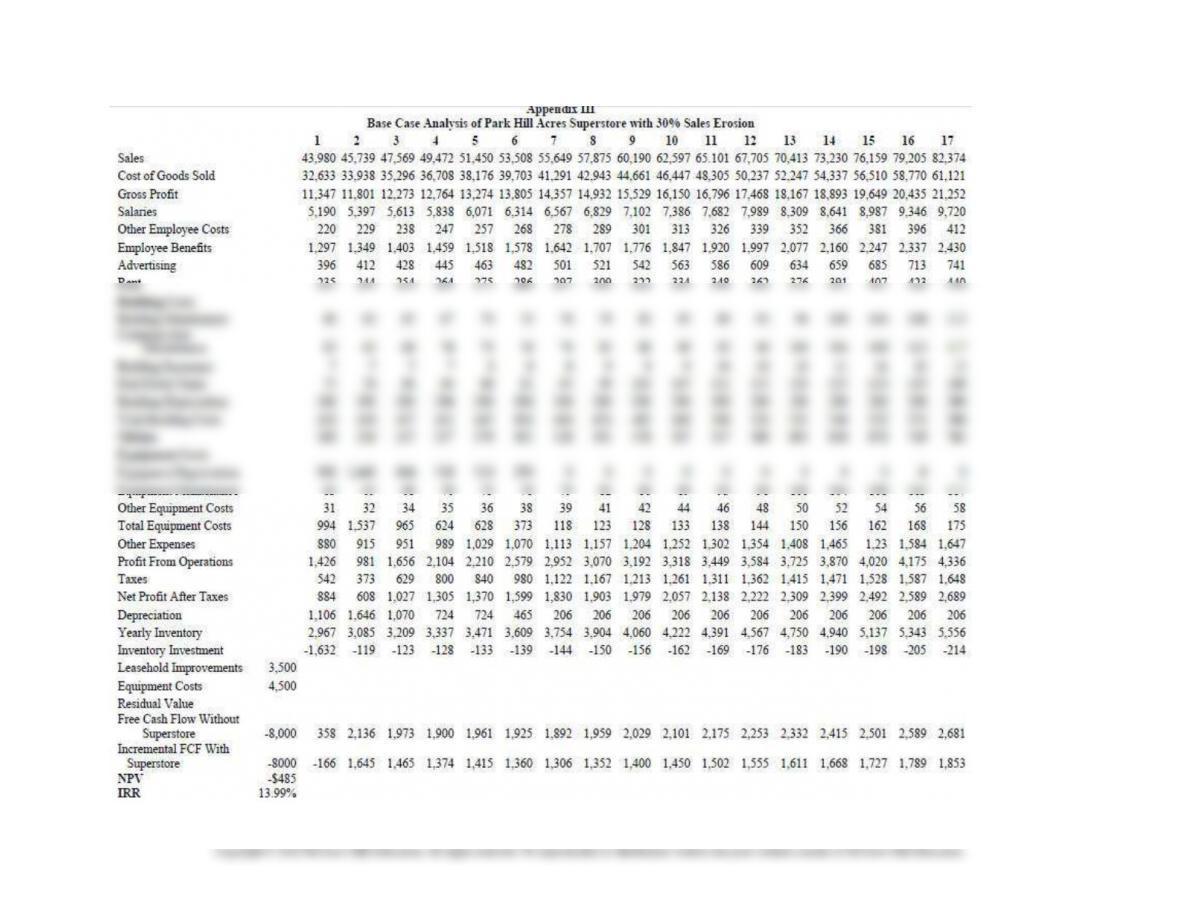

teaching guide provides a re-estimate of the superstore’s profitability assuming that 30 percent of the sales

are not incremental sales (i.e. 30 percent of the Webster Street store sales are shifted to Park Hill Acres).

Appendix III clearly shows that the CFO’s concerns are material. If these sales are eliminated, then the

NPV on the superstore becomes negative (-$ .485 million) and the IRR of 13.99 percent is less than

CLM’s cost of capital of 15 percent. (Note: Some students will question whether the cost of capital

should be 15 percent for all the alternatives. The belief is that the projects which may encounter

erosion should use a higher discount rate. This can be an interesting point of discussion. The case

authors believe that the current risk of operating in a competitive environment is captured by the

15 percent cost of capital. The risk of losing a customer to competition versus sales erosion can be

considered to be equal. Trying to estimate what difference there might be would probably introduce

more error.)

Having established the importance of the sales erosion issue, students should determine the maximum

level that the sales erosion can be before the project’s NPV becomes zero. Determining the project’s

determine the maximum level. Otherwise, students can determine this figure by trial and error).

The above analysis establishes the critical range for sales erosion. However, students still need to

12-11

Education.

Chapter 12 – Strategy and the Analysis of Capital Investments

value of the Webster Street store decreases from $2.112 million as illustrated in Appendix V to $1.012

million as illustrated in Appendix VII.

If it is highly probable that Albertsons will build a superstore, then CLM could potentially lose $2.417

million in value between the Webster Street and Park Hill Acres stores. By contrast, if CLM builds a

superstore at the Park Hill Acres location that erodes 30 percent of sale at the Webster Street store, it will

only reduce shareholders value by -$ 0.485 million. Hence, CLM is better off to shift sales from its

Webster Street store to a new Park Hill Acres superstore rather than losing the sales to its competitor

Albertsons.

3. Prepare a financial analysis of all of the feasible investment alternatives available to CLM in the

Park Hill area. Identify two options that warrant serious consideration based on this financial

analysis.

Answer: Since some of the options represent financial projections involving both stores, students will

need to break their analysis into two parts in order to answer this question. First, students will need to

estimate the economic impact of each option on each store. Second, the NPV for each of these ‘stand

alone’ store economics can be combined to determine the overall financial impact.

In order to complete the first part of this question, students need to develop individual store financial

projections for the following situations:

Appendices VIII and IX include the pro forma projections for the store expansion for the Park Hill Acres

store. Appendix VIII includes the pro formas without the expansion. Appendix IX includes the pro formas

probability that Albertsons will put in its own superstore in the Park Hill Acres area.

The cost of closing the Webster Street store includes both direct costs and opportunity costs. As disclosed

12-12

Education.

Chapter 12 – Strategy and the Analysis of Capital Investments

in Case Exhibit 5, the direct costs include the store closing costs of $500,000 plus the lease termination

costs. The lease termination costs include the $100,000 penalty along with the present value of lease costs

for the remaining five years of the lease as calculated below:

$1.298 million in opportunity costs).

Students can now combine the ‘stand-alone’ economics to determine the NPVs for each of the investment

options for the Park Hill area.

(Note: In reviewing the analysis with students, the instructor can underscore the point that CLM

needs to use NPV as the investment standard rather than IRR because the NPVs for the individual

store options can be added together to determine the overall profitability of the option. Since IRR

violates the ‘additive principle’, one cannot accurately compare the options using the IRR criteria).

In order to develop the NPV for the various combined options from the stand-alone economics in the

appendices, students need to recall that the ‘stand-alone’ economics for a store remodel or expansion are

presented in incremental terms. For example, the NPV for the conversion of the Park Hill store to a

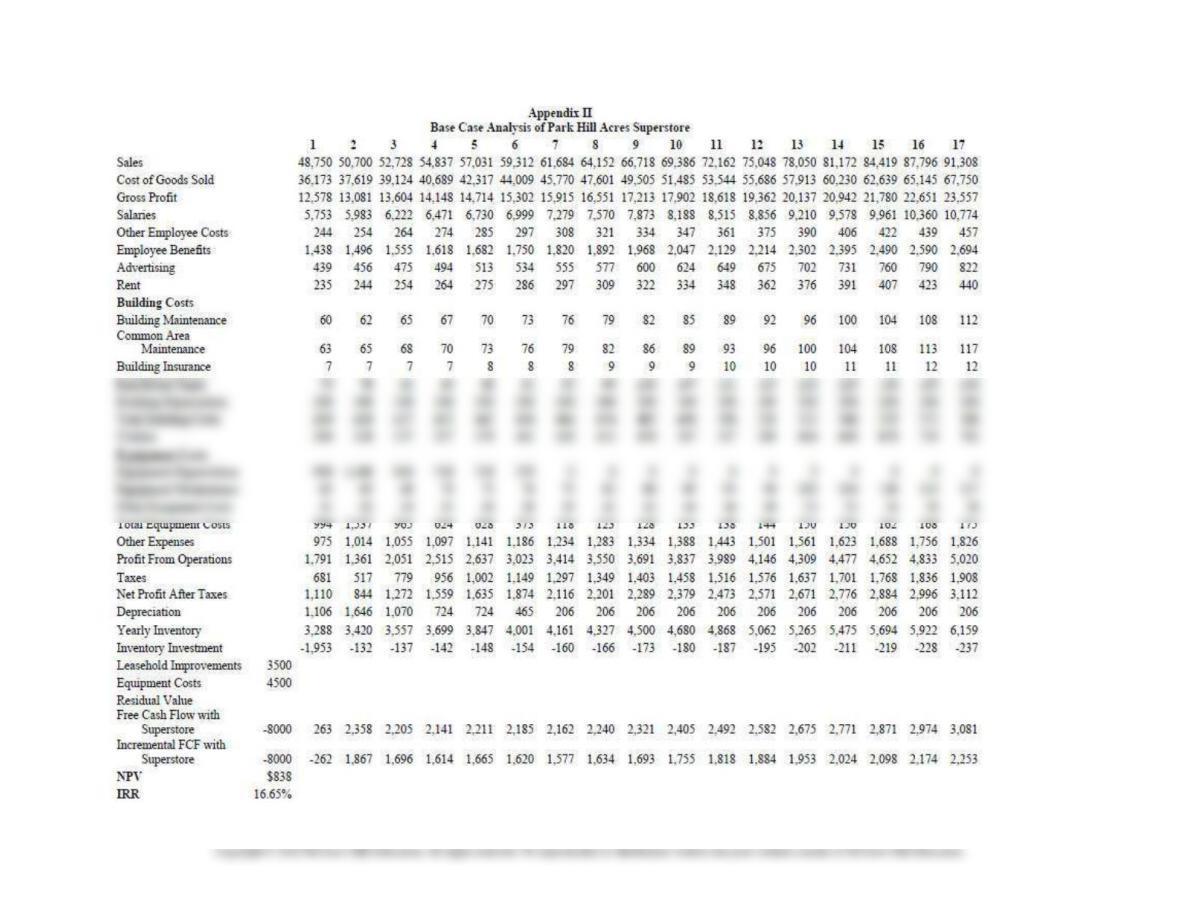

superstore is $0.838 million as illustrated in Appendix II. This $.838 million is the incremental NPV on

the incremental amount of $8 million. In order to determine the ‘absolute’ or ‘total’ NPV for the Park Hill

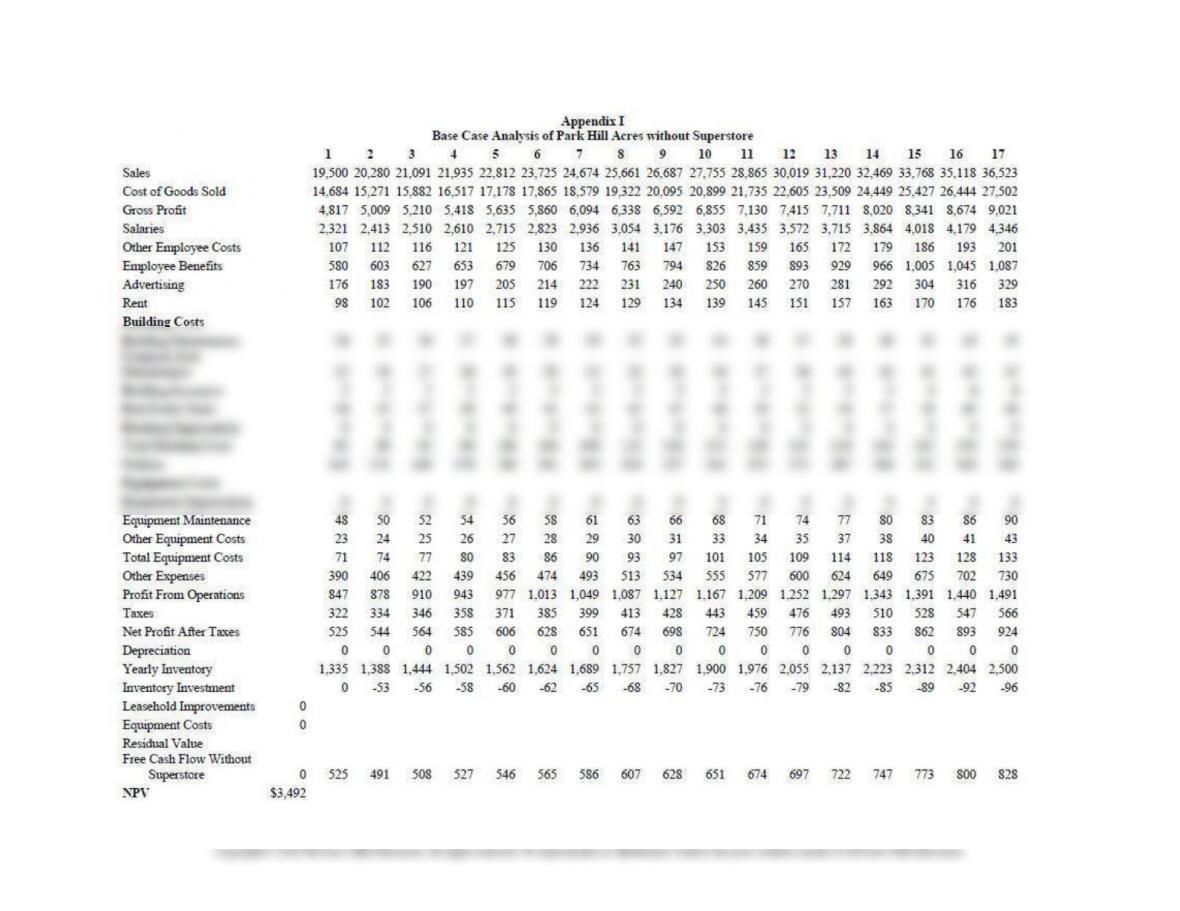

Superstore, students have to add the $0.838 in Appendix II to the NPV for the base case (no investment)

from Appendix I, which is $3.492 million. Hence, the ‘absolute’ or ‘total’ NPV for the conversion of the

Park Hill store to a superstore is $4.33 million. Likewise, the incremental NPV for expanding the Webster

store is ($1.005 million) as shown in Appendix XI. When this incremental NPV is combined with the

NPV for the base case of no investment as listed in Appendix X, students can see that the ‘absolute’ or

‘total’ NPV for expanding the Webster store is $1.107 million. In order to compare the various store

investment options for CLM, students need to convert from incremental ‘stand-alone’ NPV’s to ‘absolute’

or ‘total’ NPVs. The ‘absolute’ or ‘total’ NPVs for each of the options is calculated as follows:

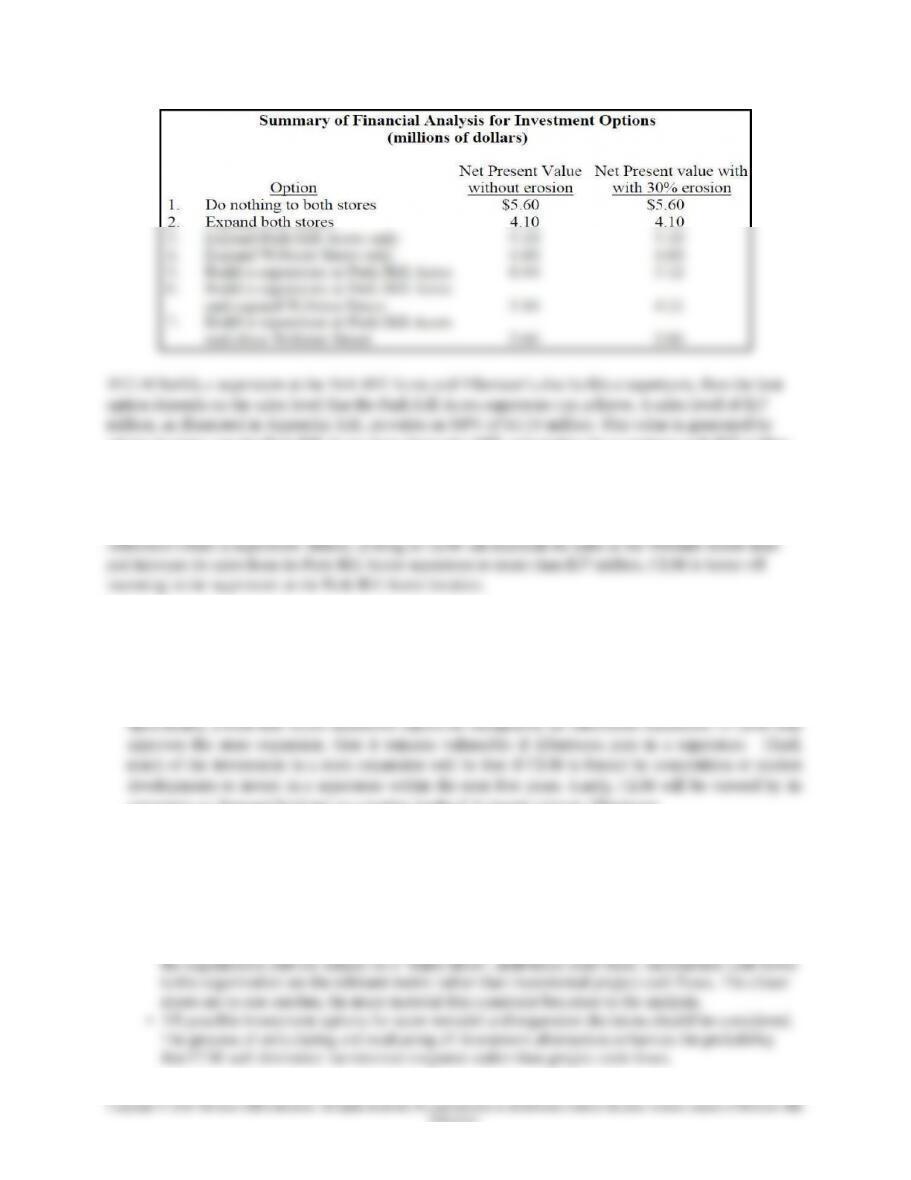

Option 1 – do nothing to both stores: Added value is $5.60 million. This number is the sum of the NPV

12-13

Education.

Year Lease Cost PV Factor (5%) PV

1 $79,400 .9524 $75,619

2 $82,576 .9070 $74,899

Chapter 12 – Strategy and the Analysis of Capital Investments

Option 2 – expand both stores: Added Value is $4.10 million. This number is the sum of the NPV of

$3.492 million from Appendix VIII plus the negative NPV of ($0.504) million from Appendix IX.

Option 3 – expand the Park Hill Acres store only: Added Value of $5.10 million. This value is generated

Option 4 – expand the Webster Street store only: Added Value is $4.60 million. Following the same logic

Note that as with the Park Hill Acres store, the expansion of the Webster store is negative.

Option 5 – build a superstore at the Park Hill Acres location: The value of this decision depends on the

degree of sales erosion that CLM suffers at its neighboring stores. If there is no erosion, the superstore

Option 6 – Build a superstore at the Park Hill Acres and expand the Webster Street store: Here again the

Option 7–build a superstore at the Park Hill Acres location and close the Webster Street store: This

This financial analysis indicates that the best financial option for CLM is a function of a) the amount of

sales erosion; b) Albertson’s decision regarding a superstore in the Park Hill area; and c) the level of sales

growth that a Park Hill superstore could achieve given an Albertson’s superstore. As the following table

12-14

Education.

Chapter 12 – Strategy and the Analysis of Capital Investments

taking the base case for Park Hill Acres from Appendix VIII, subtracting the superstore with $37 million

in sales, Appendix XIII, and adding the base case for the Webster Street store from Appendix X ($3.492 –

2.108 + 2.112).

A NPV value of $3.19 million is, as illustrated in Question 2, the same NPV as if CLM did nothing and

4. Recommend which option CLM should select for the Park Hill Acres area.

Answer: The superstore option for Park Hill Acres appears to be the better of the two alternatives for

several reasons. First, the NPV is greater for this option as compared to the ‘expansion only’ option.

Second, the superstore alternative represents a better defensive strategy than the expansion option.

customers as ‘forward-looking’ as a market leader if it invests prior to Albertsons.

5. Recommend policies that CLM should adopt in evaluating other store remodel/expansion

investment situations.

Answer: There are several important policy guidelines that students should identify for the evaluation

of other remodeling or expansion investment situations as follows:

•Individual store remodel or expansions need to be considered in light of their overall impact on

12-15

Education.

Chapter 12 – Strategy and the Analysis of Capital Investments

•Sensitivity analysis should be utilized to quantify the critical range for sales erosion.

•CLM decision-makers need to anticipate the probability of its competitions’ investment decisions

to judge the relevance and significance of sales erosion.

•NPV should be the primary financial investment tool utilized to evaluate various investment

options rather than IRR.

Note to Instructors: Embedded below is an Excel spreadsheet that can be used to generate the solution

tables to follow.

12-16

Education.

Microsoft Excel

Worksheet

Chapter 12 – Strategy and the Analysis of Capital Investments

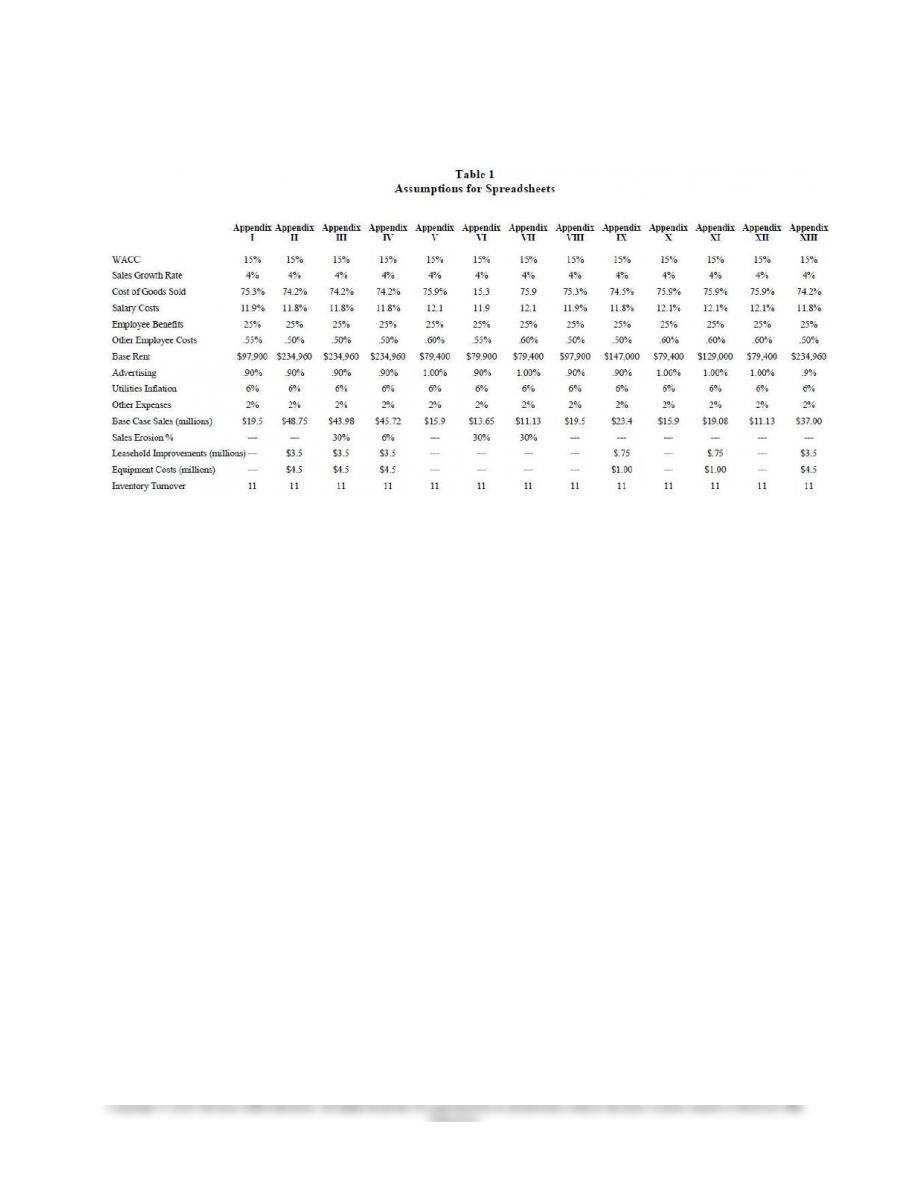

Table 1 Assumptions for Spreadsheets

12-17

Education.

Chapter 12 – Strategy and the Analysis of Capital Investments

12-18

Chapter 12 – Strategy and the Analysis of Capital Investments

12-19

Chapter 12 – Strategy and the Analysis of Capital Investments

12-20