Chapter 5 – Activity-Based Costing and Customer Profitability Analysis

The Value Chain

Timber; do we harvest our own timber?

Sorting and preparing timber; receiving the lumber in the pulp plant

Pulp manufacturing

Debarking; a 16×100 ft drum; tumbling the logs

Chipping; into 1” cubes

Digesting; heat and soak with chemicals

Bleaching; brown to white

Paperboard production

Headbox; mix pulp cubes with water and chemicals

Wire; paper mixture is applied to wire mesh that travels through a press and forces the

Pulp mixture against the wire to remove water

Drying; cylindrical dryers and steam are used

Rolling; into “parent” rolls

Further processing

Coating

Rewinding and slitting

5-31

Education.

Chapter 5 – Activity-Based Costing and Customer Profitability Analysis

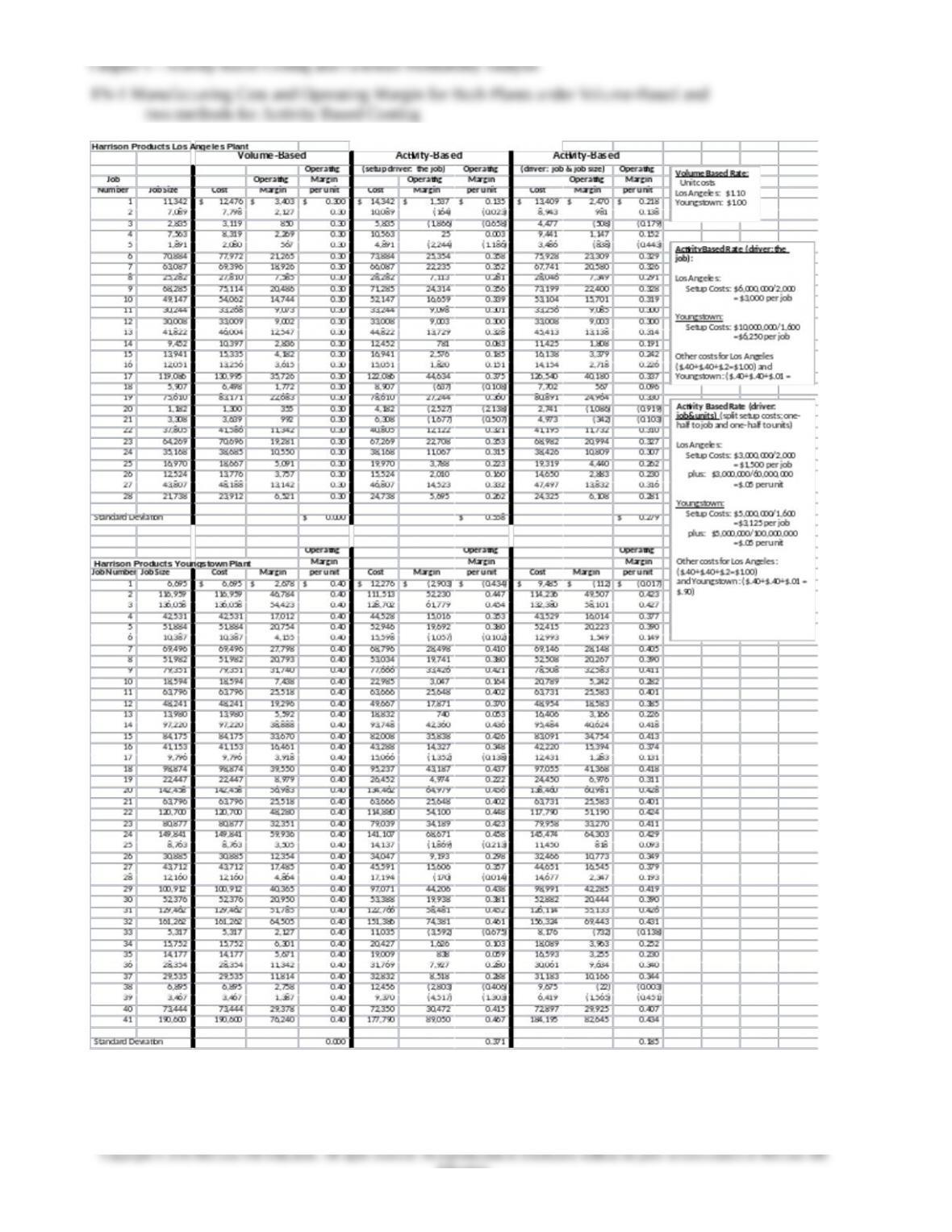

5-5 Harrison Products, Inc

The Harrison Products Inc (HPI) case is based on disguised information and data taken from that of a U.S.

multinational company. Many of the costing and strategic issues addressed in the case are faced by that

company. The main issues are (1) what costing system to use and (2) what manufacturing strategy to use to

best serve the company’s customers and to meet the competitive challenge of low cost. The case is intended

for the undergraduate cost course, the advanced cost/managerial course and the MBA managerial course.

Because of the amount of data involved and the analysis required, Excel is strongly recommended for the

solution of the case.

The main learning objectives of the case are to examine the application of volume-based and activity-based

costing in a manufacturing context. There are three unique issues in the case:

1. How to determine the cost driver for setup costs. The student is asked to determine the amount

of ABC cost allocated to a sample of jobs using two different assumptions of how setup costs

occur in this manufacturing case. The objective is to have the students understand that it is

important to carefully determine the cost driver; it may be a simple job-based driver, or a time-

based, or unit-based approach.

2. To understand the possible influence of batch size not only on batch level costs but also on unit

level costs. In the case data, which (while disguised) reflects the actual experience of the U.S.

multinational upon which this case was developed, it is clear from further analysis that larger

batch sizes lead to faster runtimes, leading to lower unit costs. The link between batch size and

unit cost has been understood for some time but is not often included in cases for student study

and analysis.

3. To understand how manufacturing strategy can affect product costs. In this case, one of the

company’s plants was designed for relatively large batch sizes and the other was designed for

smaller batches. Both batch-level and unit-level costs are affected by these design decisions.

Answers to Questions:

1, 2, and 3: The answers to parts 1,2 and 3 are shown in TN-1. The solution also shows the

operating margin per unit which is useful in the discussion of the requirement 4. The calculation of the

volume-based and activity-based rates is shown on the right-hand side of the Exhibit. It is highly

recommended that students be required to solve the case using Excel.

4. In comparing the results for parts 1,2 and 3, it is apparent that the volume-based approach, as it

is based only on volume, produces the same unit costs for each job, irrespective of job size.

Thus, the operating margin per unit is the same for each job ($0.30 for the Los Angeles plant

The method illustrated in part 3 reduces the effect of setup costs on job profitability, since in

this case the total setup costs are charged one-half to the job and one-half to units. The result is

that the smaller jobs are more profitable under the part 3 method than for the part 2 method,

though many of the smaller jobs are still unprofitable under the part 3 method.

The standard deviation of the operating margin per unit is shown for each of the three

methods and each plant; the variation is greatest for activity-based costing (part 2 method) and of

course zero for the volume-based method.

The activity-based methods in parts 2 and 3 are preferred over the volume-based method

because they appropriately apply the job-related setup costs to each job and thereby recognizing

5-32

Education.

Chapter 5 – Activity-Based Costing and Customer Profitability Analysis

the more accurate cost for each job. The method in part 3 would be preferred since it takes into

account the additional clean-up and preparation time required after the larger jobs. Generally,

determining which of the two activity-based methods is best would require a careful study of

what drives setup time and costs, information which is not available in the case. The point of

this question is to prompt a brief discussion of the importance of properly identifying the cost

drivers to be used in ABC costing. The goal is to get product costing to most accurately reflect

the way costs are incurred in the manufacturing process.

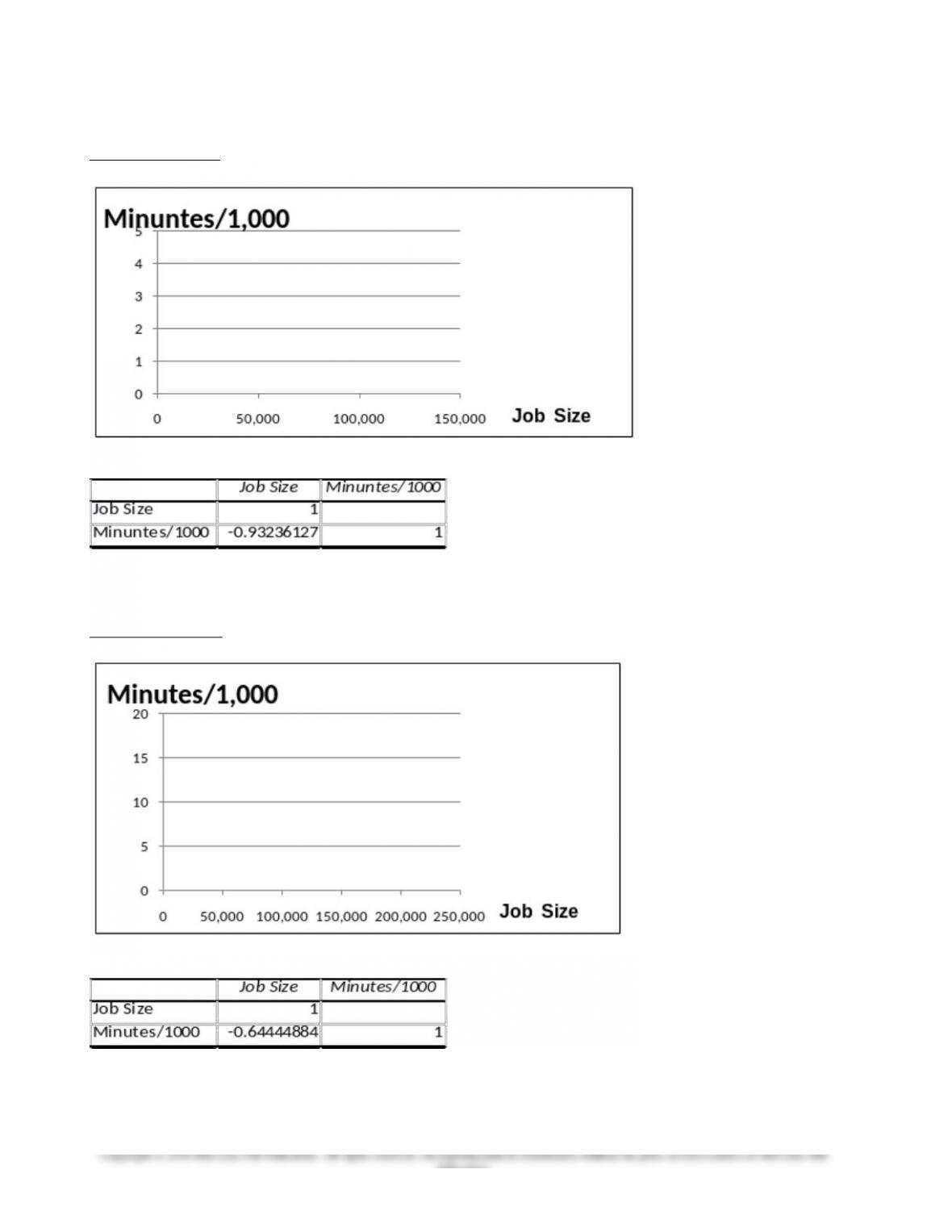

5. A graphical and correlation analysis for both plants, showing the relationship between job size

and runtime is in Exhibit TN-2. The graphs in particular show clearly that the Los Angeles plant,

the newer plant, has faster runtime for smaller jobs. This can be seen from the graph and also

by reviewing the 6-8 smallest jobs in both plants together with the related runtimes. Small

orders at the Youngstown plant have much longer runtimes. Both plants, with larger orders,

show about two minutes per 1,000 units average runtime (though the Youngstown plant gets to

the two minute mark at a slightly lower job size than the Los Angeles plant). The bottom line:

orders under approximately 50,000 units have relatively high runtimes at Youngstown, and only

somewhat elevated runtimes at Los Angeles. There are two implications of this finding:

a. It is clear that, for small orders, job size affects not only setup costs per unit but also

runtime cost per unit. An operations employee at the company originally studied in this

case explained that a key reason for the effect of batch size on average runtime is that the

equipment operators normally ran the machines slowly at the start of the job to make

the total runtime.

The implication for product costing is that product cost systems should recognize

the increased unit-level or other batch level costs (in this case, runtime) as batch sizes

approach critical thresholds (in this case, about 50,000 units in the job). That is, changes

in job order size affect not only total batch level costs (e.g., setup cost) but also

potentially the unit-level costs.

b. The implication for manufacturing strategy is the importance of matching factory design

to customer order type. In this case, HFI has lower costs when small orders are

5-33

5-34

Education.

Chapter 5 – Activity-Based Costing and Customer Profitability Analysis

TN-2: Analysis of the Relationship between Runtime and Job Size for Los Angeles

and Youngstown Plants

Los Angeles Plant

Correlation: Job Size and Runtime

Youngstown Plant

Correlation: Job Size and Runtime

Teaching Strategies for Readings

5-35

Education.

Chapter 5 – Activity-Based Costing and Customer Profitability Analysis

5-1 Activity-Based Costing and Predatory Pricing: The Case of the Petroleum Retail Industry

1. What are product-cost subsidizations?

2. What are possible consequences of product-cost subsidizations?

3. List alternative approaches to assign costs in a gasoline service center.

Three approaches can be employed to assign gasoline service center costs to products:

4. Identify cost hierarchy level groups in classifying activities at the retail level of a gasoline service center

and give at least one example each.

Unit-level activities are undertaken for each gallon of gasoline sold (such as electricity to power

pumps when dispensing gasoline);

Batch-level activities are the same for each gasoline transaction irrespective of the volume of gasoline

other centralized activities).

5. What are overheads activity-cost pools pertaining to selling gasoline in a retail gasoline service center and

what is the activity level for each of the cost pools?

Gasoline Sales Attendants (Labor): Attendants are needed to receive payments from customers who do

not pay electronically at the gasoline pump. This is a batch-level activity because payment

transactions occur only once for each purchase of gasoline, regardless of the volume of gasoline

purchased.

Kiosk Facility and Gasoline-Dispensing Facility: Rental value of the kiosk (retail gasoline facility)

that facilitates the payment transactions for gasoline purchase. This is a batch-level activity, as it

5-36

Education.