Chapter 10 – Strategy and the Master Budget

the upcoming year. This increased evaluation of expenditures would make it

10-47 (Continued)

difficult to include budgetary slack in the budget for the upcoming year and

likely uncover opportunities of cost savings and operational improvements.

c. The biggest disadvantage of ZBB is the significant amount of time and cost

10-50

Education.

Chapter 10 – Strategy and the Master Budget

10-48 Budgetary Pressure and Ethics (30 minutes)

1. The use of alternative accounting methods to manipulate reported earnings is

professionally unethical because it violates the Standards contained in the IMA’s

Statement of Ethical Professional Practice (see: www.imanet.org). The

Competence standard is violated because of failure to perform duties in

2. Yes, costs related to revenue should be expensed in the period in which the

revenue is recognized (“matching principle”). Perishable supplies are purchased

for use in the current period, will not provide benefits in future periods, and should

therefore be matched against revenue recognized in the current period. In short,

3. The actions of Gary Woods were appropriate. Upon discovering how supplies

were being accounted for, Wood brought the matter to the attention of his

immediate superior, Gonzales. Upon learning of the arrangement with P&R, Wood

told Gonzales that the action was improper; he then requested that the accounts

be corrected and the arrangement discontinued. Wood clarified the situation with

10-51

Education.

Chapter 10 – Strategy and the Master Budget

PROBLEMS

10-49 Budgeting for a Merchandising Firm (50 minutes)

1. Budgeted cash collections—December:

From November’s sales = net A/R, November 30th (given) =

2. Net (i.e., book value of) accounts receivable—December 31 st

:

Budgeted sales in December (given) $250,000

Allowance for doubtful accounts $250,000 × 2% = 5,000

3. Budgeted pre-tax operating income—December:

Total sales (given) $250,000

Gross margin ratio × 30%

Gross margin $ 75,000

Operating expenses:

4. Budgeted Inventory—December 31 st

:

5. Budgeted Purchases—December:

Inventory, December 1st (given) = $132,000

Plus: Purchases during December (plug figure) = 169,000

Cost of goods available for sale ($120,000 + $165,000) = $301,000

10-52

Education.

Chapter 10 – Strategy and the Master Budget

10-49 (Continued)

6. Budgeted Accounts Payable—December 31 st

:

Accounts Payable, December 1st (given) $162,000

Plus: Budgeted Purchases, December (part 5 above) $169,000

Total Accounts Payable during December $331,000

10-53

Education.

Chapter 10 – Strategy and the Master Budget

10-50 Comprehensive Profit Plan (90 minutes)

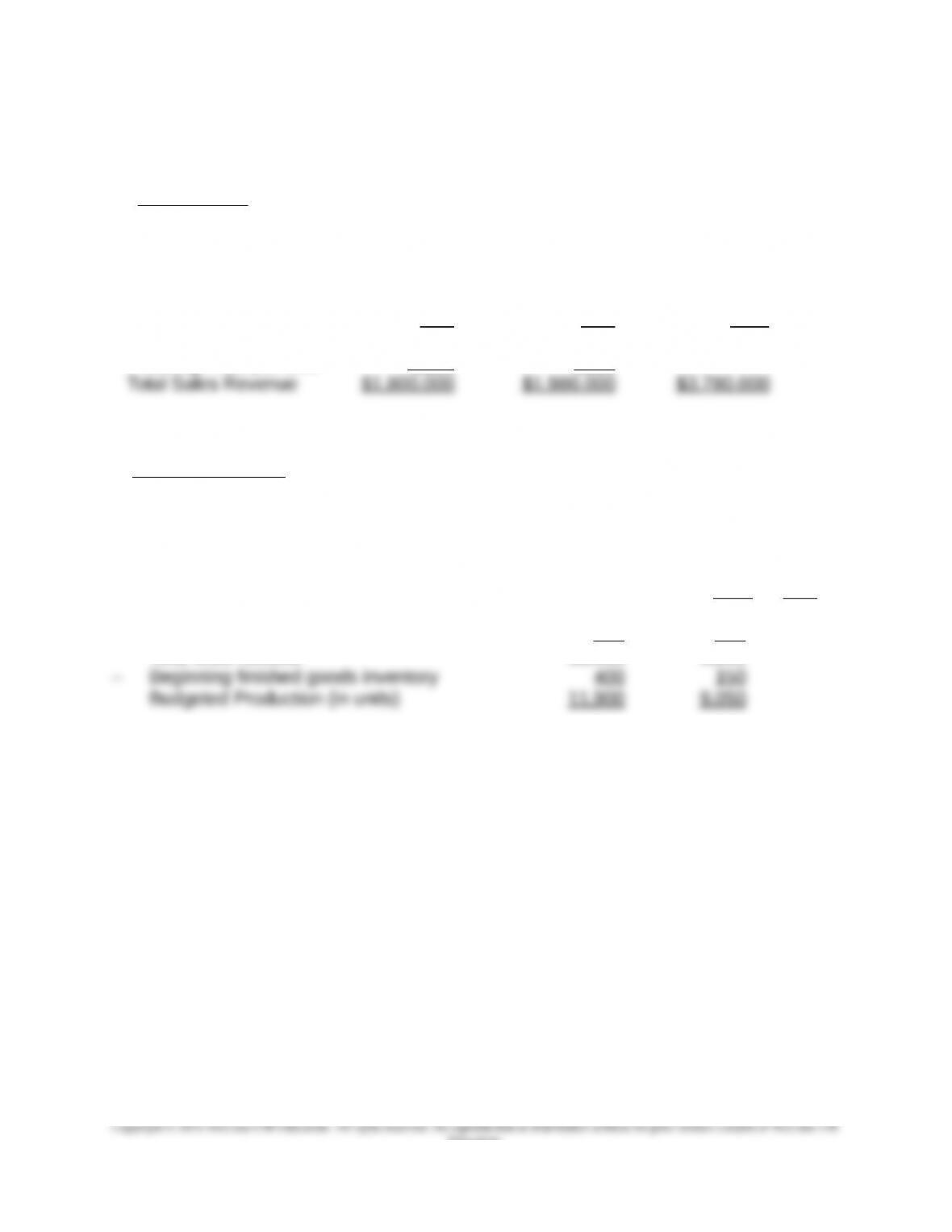

1. Sales Budget

Spring Manufacturing Company

Sales Budget

2016

C12 D57 Total

Sales (in units) 12,000 9,000 21,000

× Selling Price per Unit $150 $220

2. Production Budget

Spring Manufacturing Company

Production Budget

2016

C12 D57

Budgeted Sales (in units) 12,000 9,000

+ Desired finished goods ending inventory 300 200

Total units needed 12,300 9,200

10-54

Education.

Chapter 10 – Strategy and the Master Budget

10-50 (Continued-1)

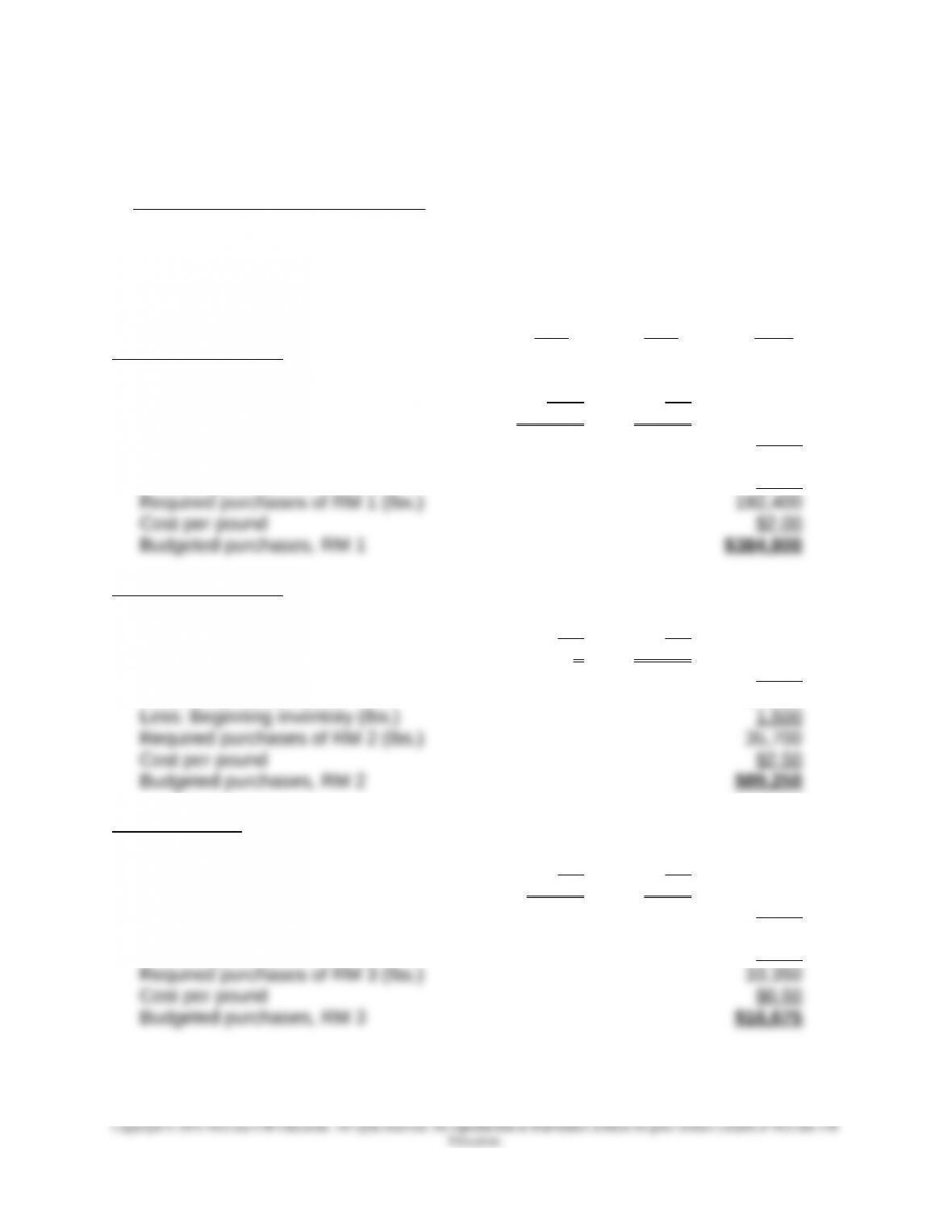

3. Direct Materials Purchases Budget

Spring Manufacturing Company

Direct Materials Purchases Budget (units and dollars)

2016

C12 D57 Total

Raw Material (RM) 1:

Budgeted Production 11,900 9,050

Pounds per Unit × 10 × 8

RM 1 needed for production 119,000 72,400 191,400

Plus: Desired Ending Inventory (lbs.) 4,000

Total RM 1 needed (lbs.) 195,400

Less: Beginning inventory (lbs.) 3,000

Raw Material (RM) 2:

Budgeted Production 11,900 9,050

Pounds per Unit × 0 × 4

RM 2 needed for production 0 36,200 36,200

Plus: Desired Ending Inventory (lbs.) 1,000

Total RM 2 needed (lbs.) 37,200

Raw Material 3:

Budgeted Production 11,900 9,050

Pounds per Unit × 2 × 1

RM 3 needed for production 23,800 9,050 32,850

Plus: Desired Ending Inventory (lbs.) 1,500

Total RM 3 needed (lbs.) 34,350

Less: Beginning inventory (lbs.) 1,000

10-55

Chapter 10 – Strategy and the Master Budget

10-50 (Continued-3)

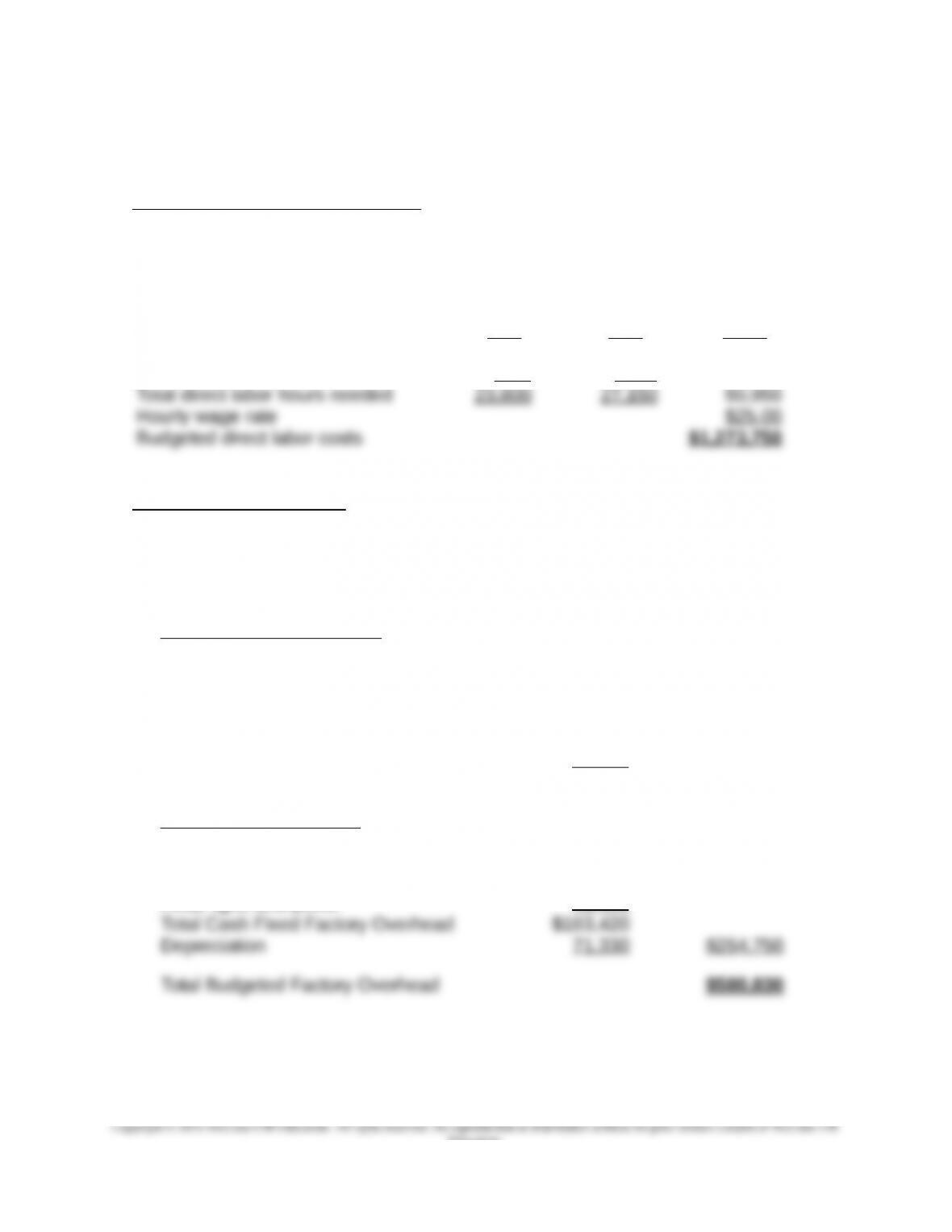

4. Direct Manufacturing Labor Budget

Spring Manufacturing Company

Direct Labor Budget

2016

C12 D57 Total

Budgeted production 11,900 9,050

Direct labor hours per unit × 2 × 3

5. Factory Overhead Budget

Spring Manufacturing Company

Factory Overhead Budget

2016

Variable Factory Overhead:

Indirect materials $10,000

Miscellaneous supplies and tools 5,000

Indirect labor 40,000

Payroll taxes and fringe benefits 250,000

Maintenance costs 10,080

Heat, light, and power 11,000 $326,080

Fixed Factory Overhead:

Supervision $120,000

Maintenance costs 20,000

Heat, light, and power 43,420

10-56

Education.

Chapter 10 – Strategy and the Master Budget

10-50 (Continued-4)

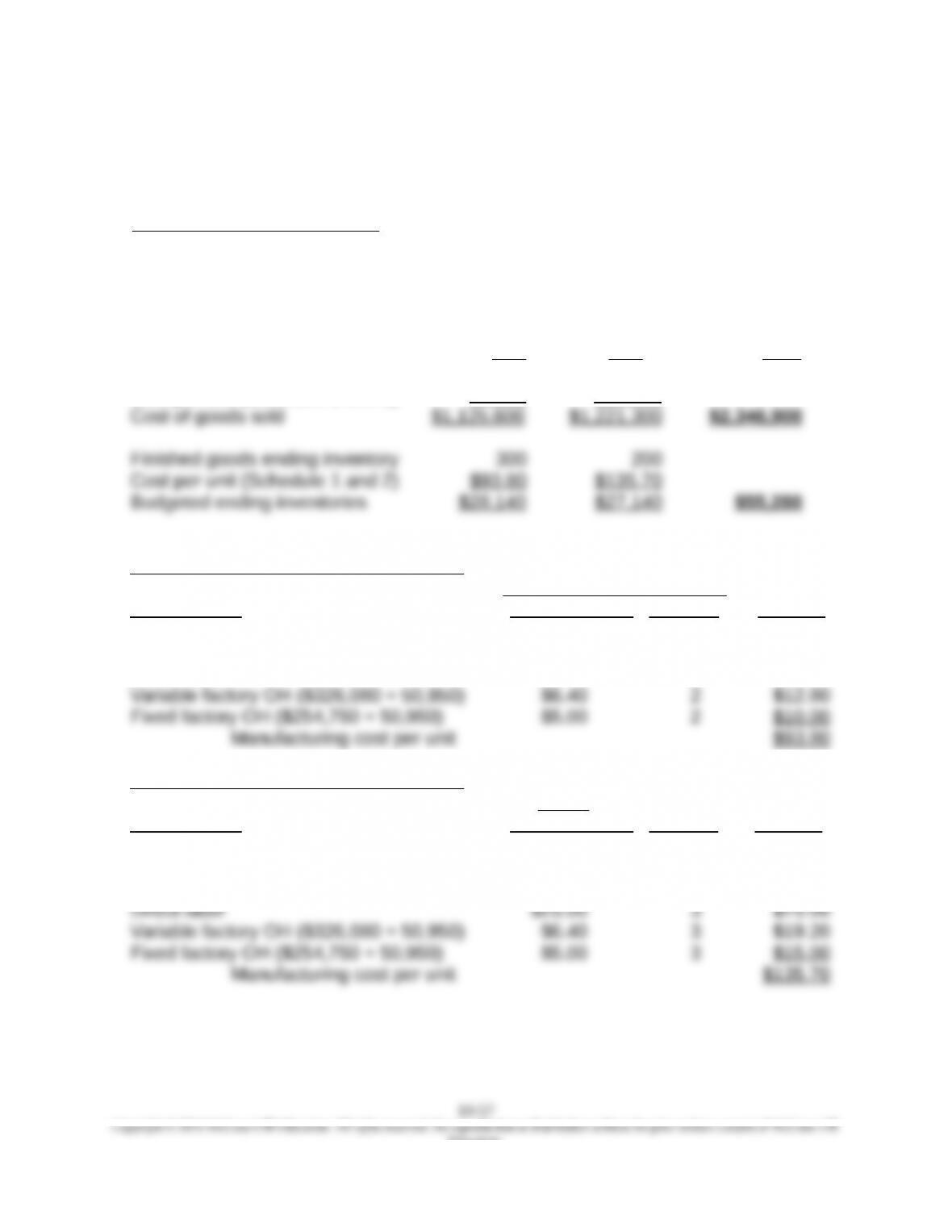

6. Budgeted Cost of Goods Sold

Spring Manufacturing Company

Ending Finished Goods Inventory and Budgeted CGS

2016

C12 D57 Total

Sales volume 12,000 9,000 21,000

Cost per unit (Schedule 1 and 2) $93.80 $135.70

Schedule 1: Cost per Unit–Product C12:

Inputs_____ Cost

Cost Element Unit Input Cost Quantity Per Unit

RM-1 $2.00 10 $20.00

RM-3 $0.50 2 $1.00

Direct labor $25.00 2 $50.00

Schedule 2: Cost per Unit–Product D57:

Inputs Cost

Cost Element Unit Input Cost Quantity Per Unit

RM-1 $2.00 8 $16.00

RM-2 $2.50 4 $10.00

RM-3 $0.50 1 $0.50

Education.

Chapter 10 – Strategy and the Master Budget

10-50 (Continued-5)

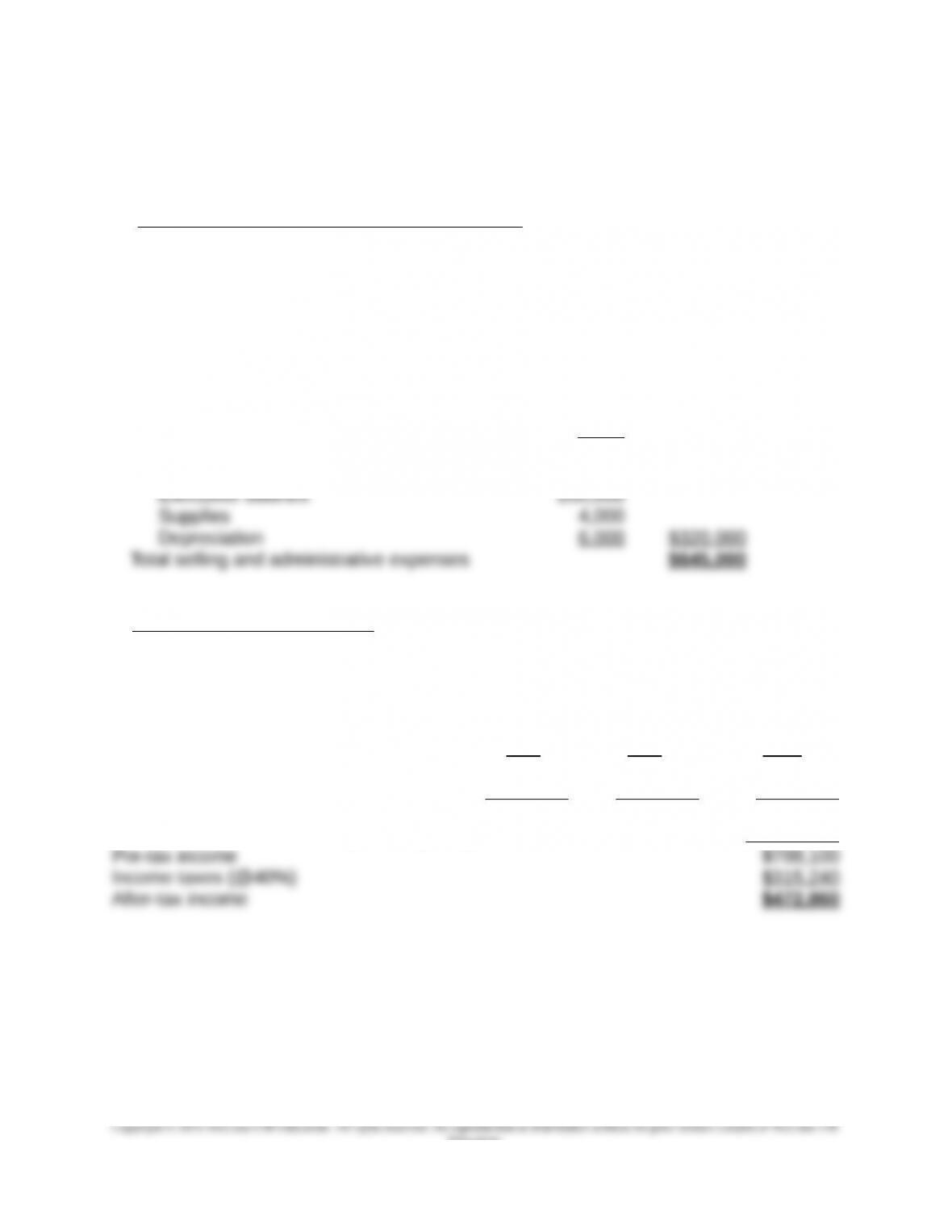

7. Budgeted selling and administrative expenses:

Spring Manufacturing Company

Selling and Administrative Expense Budget

2016

Selling Expenses:

Advertising $60,000

Sales salaries 200,000

Travel and entertainment 60,000

Depreciation 5,000 $325,000

Administrative expenses:

Offices salaries $60,000

8. Budgeted Income Statement:

Spring Manufacturing Company

Budget Income Statement

For the Year 2016

C12 D57 Total

Sales (part 1) $1,800,000 $1,980,000 $3,780,000

Cost of goods sold (part 6) 1,125,600 1,221,300 2,346,900

Gross profit $674,400 $758,700 $1,433,100

Selling and administrative expenses (part 7) $645,000

10-58

Education.

Chapter 10 – Strategy and the Master Budget

10-50 (Continued-6)

Note to Instructor: An Excel spreadsheet solution file is embedded in this document.

You can open the spreadsheet “object” that follows by doing the following:

1. Right click anywhere in the worksheet icon below.

2. Select “Worksheet Object,” then “Open.”

3. To return to the Word document, select “File” and then “Close and return to…”

while you are in the spreadsheet mode.

10-59

Education.

Pr. 10–50 7e.xlsx