Chapter 14 – Operational Performance Measurement: Sales, Direct-Cost Variances, and the Role of Nonfinancial

Performance Measures

CHAPTER 14:

OPERATIONAL PERFORMANCE MEASUREMENT: SALES, DIRECT–

COST VARIANCES, AND THE ROLE OF NONFINANCIAL

PERFORMANCE MEASURES

QUESTIONS

14-1 A master budget represents forecasted operating profit based on a single output

level (“planned sales”) for an upcoming period. As such, this budget is also

referred to as a static budget.

Pro-forma budgets represent budgeted operating income for various output

levels (production or sales). Pro-forma budgets can be prepared for any output

14-2 Standard costs (and selling prices), and their use in the construction of flexible

budgets (prepared after the current operating period is over), establish targets or

planned amounts as to operating earnings for a period. This information can be

used at the end of the period to determine why actual operating earnings for the

14-3 Management time is scarce. According to the philosophy of management by

exception, managers give primary attention to things (operations, sales

promotions, production, revenue growth, productivity gains, etc.) that are not

“abnormal” (i.e., an “exception”) it may trigger the need for an investigation to

uncover the underlying cause, which in turn may lead to some type of

intervention or change.

14-1

Education.

Chapter 14 – Operational Performance Measurement: Sales, Direct-Cost Variances, and the Role of Nonfinancial

Performance Measures

14-4 The performance of a division should not be considered as less than satisfactory

simply because all variances are “unfavorable.” For example, a company

Companies with such standards expect the division to meet the goals in each

and every operation.

14-5 Direct material price variances can be caused by any of the following factors:

purchasing material of a different quality than that envisioned in the standard

material cost; inapplicability of the standard cost per unit of raw material (i.e.,

outdated standards—the market price may have changed); purchasing was done

Purchasing Department. For example, if the Purchasing Department obtains

materials of lower quality than envisioned in the standard (perhaps to secure a

price savings), excessive spoilage and waste may occur during the production

process. Thus, in this case the Purchasing Department (not the Production

Department), would be responsible for the variance.

14-6 Direct labor rate (price) variances could be caused by: highly skilled (and paid)

labor used in place of lower-skilled labor; standard is out of date (e.g., new labor

contract); or, overtime work that is included in direct labor cost (rather than

manufacturing overhead). In some cases, the Production Manager is in the best

14-2

Education.

Chapter 14 – Operational Performance Measurement: Sales, Direct-Cost Variances, and the Role of Nonfinancial

Performance Measures

Direct labor efficiency (usage) variances could be caused by: using a different

mix of labor for the task at hand, as compared to the standard mix of labor;

poorly supervised employees; installation of new equipment; machinery and

equipment not maintained according to schedule (which could cause excess

waste and labor-hour consumption); inappropriate labor-hour standard (e.g., the

materials caused excess labor-hour consumption.

One particularly interesting situation that students should be aware of is the

potential for overemphasizing labor efficiency variances when labor is essentially

a short-term fixed cost. In this case, the labor efficiency variance can be largely

attributable to lack of orders (i.e., lack of sales demand), not worker efficiency.

For this reason, some writers suggest that when labor is essentially a short-term

fixed cost, that the labor efficiency variance not be reported for motivation and

control purposes. Otherwise, workers (and managers) may be motivated to

produce excess inventory which in turn would run counter to the JIT philosophy

that the firm may be embracing.

14-7 The answer depends on how overtime premium is treated by the accounting

prospects of the firm. In short, the labels “favorable” and “unfavorable” are

defined solely on the basis of the impact of the variance (positive or negative) on

short-term operating profit. It is a value judgment as to whether such variances

are positive or negative.

14-8 Of the three, for motivation and control purposes, standards based on the

average of recent historical performance are the least desirable. Many firms

prefer to use standards based on attainable performance in their standard cost

14-3

Chapter 14 – Operational Performance Measurement: Sales, Direct-Cost Variances, and the Role of Nonfinancial

Performance Measures

14-9 Establishing a standard cost system and identifying variances from the standard

are steps in gaining a better understanding of the operations and improving

operations. The focus of a standard cost system should be on influencing

standard cost system.

14-10 Organizations engage in a variety of processes in order to deliver the stated

value proposition to its targeted customers and in order to achieve its stated

financial objectives. These processes, for expository purposes, might be grouped

into the following: (a) operating processes, (b) customer-management processes,

14-11 A JIT system is very different from a conventional manufacturing system. In a JIT

system, a good or service is produced or delivered only when a customer

requires it. Some describe this as “demand pull” rather than “push.”

JIT production requires a product layout with a continuous flow once

production starts. Underlying the JIT system is a continuous improvement

philosophy of eliminating or reducing delay, error, and waste, such as materials

movement, storage, rework, and waiting time are part of the conventional work

environment.

Financial benefits resulting from a shift to cellular manufacturing, just-in-time

production, or continuous quality improvements may include the following:

14-4

Chapter 14 – Operational Performance Measurement: Sales, Direct-Cost Variances, and the Role of Nonfinancial

Performance Measures

reduction in work-in-process inventory levels.

3. Reduced material waste because of reduced damage caused by materials

The adoption of a JIT philosophy affects the organization’s management

accounting and control system in two primary ways:

1. To support the move to JIT, the accounting system needs to monitor

14-12 We might define total customer response time as the amount of time between

the time a customer places an order and the time when that order is received by

the customer. Manufacturing (production) cycle time can be defined as the

assessing process efficiency, based on the relationship between actual

processing time and total production time. In formula form, we can define PCE

as:

viewed, from the perspective of the customer. That is, would the customer be

willing to pay for the indicated activities/time? Does the activity add value in the

eyes of the customer?

14-5

Education.

Chapter 14 – Operational Performance Measurement: Sales, Direct-Cost Variances, and the Role of Nonfinancial

Performance Measures

BRIEF EXERCISES

14-13 Total static (master) budget variance = actual operating income static (master)

budget operating income

14-14 Total static (master) budget variance in operating profit = actual operating profit

static (master) budget operating profit

Sales volume variance in operating income = flexible-budget operating income

master budget operating income

Flexible-budget variance = actual operating income flexible-budget operating

income

14-15 Budgeted (Pro-forma) Operating Profit = (cm/unit × #units) FC

14-16 Sales price variance = actual sales volume × (actual budgeted) selling price/unit

= AQ × (AP SP)

14-17 Sales volume variance = budgeted cm/unit × (actual sales volume − master budget

sales volume)

14-6

Education.

Chapter 14 – Operational Performance Measurement: Sales, Direct-Cost Variances, and the Role of Nonfinancial

Performance Measures

14-18 Direct materials usage (quantity) variance for PVC = Standard price/lb. × (actual lbs.

used – standard quantity of lbs. that should have been used, given the actual

output for the period)

= SP × (AQ − SQ)

14-19 Purchase-price variance for PVC = actual pounds purchased × (actual – standard)

price/lb.

= AQ × (AP SP)

14-20 Flexible-budget variance for PVC = actual PVC cost for units produced – FB cost

= (actual price/lb. × actual lbs. used) – (actual output × standard #lbs./unit of

output × standard price/lb.)

14-21 Direct labor efficiency variance = standard wage rate/hr. × (actual – standard) direct

labor hours= SP × (AQ SQ)

14-22 Direct labor rate (price) variance = actual hours worked × (actual – standard) wage

rate/hr.

= AQ × (AP SP)

14-7

Education.

EXERCISES

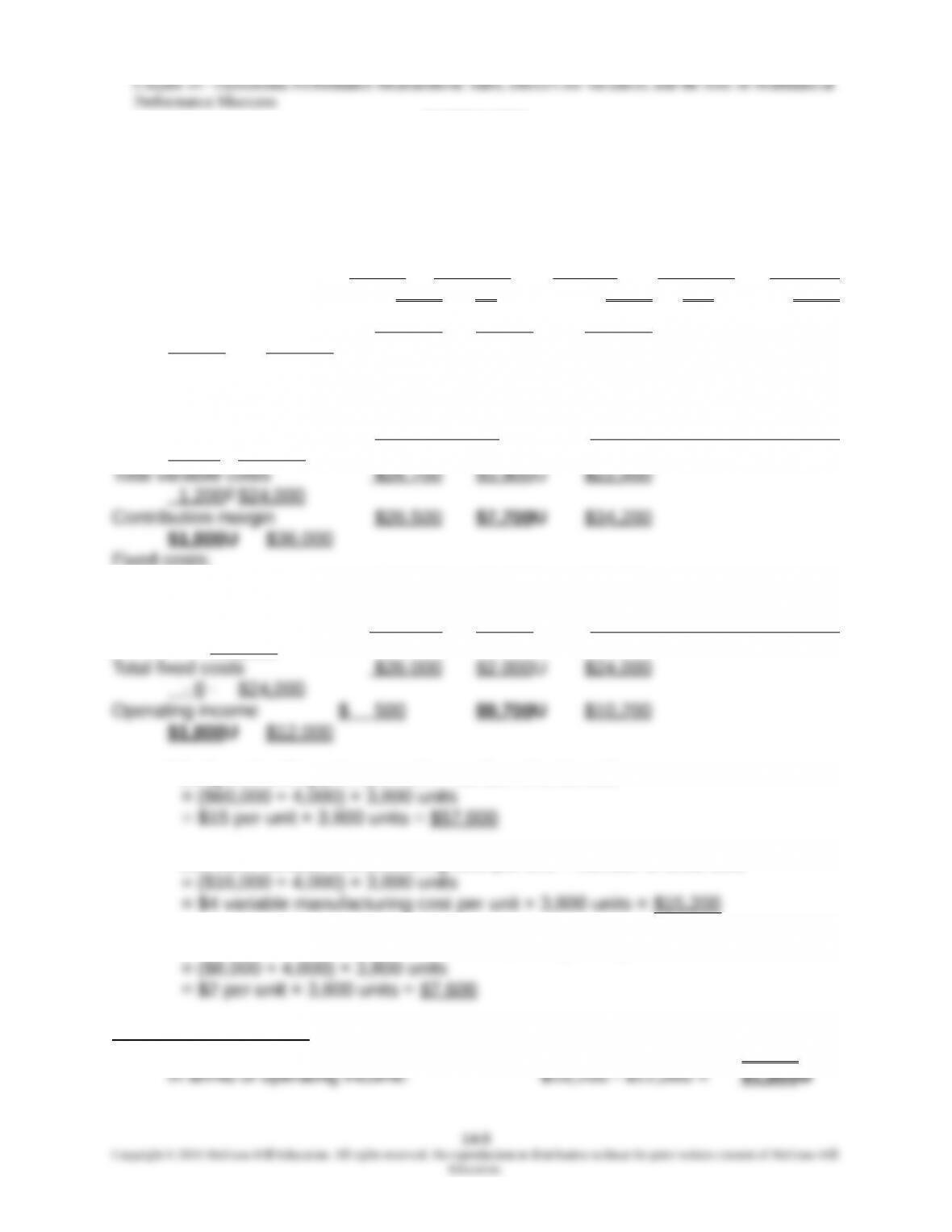

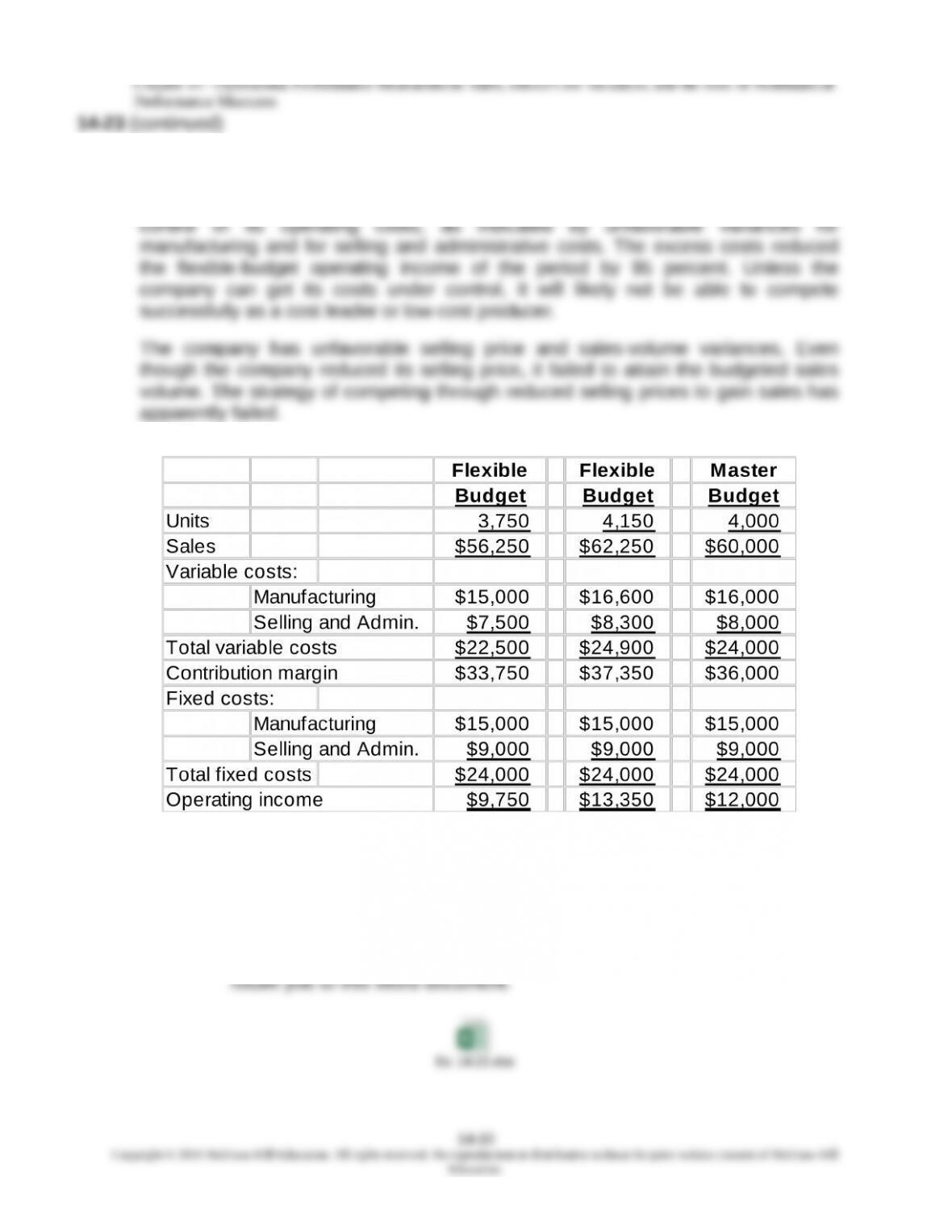

14-23 Flexible Budgets and Operating Income Variance Analysis; Spreadsheet

Application (50 minutes)

1. Flexible- Sales

Budget Flexible Volume Master

Actual Variance Budget Variance Budget

Units 3 ,800 – 0 – 3 ,800 200U 4 ,000

Sales $53 ,200 $3 ,800 U $57 ,000

1$3,000U $60,000

Variable costs:

Manufacturing $19,000 $3,800U $15,200

2$800F $16,000

Selling & Admin. 7 ,700 100U 7 ,600

3 400F 8,000

Fixed costs:

Manufacturing $16,000 $1,000U $15,000

$15,000

Selling & Admin. 10 ,000 1 ,000 U 9 ,000

9,000

1 Budgeted selling price per unit × number of units sold

2 Standard variable manufacturing cost per unit × number of units sold

3 Standard variable selling and administrative expense per unit × number of units

Sales volume variances

In terms of contribution margin: $34,200 $36,000 = $1,800U

Flexible-budget variances

Contribution margin: $26,500 $34,200 = $7,700U

Operating income: $500 $10,200 = $9,700U

14-9

Education.

2. The company reduced its selling price (from $15 per unit to $14 per unit) to compete

in the market, suggesting the pursuit of a cost-leadership, not a differentiation,

competitive strategy for the product. However, the company failed to exercise proper

3.

Note: An Excel spreadsheet solution file is embedded below. You can open this

“object” by doing the following:

1. Right click anywhere in the worksheet area below.

2. Select “worksheet object” and then select “Open.”

3. To return to the Word document, select “File” and then “Close and return

to…” while you are in the spreadsheet mode. The screen should then