Chapter 10 – Strategy and the Master Budget

CHAPTER 10: STRATEGY AND THE MASTER BUDGET

QUESTIONS

10-1 Compel strategic planning and facilitate implementation of strategic plans. An

organization’s strategy, strategic plans, and budgets are interrelated. Preparing

budgets compels reviews of an organization’s strategy and its strategic plans and

can facilitate implementations of the strategic plan. Feedback from budgets often

results in improvements to an organization’s strategy and strategic plan.

and may not be suitable to serve as a benchmark. To the extent past performance

was not effective/efficient it does not make sense to use this as the standard

against which actual performance is compared.

Promote coordination and communication within the organization. Budgets compel

managers to think of interdependencies and interrelationships among subunits of

10-2 A master budget is a comprehensive plan of action for a future period; as such, the

master budget includes both operating and financial budgets. An operating budget

consists of plans regarding revenues and resource acquisition/use across all major

operating areas of the organization (e.g., sales, production, purchasing, marketing,

10-3 Many organizations are “run by the numbers.” In these organizations managers are

held accountable for financial results and therefore need to be “data literate” as

10-1

Education.

Chapter 10 – Strategy and the Master Budget

10-4 Some would argue that the primary purpose of budgets is for planning and that

problems are created when budgets are used for control and incentive-

compensation purposes. The latter use of budgets is thought to engender both

unethical practices (e.g., ENRON, WorldCom) or, more prevalently, gaming

behavior. For example people whose performance will be compared to the budget

targets may understate their potential in order to have achievable targets set.

performance and to meet budget projections.

10-5 The sales budget is often regarded as the cornerstone in the master budget

because all operating activities in a business emanate from efforts to attain the

level of sales specified in the sales budget. A firm can complete the plan for other

activities of a period only after it knows the expected sales levels for the current

and the immediate future periods. A manufacturing firm, for example, cannot

complete its production schedule for the upcoming period without knowing the

10-6 Additional factors include:

Beginning and desired ending inventories of work-in-process (WIP) and

finished goods

10-7 A cash budget that is prepared according to the statement of cash flows required

for external reporting purposes generally includes five components:

Beginning-of-period cash balance

Net cash flow from operations

10-2

Education.

Chapter 10 – Strategy and the Master Budget

10-8 Zero-base budgeting (ZBB) is a budgeting process that requires managers to

prepare budgets each period from ground zero for all operations.

A typical budgeting process is “incremental” in nature. That is, budgets for the

upcoming period start from the approved budgets for the current period, with

amounts added to reflect planned changes for the upcoming period. Thus,

traditional budgets assume that most, if not all, of the current activities and

A number of companies (e.g., Xerox, Texas Instruments) and government

organizations (e.g., State of Georgia) have at one time or another used ZBB.

10-9 Budgetary slack, or “padding” the budget, is the practice of knowingly including a

higher amount of expenditure in the budget (or lower amount of revenue) than

managers actually believe should be the case. One reason that it is common to

find slacks in budgets is the desire of managers to use such slack as a cushion for

the amount of resources they feel they actually need.

10-10 A time-driven activity-based cost (TDABC) system, as explained in Chapter 5, is a

refinement and simplification of a traditional ABC system. Rather than identifying

activities and associated activity costs, a TDABC system calculates a cost rate for

each major activity, process, or department using only pieces of information: (1)

Advocates of TDABC believe that this system both reduces the cost of

implementing an ABC system and improves the accuracy of the resulting activity-

cost data. Resulting activity-cost data from a TDABC system can be used, as is

10-3

Education.

Chapter 10 – Strategy and the Master Budget

10-11 A fixed-performance contract refers to the performance associated with the results

reflected in the master (static) budget that is prepared at the beginning of the year.

This amount is “fixed” in the sense that the amount is negotiated prior to the

beginning of the budget period and not adjusted afterwards. For incentive-

10-12 A fixed-performance contract implies a fixed (static) target, usually negotiated

prior to the start of the budget period. Incentive compensation (i.e., managerial

reward) is contingent on whether, or the extent to which, this fixed target is

achieved during the period. In typical fixed-performance contracts there are

minimum and maximum rewards. Thus, the performance-reward contract is

discontinuous.

By contrast, an organization can employ a “linear performance contract.” Quite

literally, this implies a zero compensation if performance (e.g., operating income)

is zero (or negative). It also implies unlimited compensation for extraordinary

10-13 The term “relative performance contract” means that the basis against which

actual managerial performance is compared is either an internal or an external

benchmark, rather than budgeted performance embodied in the annual (fixed or

The use of both “relative performance contracts” and “rolling financial forecasts”

are key recommendations set forth by the Beyond Budgeting Roundtable

(www.bbrt.org). Also, see Jeremy Hope and Robin Fraser, Beyond Budgeting:

How Managers Can Break Free from the Annual Performance Trap. Boston, MA:

Chapter 10 – Strategy and the Master Budget

“Who Needs Budgets?” HBR OnPoint Product Number 306X. Boston, MA:

Harvard Business School Publishing Corporation, 2003.

10-5

Education.

Chapter 10 – Strategy and the Master Budget

BRIEF EXERCISES

10-14

Q2 Q3

Sales—2016 16,000 15,000

Plus projected 25% increase for 2017 4,000 3,750

10-15 Payment history:

% paid in month of purchase: 25%

% paid in month following month of purchase: 75%

Expected Cash Disbursements:

10-16 Number of units produced in Qtr. 1:

Ending inventory of direct materials (DM) = 50,000 lbs.

Target ending inventory % = 25% of following month’s production

requirements

Therefore, DM used for production in Qtr. 1 = 50,000 ÷ 0.25 = 200,000 lbs.

Units produced in Qtr. 1 = lbs. of DM used/lbs. of DM per unit of

output = 200,000 ÷ 8 = 25,000 units

10-17 Scheduled Production, Quarter 2:

Units required to meet estimated sales, Qtr. 2 = 12,000 units

Units required to meet targeted ending inventory:

15,000 units × 10% = 1,500 units

10-18 Current level of monthly operating costs = $10,000:

10-6

Education.

Chapter 10 – Strategy and the Master Budget

10-19 Collection of Credit Sales—November 2016:

30% of Credit Sales made in October = 0.30 × $30,000 = $9,000

70% of Credit Sales made in November = 0.70 × $24,000 = $16,800

Collection of Credit Sales—December 2016:

10-20 Collection of Credit Sales—December:

From credit sales made in November = 0.20 × $90,000 = $18,000

From credit sales made in December:

10-21 Estimated interest expense—April = borrowing in April × (annual rate ÷ 12)

= [($30,000 − $18,000) + $1,000] × (0.12 ÷ 12)

Note that, strictly speaking, to maintain a minimum cash balance of $30,000, the

company would have to borrow an extra $1,000 to be able to cover the interest

payment (eom) and still have at least $30,000 of cash.

Estimated financing transactions—May:

Interest expense (paid eom): $13,000 × 0.01 = $130

Principal repayment:

Beginning-of-month cash balance

= $18,000 + ($13,000 − $130) = $30,870

Plus: net cash flow in May, prior to financing = $22 ,000

Cash balance prior to financing transactions = $52,870

10-22 Direct Material (DM) Purchases, December = (DM issued to production +

ending DM inventory) – beginning DM inventory

10-7

Education.

Chapter 10 – Strategy and the Master Budget

10-23 Total budgeted marketing expenses, 4th quarter:

Sales volume (units):

3rd Quarter (actual) = 4,000

Estimated 4th-Qtr. Increase = 10%

Variable marketing expenses, per unit sold = $0.05

Fixed marketing expenses, per MONTH:

Salaries (cash) = $10,000

Depreciation–delivery trucks = $5,000

Insurance (paid monthly) = $2,000

Total budgeted marketing expense and cash payments, 4th quarter:

Variable costs ($0.05 × [4,000 units × 1.10]) = $220

Fixed costs:

Salaries = (3 × $10,000) = $30,000

Depreciation = (3 × $5,000) = $15,000

10-8

Education.

Chapter 10 – Strategy and the Master Budget

EXERCISES

10-24 Purchase Discounts (25 minutes)

The financial cost of not taking advantage of the early-payment discount for

purchases made on credit can be approximated by the following formula (we use

the term “approximate” here to denote the fact that the estimate below does not

assume compounding of interest and as such provides a conservative estimate):

Opportunity cost (%) = [discount % ÷ (1 − discount %)] × [365 ÷ no. of

extra days allowed if discount is not taken]

1. In the case of 2/10, n/30, the approximate economic cost of not taking

advantage of the early-payment discount is:

= [0.02 ÷ (1 − 0.02)] × [365 ÷ 20] = 0.020408 × 18.25 = 37.24%

Basically, if you choose not to take the early-payment discount, you are giving

up a 2% discount (on the net amount) in return for an extra 20 days in which

of the net bill (the bill without financing cost).

2. In the case of 1/10, n/30, the opportunity cost of not taking advantage of the

early-payment cash discount is:

3. Given the significant opportunity cost of not taking advantage of early-

payment cash discounts, good accounting practice would be to record

10-9

Education.

Chapter 10 – Strategy and the Master Budget

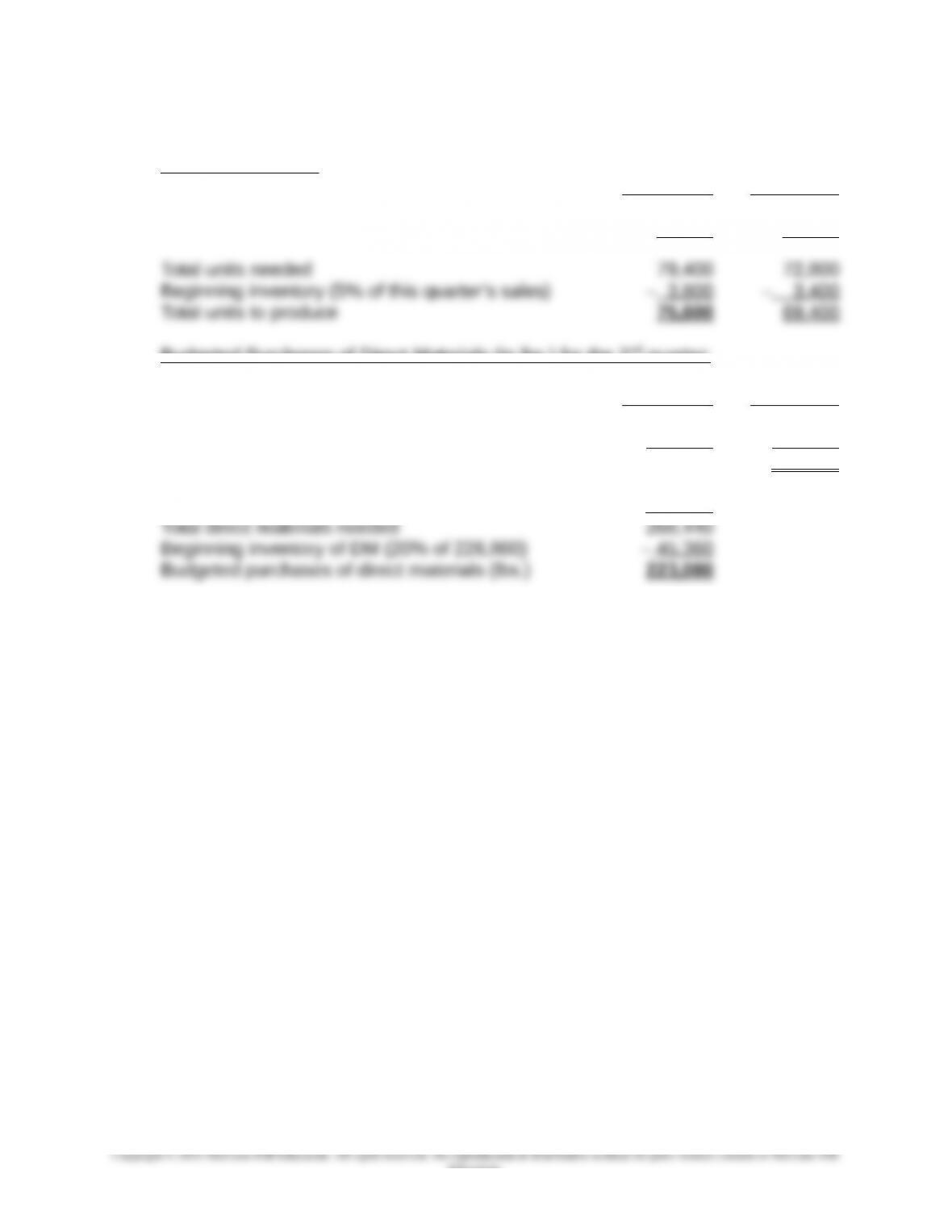

10-25 Production and Materials Purchases Budgets (20-25 minutes)

Production Budget:

2 nd

Quarter 3 rd

Quarter

Budgeted sales 76,000 68,000

Desired ending inventory (5% of next quarter’s sales) + 3,400 + 4,800

Budgeted Purchases of Direct Materials (in lbs.) for the 2 nd

quarter:

2 nd

Quarter 3 rd

Quarter

Budgeted production 75,600 69,400

Direct materials (lbs.) per unit produced × 3 × 3

Direct materials needed in production 226,800 208,200

Desired ending inventory of direct materials (lbs.)

(20% of 208,200 lbs.) + 41,640

10-10

Education.