Chapter 5 – Activity-Based Costing and Customer Profitability Analysis

5-31 Applications of ABC Costing in Government (20 min)

1,2.

Some of the examples are noted in the text, including the U.S. Postal Service,

the U.S. Patent Office, and the U.S. Army. Others include the U.S. Coast

Guard, the US. National Security Agency (ABC used to better understand the

cost of its mission support services), the U.S. Mint (pressure from top

management to better understand the organization’s cost structure and cost

behavior), and the U.S. National Institute of Health (ABC is used to determine

more accurately the cost of providing its services including building and space

acquisition, property management, and research program support).

A variety of examples are possible here. For additional examples: Gary

Cokins, Activity-Based Cost Management in Government, Management

Concepts, Inc., 2001. Also, see case studies of governmental agencies in

Cost & Effect, by Robert S. Kaplan and Robin Cooper, Harvard Business

School Press, 1998, pp 245-250. Kaplan and Cooper explain application at

the U.S. Veterans Affairs Department, the U.S. Immigration and Naturalization

Service, theU.S. Internal Revenue Service, and the City of Indianapolis.

5-11

Chapter 5 – Activity-Based Costing and Customer Profitability Analysis

5-32 Product-line Profitability, ABC (25 min)

1. Product-line profitability under the current costing system

Frozen Food Baked Goods Fresh Produce

Sales $120,000 $91,000 $158,175

Cost of goods sold 105,000 67,000 110,000

Gross margin $ 15,000 $24,000 $ 48,175

2. Product-line profitability under ABC

Frozen Food Baked Goods Fresh Produce

Sales $120,000 $91,000 $158,175

Cost of goods sold 105,000 67,000 110,000

Gross margin $ 15,000 $24,000 $ 48,175

Store support:

Order processing 800 $3,600 $8,000

Receiving 1,320 6,050 13,200

3. Both baked goods and fresh produces drop in profitability when ABC is

used. The decrease in profitability of fresh produce is most noticeable. The

profitability of fresh produce decreases from 10.46 percent of the sales

5-12

Chapter 5 – Activity-Based Costing and Customer Profitability Analysis

5.32 (coninued)

4. The rates come from dividing the total dollar amount in a cost pool by the

activity driver quantity for each cost pool. The issue that management

faces is deciding whether to use the expected consumption quantity of the

activity driver or the practical capacity level of the activity driver,

regardless of consumption. It is not clear from the information provided

whether management used the expected consumption rates or practical

used one of the two following formulas:

Cost of order processing ÷ 155

Or

Cost of order processing ÷ practical capacity

Since practical capacity will be greater than or equal to expected

consumption, the driver rate would be lowest when using practical

capacity. Also, the rates would vary as expected consumption changed,

but practical capacity is likely to remain fairly stable, making the driver

rates more stable.

5-13

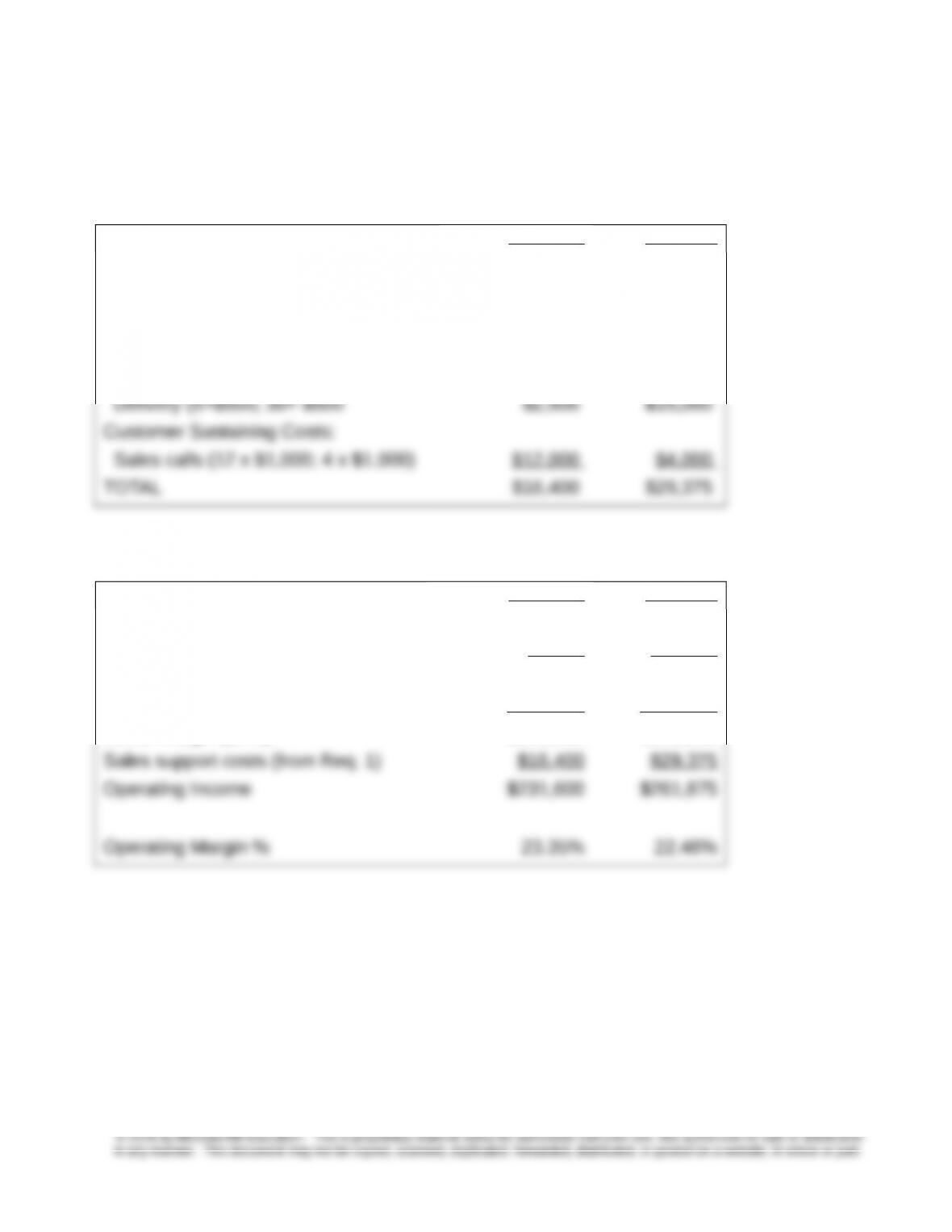

5-33 Product Line Profitability Analysis

1.2.,

Paint & Paint

Supplies Carpet

Other Flooring

Products

Sales $295,000 $214,900 $167,900

Cost of goods sold $165,000 $150,000 $135,250

Gross Margin $130,000 $64,900 $32,650

Store Support (24% of revenue) $70,800 $51,576 $40,296

Operating Income $59,200 $13,324 ($7,646)

Operating Margin 20.07% 6.20% -4.55%

Product line profitability under ABC.

Paint & Paint

Supplies Carpet

Other Flooring

Products

Sales $295,000 $214,900 $167,900

Cost of goods sold $165,000 $150,000 $135,250

Gross Margin $130,000 $64,900 $32,650

Store Support:

Order Processing $59,500 $21,000 $14,000

Note: for example, Paint&Supplies order processing ABC cost = $59,500 = $140 × 425; similarly

for other activities

3. Paint & Paint supplies have little change in operating profit. Carpet and

Other Flooring Products, however, have significant changes. This is

important because it indicates that the current costing system does not

provide an accurate reflection of store support. It is also interesting that the

Other Flooring Products are more profitable than Carpet under the ABC

buying carpet, management might consider charging more for carpeting.

5-34 Customer Profitability Analysis: Luxury Hotel Industry (15 min)

1. The information-gathering programs are a logical fit for the luxury type

hotels described here. These firms compete on their ability to attract high-

5-14

Chapter 5 – Activity-Based Costing and Customer Profitability Analysis

paying customers to their luxury hotels. These additional services can give

the hotel a competitive edge. It is much more common now to see hotels with

loyalty programs, where membership in the program triggers room upgrades,

free coffee, and other benefits. Hilton and Hyatt are among those that have

these programs; they are called Hilton HHonors, and Hyatt Gold Passport,

respectively.

2. There is a good application for activity-based costing here. The program

should be analyzed by activity (the different types of premium services

offered), and then the cost drivers of these activities should then be identified,

and traced to the cost object, which in this case is the individual customer. It

3. Some will argue there is no ethical issue with the information gathering.

Others might argue that the guest should be informed that the information is

being obtained and used throughout the hotel chain’s system. For example,

Marriott has guests fill out a form to participate, so the program is entirely

optional. Other ethical issues arise, for example, if the hotel chain chooses to

5-15

Chapter 5 – Activity-Based Costing and Customer Profitability Analysis

5-35 Customer Profitability Analysis (25 minutes)

1.

Jerry Inc. Kate Co.

Customer Unit Level Costs:

Sales return(40×$5;175×$5) $200 $875

Customer Batch Level Costs:

Order processing (5×$300; 30×$300) $1,500 $9,000

Sales return (2×$100; 5×$100) $200 $500

2.

Jerry Inc. Kate Co.

Sales $1,000,000 $1,200,000

Sales Return (40×$200; 175×$200) $8,000 $35,000

Net Sales $992,000 $1,165,000

Cost of goods sold $744,000 $873,750

Gross margin (25%) $248,000 $291,250

5-16

Chapter 5 – Activity-Based Costing and Customer Profitability Analysis

5-36 Customer Profitability Analysis (25 min)

1. Determinaion of the $100.50 order-illing cost per unit

Total number of orders:(2 × 100 PCs) + (10 × 4,000 SCs) = 40,200

Total number of orders 40,200

Number of orders per block 60

Total number of blocks 670

Cost per block × $60,000

Total cost of order blocks $ 40,200,000

Total number of orders 40,200

Per order order-filling cost × $1,500

2. Order illing cost per unit sold to PC:

Total number of orders 2

Number of orders per block 60

Total number of blocks 1/30

Cost per block × $60,000

Total block cost $2,000

Total number of orders 2

Order-filling cost per order × $1,500

Total cost per order + 3,000

5-17

Chapter 5 – Activity-Based Costing and Customer Profitability Analysis

5-36 (continued)

3. Order illing cost per order by SC:

Cost per block $60,000

Number of orders per block ÷ 60

Block cost per order $1,000

Number of orders per SC × 10

Total block cost per SC $10,000

Order-filling cost per order $1,500

Proitability per unit at $800 selling price per unit to SC

Selling price per unit $800.00

Manufacturing cost $600.00

5-18

Preferred Customer

Selling price per unit $700.00

Manufacturing cost $600.00

Order-filling cost/unit + 1.00

Total cost per unit 601.00

Net Profit per unit $ 99.00

Profit margin per unit 14.14%

Chapter 5 – Activity-Based Costing and Customer Profitability Analysis

5-37 Tools for Successful ABC/M Implementation (10 min)

Other guides or tip for successful implementation are noted in the text, but

some are listed below:

Choose a type of context where ABC is likely to succeed, such as a

situation where there is product variety and operating complexity, so that

the ABC analysis provides significantly useful information

Keep the initial design system; use a simple prototype and build the

system gradually

Additional Sources: Dan Swenson and Douglas Barney, “ABC/M: Which

Companies Have Success?” The Journal of Corporate Accounting & Finance,

March/April 2001, pp 35-44. See also, Douglas T. Hicks, “Good Decisions

Require Good Models: Developing Activity-Based Solutions that Work for

Decision Makers,” Cost Management, March/April 2005, pp 32-40, and

Michael D. Shields and Michael A. McEwen, “Implementing Activity-Based

Costing Systems Successfully,” Cost Management, Winter, 1996, pp15-22.

5-19

Chapter 5 – Activity-Based Costing and Customer Profitability Analysis

PROBLEMS

5-38 Activity-Based Costing, Value Chain Analysis (25 min)

1. Manufacturing cost (total, and per unit):

Prime manufacturing cost (80 ×$1,300) = $104,000

Manufacturing overhead:

Materials handling (80 × 100 × $0.60) = $4,800

Machining (80 × 3 × $51.00) = $12,240

Assembly (80 × 100 × $2.85) = $22,800

Manufacturing cost per unit = $1,828.00

2. Computation of full cost:

Upstream activity costs = $180.00 7.80%

Manufacturing costs = $1,828.00 79.20%

Strategic implications:

(1) Knowing the full cost of a product including upstream and

downstream costs allows the firm to be aware of all costs attributable

to the product.

(2) The amounts and proportions of upstream, manufacturing, and

downstream costs facilitate comparisons with competitors.

(3) The company should consider ways of spending less cost in the

manufacturing activity, and more on upstream and downstream

5-20