Chapter 18 – Strategic Performance Measurement: Cost Centers, Profit Centers, and the Balanced Scorecard

18-40 Financial Incentives and Auto Repair/Inspection Companies (20

min)

The findings of the research suggest that in fact the financial incentives of

the auto repair shop are to pass vehicles that fail the emissions test

because many of the owners of these vehicles are regular customers. The

auto repair shop wants to retain these customers for the more lucrative

work of replacing tires, batteries, and performing repair work. The loss of

a customer due to a failed test could be very costly to the repair shop in the

long term.

The financial incentives needed to ensure compliance with the inspection

standards require independence between the shop owner and the vehicle

owner. Independent inspection stations that only perform inspections

would be one answer to the problem, but this solution could be a very

reducing or eliminating state sales tax on this type of work, by using state

income tax credits or partial reimbursements as financial incentives for the

motorist to perform the needed emissions-related work. The key issue is to

provide the financial incentives for the auto owner to keep their vehicles

emission-compliant.

The ethical issues arise clearly in this case as the shop owner and the

vehicle owner have financial incentives not to follow the state’s regulations

regarding emission controls.

The sustainability issue is also clear. The failure to perform proper

inspections could lead to a greater number of vehicles on the road with

emissions problems, increasing greenhouse gasses and reducing the

quality of the environment.

Reference: Pierce, L. and J. Snyder. (2008). “Ethical Spillovers in Firms:

Evidence from Vehicle Emissions Testing.” Management Science 54 (11):

pp 1891-1903.

Chapter 18 – Strategic Performance Measurement: Cost Centers, Profit Centers, and the Balanced Scorecard

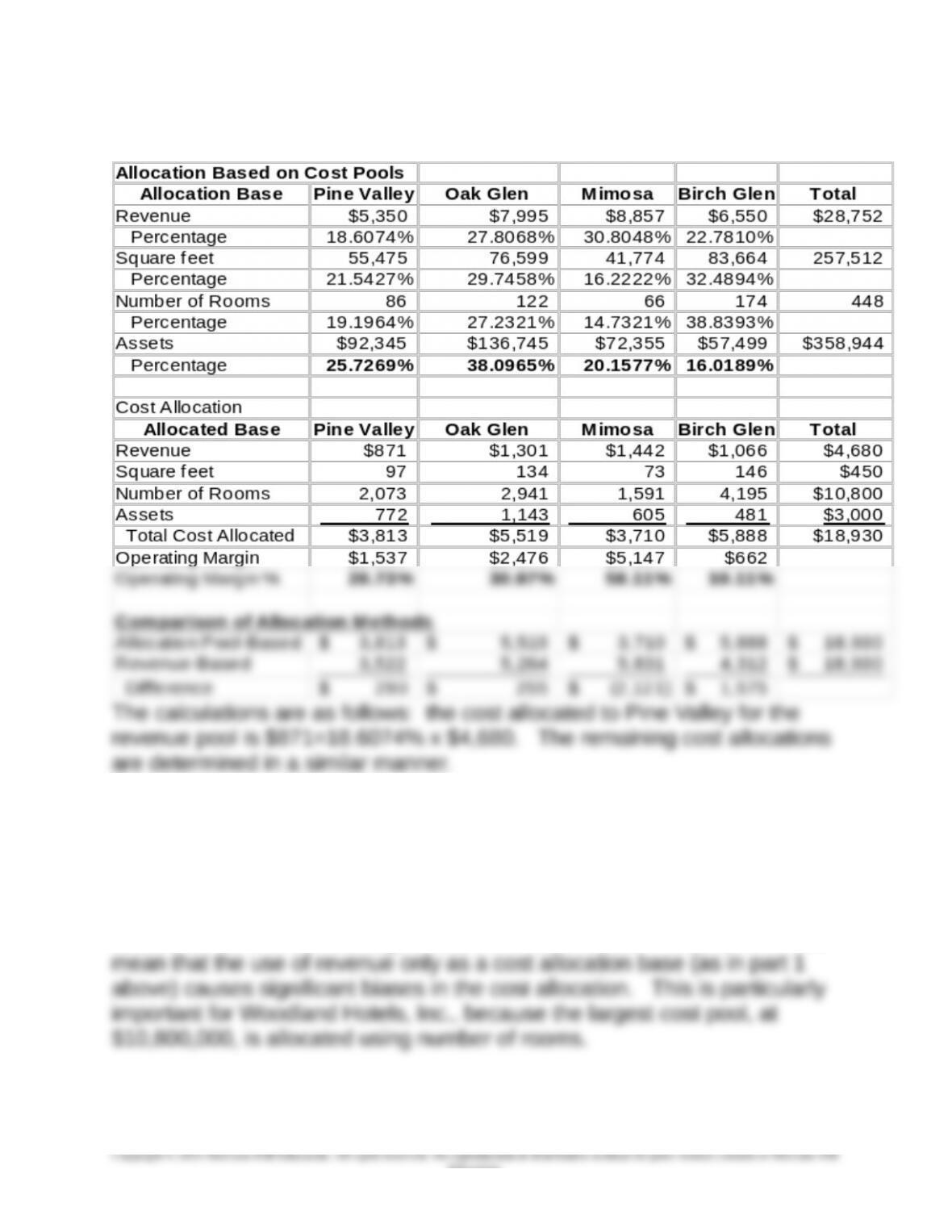

18-41 Allocation of Central Costs; Profit Centers (30 min)

1. Allocation based on revenue

related to revenue; for example, it is unlikely that interest or

administrative and executive salaries are closely related to revenue.

Also, the cost of front office personnel is likely to be related to same

measure of the number of customers of the resort. Perhaps the

number of rooms is a better measure of the usage of the cost of front

office personnel.

2. There are a number of possible answers. A useful starting point for

class discussion might be the following solution:

The four allocation bases are revenues, square feet, number of

rooms, and value of resort assets. The operating costs are assigned

18-32

Education.

Chapter 18 – Strategic Performance Measurement: Cost Centers, Profit Centers, and the Balanced Scorecard

18-41 (continued -1)

Square Feet: carpet cleaning, contract to repaint rooms; it could be

argued that these costs are driven by the size of the areas to be

cleaned and painted

Value of resort’s assets: interest on resort purchase; the reasoning

here is that the cost of the assets is what drives interest cost

Revenue cost pool: advertising, depreciation on reservations

computer system, administrative and executive salaries. These are

the office costs that cannot be traced to one of the above costs

drivers (square feet, number of rooms, assets), but using the ability to

3. Cost Allocation

This part can be compared to the application of ABC costing in

chapter 5; the goal is to allocate costs in a manner that most nearly

reflects the consumption of the costs.

The allocation using the multiple cost pools is preferred because it

allocates costs in a manner more closely related to the cause-effect

18-33

Education.

Chapter 18 – Strategic Performance Measurement: Cost Centers, Profit Centers, and the Balanced Scorecard

18-41 (continued -2)

The allocation rates for each of the four cost drivers are determined above.

Note the large differences between the rates for revenue and for the

number of rooms; relative to Oak Glen, Pine Valley is a smaller resort with

lower room rates, while Mimosa is also a smaller resort but with higher

rates, and Birch Glen is a larger resort with lower rates. These differences

18-34

Education.

Chapter 18 – Strategic Performance Measurement: Cost Centers, Profit Centers, and the Balanced Scorecard

18-41 (continued -3)

Based on the relationship between revenue and number of rooms,

the result is that Pine Valley and Oak Glen’s cost allocation and operating

margin are similar under the revenue-only and the multiple-driver

18-35

Education.

Chapter 18 – Strategic Performance Measurement: Cost Centers, Profit Centers, and the Balanced Scorecard

18-42 Product Cost Under Full versus Variable Costing (10 min)

1.

Under absorption costing both the fixed and variable production costs are

used to determine the cost of each unit produced. The number of units

sold (20,000) is irrelevant to the cost of production.

2.

18-43 Full Costing and Variable Costing Operating Income (15 min)

1.

Revenue = 50,000 × $ 4.00 = $200,000

2.

Revenue = 50,000 × $ 4.00 = $200,000

18-36

Chapter 18 – Strategic Performance Measurement: Cost Centers, Profit Centers, and the Balanced Scorecard

18-44 Profit Centers: Comparison of Variable and Full Costing (20

min)

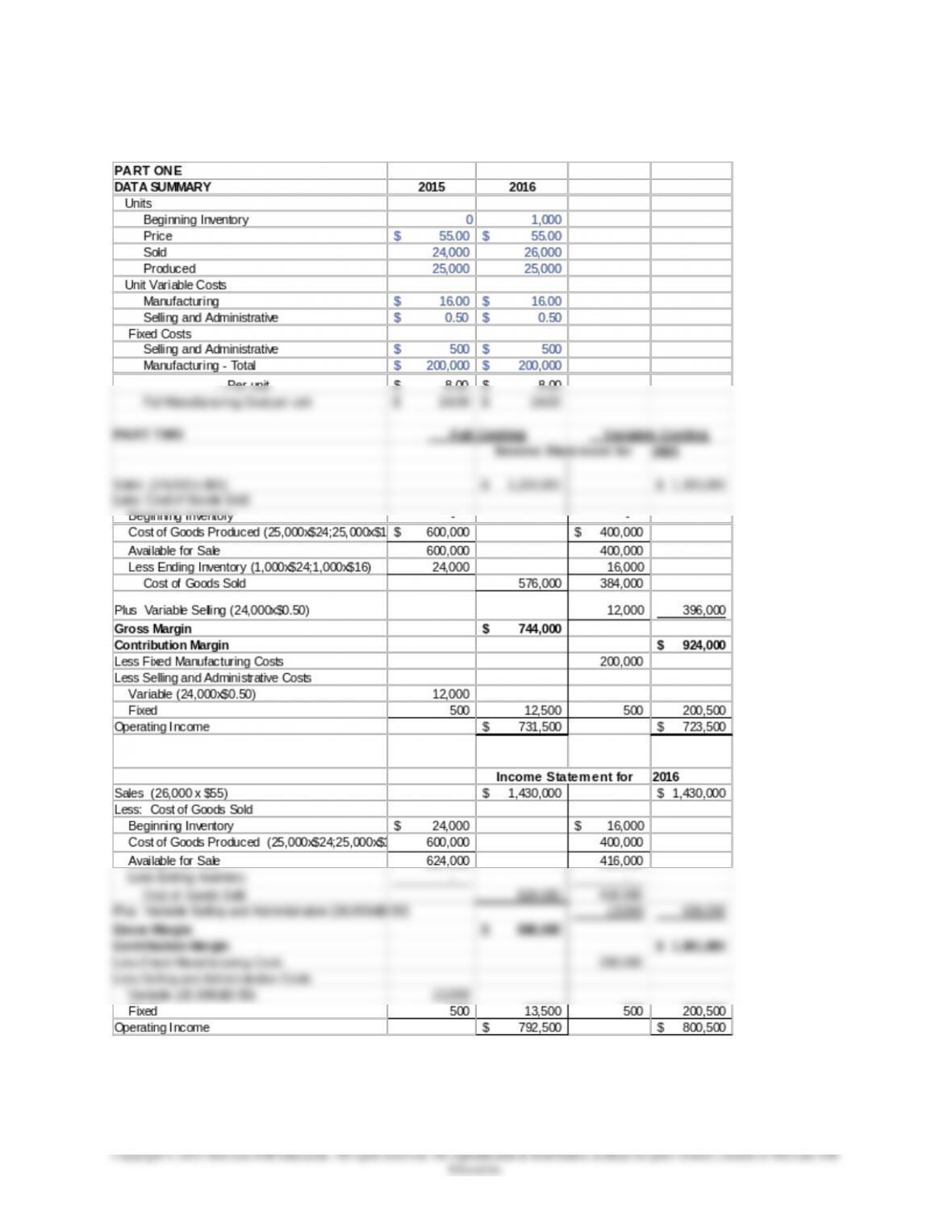

PART ONE

DATA SUMMARY Prior Year Current Year

Units

Beginning Inventory 0 200

Price $ 3.00 $ 3.00

Sold 1,800 2,200

Produced 2,000 2,000

Unit Variable Costs

Manufacturing $ 0.60 $ 0.60

Selling and Administrative $ 0.40 $ 0.40

PART TWO Full Costing Variable Costing

Income Statement for Prior Year

Sales (1,800 x $3) $ 5,400 $ 5,400

Less: Cost of Goods Sold

Beginning Inventory – –

Cost of Goods Produced (2,000 x $1.10; 2,000x$.6) $ 2,200 $ 1,200

Available for Sale 2,200 1,200

Less Ending Inventory (200x $1.10;200x$.6) 220 120

Cost of Goods Sold 1,980 1,080

Plus Variable Selling (1,800x$.40) 720 1,800

Income Statement for Current Year

Sales (2,200 x $3) $ 6,600 $ 6,600

Less: Cost of Goods Sold

Beginning Inventory $ 220 $ 120

Cost of Goods Produced (2,000 x $1.10; 2,000x$.6) 2,200 1,200

Available for Sale 2,420 1,320

Less Ending Inventory – –

Cost of Goods Sold 2,420 1,320

Plus Variable Selling and Administrative (2,200x$.40) 880 2,200

18-37

Education.

Chapter 18 – Strategic Performance Measurement: Cost Centers, Profit Centers, and the Balanced Scorecard

18-38

Education.

Chapter 18 – Strategic Performance Measurement: Cost Centers, Profit Centers, and the Balanced Scorecard

18-44 (continued -1)

PART THREE

Reconciling Difference in Operating Income between Full

and Variable Costing

Prior Year Current Year

Change in Inventory in Units 200 (200)

Multiply times Fixed Overhead Rate $ 0.50 $ 0.50

An increase in inventory units means full costing operating income is higher

than variable costing operating income.

A decrease in inventory units means variable costing operating income is

18-39

Education.

Chapter 18 – Strategic Performance Measurement: Cost Centers, Profit Centers, and the Balanced Scorecard

18-45 Full versus Variable Costing (25 min)

1.

18-40