Chapter 17 – The Management and Control of Quality

17-74 (Continued-2)

3. The report indicates that prevention, appraisal, and internal failure costs have

increased from 2016 to 2017. The external failure cost category decreased by

2017.

Lee Enterprises benefits from decreases in its external failure costs. Three external

failure costs (product recalls, warranty repairs, and warranty replacements) have

decreased by approximately 70 percent from what these costs were the year before.

4. One of the most effective ways for production workers to be conscientious in their

work is to hold them responsible for mistakes. Holding employees responsible for

their work can include a policy for workers to do rework on their own time and to pay

Note: Two linked Excel spreadsheet solution files for this Problem are embedded

below. You can open each spreadsheet “object” by doing the following:

1. Right click anywhere in the worksheet area.

2. Select “worksheet object” and then select “Open.”

3. To return to the Word document, select “File” and then “Close and return to...”

while you are in the spreadsheet mode. The screen should return you to this

Word document.

17-82

Education.

Pr. 17-74(b) 7e.xlsx

Pr. 17-74(a) 7e.xlsx

Chapter 17 – The Management and Control of Quality

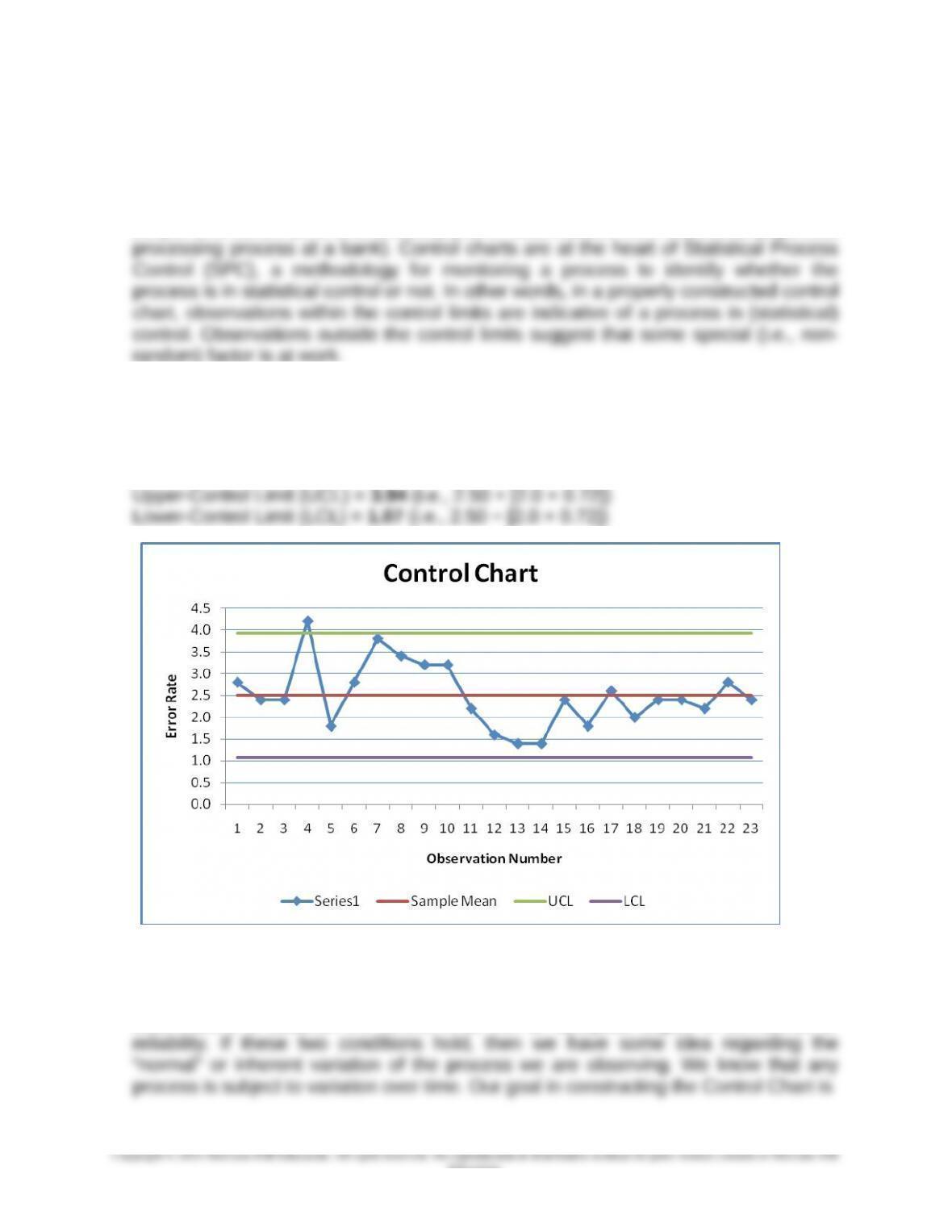

17-75 Constructing and Interpreting a Control Chart (50 Minutes)

1. A “control chart” might best be thought of as a time-series run chart with statistically

determined upper and lower control limits, around a target value (usually defined as

the mean value of the characteristic under examination). By contrast, a run chart is a

simple time-series (i.e., time-ordered) plot of observations from a process (e.g., loan

2. Construction of Control Chart:

Sample mean of process = 2.50

Sample standard deviation = 0.72

No. of standard deviations = 2

3. Interpretation of control limits: we assume that the sample observations were

obtained during the time that the underlying process (in this case, processing of loan

applications) is in control, that is, is stable. We also assume that we have sufficient

observations to establish the control limits with an adequate degree of confidence or

17-83

Education.

Chapter 17 – The Management and Control of Quality

17-75 (Continued)

to develop a tool that will provide an indication of when, going forward, the process is

likely in or out of statistical control. Because we are working with some uncertainty,

we realize that we can make one of two errors in interpreting the control chart results:

we might conclude that the process is out of control when in fact (unbeknownst to us)

it is in control; or, we might conclude that everything is fine, when in fact the variation

4. As indicated above in (3), the basic approach to judging process control is statistical

in nature. That is, on the basis of whether or not actual observations fall within the

control limits we draw a conclusion as to whether the process is in control (i.e., the

variations we are observing have random, or non-systematic, causes) or out-of-

control. This approach is sometimes referred to as the “outlier” approach to

interpreting results from a Control Chart.

Another approach would be to look for what appear to be an abnormal number of

runs. The likelihood of a stable process generating, say, eight points in a row on the

same side of the centerline is like tossing a coin and getting “tails” eight times in a

variation.

5. Some plausible quality measures for non-manufacturing companies:

a) Hospitals—lab test accuracy, insurance claim accuracy, on-time delivery of meals

and medications

b) Insurance Company—claims-processing response time, billing accuracy

17-84

Education.

Chapter 17 – The Management and Control of Quality

17-76 Research: Applying Lean Principles to “Knowledge Work” (60 minutes,

including reading time)

1. The term “lean,” as derived from the Toyota Production System, can be taken to

mean “relentless attention to detail, commitment to data-driven experimentation, and

charging employees with the ongoing task of increasing efficiency and eliminating waste

2. The term “knowledge work” is used by the authors of this article to mean any decision

process (or operation) that involves judgment and expertise (so-called “tacit

knowledge”—that is, knowledge “locked inside the worker’s head). Unlike many

manufacturing contexts (in which work processes can more or less be defined

unambiguously and therefore modeled), conventional wisdom holds that “knowledge-

3. Perhaps the most significant assertion is stated at the very end of the article (p. 110):

turning a knowledge operation into a lean system is difficult, but possible; this very

difficulty implies that the system will be hard for competitors to replicate. In other words,

making a knowledge-based operation “lean” can allow the organization to improve

faster than competitors and therefore be a source of competitive advantage for the

organization.

4. The authors believe (based on their experience of over 1,800 projects at Wipro

Technologies) that knowledge work can be made lean if organizations draw on six

principles, summarized as follows:

Continually Root Out/Eliminate Waste

The authors assert that even in knowledge work, there are routine activities that do not

involve judgment or expertise and that are therefore candidates for application of “lean

principles.”

17-85

Education.

Chapter 17 – The Management and Control of Quality

17-76 (Continued-1)

The key, according to the authors, is to (p. 103) “get everyone in the organization to

systematically make waste visible and (then to) do something about it.” To accomplish

this, the authors offer the following specific strategies: teach everyone in the

and how the specification (codification) of tasks resulted in increased

performance (i.e., document the benefits)

(d) Keep studying the work that has been designated as “tacit” (what is currently

an uncommon event may, in the future, occur frequently, i.e., may be

repetitive in nature and therefore capable of being codified)

Structure Communications (i.e., how workers should communicate with one

another)

The workplace today is truly global in nature: work teams may have members from all

over the world. Thus, an effective employee communication plan or structure should be

in place to determine how employee communications should take place.

Three suggestions are offered by the authors in terms of structuring communications:

17-86

Education.

Chapter 17 – The Management and Control of Quality

17-76 (Continued-2)

(c) Resolve disagreements with facts, not opinions

it becomes to find a fix for the problem)

Plan for an Incremental Journey: A Lean System Takes Years to Build

(a) Start small (e.g., use pilot projects, to explore for your organization whether a

lean approach is a viable option)

(b) Codify lessons learned

(c) Keep looking for new ways to work—keep in mind that the ultimate goal is to

fundamentally change how knowledge work is performed

training and motivating their teams. Among other things, these managers

should impress upon their teams the notion that lean efforts will improve

performance.

17-87

Education.

Chapter 17 – The Management and Control of Quality

17-76 (Continued-3)

(b) Senior leaders must be long-term champions—remember: the ultimate goal is

17-88

Education.

Chapter 17 – The Management and Control of Quality

CHECK FIGURES

17-37 No check figure.

17-40 No check figure.

17-41 No check figure.

17-45 No check figure.

17-46 No check figure.

17-48 No check figure.

17-49 1. Total Prevention Costs = $280,000; Total Internal Failure Costs = $600,000;

$137,700.

17-55 No check figure.

17-56 1. Production (manufacturing) lead time: under current process = 480 minutes;

Alternative #1 = 0.48; under Alternative #2 = 0.39

17-59 No check figure.

17-89

Education.

Chapter 17 – The Management and Control of Quality

17-62 No check figure.

17-63 No check figure.

17-65 No check figure.

17-66 3. Estimated annual increase in contribution margin = $950,000; estimated

17-67 No check figure.

17-68 1. Change in pre-tax cash flow per year (after installation of new tracking

Failure Cost to Sales = 1.10%; External Failure Costs to Sales = 1.50%.

17-72 No check figure.

17-73 2. Net promoter score = 2.8% (i.e., 36.2% − 33.4%)

17-76 No check figure.

17-90

Education.