Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

Chapter 07 - Cost Allocation: Departments, Joint Products, and By-Products

7-24 Cost Allocation and Taxation at Nonprofit Organizations (10 min)

The nonprofit has an incentive to allocate a relatively large portion of the

common costs to the business activity to reduce taxes, but current Treasury

regulations require that the cost allocation be reasonable. This has led

some to argue that common costs should not be allocated in these cases.

However, an analytical study (using economic models) of the economic

Based on an article by Daniel Tinkelman, “Nonprofit Organizations’ Cost

Allocations,” The CPA Journal, July 2005. See also, Michelle H. Yetman

and Robert J. Yetman, “The Effects of Governance on the Accuracy of

Charitable Expenses Reported by Nonprofit Organizations,” Contemporary

Accounting Research, September 2012, pp 738-767.

7-11

Education.

7-25 Fuel Surcharges: Allocating the Increased Cost of Fuel (20

min)

1.,2.

The rising cost of fuel has affected many industries, but particularly

those in the transportation industries. In air freight, trucking, and

railroads, the surcharges can be as high as 35% of average charges.

The surcharges can be a substantial portion of total revenues for

The issue of surcharges for railroads has been a contentious

one for the shippers and railroads. There have been several law

suits regarding the conflicts and currently several of the largest U.S.

railroads are subject to a suit charging price fixing regarding their use

of surcharges. The railroads’ attempt to have the suit dismissed

recently failed in U.S. courts (https://ecf.dcd.uscourts.gov/cgi-

bin/show_public_doc?2007mc0489-138). Apparently the STB ruling in

January 2007 was ineffective in resolving the surcharge issue for the

railroads and shippers. One reason it may have failed is that it

did not provide clear guidance regarding what would be an

fuel cost increases. Also, one might consider an allocation that is

based on both miles and weight of product shipped. The goal is to

find the causal link between the use of fuel and the railroads’ service

to the shipper.

The railroads in 2012 and 2013 appealed the certification of the

The litigation is on-going, as of August 2014.

See an August 12, 2013 report in Claims Journal by Andrew Zajac and Tom

Schoenberg, “Railroads Win Class Certification Appeal in Price-Fix Case,

http://www.claimsjournal.com/news/national/2013/08/12/234720.htm

7-12

Chapter 07 - Cost Allocation: Departments, Joint Products, and By-Products

7-25 (continued -1)

3. The sustainability issue arises in the case of rail transport because

rail transport is more efficient than truck transport. A shipper that

has the option between the two methods of transport should consider

Based on: “U.S. Appellate Court Reverses Class-certification

Decision for Fuel Surcharge-fixing Lawsuit Against Four Class Is,”

August 12, 2013,

http://www.progressiverailroading.com/norfolk_southern/news/US-

appellate-court-reverses-classcertification-decision-for-fuel-

surchargefixing-lawsuit-against-four-Class-Is--37234;

Also, Christine Hauser, “Shippers May Raise Fuel Fees,” The New

York Times, April 26, 2011; Mina Kimes, “Railroads: Cartel or Free

Market Success Story?” Fortune, September 26, 2011; John D.

Schultz, “Fuel Surcharge Lawsuits: Antitrust Fines Growing,”

Logistics Management, July 1, 2008;Gargi Chakrabarty, “Many

Businesses in no Hurry to Pass on Savings,” Rocky Mountain News,

October 31, 2008.

7-13

Education.

Chapter 07 - Cost Allocation: Departments, Joint Products, and By-Products

7-26 Cost Allocation and Legal Disputes (30 Min)

The actual case is based on a dispute between the Department of Health

and Family Services (DHFS) of the State of Wisconsin and St. Francis

Home in the Park (the nursing home). The judgments shown below are by

the State of Wisconsin Court of Appeals, dated March 23, 1999. The full

explanation of the case is at the following site:

https://www.wicourts.gov/ca/opinion/DisplayDocument.html?

content=html&seqNo=13846

1. The court determined that further documentation was not required,

but that the stated reason for charging these items to the nursing

home is persuasive, and that further, DHFS had not shown that it had

costs to the nursing home was therefore allowed.

2. The court determined that DHFS had “no substantial basis” for

disallowing the direct assignment of the nourishment costs to the

nursing home. The court judged that it was apparent that the nursing

the costs should therefore be traced directly to the nursing home.

3. The court again agreed with NCI’s position, stating that it was

unreasonable for NCI to provide a fully reliable system for only a few

court disallowed DHFS’s objection.

4. Both parties were asked and agreed that the square footage basis for

allocation of costs does not represent actual electricity usage. The

court stated: “..the square footage allocation wrongly assumes that

electricity is a fixed overhead cost that does not vary with the level of

substantial basis to disallow the method used by NCI.

5. The argument that NCI competes in the same manner (cost

leadership) for both the nursing home and the apartment-retirement

home is arguable. Is there evidence that the retirement home is a

7-14

Education.

Chapter 07 - Cost Allocation: Departments, Joint Products, and By-Products

7-27 Cost Allocation; Cost Shifting (15 min)

1. The cost-shifting in this case is from the airlines (that experience

lower costs of baggage handling) to TSA (that experience a larger

number of “carry-on” bags to examine) and to the airline passengers

(who experience the discomfort of increased time in going through

TSA security and the cost of the $2.50 security fee that is included in

each passenger’s one-way ticket.

Note: because of increased baggage handling and security

responsibilities, the Transportation Security Administration (TSA) has

at the gate because the increase in the number of carry-on bags

exceeds the aircraft’s capacity for these bags.

2. Cost-shifting is frequently an area of ethical concern, as it involves

shifting the cost burden from one entity or individual to another.

new charges and delays, and others seeking low air fares.

3. Given the emphasis airline customers place on price, air travel has

become somewhat of a commodity. It is hard to differentiate the

different carriers. The “fees for services” approach is consistent with

Source: See Real World Focus “Commodities, Globalization and Cost

Leadership,” in Chapter 1, p 17. Also, Christine Negroni, “More Fees,

More Carry-Ons,” The New York Times, March 29, 2011, p B4; Michelle

Higgins, “Elite for a Day, In Coach for a Fee,” The New York Times,

September 4, 2011. “For TSA security fee information, see www.TSA.gov.

7-15

Education.

Chapter 07 - Cost Allocation: Departments, Joint Products, and By-Products

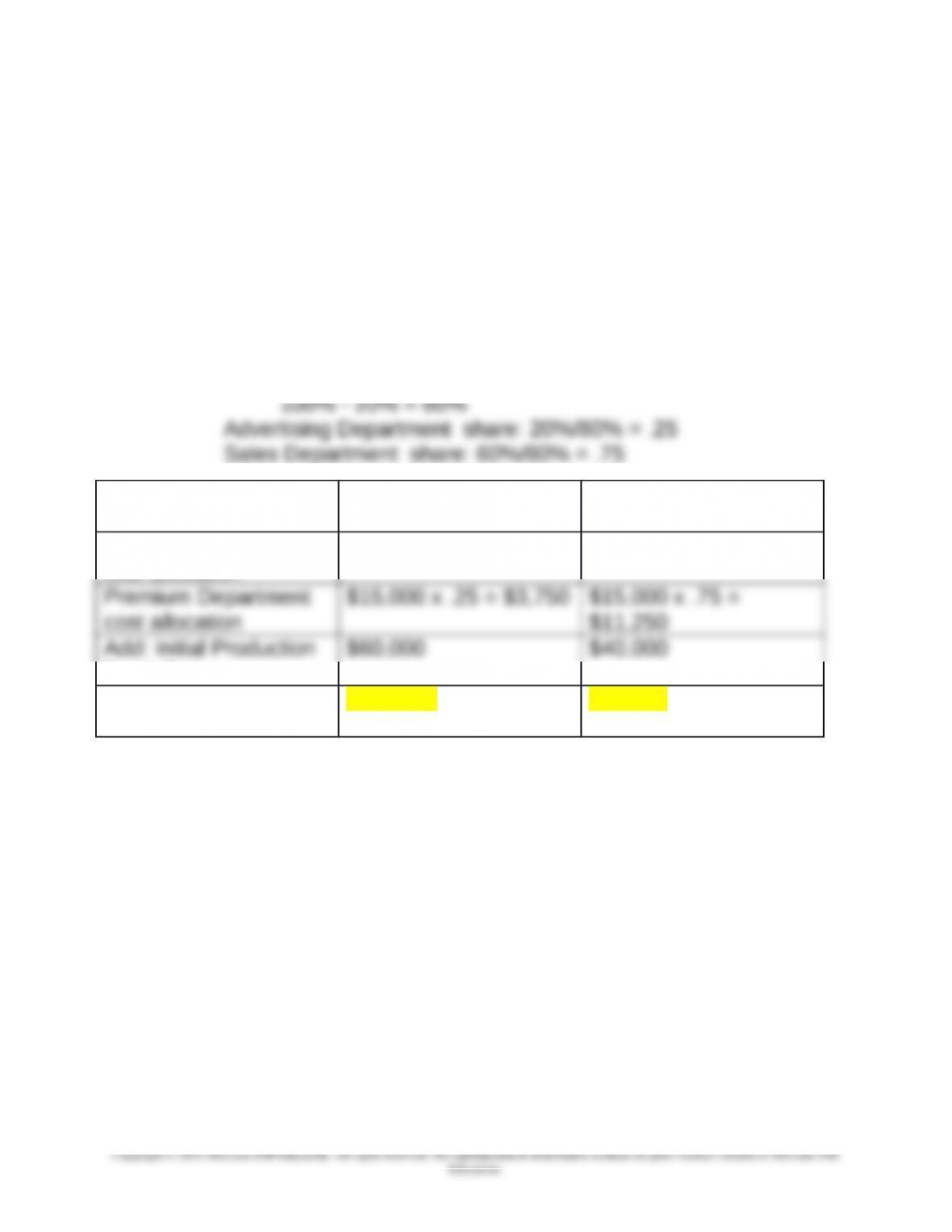

7-28 Departmental Cost Allocation (25 min)

1. The Direct Method

Net service to both Production Departments (Advertising and Sales)

for the Actuarial Service Dept:

100% - 80% = 20%

Advertising Department share: 10%/20% = .5

Sales Department share: 10%/20% = .5

Net Service to both Production Departments for Premium

Department:

Advertising

Department

Sales Department

Actuarial Department

cost allocation

$80,000 x .5 = $40,000 $80,000 x .5 = $40,000

Dept. Costs

Total Cost for Each

Production Dept.

$103,750 $91,250

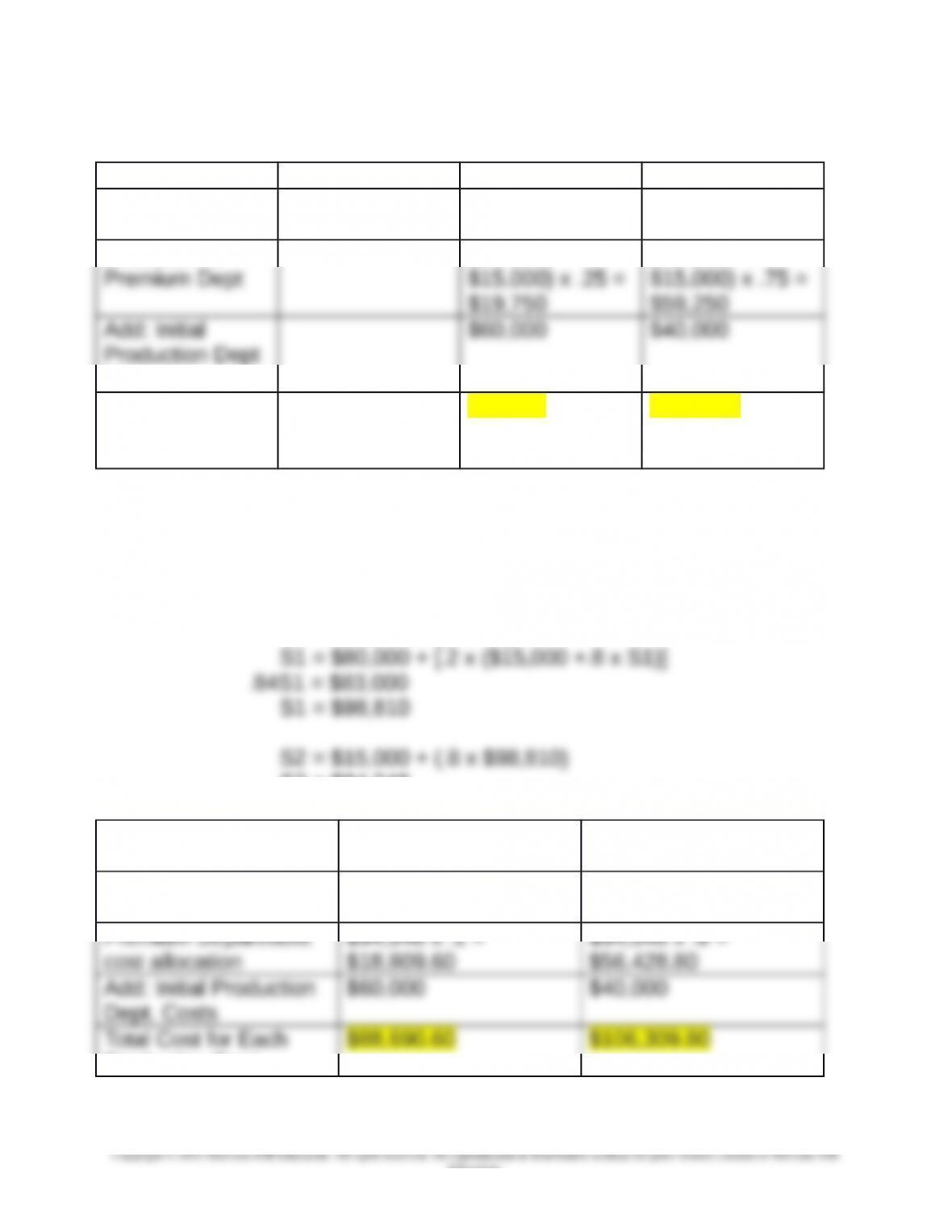

2. Step Method

The Actuarial Department goes first, since it provides the greatest

service to other service departments.

7-16

Chapter 07 - Cost Allocation: Departments, Joint Products, and By-Products

7-28 (continued -1)

Premium Dept. Advertising Dept Sales Dept

Allocation of

Actuarial Dept

$80,000 x .8 =

$64,000

$80,000 x .1 =

$8,000

$80,000 x .1 =

$8,000

Allocation of

($64,000 +

($64,000 +

Costs

Total Cost for

Each Production

Department

$87,750 $107,250

3. The Reciprocal Method

Solve the Simultaneous Equations: (S1=actuarial; S2=premium)

S1 = $80,000 + (.2 x S2)

S2 = $15,000 + (.8 x S1)

S2 = $94,048

Advertising

Department

Sales Department

Actuarial Department

cost allocation

$98,810 x .1 = $9,881 $98,810 x .1 = $9,881

Production Dept.

7-17

Education.

Chapter 07 - Cost Allocation: Departments, Joint Products, and By-Products

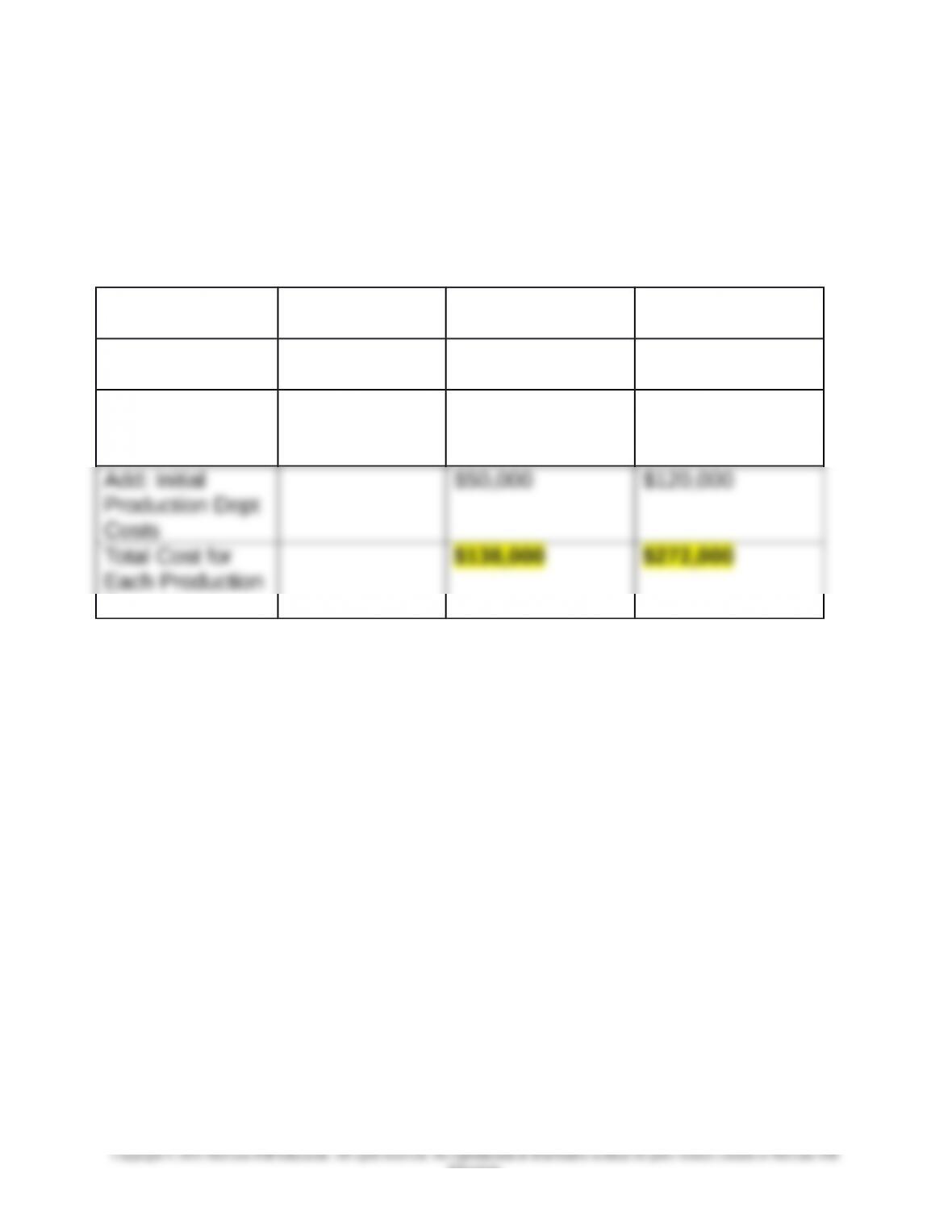

7-29 Departmental Cost Allocation (30 min)

First, find the unknown service rates:

From S1 to P2 = 100% - 10% - 20% = 70%

From S2 to P1 = 100% - 10% - 30% = 60%

1. The Direct Method

Net service to both Production Departments for Service

Department 1: 100% - 10% = 90%

Production Department 1 share: 60%/90% = 2/3

Production Department 2 share: 30%/90% = 1/3

Production

Department 1

Production

Department 2

Service department 1

cost allocation

$180,000 x 2/9 =

$40,000

$180,000 x 7/9 =

$140,000

Service department 2

cost allocation

$60,000 x 2/3 =

$40,000

$60,000 x 1/3=

$20,000

Production Dept.

7-18

Education.

Chapter 07 - Cost Allocation: Departments, Joint Products, and By-Products

7-29 (continued -1)

2. Step Method

Both service departments serve each other the same percentage of

total service; hence, either can go first. Here, Service Dept 1 goes

first on the basis that it has the highest total cost:

Service Dept 2 Production Dept

1

Production Dept

2

Allocation of

Service Dept 1

$180,000 x .1 =

$18,000

$180,000 x .2 =

$36,000

$180,000 x .7 =

$126,000

Allocation of

Service Dept 2

($60,000 +

$18,000) x 2/3 =

$52,000

($60,000 +

$18,000) x 1/3 =

$26,000

Department

7-19

Education.

Chapter 07 - Cost Allocation: Departments, Joint Products, and By-Products

7-29 (continued -2)

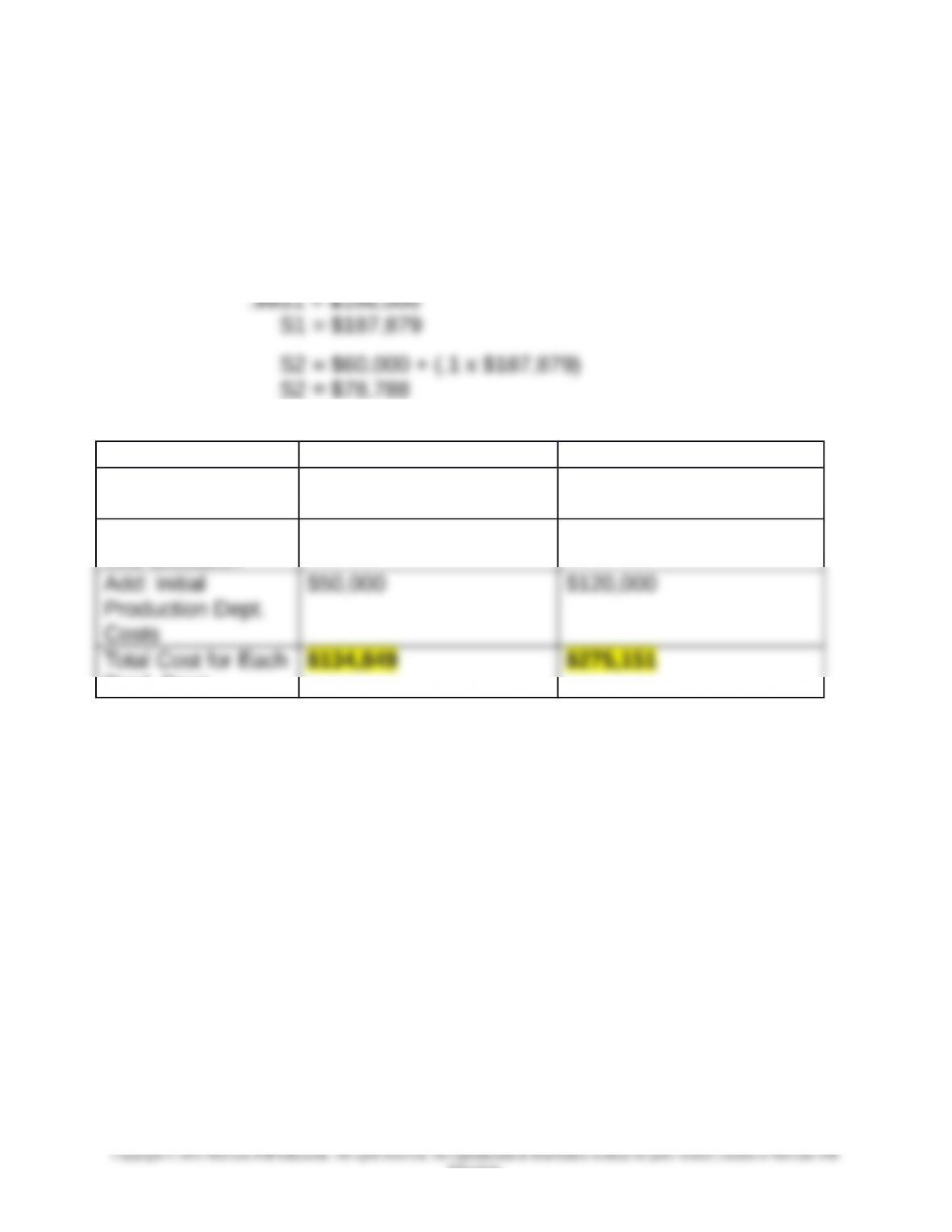

3. The Reciprocal Method

Solve the Simultaneous Equations:

S1 = $180,000 + (.1 x S2)

S2 = $60,000 + (.1 x S1)

S1 = $180,000 + [.1 x ($60,000 +.1 x S1)]

Production Department 1 Production Department 2

Service Dept 1

cost allocation

$187,879 x .2 =

$37,576

$187,879 x .7 = $131,515

Service Dept 2

cost allocation

$78,788 x .6 = $47,273 $78,788 x .3 = $23,636

Prod. Dept.

7-20

Education.