Archives

Accounting Chapter 1 Are Fully Remunerated Serve Full Time

a 21. Financial accounting. d 22. Users of financial reports. d 23. Identify the major financial statements. a 24. Financial reporting entity. d 25. Differences between financial and managerial accounting. b 26. Financial reporting communication. b 27. Managerial accounting. a […]

Accounting Chapter 14 Ignoring Income Tax Considerations How Should These

a 21. Liability identification. a 22. Bond terms. b 23. Definition of “debenture bonds.” a P24. Definition of bearer bonds. d S25. Definition of income bonds. a S26. Effective-interest vs. straight-line method. d S27. Interest rate of the bond indenture. […]

Accounting Chapter 19 Taxes 88 Khan Inc Reports Taxable And

b 21. Differences between taxable and accounting income. c 22. Differences between taxable and accounting income. b 23. Determination of deferred tax expense. a 24. Differences arising from depreciation methods. a P25. Temporary difference and a revenue item. b S26. […]

Accounting Chapter 2 The Accounting Principal Expense Recognition Best Demonstrated

c 21. GAAP defined. d 22. Purpose of conceptual framework. c 23. Conceptual framework. d 24. Conceptual framework purpose. d S25. Conceptual framework benefits. d 26. Objectives of financial reporting. a 27. Decision usefulness. d 28. General purpose of financial […]

Accounting Chapter 22 January 2027 During 2015 Hess Determined That

b 21. Accounting changes and consistency concept. b 22. Identify changes in accounting principle. c 23. Identify a non-retrospective change. d 24. Identify a change in accounting principle. a 25. Entry to record a change in depreciation methods. c 26. […]

Accounting Chapter 23 Companys Statement Cash Flows For 2015 Was

c 21. Objective of the statement of cash flows. c 22. Primary purpose of the statement of cash flows. c S23. Answers provided by the statement of cash flows. b S24. First step in cash flow statement preparation. d 25. […]

Accounting Chapter 24 June 30 2015 What The Total Amount

d 21. Disclosure of significant accounting policies. c 22. Disclosure of inventory accounting policy. c 23. Definition of errors and irregularities. d S24. Full disclosure principle description. b S25. APB Opinion No. 22 disclosure. b S26. Related party transactions. c […]

Accounting Chapter 3 December 31 2014 December 31 2013 Prepaid

d 21. Purpose of an accounting system. d 22. Definition of posting. d 23. Purpose of an accounting system. d 24. Book of original entry. d 25. Purpose of trial balance. d 26. Identification of a real account. b 27. […]

Accounting Chapter 4 Net Income Dividends Common Stock Dividends Preferred

c 21. Elements of the income statement. d 22. Usefulness of the income statement. b 23. Limitations of the income statement. d S24. Use of an income statement. d S25. Income statement reporting. b 26. Usefulness of income statement. b […]

Accounting Chapter 5 Balance Sheet And Statement Cash Flows 101

Answer No. Description d 21. Limitation of the balance sheet. c 22. Uses of the balance sheet. b 23. Use of balance sheet information. d 24. Use of balance sheet information. d 25. Limitation of the balance sheet. c S26. […]

Accounting Chapter 6 December 31st For The Next Six Years

Answer No. Description a 21. Appropriate use of an annuity due table. d 22. Time value of money. b 23. Present value situations. a 24. Definition of interest. c 25. Interest variables. d 26. Identification of compounding approach. b 27. […]

Accounting Exam A Common Stock 10 Par 16 Inventory

COMPREHENSIVE EXAMINATION A PART 1 (Chapters 1-6) Problem A-I — Multiple Choice. Choose the best answer for each of the following questions and enter the identifying letter in the space provided. ____ 1. How does failure to record accrued revenue […]

Accounting Exam B December 30 The Invoice Shows That Merchandise

COMPREHENSIVE EXAMINATION B PART 2 (Chapters 7–9) Problem B-I — Multiple Choice — Cash and Receivables. Choose the best answer for each of the following questions and enter the identifying letter in the space provided. ____ 1. When should the […]

Accounting Exam C Hanson Corporation Sold Its 8 10 year

COMPREHENSIVE EXAMINATION C PART 3 (Chapters 10–14) Problem C-I — Multiple Choice — Tangible and Intangible Assets. Choose the best answer for each of the following questions and enter the identifying letter in the space provided. ____ 1. When the […]

Accounting Exam D January 2014 Was Instructions Prepare Necessary

COMPREHENSIVE EXAMINATION D PART 4 (Chapters 15-17) Approximate Problem Topic Time D-I Treasury Stock. 20 min. D-II *Cash Dividends. 10 min. D-III Stock Dividends and Stock Splits. 10 min. D-IV Earnings Per Share Concepts. 10 min. D-V Earnings Per Share […]

Accounting Exam E Pinkley Company For Machinery Which Was Carried

COMPREHENSIVE EXAMINATION E PART 5 (Chapters 18-21) Approximate Problem Topic Time E-I Long-Term Contracts. 15 min. E-II Installment Sales Method. 20 min. E-III Deferred Income Taxes. 25 min. E-IV Pensions. 15 min. E-V Leases. 25 min. 100 min. Test Bank […]

Accounting Exam F The Following Calculations Present Depreciation Both Bases

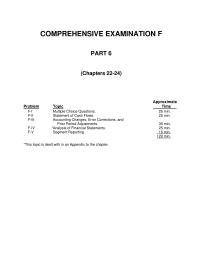

COMPREHENSIVE EXAMINATION F PART 6 (Chapters 22-24) Approximate Problem Topic Time F-I Multiple Choice Questions. 25 min. F-II Statement of Cash Flows. 25 min. F-III Accounting Changes, Error Corrections, and Prior Period Adjustments. 30 min. F-IV * Analysis of Financial […]

Alternate Solutions Account Insurance Expense Date Explanation

81A BALANCE 5148 DATE EXPLANATION REF. DEBIT CREDIT 2014 1/1 Balance ✔ ACCOUNT: Federal Withholding Taxes Payable 216 BALANCE 1595 2486 2676 2901 4418 4618 11/30 Balance ✔ 12/9 CD 18 1 9 0 12/23 CD 18 2 2 5 […]

Alternate Solutions Homework To record cost of goods returned by customer

59A ALTERNATIVE SOLUTION The following pages 61A-114A contain the solution to the “Alternative Set of Instructions” (pages 87-89) for the Rockford Corporation practice set. 61A JOURNALS GENERAL JOURNAL PURCHASES JOURNAL SALES JOURNAL CASH RECEIPTS JOURNAL CASH DISBURSEMENTS JOURNAL DATE Account […]

Alternate Solutions Selling Expenses Advertising Expense Miscellaneous

ACCOUNTS PAYABLE SUBSIDIARY LEDGER BALANCE 26400 -0- 63940 12/2 280 26400 12/30 1/10, n/30 320 63940 DATE EXPLANATION REF. DEBIT CREDIT 2014 11/30 Balance ✔ ACCOUNT: Oxenford Copperworks 35 BALANCE 14850 11/30 Balance ✔ DATE EXPLANATION REF. DEBIT CREDIT 2014 […]

Chapter 1 Accounts Receivable–Iwanaga Plumbing and Heating

1A ALTERNATIVE SOLUTION The following pages 3A-57A contain the solution to the “Alternative Set of Instructions” (pages 17-19) for the Rockford Corporation practice set. 3A JOURNALS GENERAL JOURNAL PURCHASES JOURNAL SALES JOURNAL CASH RECEIPTS JOURNAL CASH DISBURSEMENTS JOURNAL DATE Account […]

Chapter 1 Audited Financial Statements Provide These Users With

Continuing Case Solution Chapter 1 Memorandum To: Eric Conner and Phil Martin, CM Corporation From: L. Harbach Re: SEC Regulations and FASB Standards for Non-Public Companies Date: January 2, 2013 (a) As a non-public company, CM Corporation is not subject […]

Chapter 1 Authoritative pronouncements and rulemaking bodies

CHAPTER 1 Financial Accounting and Accounting Standards ASSIGNMENT CLASSIFICATION TABLE (By Topic) Topics Questions Cases 1. Subject matter of accounting. 1 4 2. Environment of accounting. 2, 3, 28 6, 7 3. Role of principles, objectives, standards, 4, 5, 6, […]

Chapter 1 Increase in salaries and wages payable

ACCOUNTS PAYABLE SUBSIDIARY LEDGER BALANCE 26400 -0- 63940 11/30 Balance ✔ 12/2 280 26400 12/30 1/10, n/30 320 63940 DATE EXPLANATION REF. DEBIT CREDIT 2014 ACCOUNT: Oxenford Copperworks 35 BALANCE 14850 11/30 Balance ✔ DATE EXPLANATION REF. DEBIT CREDIT 2014 […]

Chapter 1 Paid-in Capital in Excess of Stated Value

23A BALANCE 5148 DATE EXPLANATION REF. DEBIT CREDIT 2014 1/1 Balance ✔ ACCOUNT: Federal Withholding Taxes Payable 216 BALANCE 1595 2486 2676 2901 4418 4618 11/30 Balance ✔ 12/9 CD 18 1 9 0 12/23 CD 18 2 2 5 […]

Chapter 1 The public/private mixed approach appears to be the

CA 1-10 (Continued) (c) Arguments against the politicalization of the accounting rule-making process: 1. Many accountants feel that accounting is primarily technical in nature. Consequently, they feel that substantive, basic research by objective, independent and fair-minded researchers ultimately will result […]

Chapter 10 GAAP identifies assets which qualify for interest capitalization

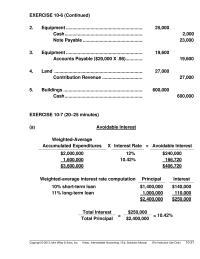

EXERCISE 10-6 (Continued) 2. Equipment ………………………………………………………. 25,000 Cash ………………………………………………………. 2,000 Note Payable …………………………………………………. 23,000 3. Equipment ………………………………………………………. 19,600 Accounts Payable ($20,000 X .98) ……………………. 19,600 4. Land …………………………………………………………………….. 27,000 Contribution Revenue ………………………….. 27,000 5. Buildings ………………………………………………………. 600,000 Cash ………………………………………………………. 600,000 […]

Chapter 10 I have analyzed the four options you presented

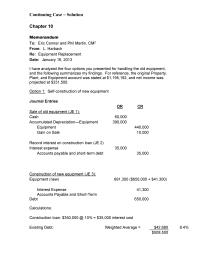

Continuing Case Solution Chapter 10 Memorandum To: Eric Conner and Phil Martin, CM2 From: L. Harbach Re: Equipment Replacement Date: January 16, 2013 I have analyzed the four options you presented for handling the old equipment, Option 1: Self-construction of […]

Chapter 10 Interest imputed on common stock financing is not

CHAPTER 10 Acquisition and Disposition of Property, Plant, and Equipment SOLUTIONS TO B PROBLEMS PROBLEM 10-1 (a) REAGAN COMPANY Analysis of Land Account for 2012 Balance at January 1, 2012 ………………. $ 230,000 Land site number 621 Acquisition cost ……………………………… […]

Chapter 10 Loans Outstanding During Construction Period

PROBLEM 10-6 INTEREST CAPITALIZATION Balance in the Land Account Purchase Price …………………………………………………………….. $139,000 Surveying Costs …………………………………………………………… 2,000 Expenditures (2012) Weighted—Average Accumulated Expenditures Date Amount Fraction 1-Dec $147,000 1/12 $12,250 1-Dec 30,000 1/12 2,500 1-Dec 3,000 1/12 250 $180,000 $15,000 Interest […]

Chapter 10 The Basic Principle Involved Record The New

CHAPTER 10 Acquisition and Disposition of Property, Plant, and Equipment ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis 1. Valuation and classification of land, buildings, and equipment. 1, 2, 3, 4, 6, 7, 12, […]

Chapter 10 Typical transactions involve allocation of the cost

EXERCISE 10-23 (20–25 minutes) (a) C (b) E (immaterial) (c) C (d) C (e) C (f) C (g) C (h) E EXERCISE 10-24 (20–25 minutes) (a) Depreciation Expense (8/12 X $60,000) …………………….. 40,000 Accumulated Depreciation—Machinery ……………. 40,000 Loss on Disposal […]

Chapter 10 Use appraised values to break-out the lump-sum

E10-15B (Continued) (c) Notes Payable ………………………………………………………. 10,000 Interest Expense ……………………………………………………. 2,650 Cash ………………………………………………………. 10,000 Discount on Notes Payable ………………………….. 2,650 E10-16B (25–35 minutes) OGDEN INDUSTRIES Acquisition of Assets 1 and 2 Use appraised values to break-out the lump-sum purchase Description […]

Chapter 10 Repair cost incurred in the first year of operations

CHAPTER 10 SOLUTIONS TO B EXERCISES E10-1B (15–20 minutes) Item Land Land Improvements Building Other Accounts (a) ($357,500) Notes Payable (b) $357,500 (c) $ 10,400 (d) 9,100 (e) 7,800 (f) (1,300) (g) 28,600 (h) 325,000 (i) 11,700 (j) $ 5,200 […]

Chapter 10 This illustrates the exception to no gain or loss recognition

PROBLEM 10-9 (Continued) Wiggins, Inc.’s Books Cash ……………………………………………………………… 15,000 Machienry (A) ………………………………………………… 50,400** Accumulated Depreciation—Machinery (B) ……… 47,000 Machinery (B) …………………………………………. 110,000 Gain on Disposal of Machinery ………………… 2,400* Computation of total gain: Fair value of Asset B $75,000 Less: […]

Chapter 11 Continuing Case Solution A Memorandum To

Continuing Case Solution Chapter 11 (a) Memorandum To: Eric Conner and Phil Martin, CM2 From: L. Harbach Re: Depreciation and Impairment Date: January 18, 2013 According to FASB ASC 360-10-35-4: The cost of a productive facility is one of the […]

Chapter 11 Depreciation Not Taken Assets Intended Sold

PROFESSIONAL RESEARCH (Continued) 35–30 For example, valuation techniques consistent with the market approach often use market multiples derived from a set of comparables. Multiples might lie in ranges with a different multiple for each comparable. The selection of where within […]

Chapter 11 Homework Sons Inc 150 115 10 Cost Rate

PROBLEM 11-2 Depreciation Expense 2014 2015 (a) Straight-line: ($89,000 – $5,000) ÷ 7 = $12,000/yr. 2014: $12,000 X 7/12 $7,000 2015: $12,000 $12,000 (b) Units-of-output: ($89,000 – $5,000) ÷ 525,000 units = $.16/unit 2014: $.16 X 55,000 8,800 2015: $.16 […]

Chapter 11 Machine C—Using the double-declining balance method

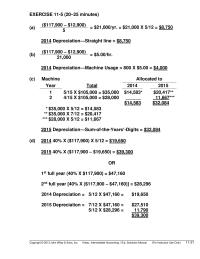

EXERCISE 11-5 (20–25 minutes) (a) ($117,900 – $12,900) = $21,000/yr. = $21,000 X 5/12 = $8,750 5 2014 Depreciation—Straight line = $8,750 (b) ($117,900 – $12,900) = $5.00/hr. 21,000 2014 Depreciation—Machine Usage = 800 X $5.00 = $4,000 (c) Machine […]

Chapter 11 The amounts to be recorded on the books of Darby

CHAPTER 11 Depreciation, Impairments, and Depletion SOLUTIONS TO B PROBLEMS PROBLEM 11-1 (a) 1. Depreciable Base Computation: Purchase price ………………………… $85,000 Less: Purchase discount (2%) ….. 1,700 Freight-in ………………………………… 800 Installation ………………………………. 3,800 87,900 Less: Salvage value ………………… 1,500 Depreciation […]

Chapter 11 The Principal Disadvantage That After Period Time

CHAPTER 11 Depreciation, Impairments, and Depletion ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis 1. Depreciation methods; meaning of depreciation; choice of depreciation methods. 1, 2, 3, 4, 5, 6, 10, 14, 20, 21, […]

Chapter 11 The Year Which There Are Remaining Years

CHAPTER 11 SOLUTIONS TO B EXERCISES E11-1B (15–20 minutes) (a) Straight-line method depreciation for each of Years 1 through 3 = $500,000 – $50,000 = $45,000 10 (b) Sum-of-the-years’-digits = 10 X 11 = 55 2 10/55 X ($500,000 – […]

Chapter 11 You Also Mentioned That Using Straightline Depreciation

SOLUTIONS TO CONCEPTS FOR ANALYSIS CA 11-1 (a) The purpose of depreciation is to distribute the cost (or other book value) of tangible plant assets, less salvage, over their useful lives in a systematic and rational manner. Under generally accepted […]

Chapter 11 Encino Athletic Equipment Company are calculated

Name: Date: Instructor: Course: for $315,000 10 $15,000 240,000 25,000 2,650 25,500 Amount Amount Formula Number Formula Number Formula Depreciable value: Life units expected: Depreciation per unit: Period units: Period depreciation: Amount Amount Formula Number Formula Number Formula Formula Formula […]

Chapter 12 Assets Gt 350 Intangibles Goodwill And

CA 12-2 (Continued) Developments between the balance sheet date and the date that the financial statements are released would properly be reflected in notes to the statements as post-balance sheet (or subsequent events) disclosure. CA 12-3 (a) Research, as defined […]

Chapter 12 Events such as an expectation of selling assets

Copyright © 2013 John Wiley & Sons, Inc. Kieso, Intermediate Accounting, 15/e, Exercise B Solutions (For Instructor Use Only) 12-1 Music copyrights Customer lists Goodwill Covenants not to compete Internet domain name Brand names CHAPTER 12 SOLUTIONS TO B EXERCISES […]

Chapter 12 Fair Value Conchita Division Carrying Value

EXERCISE 12-11 (Continued) (b) Analysis of 2014 transactions 1. The $245,700 incurred for research and development should be expensed. 2. The book value of Patent B is $11,250 and its estimated future cash flows are $6,000: (3 X $2,000); therefore […]

Chapter 12 Research and development expense in the income statement

CHAPTER 12 SOLUTIONS TO B PROBLEMS PROBLEM 12-1B Franchises …………………………………………………………… 60,000 Prepaid Rent ………………………………………………………… 24,000 Retained Earnings (Net loss + R&D) ………………………. 108,000 Patents ($80,000 + $13,500) …………………………………… 93,500 Research and Development Expense …………………….. 265,000 Intangible Assets …………………………………………. 550,500 Amortization […]

Chapter 12 The goodwill is considered impaired because the fair

Continuing Case Solution Chapter 12 Part I Memorandum To: Eric Conner and Phil Martin, CM2 From: L. Harbach Re: Goodwill and R&D Costs Date: January 20, 2013 Goodwill: Goodwill is defined as the excess cost over the fair value of […]

Chapter 12 The Impairment Loss Measured The Amount Which

CHAPTER 12 Intangible Assets ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis 1. Intangible assets; concepts, definitions; items comprising intangible assets. 1, 2, 3, 4, 5, 6, 7, 8, 9, 10, 11, 12, 13, […]

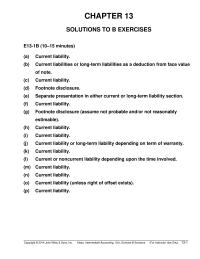

Chapter 13 Because the cause for litigation occurred before

PROBLEM 13-9B (Continued) 2015 Inventory of Premiums …………………………………………… 400,000 Cash ……………………………………………………………… 400,000 (To record the purchase of 500,000 download codes at $0.80 each) Cash ……………………………………………………………………… 1,520,000 Sales Revenue ……………………………………………….. 1,520,000 (To record the sale of 7,600,000 candy bars at 20 […]

Chapter 13 Current Liabilities Warranty Liability 189750 Longterm

CHAPTER 13 SOLUTIONS TO B PROBLEMS PROBLEM 13-1B (a) March 10 Purchases ……………………………………………………… 42,000 Accounts Payable …………………………………. 42,000 March 19 Accounts Payable ………………………………………….. 42,000 Purchase Discounts ($42,000 X 1%) ……….. 420 Cash …………………………………………………….. 41,580 April 1 Cash ……………………………………………………………… 172,000 Discount […]

Chapter 13 Financial statement impact of liability transactions

CHAPTER 13 Current Liabilities and Contingencies ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis 1. Concept of liabilities; definition and classification of current liabilities. 1, 2, 3, 4, 6, 8 1, 16 1, 2 […]

Chapter 13 Separate presentation in either current or long-term

(c) Current liability. (d) Footnote disclosure. (e) Separate presentation in either current or long-term liability section. (f) Current liability. (g) Footnote disclosure (assume not probable and/or not reasonably estimable). (l) Current or noncurrent liability depending upon the time involved. (m) […]

Chapter 13 The Student Must Compute Income Tax Withheld

EXERCISE 13-6 (Continued) (b) Accrued liability at year-end: 2013 2014 Jan. 1 balance $ 0 $7,740 + accrued 7,740 8,352 – paid ( 0) (6,966) Dec. 31 balance $7,740 (1) $9,126 (2) (1) 9 employees X $10.75/hr. X 8 hrs./day […]

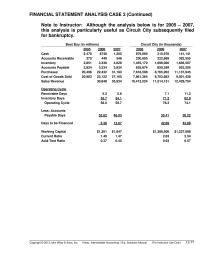

Chapter 13 The warranty payable and the interest payable

FINANCIAL STATEMENT ANALYSIS CASE 3 (Continued) Note to Instructor: Although the analysis below is for 2005 – 2007, this analysis is particularly useful as Circuit City subsequently filed for bankruptcy. Best Buy (in millions) Circuit City (in thousands) 2005 2006 […]

Chapter 13 These Audits May Result The Assessment Additional

FINANCIAL REPORTING PROBLEM (Continued) (c) P&G provided the following discussion related to commitments and contingencies: Note 10: Commitments and Contingencies Guarantees In conjunction with certain transactions, primarily divestitures, we may provide routine indemnifications (e.g., indemnification for representa– tions and warranties […]

Chapter 13 Unearned Revenue Account Make Sure That The

Continuing Case Solution Chapter 13 Part I Memorandum To: Eric Conner and Phil Martin, CM2 From: L. Harbach Re: Unearned Revenue and Contingencies Date: January 24, 2013 Here are the answers to your questions for the year ended December 31, […]

Chapter 13 Windsor Airlines need not establish a liability

PROBLEM 13-7 (a) (1) Cash ………………………………………………………. 4,440,000 Sales Revenue (600 X $7,400) ………………………….. 4,440,000 (2) Warranty Expense ([600 X $390] / 2) …………………………. 117,000 Inventory ($170 X 600 X 1/2) ………………………….. 51,000 Salaries and Wages Payable ($220 X 600 X […]

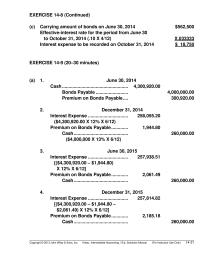

Chapter 14 American Bank Under The Debt Restructuring Agreement

EXERCISE 14-8 (Continued) (c) Carrying amount of bonds on June 30, 2014 $562,500 Effective-interest rate for the period from June 30 to October 31, 2014 (.10 X 4/12) X.033333 Interest expense to be recorded on October 31, 2014 $ 18,750 […]

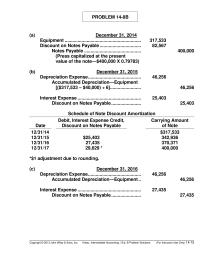

Chapter 14 Cash Interest Carrying Paid Expense Premium Amount

PROBLEM 14-8B (a) December 31, 2014 Equipment ………………………………………………………. 317,533 Discount on Notes Payable ………………………….. 82,567 Notes Payable ……………………………………………….. 400,000 (Press capitalized at the present value of the note—$400,000 X 0.79783) (b) December 31, 2015 Depreciation Expense …………………………………………….. 46,256 Accumulated Depreciation—Equipment […]

Chapter 14 Interest Expense For The Period From January

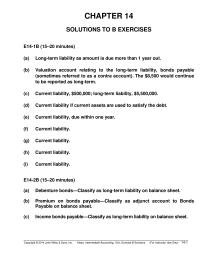

CHAPTER 14 SOLUTIONS TO B EXERCISES E14-1B (15–20 minutes) (a) Long-term liability as amount is due more than 1 year out. (b) Valuation account relating to the long-term liability, bonds payable (sometimes referred to as a contra account). The $8,500 […]

Chapter 14 Interest Expense Or Bond Issue Expense Would

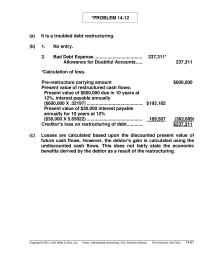

*PROBLEM 14-12 (a) It is a troubled debt restructuring. (b) 1. No entry. 2. Bad Debt Expense …………………………………………. 237,311* Allowance for Doubtful Accounts …………….. 237,311 *Calculation of loss. Pre-restructure carrying amount $600,000 Present value of restructured cash flows: Present value […]

Chapter 14 Longterm Liabilities Assignment Classification Table By

CHAPTER 14 Long-Term Liabilities ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis 1. Long-term liability; classification; definitions. 1, 10, 14, 22 1, 2 10, 11 1, 2 2. Issuance of bonds; types of bonds. […]

Chapter 14 Maturities and sinking fund requirements on long-term

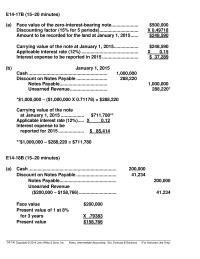

E14-17B (15–20 minutes) (a) Face value of the zero-interest-bearing note………………… $500,000 Discounting factor (15% for 5 periods) ………………………… X 0.49718 Amount to be recorded for the land at January 1, 2015 …… $248,590 Carrying value of the note at January […]

Chapter 14 Proceeds From Sale Bonds Premium Bonds

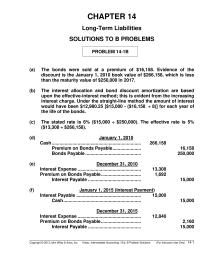

CHAPTER 14 Long-Term Liabilities SOLUTIONS TO B PROBLEMS PROBLEM 14-1B (a) The bonds were sold at a premium of $16,158. Evidence of the discount is the January 1, 2010 book value of $266,158, which is less than the maturity value […]

Chapter 15 Emporia Plastics Inc Trading The Equity Successfully

EXERCISE 15-6 (25–30 minutes) (a) Cash [(5,000 X $45) – $7,000] ……………………………… 218,000 Common Stock (5,000 X $5) ………………………… 25,000 Paid-in Capital in Excess of Par— Common Stock …………………………..……………. 193,000 (b) Land (1,000 X $46) …………………………………………….. 46,000 Common Stock (1,000 […]

Chapter 15 Equity Has Indefinite Life With Maturity Date

Continuing Case Solution 1 Chapter 15 (a) [Note to the instructor: You could require the students to show the journal entry for issuing each type of debt or equity instrument and the related interest or dividend payments.] Memorandum To: Eric […]

Chapter 15 Major Differences Relate Terminology Used Introduction Items

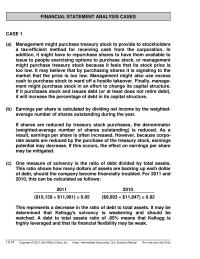

FINANCIAL STATEMENT ANALYSIS CASES CASE 1 (a) Management might purchase treasury stock to provide to stockholders a tax-efficient method for receiving cash from the corporation. In addition, it might have to repurchase shares to have them available to issue to […]

Chapter 15 One might use the cost of treasury stock

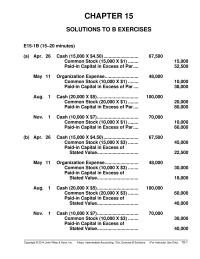

May 11 Organization Expense …………………….. 48,000 Common Stock (10,000 X $1) …….. 10,000 Paid-in Capital in Excess of Par …. 38,000 Aug. 1 Cash (20,000 X $5) ………………………….. 100,000 Common Stock (20,000 X $1) …….. 20,000 Paid-in Capital in Excess […]

Chapter 15 Paid-in capital in excess of par no effect

PROBLEM 15-8B (Continued) Note: The journal entries made for the previous transaction are: Equity Investments ($3.50 – $3.10) X 10,250 …………… 4,100 Unrealized Holding Gain or Loss—Income ………. 4,100 (To record increase in value of securities to be issued) Retained […]

Chapter 15 The Stock Dividend Results Increase The Amount

PROBLEM 15–12 PENN COMPANY Stockholders’ Equity June 30, 2015 Capital stock 8% preferred stock, $25 par value, cumulative and nonparticipating, 100,000 shares authorized, 40,000 shares issued and outstanding—Note A ……………. $1,000,000 Common stock, $10 par value, 300,000 shares authorized, 115,400 […]

Chapter 15 Wellington declares and issues a 15% stock dividend

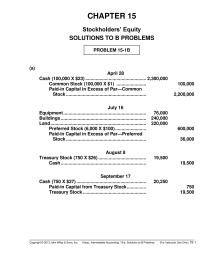

CHAPTER 15 Stockholders’ Equity SOLUTIONS TO B PROBLEMS PROBLEM 15-1B (a) April 28 Cash (100,000 X $23) ……………………………………….. 2,300,000 Common Stock (100,000 X $1) ………………….. 100,000 Paid-in Capital in Excess of Par—Common Stock …………………………………………………….. 2,200,000 July 16 Equipment ………………………………………………………. 76,000 […]

Chapter 16 Diluted Earnings Per Share Deps Of calculation Deps

Continuing Case Solution Chapter 16 Memorandum To: Eric Conner and Phil Martin, CM2 From: L. Harbach Re: Basic and Diluted Earnings Per Share Date: January 28, 2013 If CM2 decided to issue 5% cumulative, convertible preferred stock and complex. This […]

Chapter 16 Eps Standards Are Important Analysts Who Rely

CA 16-6 (Continued) 36,000 [(30,000 X $30) ÷ $25] shares of treasury stock at $25 with the proceeds. Therefore, if you add the 30,000 exercised warrants to the common stock outstanding and then subtract the 36,000 shares presumably purchased, the […]

Chapter 16 Fair Value Estimated Using Acceptable Option Pricing

CHAPTER 16 Dilutive Securities and Earnings Per Share ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis 1. Convertible debt and preferred stock. 1, 2, 3, 4, 5, 6, 7 1, 2, 3 1, 2, […]

Chapter 16 FASB allows companies to rebut the presumption that contracts

PROFESSIONAL SIMULATION (Continued) Schedule A *Computation of weighted-average number of shares adjusted for dilutive securities Average number of shares under options outstanding …………. 140,000 Option price per share ……………………………………………………….. X $10 Proceeds upon exercise of options …………………………………….. $1,400,000 Market price […]

Chapter 16 Income Before Income Taxes Income Taxes 40

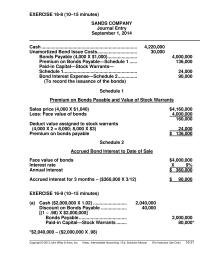

EXERCISE 16-8 (10–15 minutes) SANDS COMPANY Journal Entry September 1, 2014 Cash ……………………………………………………………….. 4,220,000 Unamortized Bond Issue Costs…………………………. 30,000 Bonds Payable (4,000 X $1,000) ………………….. 4,000,000 Premium on Bonds Payable—Schedule 1 …… 136,000 Paid-in Capital—Stock Warrants— Schedule 1 ………………………………………………… 24,000 […]

Chapter 16 memo entry made to indicate the number of rights

CHAPTER 16 Dilutive Securities and Earnings Per Share SOLUTIONS TO B PROBLEMS PROBLEM 16-1B **Allocated to Bonds: $97 X $1,060,000 = $970,000; $97 + $9 Discount = $1,000,000 – $970,000 = $30,000 **Allocated to Warrants: $9 X $1,060,000 = $90,000 […]

Chapter 16 That Portion The Proceeds Assigned The Warrants

PROBLEM 16-1 (Continued) Calculations: Common Stock Paid-in Capital in Excess of Par At beginning of year ………………….. 300,000 shares $ 600,000 From stock rights (entry #3) ………. 9,500 shares 209,000 From stock warrants (entry #4) ….. 1,600 shares 44,800 From […]

Chapter 16 Weighted-average number of shares outstanding

E16-16B (Continued) (d) Income from continuing operationsa $1.06 Loss from discontinued operationsb (0.08) Net income $0.98 a Net income available for common $6,552,000 Add: Loss from discontinued operations 500,000 Income from continuing operations $7,052,000 $7,052,000 = $1.06 6,660,000 b $(500,000) […]

Chapter 16 When The Warrants Are Nondetachable Separate Recognition

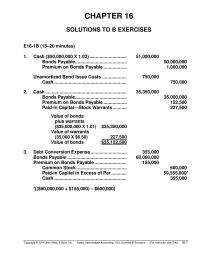

CHAPTER 16 SOLUTIONS TO B EXERCISES E16-1B (15–20 minutes) 1. Cash ($50,000,000 X 1.02) ……………………….. 51,000,000 Bonds Payable …………………………………. 50,000,000 Premium on Bonds Payable ……………… 1,000,000 Unamortized Bond Issue Costs ………………. 750,000 Cash ……………………………………………….. 750,000 2. Cash ……………………………………………………… 35,350,000 Bonds […]

Chapter 17 Any Change The Net Unrealized Holding Gain

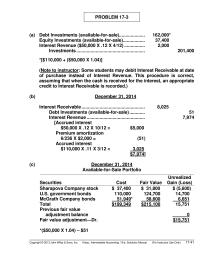

Copyright © 2013 John Wiley & Sons, Inc. Kieso, Intermediate Accounting, 15/e, Solutions Manual (For Instructor Use Only) 17–41 PROBLEM 17-3 (a) Debt Investments (available-for-sale)……………….. 162,000* Equity Investments (available-for-sale) …………….. 37,400 Interest Revenue ($50,000 X .12 X 4/12) ……………. 2,000 […]

Chapter 17 Compute the unrealized gains or losses and prepare

Name: Date: Instructor: Course: Cost Fair Value Unrealized Gain (Loss) Amount Amount Formula Amount Amount Formula Amount Amount Formula Formula Formula Formula Amount Formula Amount Amount Securities Total of portfolio (c) Compute the unrealized gains or losses and prepare the […]

Chapter 17 Continuing Case Solution Judgment Necessary Assess The

Continuing Case Solution 7 Chapter 17 (a) 1. Stock investment in Infrared of 10% of the outstanding voting stock: DR CR Cash ($24,000 x 10%) 2,400 2. Stock investment in Infrared of 30% of the outstanding voting stock: DR CR […]

Chapter 17 Schedule of Interest Revenue and Bond Discount

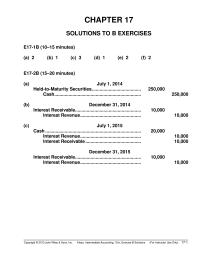

Interest Receivable…………………………………………… 10,000 Interest Revenue ……………………………………….. 10,000 (c) July 1, 2015 Cash ……………………………………………………………….. 20,000 Interest Revenue ……………………………………….. 10,000 Interest Receivable ……………………………………. 10,000 December 31, 2015 Interest Receivable…………………………………………… 10,000 Interest Revenue ……………………………………….. 10,000 CHAPTER 17 SOLUTIONS TO B EXERCISES E17-1B (10–15 […]

Chapter 17 The 20 Rule That Investment Direct Indirect

CHAPTER 17 Investments ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis 1. Debt securities. 1, 2, 3, 13 1 6 (a) Held-to-maturity. 4, 5, 7, 8, 10, 13, 21 1, 3 2, 3, 5 […]

Chapter 17 The Circumstances Leading The Decision Sell Transfer

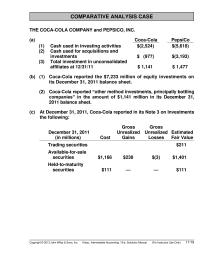

COMPARATIVE ANALYSIS CASE THE COCA-COLA COMPANY and PEPSICO, INC. (a) Coca-Cola PepsiCo (1) Cash used in investing activities $(2,524) $(5,618) (2) Cash used for acquisitions and investments $ (977) $(3,193) (3) Total investment in unconsolidated affiliates at 12/31/11 $ 1,141 […]

Chapter 17 The Entries Would The Same Except That

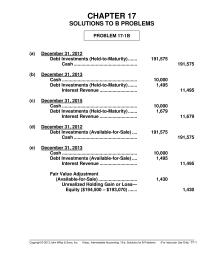

CHAPTER 17 SOLUTIONS TO B PROBLEMS PROBLEM 17-1B (a) December 31, 2012 Debt Investments (Held-to-Maturity) ……. 191,575 Cash …………………………………………. 191,575 (b) December 31, 2013 Cash …………………………………………………. 10,000 Debt Investments (Held-to-Maturity) ……. 1,495 Interest Revenue ……………………….. 11,495 (c) December 31, 2015 […]

Chapter 17 The Unrealized Holding Loss The Difference Between

Copyright © 2013 John Wiley & Sons, Inc. Kieso, Intermediate Accounting, 15/e, Solutions Manual (For Instructor Use Only) 17–61 *PROBLEM 17-15 (a) January 7, 2014 Put Option ……………………………………………………… 360 Cash ………………………………………………………… 360 (b) March 31, 2014 Put Option ……………………………………………………… 2,000 […]

Chapter 17 Variable rate Debt Variable Rate Debt Payment Debt

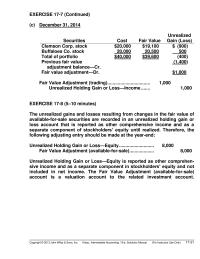

EXERCISE 17-7 (Continued) (c) December 31, 2014 Securities Cost Fair Value Unrealized Gain (Loss) Clemson Corp. stock $20,000 $19,100 ($ (900) Buffaloes Co. stock 20,000 20,500 ( 500) Total of portfolio $40,000 $39,600 ( (400) Previous fair value adjustment balance—Cr. […]

Chapter 17 reported as a separate component of stockholders’

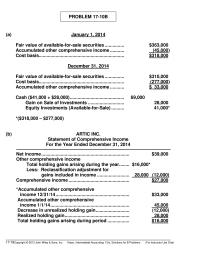

PROBLEM 17-10B (a) January 1, 2014 Fair value of available-for-sale securities …………… $363,000 Accumulated other comprehensive income ……….. (45,000) Cost basis………………………………………………………… $318,000 December 31, 2014 Fair value of available-for-sale securities …………… $310,000 Cost basis………………………………………………………… (277,000) Accumulated other comprehensive income ……….. […]

Chapter 18 Billings Construction Process Accounts Reported The Balance

Copyright © 2013 John Wiley & Sons, Inc. Kieso, Intermediate Accounting, 15/e, Solutions Manual (For Instructor Use Only) 18-1 CHAPTER 18 Revenue Recognition ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis sales transactions; high […]

Chapter 18 Deduct Contract Costs Incurred Loss Contract

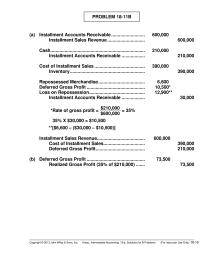

PROBLEM 18-11B (a) Installment Accounts Receivable …………………….. 600,000 Installment Sales Revenue ……………………….. 600,000 Cash ………………………………………………………………. 210,000 Installment Accounts Receivable ……………… 210,000 Cost of Installment Sales ………………………………… 390,000 Inventory …………………………………………………. 390,000 Repossessed Merchandise ……………………………… 6,600 Deferred Gross Profit ……………………………………… 10,500* Loss […]

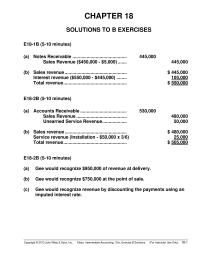

Chapter 18 Gee would recognize revenue by discounting

CHAPTER 18 SOLUTIONS TO B EXERCISES E18-1B (5-10 minutes) (a) Notes Receivable …………………………………… 445,000 Sales Revenue ($450,000 – $5,000) ……. 445,000 (b) Sales revenue ………………………………………… $ 445,000 Interest revenue ($550,000 – $445,000) …….. 105,000 Total revenue …………………………………………. $ 550,000 E18-2B […]

Chapter 18 Installment Accounts Receivables That Are Normally Treated

EXERCISE 18-7 (Continued) 2. 6/3 Accounts Receivable (Ann Mount) ………… 7,840 Sales Revenue [$8,000 – (2% X $8,000)] ………………. 7,840 6/5 Sales Returns and Allowances ……………… 588 Accounts Receivable (Ann Mount) [$600 – (2% X $600)] ……………………. 588 6/7 Delivery […]

Chapter 18 Revenue from disposing of assets other than products

Continuing Case Solution Chapter 18 (a) Memorandum To: Eric Conner and Phil Martin, CM2 From: L. Harbach Re: Revenue Recognition Date: February 2, 2013 The revenue recognition principle states that revenue should be recognized when the earnings process is complete, […]

Chapter 18 The actual freight costs are expenses made by

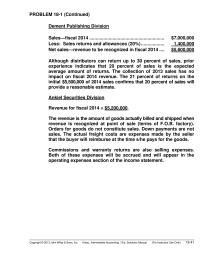

PROBLEM 18-1 (Continued) Dement Publishing Division Sales—fiscal 2014 …………………………………………………. $7,000,000 Less: Sales returns and allowances (20%) ……………… 1,400,000 Net sales—revenue to be recognized in fiscal 2014 …. $5,600,000 Although distributors can return up to 30 percent of sales, prior experience […]

Chapter 18 This Represents More Conservative Policy Light The

ACCOUNTING, ANALYSIS, AND PRINCIPLES (Continued) Principles Both methods attempt to report revenues that faithfully represent the operations of the company so that future earnings and cash flows can be predicted (relevance). With the percentage-of–completion method, companies use subjective estimates (based […]

Chapter 18 Unearned Franchise Fee Revenue From Franchise

CA 18-4 (Continued) a premium, the types of customers who receive credits, and the ease of exchanging credits for premiums will all affect the proportion of credits actually redeemed in relation to the potential redemptions. The difference between the five […]

Chapter 18 When Gross Profit Expressed Percentage Cost Must

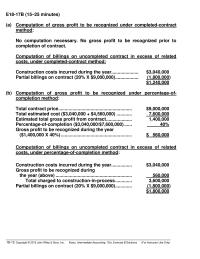

E18–17B (15–25 minutes) (a) Computation of gross profit to be recognized under completed-contract method: No computation necessary. No gross profit to be recognized prior to completion of contract. Computation of billings on uncompleted contract in excess of related costs, under […]

Chapter 18 An alternative valuation of the repossessed

PROBLEM 18-13 (Continued) Balance at repossession ………….. $360* Gross profit (40% X $360) ………… (144) Book value ……………………………… 216 Value of repossessed merchandise ……………………….. (100) Loss on repossession ……………… $116 *$30 X (20 payments – 8 payments) = $360 Copyright […]

Chapter 18 The disadvantage is that when the contract extends

CHAPTER 18 SOLUTIONS TO B PROBLEMS PROBLEM 18-1B (a) 1. The point of sale method recognizes revenue when the earnings process is complete and an exchange transaction has taken place. This can be the date goods are delivered, when title […]

Chapter 19 Deferred Tax Liability The Beginning 2013 Deferred

EXERCISE 19-8 (10–15 minutes) (a) 2014 Income Tax Expense ………………………………………. 336,000 Deferred Tax Asset ($20,000 X 40%) ………………… 8,000 Deferred Tax Liability ($30,000 X 40%) ……… 12,000 Income Taxes Payable ($830,000 X 40%) …… 332,000 2015 Income Tax Expense ………………………………………. […]

Chapter 19 Existing Contracts Firm Sales Backlog That Will

Continuing Case Solution Chapter 19 (a) Memorandum To: Eric Conner and Phil Martin, CM2 From: L. Harbach Re: Income Taxes Date: February 4, 2013 According to GAAP (see FASB ASC 740-10-05-05), the framework for the accounting for taxes is comprised […]

Chapter 19 Income Tax Expense Current Deferred Adjustment

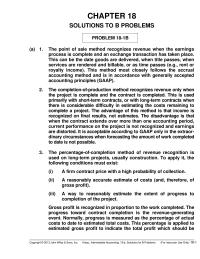

CHAPTER 19 SOLUTIONS TO B PROBLEMS PROBLEM 19-1B (a) X (0.30) = $270,000 taxes due for 2014 X = $270,000 ÷ 0.30 X = $900,000 taxable income for 2014 (b) Taxable income [from part (a)]………………………….. $900,000 Excess depreciation ………………………………………… 75,000 […]

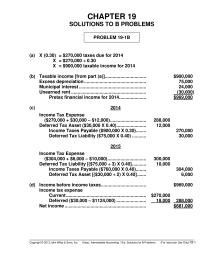

Chapter 19 Pretax financial income is equal to the taxable

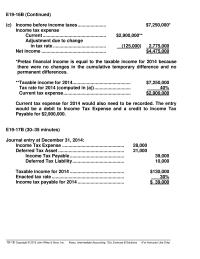

E19-16B (Continued) (c) Income before income taxes …………………. $7,250,000* Income tax expense Current …………………………………………. $2,900,000** Adjustment due to change in tax rate ………………………………….. (125,000) 2,775,000 Net income ………………………………………….. $4,475,000 *Pretax financial income is equal to the taxable income for 2014 […]

Chapter 19 Pretax Financial Income Nondeductible Expense Subtotal Taxable

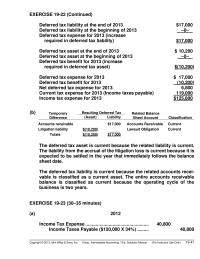

EXERCISE 19-22 (Continued) Deferred tax liability at the end of 2013 $17,000 Deferred tax liability at the beginning of 2013 –0– Deferred tax expense for 2013 (increase required in deferred tax liability) $17,000 Deferred tax asset at the end of […]

Chapter 19 Reduce The Deferred Tax Asset Valuation Allowance

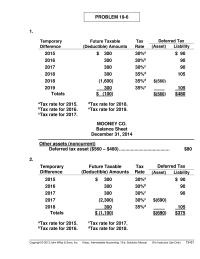

PROBLEM 19-6 1. Temporary Difference Future Taxable (Deductible) Amounts Tax Rate Deferred Tax (Asset) Liability 2015 $ 300 30%a $ 90 2016 300 30%b 90 2017 300 30%c 90 2018 300 35%d 105 2018 (1,600) 35%d $(560) 2019 300 35%e […]

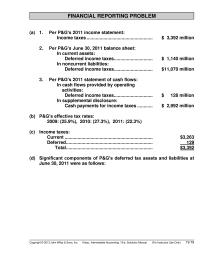

Chapter 19 Significant components of P&G’s deferred tax assets

FINANCIAL REPORTING PROBLEM (a) 1. Per P&G’s 2011 income statement: Income taxes …………………………………………… $ 3,392 million 2. Per P&G’s June 30, 2011 balance sheet: In current assets: Deferred income taxes ………………………… $ 1,140 million In noncurrent liabilities: Deferred income taxes […]

Chapter 19 Temporary difference resulting in future deductible

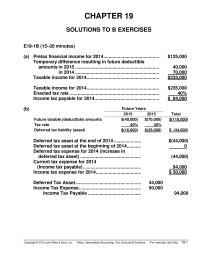

CHAPTER 19 SOLUTIONS TO B EXERCISES E19-1B (15–20 minutes) (a) Pretax financial income for 2014 ……………………………………. $125,000 Temporary difference resulting in future deductible amounts in 2015 ……………………………………………………….. 40,000 in 2014 ……………………………………………………….. 70,000 Taxable income for 2014 ……………………………………………….. $235,000 Taxable income […]

Chapter 19 the amount of cumulative temporary difference existing

PROBLEM 19-5B (Continued) (c) 2014 Income Statement Operating loss before income taxes …………… $(140,000) Income tax benefit Benefit due to loss carryback ……………… $21,000 Benefit due to loss carryforward …………. 25,500 46,500 Net loss ……………………………………………………. $(93,500) (d) 2016 Income Statement […]

Chapter 19 Reconcile pretax financial income with taxable income

CHAPTER 19 Accounting for Income Taxes ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis 1. Reconcile pretax financial income with taxable income. 1, 13 1, 2, 3, 4, 5, 12, 18, 20, 21 1, […]

Chapter 2 Both Relevance And Faithful Representation Are Considered

Continuing Case Solution Chapter 2 Memorandum To: Eric Conner and Phil Martin, CM Corporation From: L. Harbach Re: Elements of FASB Conceptual Framework Date: January 4, 2013 (a) The objective of financial reporting is to provide financial information that is […]

Chapter 2 Examples Costs That Should Treated Measures Assets

Copyright © 2013 John Wiley & Sons, Inc. Kieso, Intermediate Accounting, 15/e, Solutions Manual (For Instructor Use Only) 2-21 TIME AND PURPOSE OF CONCEPTS FOR ANALYSIS CA 2-1 (Time 20–25 minutes) Purpose—to provide the student with the opportunity to comment […]

Chapter 2 Examples Include Officers Salaries Most Selling Costs

CHAPTER 2 Conceptual Framework for Financial Reporting ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Concepts for Analysis 1. Conceptual framework– general. 1, 7 1, 2 2. Objective of financial reporting. 2 1, 2 3 3. Qualitative characteristics […]

Chapter 2 The Expense Recognition Principle Indicates That Expenses

and therefore must rely, at least partly, on the information in financial reports. (c) False – Standard-setting that is based on personal conceptual frameworks will lead to different conclusions about identical or similar issues. As a result, standards will not […]

Chapter 2 Those Relationships Are Sometimes Collectively Referred Articulation

COMPARATIVE ANALYSIS CASE (Continued) Pepsi Inventory In the first quarter of 2011, Quaker Foods North America (QFNA) changed its method of accounting for certain U.S. inventories from the last-in, first-out (LIFO) method to the average cost method. This change is […]

Chapter 20 Accumulated other comprehensive loss

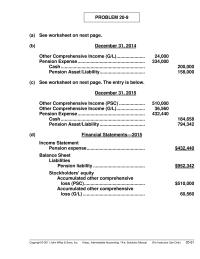

PROBLEM 20-9 (a) See worksheet on next page. (b) December 31, 2014 Other Comprehensive Income (G/L) …………………. 24,000 Pension Expense ……………………………………………. 334,000 Cash ……………………………………………………….. 200,000 Pension Asset /Liability …………………………….. 158,000 (c) See worksheet on next page. The entry is below. […]

Chapter 20 Because the amount of net gain or loss does not exceed

Time and Purpose of Problems (Continued) Problem 20-12 (Time 35–45 minutes) Purpose—to provide a problem that requires preparation of a worksheet, journal entries, and indicates financial statement presentation. *Problem 20-13 (Time 30–35 minutes) Purpose—to provide a problem that requires preparation […]

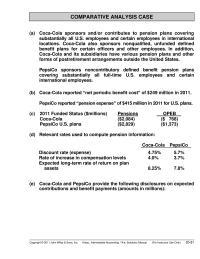

Chapter 20 Coca-Cola sponsors and/or contributes to pension

COMPARATIVE ANALYSIS CASE (a) Coca-Cola sponsors and/or contributes to pension plans covering substantially all U.S. employees and certain employees in international locations. Coca-Cola also sponsors nonqualified, unfunded defined benefit plans for certain officers and other employees. In addition, Coca-Cola and […]

Chapter 20 Continuing Case Solution B Memorandum To Eric

Continuing Case Solution 25 Chapter 20 (a) Memorandum To: Eric Conner and Phil Martin, CM2 From: L. Harbach Re: Postretirement Pension Benefits Date: February 10, 2013 Defined benefit pension plans are so-named because the benefit provided to the employee is […]

Chapter 20 Expected Future Years Service Average Remaining Service

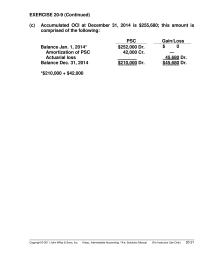

EXERCISE 20-9 (Continued) (c) Accumulated OCI at December 31, 2014 is $255,680; this amount is comprised of the following: PSC Gain/Loss Balance Jan. 1, 2014* $252,000 Dr. $ 0 Amortization of PSC 42,000 Cr. — Actuarial loss 45,680 Dr. Balance […]

Chapter 20 Note to financial statements disclosing components

CHAPTER 20 SOLUTIONS TO B EXERCISES E20-1B (5–10 minutes) (a) Computation of pension expense: Service cost ………………………………………………… $250,000 Interest cost ($2,600,000 X 0.08) …………………… 208,000 Actual (expected) return on plan assets ……….. (65,000) Prior service cost amortization …………………….. 40,000 Pension […]

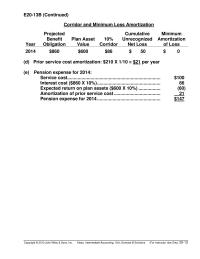

Chapter 20 The excess of the cumulative net gain or loss

E20-13B (Continued) Corridor and Minimum Loss Amortization Year Projected Benefit Obligation Plan Asset Value 10% Corridor Cumulative Unrecognized Net Loss Minimum Amortization of Loss 2014 $860 $600 $86 $ 50 $ 0 (d) Prior service cost amortization: $210 X 1/10 […]

Chapter 20 Unexpected Gain Amortization Contributions Benefits Increase

PROBLEM 20-7B MANGROVE CORP. Pension Worksheet—2014 General Journal Entries Memo Record Items Annual Pension Expense Cash OCI—Prior Service Cost OCI— Gain/Loss Pension Asset / Liability Projected Benefit Obligation Plan Assets Balance, Jan. 1, 2014 160,000 Cr. 520,000 Cr. 360,000 Dr. […]

Chapter 21 Cost Fair Market Value Leased Asset

CHAPTER 21 SOLUTIONS TO B EXERCISES E21-1B (15–20 minutes) (a) This is a capital lease to Manor since the lease term (6 years) is greater than 75% of the economic life (6 years) of the leased asset. The lease term […]

Chapter 21 Current Liabilities Lease Liability Interest Payable

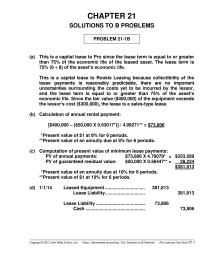

CHAPTER 21 SOLUTIONS TO B PROBLEMS PROBLEM 21-1B (a) This is a capital lease to Pro since the lease term is equal to or greater than 75% of the economic life of the leased asset. The lease term is 75% […]

Chapter 21 One The First Areas Studied Is What

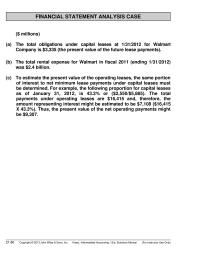

FINANCIAL STATEMENT ANALYSIS CASE ($ millions) (a) The total obligations under capital leases at 1/31/2012 for Walmart Company is $3,335 (the present value of the future lease payments). (b) The total rental expense for Walmart in fiscal 2011 (ending 1/31/2012) […]

Chapter 21 The Amount Capitalized Represents The Completed Service

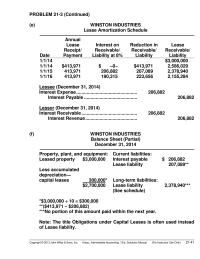

PROBLEM 21-3 (Continued) (e) WINSTON INDUSTRIES Lease Amortization Schedule Date Annual Lease Receipt/ Payment Interest on Receivable/ Liability at 8% Reduction in Receivable/ Liability Lease Receivable/ Liability 1/1/14 $3,000,000 1/1/14 $413,971 $ –0– $413,971 2,586,029 1/1/15 413,971 206,882 207,089 2,378,940 […]

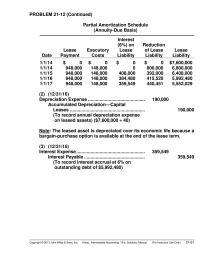

Chapter 21 The Cost The Lease Matched With Revenue

PROBLEM 21-12 (Continued) Partial Amortization Schedule (Annuity-Due Basis) Date Lease Payment Executory Costs Interest (6%) on Lease Liability Reduction of Lease Liability Lease Liability 1/1/14 $ 0 $ 0 $ 0 $ 0 $7,600,000 1/1/14 948,000 148,000 0 800,000 6,800,000 […]

Chapter 21 The Lease Accounted For Properly Capital Lease

Extensive detail and information is contained within the help function of Microsoft Excel and in the provided text. You should enter your name, date, instructor’s name, and course into the cells at the top of the page. This information will […]

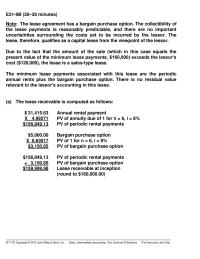

Chapter 21 The lease agreement has a bargain purchase option

E21-9B (20–30 minutes) Note: The lease agreement has a bargain purchase option. The collectibility of the lease payments is reasonably predictable, and there are no important uncertainties surrounding the costs yet to be incurred by the lessor. The lease, therefore, […]

Chapter 21 The lease agreement has a bargain-purchase option

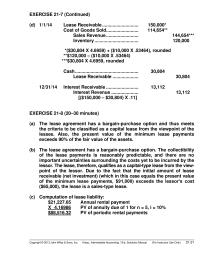

EXERCISE 21-7 (Continued) (d) 1/1/14 Lease Receivable ………………………. 150,000* Cost of Goods Sold……………………. 114,654** Sales Revenue ……………………. 144,654*** Inventory ……………………………. 120,000 * *($30,804 X 4.6959) + ($10,000 X .53464), rounded **$120,000 – ($10,000 X .53464) ***$30,804 X 4.6959, rounded Cash […]

Chapter 21 The Same Time There Increase Liabilities

Continuing Case Solution 29 Chapter 21 (a) Memorandum To: Eric Conner and Phil Martin, CM2 From: L. Harbach Re: Leases Date: February 13, 2013 According to FASB ASC 840-10-25-1, the lease proposal offered by Tyler Leasing Company meets at least […]

Chapter 21 Walker Company Can Use The Sales type Lease

CHAPTER 21 Accounting for Leases ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis *1. Rationale for leasing. 1, 2, 4 1, 2 *2. Lessees; classification of leases; accounting by lessees. 3, 5, 7, 8, […]

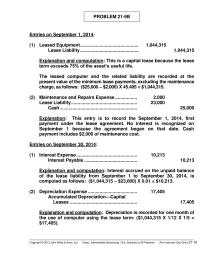

Chapter 21 Depreciation is recorded for one month of the use

PROBLEM 21-9B Entries on September 1, 2014: (1) Leased Equipment ……………………………………… 1,044,315 Lease Liability ……………………………………… 1,044,315 Explanation and computation: This is a capital lease because the lease term exceeds 75% of the asset’s useful life. The leased computer and the […]

Chapter 22 A change in the experience rate is considered a change

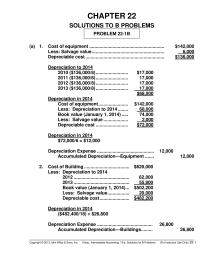

CHAPTER 22 SOLUTIONS TO B PROBLEMS PROBLEM 22-1B (a) 1. Cost of equipment …………………………………………………. $142,000 Less: Salvage value ……………………………………………….. 6,000 Depreciable cost ……………………………………………………. $136,000 Depreciation to 2014 2010 ($136,000/8) ……………………. $17,000 2011 ($136,000/8) ……………………. 17,000 2012 ($136,000/8) ……………………. 17,000 2013 […]

Chapter 22 Bond interest expense for 2014 and 2015 was computed

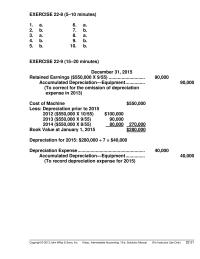

EXERCISE 22-8 (5–10 minutes) 1. a. 6. a. 2. b. 7. b. 3. a. 8. a. 4. b. 9. b. 5. b. 10. b. EXERCISE 22-9 (15–20 minutes) December 31, 2015 Retained Earnings ($550,000 X 9/55) ………………………. 90,000 Accumulated Depreciation—Equipment […]

Chapter 22 Commission The Staff Believes That This Disclosure

FINANCIAL REPORTING PROBLEM (a) New Accounting Pronouncements and Policies Derivative Instruments and Hedging Activites On January 1, 2009 we adopted new accounting guidance on disclosures about derivative instruments and hedging activities. The new guidance impacted disclosures only and requires additional […]

Chapter 22 GAAP requires that all research and development costs

PROBLEM 22-7B (Continued) (9) Insurance Expense ($6,000 ÷ 2) ………………………………….. 3,000 Prepaid Insurance ($3,000 X 9/12) ………………………………. 2,250 Retained Earnings ……………………………………………… 5,250 (10) Amortization Expense ($210,000 ÷ 12) ………………………… 17,500 Retained Earnings …………………………………………………….. 17,500 Trademarks ……………………………………………………….. 35,000 22–12Copyright © 2013 […]

Chapter 22 Process Deferred Tax Liability Retained

Copyright © 2013 John Wiley & Sons, Inc. Kieso, Intermediate Accounting, 15/e, Exercise B Solutions (For Instructor Use Only) 22-1 *($105,000 + $70,000 + $150,000) – ($120,000 + $80,000 + $165,000) (b) Net income (average-cost) 2012 $105,000 2013 70,000 2014 […]

Chapter 22 the Company changed its method of pricing inventory from

PROBLEM 22-5 (Continued) In 2014, the Company changed its method of pricing inventory from the last-in, first out (LIFO) to the average cost method in order to more fairly present the financial operations of the company. The financial statements for […]

Chapter 22 This Change Represents Change Reporting Entity This

CHAPTER 22 Accounting Changes and Error Analysis ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis 1. Differences between change in principle, change in estimate, change in entity, errors. 2, 4, 6, 7, 8, 9, […]

Chapter 22 Excel File Solution Note to instructor

Continuing Case Solution 32 Chapter 22 Excel File Solution Note to instructor As an extension to the chapter 22 exercise, you could add the following requirement: Prepare the correcting entries to be made in 2013, and record the information on […]

Chapter 23 Adjustments Reconcile Net Income Net Cash Provided

CHAPTER 23 Statement of Cash Flows ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis 1. Format, objectives purpose, and source of statement. 1, 2, 7, 8, 12 1, 2, 5, 6 2. Classifying investing, […]

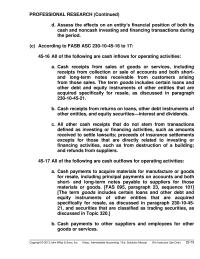

Chapter 23 All of the following are cash outflows for operating

PROFESSIONAL RESEARCH (Continued) d. Assess the effects on an entity’s financial position of both its cash and noncash investing and financing transactions during the period. (c) According to FASB ASC 230-10–45-16 to 17: 45–16 All of the following are cash […]

Chapter 23 Cash Dividends Paid Payment Notes Payable Issuance

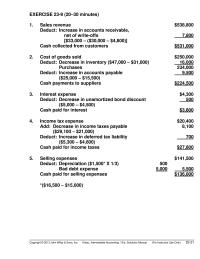

EXERCISE 23-9 (20–30 minutes) 1. Sales revenue $538,800 Deduct: Increase in accounts receivable, net of write-offs [$33,000 – ($30,000 – $4,800)] 7,800 Cash collected from customers $531,000 2. Cost of goods sold $250,000 Deduct: Decrease in inventory ($47,000 – $31,000) […]

Chapter 23 Cost Goods Sold Add Ending Inventory

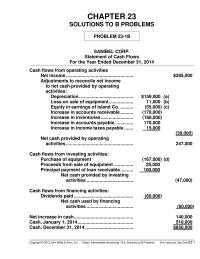

CHAPTER 23 SOLUTIONS TO B PROBLEMS PROBLEM 23-1B SANIBEL CORP. Statement of Cash Flows For the Year Ended December 31, 2014 Cash flows from operating activities Net income ……………………………………………. $285,000 Adjustments to reconcile net income to net cash provided by […]

Chapter 23 Depreciation Expense Gain Sale Investments

PROBLEM 23-2 (Continued) Supplemental disclosures of cash flow information: Cash paid during the year for: Interest $2,000 Income taxes: $6,500 Noncash investing and financing activities Retired notes payable by issuing common stock $10,000 Purchased equipment by issuing notes payable 16,000 […]

Chapter 23 Examples Noncash Transactions Are The Conversion Debt

SOLUTIONS TO CONCEPTS FOR ANALYSIS CA 23-1 (a) The main purpose of the statement of cash flows is to show the change in cash from one period to the next. Another objective of a statement of the type shown is […]

Chapter 23 Other Expenses Less Decrease Prepaid Expenses

PROBLEM 23-5B (Continued) (3) Funds to redeem bonds ($300,000 X 1.01) ……….. $303,000 Face value of bonds ……………………………………….. $300,000 Unamortized discount 12/31/13 ……………………….. $6,075 Amortization to 5/31/14 not requiring cash ($9,000 ÷ 40) X 5/12 ……………………………………… 94 Balance at date […]

Chapter 23 The Indirect Method Uses Net Income The

Continuing Case Solution Chapter 23 Memorandum To: Eric Conner and Phil Martin, CM2 From: L. Harbach Re: Statement of Cash Flows Date: February 18, 2013 Here are my responses to your questions about the statement of cash flows: 1. The […]

Chapter 23 The sale of treasury stock is reported in the financing

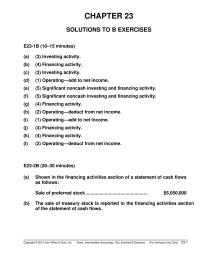

CHAPTER 23 SOLUTIONS TO B EXERCISES E23-1B (10–15 minutes) (a) (3) Investing activity. (b) (4) Financing activity. (c) (3) Investing activity. (d) (1) Operating—add to net income. (e) (5) Significant noncash investing and financing activity. (f) (5) Significant noncash investing […]

Chapter 23 Adjustments to reconcile net income to net cash

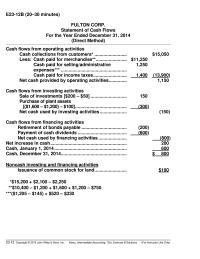

E23-12B (20–30 minutes) FULTON CORP. Statement of Cash Flows For the Year Ended December 31, 2014 (Direct Method) Cash flows from operating activities Cash collections from customers* ……………………. $15,050 Less: Cash paid for merchandise**…………………… $11,250 Cash paid for selling/administrative expenses*** […]

Chapter 24 Cost Goods Sold Increases Rate 1915 Despite

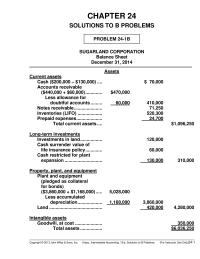

CHAPTER 24 SOLUTIONS TO B PROBLEMS PROBLEM 24-1B Accounts receivable ($440,000 + $60,000) …………. $470,000 Less allowance for doubtful accounts ……… 60,000 410,000 Notes receivable …………………. 71,250 Inventories (LIFO) ………………. 520,300 Prepaid expenses ……………….. 24,700 Total current assets …. $1,096,250 […]

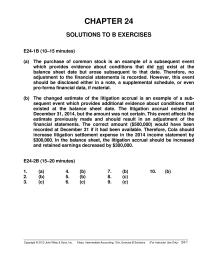

Chapter 24 Fraudulent Financial Reporting Usually Occurs The Result

CHAPTER 24 Full Disclosure in Financial Reporting ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis * 1. The disclosure principle; type of disclosure. 2, 3 1, 2, 3 * 2. Role of notes that […]

Chapter 24 The Companys Net Investment Plant And Equipment

balance sheet date but arose subsequent to that date. Therefore, no adjustment to the financial statements is recorded. However, this event should be disclosed either in a note, a supplemental schedule, or even pro-forma financial data, if material. December 31, […]

Chapter 24 The concept underlying the integral approach

ACCOUNTING, ANALYSIS, AND PRINCIPLES (Continued) Analysis Profit margin on sales = Net income ÷ Net sales Integral approach: 1st Quarter 2nd Quarter 3rd Quarter 4th Quarter Net income (Loss) $100,000 $187,500 $687,500 $150,000 Net sales 320,000 600,000 2,200,000 480,000 Profit […]

Chapter 24 The Student Required Evaluate Each Example And

SOLUTIONS TO PROBLEMS PROBLEM 24-1 ALMADEN CORPORATION Balance Sheet December 31, 2014 Assets Current assets Cash ($571,000 – $300,000) …. $ 271,000 Accounts receivable ($480,000 + $30,000) …………. $510,000 Less allowance for doubtful accounts ……… 30,000 480,000 Notes receivable …………………. […]

Chapter 24 Snacks And Pet Care Fabric Care And

CA 24-8 (Continued) 2. The company’s revenue and expenses would be reported as follows on its quarterly report prepared for the first quarter of the 2014–2015 fiscal year: Sales revenue ………………………………………………………………………………. $60,000,000 Cost of goods sold ………………………………………………………………………… 36,000,000 Variable selling […]

Chapter 3 Accumulated Depreciation Equipment Interest Expense

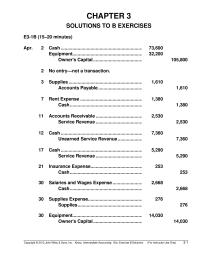

CHAPTER 3 SOLUTIONS TO B EXERCISES E3-1B (15–20 minutes) Apr. 2 Cash ………………………………………………………. 73,600 Equipment………………………………………………………. 32,200 Owner’s Capital ………………………………………………………. 105,800 2 No entry—not a transaction. 3 Supplies ………………………………………………………. 1,610 Accounts Payable ………………………………………………………. 1,610 7 Rent Expense ………………………………………………………. 1,380 Cash ………………………………………………………. […]

Chapter 3 Alternate Solution June Murray Md Conversion Income

E3-12B (20–25 Minutes) (a) COMP CORP. Income Statement For the Year Ended December 31, 2014 Revenues Service revenue ………………………………………. $53,600 Expenses Salaries and wages expense ……………………. $25,600 Rent expense ………………………………………….. 8,000 Supplies expense ……………………………………. 7,100 Depreciation expense ………………………….. 2,500 Interest […]

Chapter 3 Jurassic Park Co Worksheet Partial For Month

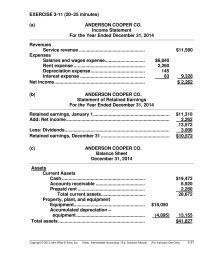

EXERCISE 3-11 (20–25 minutes) (a) ANDERSON COOPER CO. Income Statement For the Year Ended December 31, 2014 Revenues Service revenue ……………………………………………… $11,590 Expenses Salaries and wages expense ………………………….. $6,840 Rent expense …………………………..…………………….. 2,260 Depreciation expense ……………………………………… 145 Interest expense …………………………………………….. […]

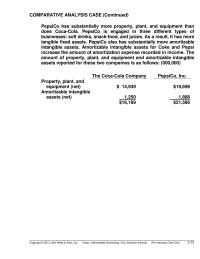

Chapter 3 PepsiCo is engaged in three different types of businesses

COMPARATIVE ANALYSIS CASE (Continued) PepsiCo has substantially more property, plant, and equipment than does Coca-Cola. PepsiCo is engaged in three different types of businesses: soft drinks, snack-food, and juices. As a result, it has more tangible fixed assets. PepsiCo also […]

Chapter 3 Service Revenue, Salaries and Wages Expense

PROBLEM 3-3 1. Dec. 31 Salaries and Wages Expense ………………………….. 2,120 Salaries and Wages Payable ………………………….. 2,120 (5 X $700 X 2/5) = $1,400 (3 X $600 X 2/5) = 720 Total accrued salaries $2,120 2. 31 Unearned Rent Revenue […]

Chapter 3 The Accrual Basis Accounting Allows External Based

Continuing Case Solution Chapter 3 Memorandum To: Eric Conner and Phil Martin, CM From: L. Harbach Re: Adjusting Entries and Accrual Accounting Date: January 5, 2013 At the end of the year, it is critical to perform adjusting entries to […]

Chapter 3 The cost of computers and printers sold in January

PROBLEM 3-10 (a), (b), (c) Cash Accounts Receivable Allow. for Doubtful Accts. Bal. 18,500 Bal. 32,000 Bal. 700 Adj. 1,400 2,100 Inventory Equipment Accum. Depr.—Equipment Bal. 80,000 Bal. 84,000 Bal. 35,000 Adj. 12,000 47,000 Prepaid Insurance Notes Payable Interest Expense […]

Chapter 3 Explain the reasons for preparing adjusting entries and identify

CHAPTER 3 The Accounting Information System ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems 1. Transaction identification. 1, 2, 3, 5, 6, 7, 8 1, 2 1, 2, 3, 4, 17 1 2. Nominal accounts. 4, 7 […]

Chapter 3 Liabilities and Stockholders’ Equity Current liabilities

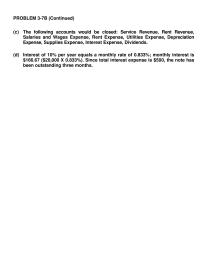

PROBLEM 3-7B (Continued) (c) The following accounts would be closed: Service Revenue, Rent Revenue, Salaries and Wages Expense, Rent Expense, Utilities Expense, Depreciation Expense, Supplies Expense, Interest Expense, Dividends. (d) Interest of 10% per year equals a monthly rate of […]

Chapter 3 Operating expenses Selling expenses Salaries and wages expense

PROBLEM 3-1B (a) (Explanations are omitted.) and (d) Cash Equipment Mar. 1 50,000 Mar. 3 1,500 Mar. 2 22,800 10 850 4 1,165 26 2.600 21 7,600 23 3,000 Owner’s Capital 31 2,500 Mar. 23 3,000 Mar. 1 50,000 31 […]

Chapter 4 A Loss Discontinued Operations Reported Net

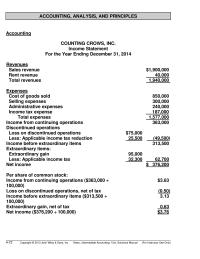

ACCOUNTING, ANALYSIS, AND PRINCIPLES Accounting COUNTING CROWS, INC. Income Statement For the Year Ending December 31, 2014 Revenues Sales revenue $1,900,000 Rent revenue 40,000 Total revenues 1,940,000 Expenses Cost of goods sold 850,000 Selling expenses 300,000 Administrative expenses 240,000 Income […]

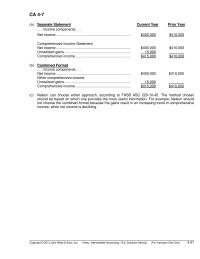

Chapter 4 A Separate Statement Current Year Income

CA 4-7 (a) Separate Statement Current Year Prior Year . . . income components . . . Net income …………………………………………………………………. $400,000 $410,000 Comprehensive Income Statement Net income …………………………………………………………………. $400,000 $410,000 Unrealized gains ………………………………………………………….. 15,000 Comprehensive income ………………………………………………… $415,000 $410,000 (b) […]

Chapter 4 Another Treatment Show The Other Revenues And

CHAPTER 4 Income Statement and Related Information ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis 1. Income measurement concepts. 1, 2, 3, 4, 5, 6, 7, 8, 9, 10, 18, 22, 23, 30, 33, […]

Chapter 4 Correction Depreciation Overstatement Net Tax Retained

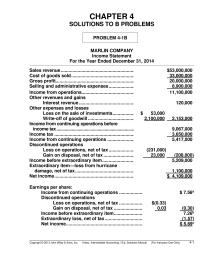

CHAPTER 4 SOLUTIONS TO B PROBLEMS PROBLEM 4-1B MARLIN COMPANY Income Statement For the Year Ended December 31, 2014 Sales revenue ………………………………………………………… $53,000,000 Cost of goods sold …………………………………………………. 33,000,000 Gross profit ……………………………………………………………. 20,000,000 Selling and administrative expenses ……………………….. 8,900,000 Income […]

Chapter 4 Earnings Per Share Income From Continuing Operations

CHAPTER 4 SOLUTIONS TO B EXERCISES E4-1B (18–20 minutes) Computation of net income Change in assets: $252,800 + $144,000 + $406,400 – $150,400 = $652,800 Increase Change in liabilities: $ 262,400 – $163,200 = 99,200 Increase Change in stockholders’ equity: […]

Chapter 4 File Entries Decrease Sales Je Account Name

Continuing Case Solution Chapter 4 (a) Ratio Discussion 2011 2012 2013 Gross margin** / Sales $4,159,057 / $9,960,712 = 0.4176 $4,107,670 / $9,994,329 = 0.4110 $3,725,000 / $9,575,000 = 0.3890 ** Gross margin is also called gross profit. Ratio Analysis: […]

Chapter 4 Income attributed to controlling stockholders

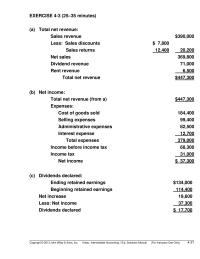

EXERCISE 4-3 (25–35 minutes) (a) Total net revenue: Sales revenue $390,000 Less: Sales discounts $ 7,800 Sales returns 12,400 20,200 Net sales 369,800 Dividend revenue 71,000 Rent revenue 6,500 Total net revenue $447,300 (b) Net income: Total net revenue (from […]

Chapter 4 The student must determine through analysis the ending

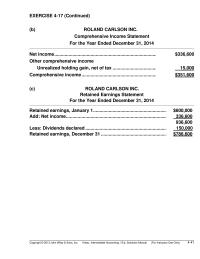

EXERCISE 4-17 (Continued) (b) ROLAND CARLSON INC. Comprehensive Income Statement For the Year Ended December 31, 2014 Net income ……………………………………………………………………… $336,600 Other comprehensive income Unrealized holding gain, net of tax ……………………………… 15,000 Comprehensive income …………………………………………………… $351,600 (c) ROLAND CARLSON INC. […]

Chapter 5 Could There Earnings Management Going On Net

Continuing Case Solution Chapter 5 Part I: Analysis of Balance Sheet and Cash Flows (a) Liquidity and Solvency Ratios 2011 2012 2013 Liquidity Ratios: Current Ratio = Current assets / Current liabilities $1,483,062 / $845,198 = 1.7547 $2,126,086 / $1,722,962 […]

Chapter 5 Net Cash Used Investing Activities Net Cash

SOLUTIONS TO CONCEPTS FOR ANALYSIS CA 5-1 1. The new estimate would be used in computing depreciation expense for 2014. No adjustment of the balance in accumulated depreciation at the beginning of the year would be made. Instead, the remaining […]

Chapter 5 Some Companies Report The Subtotal Net Assets

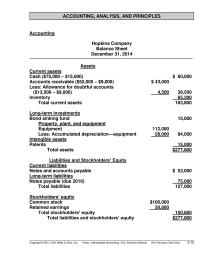

ACCOUNTING, ANALYSIS, AND PRINCIPLES Accounting Hopkins Company Balance Sheet December 31, 2014 Assets Current assets Cash ($75,000 – $15,000) $ 60,000 Accounts receivable ($52,000 – $9,000) $ 43,000 Less: Allowance for doubtful accounts ($13,500 – $9,000) 4,500 38,500 Inventory 65,300 […]

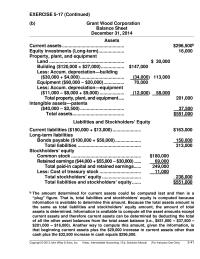

Chapter 5 The amount determined for current assets could be computed

EXERCISE 5-17 (Continued) (b) Grant Wood Corporation Balance Sheet December 31, 2014 Assets Current assets ………………………………………… $296,500b Equity investments (Long-term) ……………….. 16,000 Property, plant, and equipment Land …………………………………………………. $ 30,000 Building ($120,000 + $27,000) ……………… $147,000 Less: Accum. depreciation—building ($30,000 […]

Chapter 5 Thus Separating Longterm Assets From Current Assets

CHAPTER 5 Balance Sheet and Statement of Cash Flows ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis 1. Disclosure principles, uses of the balance sheet, financial flexibility. 1, 2, 3, 4, 5, 6, 7, […]

Chapter 5 When the company accounts for the treasury stock

CHAPTER 5 SOLUTIONS TO B EXERCISES E5-1B (15–20 minutes) (a) Current asset. (b) Current asset. (c) If the investment in preferred stock is readily marketable and held with the intention of converting the stock to cash if the need should […]

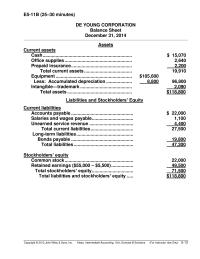

Chapter 5 Which would be disclosed in notes accompanying

E5-11B (25–30 minutes) DE YOUNG CORPORATION Balance Sheet December 31, 2014 Assets Current assets Cash …………………………………………………………… $ 15,070 Office supplies ……………………………………………. 2,640 Prepaid insurance ……………………………………….. 2,200 Total current assets ………………………………. 19,910 Equipment ………………………………………………….. $105,600 Less: Accumulated depreciation ……………….. 8,800 96,800 […]

Chapter 5 An assumption made here is that cash included the restricted

EXERCISE 5-4 (30–35 minutes) Denis Savard Inc. Balance Sheet December 31, 20– Assets Current assets Cash …………………………………………………… $XXX Less: Cash restricted for plant expansion ……………………………………. XXX $XXX Accounts receivable ……………………………. XXX Less: Allowance for doubtful accounts ……………………………………… XXX XXX Notes […]

Chapter 5 the cash restricted for plant expansion would be added

CHAPTER 5 SOLUTIONS TO B PROBLEMS PROBLEM 5-1B COMPANY NAME Balance Sheet December 31, 20XX Assets Current assets Cash on hand (including petty cash) …………. $XXX Cash in bank ……………………………………………. XXX $XXX Debt investments (trading) ……………………….. XXX Accounts receivable ………………………………… […]

Chapter 6 Anita Will Retire Years After Deposits Stop

PROBLEM 6-10 1. Purchase. Time diagrams: Installments i = 10% PV – OA = ? R = $350,000 $350,000 $350,000 $350,000 $350,000 0 1 2 3 4 5 n = 5 Property taxes and other costs i = 10% PV […]

Chapter 6 Bid A should be accepted since its present value

PROBLEM 6-2 (a) Time diagram: i = 8% FV – OA = $90,000 R R R R R R R R R = ? ? ? ? ? ? ? ? 0 1 2 3 4 5 6 7 8 […]

Chapter 6 Given no established value for the building

CHAPTER 6 Accounting and the Time Value of Money SOLUTIONS TO B PROBLEMS PROBLEM 6-1B (a) Given no established value for the building, the fair market value of the note would be estimated to value the building. Time diagram: i […]

Chapter 6 The stamping machine should be purchased from Vendor

PROBLEM 6-8B Vendor A: $ 50,000 payment X 3.99271 (PV of ordinary annuity 8%, 5 periods) $ 199,636 + 40,000 down payment + 47,000 maintenance contract $ 286,636 total cost from Vendor A Vendor B: $ 14,000 semiannual payment X […]

Chapter 6 The unknown interest rate is calculated by first dividing

CHAPTER 6 SOLUTIONS TO B EXERCISES E6-1B (5–10 minutes) Rate of Interest Number of Periods 1. a. 8% 8 b. 4% 40 c. 5% 20 2. a. 8% 25 b. 6% 30 c. 4% 28 E6-2B (5–10 minutes) (a) Simple […]

Chapter 6 These Concepts Are Applied The Following Areas

CHAPTER 6 Accounting and the Time Value of Money ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems 1. Present value concepts. 1, 2, 3, 4, 5, 9, 17 2. Use of tables. 13, 14 8 1 3. […]

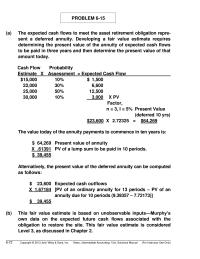

Chapter 6 This fair value estimate is based on unobservable

PROBLEM 6-15 (a) The expected cash flows to meet the asset retirement obligation repre- sent a deferred annuity. Developing a fair value estimate requires determining the present value of the annuity of expected cash flows to be paid in three […]

Chapter 6 Present value of an ordinary annuity

SOLUTIONS TO EXERCISES EXERCISE 6-1 (5–10 minutes) (a) (b) Rate of Interest Number of Periods 1. a. 9% 9 b. 3% 20 c. 5% 30 2. a. 9% 25 b. 5% 30 c. 3% 28 EXERCISE 6-2 (5–10 minutes) (a) […]

Chapter 7 Allowance For Doubtful Accounts Receivable

TIME AND PURPOSE OF PROBLEMS Problem 7-1 (Time 20–25 minutes) Purpose—to provide the student with an understanding of the balance sheet effect that occurs when the cash book is left open. In addition, the student is asked to adjust the […]

Chapter 7 Assumes that the purchase of the inventory was recorded

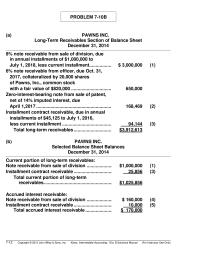

PROBLEM 7-10B (a) PAWNS INC. Long-Term Receivables Section of Balance Sheet December 31, 2014 8% note receivable from sale of division, due in annual installments of $1,000,000 to July 1, 2018, less current installment…………….. $ 3,000,000 (1) 6% note receivable […]

Chapter 7 Failure Debtors Pay When Due The Effects

FINANCIAL STATEMENT ANALYSIS CASE 1 (Continued) (e) Occidental would record a loss of $30,000,000 as revealed in the following entry to record the transaction: Cash………………………………………………………. 345,000,000 Loss on Sale of Receivables ………………………….. 30,000,000 Accounts Receivable ………………………….. 360,000,000 Recourse Liability ………………………….. […]

Chapter 7 Less Recourse Obligation Net Proceeds

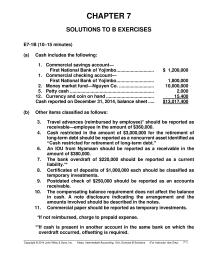

CHAPTER 7 SOLUTIONS TO B EXERCISES E7-1B (10–15 minutes) (a) Cash includes the following: 1. Commercial savings account— First National Bank of Yojimbo ……………………….. $ 1,200,000 1. Commercial checking account— First National Bank of Yojimbo ……………………….. 1,800,000 2. Money market […]

Chapter 7 The accrual-based accounting system under GAAP

Continuing Case Solution Chapter 7 Part I Memorandum To: Eric Conner and Phil Martin, CM2 From: L. Harbach Re: Bad Debt Expense Date: January 9, 2013 The accrual-based accounting system under GAAP requires that revenues and expenses be matched in […]

Chapter 7 This classification assumes that these receivables

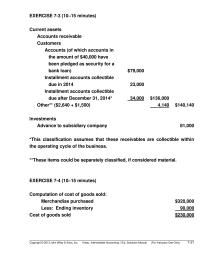

EXERCISE 7-3 (10–15 minutes) Current assets Accounts receivable Customers been pledged as security for a bank loan) $79,000 Installment accounts collectible due in 2014 23,000 Installment accounts collectible due after December 31, 2014* 34,000 $136,000 Other** ($2,640 + $1,500) 4,140 […]

Chapter 7 This material is covered in an Appendix to the chapter.

CHAPTER 7 Cash and Receivables ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis 1. Accounting for cash. 1, 2, 3, 4, 22 1 1, 2 1 2. Accounting for accounts receivable, bad debts, other […]

Chapter 7 Thus The Difference Between The Cash Received

*PROBLEM 7-14 (Continued) (b) November 30 Cash ………………………………………………………………… 1,400.00 Interest Revenue ………………………………………. 1,400.00 November 30 Office Expense (bank charges) ………………………….. 27.40 Cash ………………………………………………………… 27.40 November 30 Accounts Receivable ………………………………………… 372.13 Cash ………………………………………………………… 372.13 Copyright © 2013 John Wiley & Sons, […]

Chapter 7 Totally Uncollectible Write off Immediately Seems

CHAPTER 7 Cash and Receivables SOLUTIONS TO B PROBLEMS PROBLEM 7-1B (a) December 31 Accounts Receivable ($52,750 + $650) ………………. 53,400 Sales ………………………………………………………. 32,900 Cash ………………………………………………………. 85,650 Sales Discounts ……………………………………….. 650 December 31 Cash ………………………………………………………. 42,500 Purchase Discounts …………………………………………. 400 […]

Chapter 8 Four decimal places are used to minimize rounding errors

PROBLEM 8-5B (Continued) 3. Average cost. Received Issued Balance Date No. of units Unit cost No. of units Unit cost No. of units Unit cost* Amount Mar. 1 2,000 $6.00 2,000 $6.0000 $12,000 Mar. 6 500 6.05 2,500 6.0100 5,025 […]

Chapter 8 Inventory Will Also Reported Higher Value The

Continuing Case Solution Chapter 8 (a) Memorandum To: Eric Conner and Phil Martin, CM2 From: L. Harbach Re: Inventory Costing Methods Date: January 11, 2013 Presented below are answers to the questions you posed at our last meeting. There are […]

Chapter 8 Lifo Liquidation Will Distort Net Income Make

Time and Purposes of Concepts for Analysis (Continued) CA 8-10 (Time 30–35 minutes) Purpose—to provide the student with an opportunity to analyze the effect of changing from the FIFO method to the LIFO method on items such as ending inventory, […]

Chapter 8 Sawyer Company Computation Inventory For Product Bap

4. Cost of goods sold in the income statement. 5. Cost of goods sold in the income statement. 10. Interest expense in the income statement. 12. Not reported in the financial statements. 15. Not reported in the financial statements. 16. […]

Chapter 8 The Basic Assumption That Costs Should Charged

CHAPTER 8 Valuation of Inventories: A Cost-Basis Approach ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis 1. Inventory accounts; determining quantities, costs, and items to be included in inventory; the inventory equation; balance sheet […]

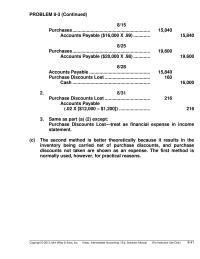

Chapter 8 The Second Method Better Theoretically Because Results

CHAPTER 8 Valuation of Inventories: A Cost-Basis Approach SOLUTIONS TO B PROBLEMS PROBLEM 8-1B 1. $260,000 – ($260,000 X 0.25) = $195,000; $195,000 – ($195,000 X 0.10) = $175,500, cost of goods purchased 2. $1,761,000 + $85,500 = $1,846,500. The […]

Chapter 8 The second method is better theoretically

PROBLEM 8-3 (Continued) 8/15 Purchases ……………………………………………………… 15,840 Accounts Payable ($16,000 X .99) ……………. 15,840 8/25 Purchases ……………………………………………………… 19,600 Accounts Payable ($20,000 X .98) ……………. 19,600 8/28 Accounts Payable ………………………………………….. 15,840 Purchase Discounts Lost ……………………………….. 160 Cash ……………………………………………………… 16,000 2. 8/31 […]

Chapter 8 this results in a higher amount for cost of goods

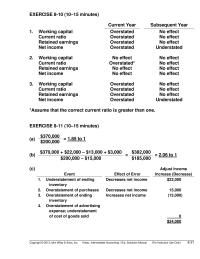

EXERCISE 8-10 (10–15 minutes) Current Year Subsequent Year 1. Working capital Overstated No effect Current ratio Overstated No effect Retained earnings Overstated No effect Net income Overstated Understated 2. Working capital No effect No effect Current ratio Overstated* No effect […]

Chapter 9 If beginning inventory is overstated, net income will

EXERCISE 9-5 (Continued) * Jan. 31 Feb. 28 Mar. 31 Apr. 30 Inventory at cost $15,000 $15,100 $17,000 $13,000 Inventory at the lower-of-cost- or-market 14,500 12,600 15,600 12,300 Allowance amount needed to reduce inventory to market $ 500 $ 2,500 […]

Chapter 9 Purchase contracts for which a firm price has

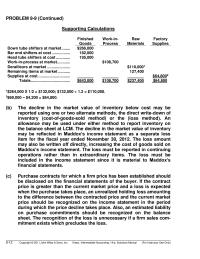

PROBLEM 9-9 (Continued) Supporting Calculations Finished Goods Work-in– Process Raw Materials Factory Supplies Down tube shifters at market …….. $266,000 Bar end shifters at cost …………….. 182,000 Head tube shifters at cost …………. 195,000 Work-in-process at market ………… $108,700 Derailleurs […]

Chapter 9 Sales Net Ending Inventory Retail

E9-16B (15–20 minutes) Furniture Beds Rugs Inventory 1/1/14 (cost) $ 76,000 $105,000 $211,000 Purchases to 9/9/14 (cost) 861,000 601,000 302,000 Cost of goods available 937,000 706,000 513,000 Deduct cost of goods sold* 486,400 538,462 437,333 Inventory 9/9/14 $450,600 $167,538 $ […]

Chapter 9 Sales See Schedule Cost Allocate Lots Total

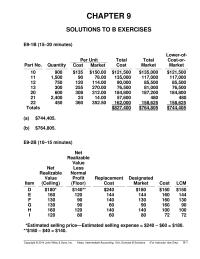

CHAPTER 9 SOLUTIONS TO B EXERCISES E9-1B (15–20 minutes) Lower-of– Part No. Quantity Per Unit Total Cost Total Market Cost-or– Market Cost Market 10 900 $135 $150.00 $121,500 $135,000 $121,500 11 1,500 90 78.00 135,000 117,000 117,000 12 750 120 […]

Chapter 9 Solutions Manual For Instructor Use Only 967

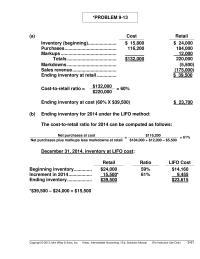

*PROBLEM 9-13 (a) Cost Retail Inventory (beginning) …………………. $ 15,800 $ 24,000 Purchases …………………………………. 116,200 184,000 Markups ……………………………………. 12,000 Totals ……………………………….. $132,000 220,000 Markdowns ……………………………….. (5,500) Sales revenue ……………………………. (175,000) Ending inventory at retail …………… $ 39,500 Cost-to-retail ratio = […]

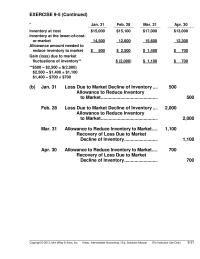

Chapter 9 The balance in the Allowance to Reduce Inventory

CHAPTER 9 Inventories: Additional Valuation Issues SOLUTIONS TO B PROBLEMS PROBLEM 9-1 Item Cost Replacement Cost Ceiling* Floor** Designated Market Lower-of– Cost-or– Market A $470 $ 460 $ 450 $350 $ 450 $450 B 450 430 480 372 430 430 […]

Chapter 9 The Difference Between The Inventory Estimate Per

TIME AND PURPOSE OF PROBLEMS Problem 9-1 (Time 10–15 minutes) Purpose—to provide the student with an understanding of the lower-of-cost-or-market approach to inventory valuation, similar to Problem 9-2. The major difference between these problems is that Problem 9-1 provides some […]

Chapter 9 The Method Requires The Reporting Estimated Losses

CHAPTER 9 Inventories: Additional Valuation Issues ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis 1. Lower-of-cost-or-market. 1, 2, 3, 4, 5, 6 1, 2, 3 1, 2, 3, 4, 5, 6 1, 2, 3, […]

Chapter 9 The Minimum Floor Deters Understatement Inventory And

Continuing Case Solution Chapter 9 (a) Memorandum To: Eric Conner and Phil Martin, CM2 From: L. Harbach Re: Lower-of-Cost-or-Market Date: January 13, 2013 Presented below is my analysis of the lower-of-cost-or-market approach. The lower-of-cost-or-market (LCM) principle is applied to ensure […]

Chapter 9 Total amount of inventory reported on March 31

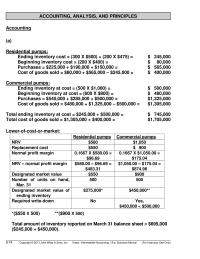

ACCOUNTING, ANALYSIS, AND PRINCIPLES Accounting (a) Residential pumps: Ending inventory cost = (300 X $500) + (200 X $475) = $ 245,000 Beginning inventory cost = (200 X $400) = $ 80,000 Purchases = $225,000 + $190,000 + $150,000 = […]