CHAPTER 14

SOLUTIONS TO B EXERCISES

E14-1B (15–20 minutes)

(a) Long-term liability as amount is due more than 1 year out.

(b) Valuation account relating to the long-term liability, bonds payable

(sometimes referred to as a contra account). The $8,500 would continue

to be reported as long-term.

E14-2B (15–20 minutes)

(a) Debenture bonds—Classify as long-term liability on balance sheet.

E14-2B (Continued)

(d) Treasury bonds—Classify as contra account to bonds payable on

balance sheet.

(h) Mortgage payable—Classify one–third as current liability and the remainder as

long-term liability on balance sheet.

E14-3B (15–20 minutes)

1.

Delgado Company:

(a)

1/1/14

Cash ……………………………………………………….

500,000

Bonds Payable …………………………..

500,000

(b)

7/1/14

Bond Interest Expense

($500,000 X 8% X 3/12) …………………………..

Cash ……………………………………………………….

(c)

12/31/14

Bond Interest Expense …………………………..

Interest Payable …………………………..

E14-3B (Continued)

2.

Kumiko Company:

(a)

6/1/14

Cash ……………………………………………………….

208,333

Bonds Payable …………………………..

200,000

Bond Interest Expense

($200,000 X 10% X 5/12) …………………………..

8,333

(b)

7/1/14

Bond Interest Expense …………………………..

10,000

Cash ($200,000 X 10% X 6/12) …………………………..

(c)

12/31/14

Bond Interest Expense …………………………..

10,000

Interest Payable …………………………..

Note: Some students may credit Interest Payable on 6/1/14. In that case,

the entry on 7/1/14 will have a debit to Interest Payable for $8,333 and a

debit to Bond Interest Expense for $1,667.

E14-4B (15–20 minutes)

(a)

1/1/14

Cash ($400,000 X 102%) …………………………..

408,000

Bonds Payable ……………………………………………….

400,000

Premium on Bonds

Payable ……………………………………………………….

8,000

(b)

7/1/14

Bond Interest Expense …………………………..

Premium on Bonds Payable

($8,000 ÷ 40) …………………………..…………………………..

Cash ($400,000 X 8% X 6/12) …………………………..

(c)

12/31/14

Bond Interest Expense …………………………..

Premium on Bonds Payable …………………………..

Interest Payable …………………………..

E14-5B (15–20 minutes)

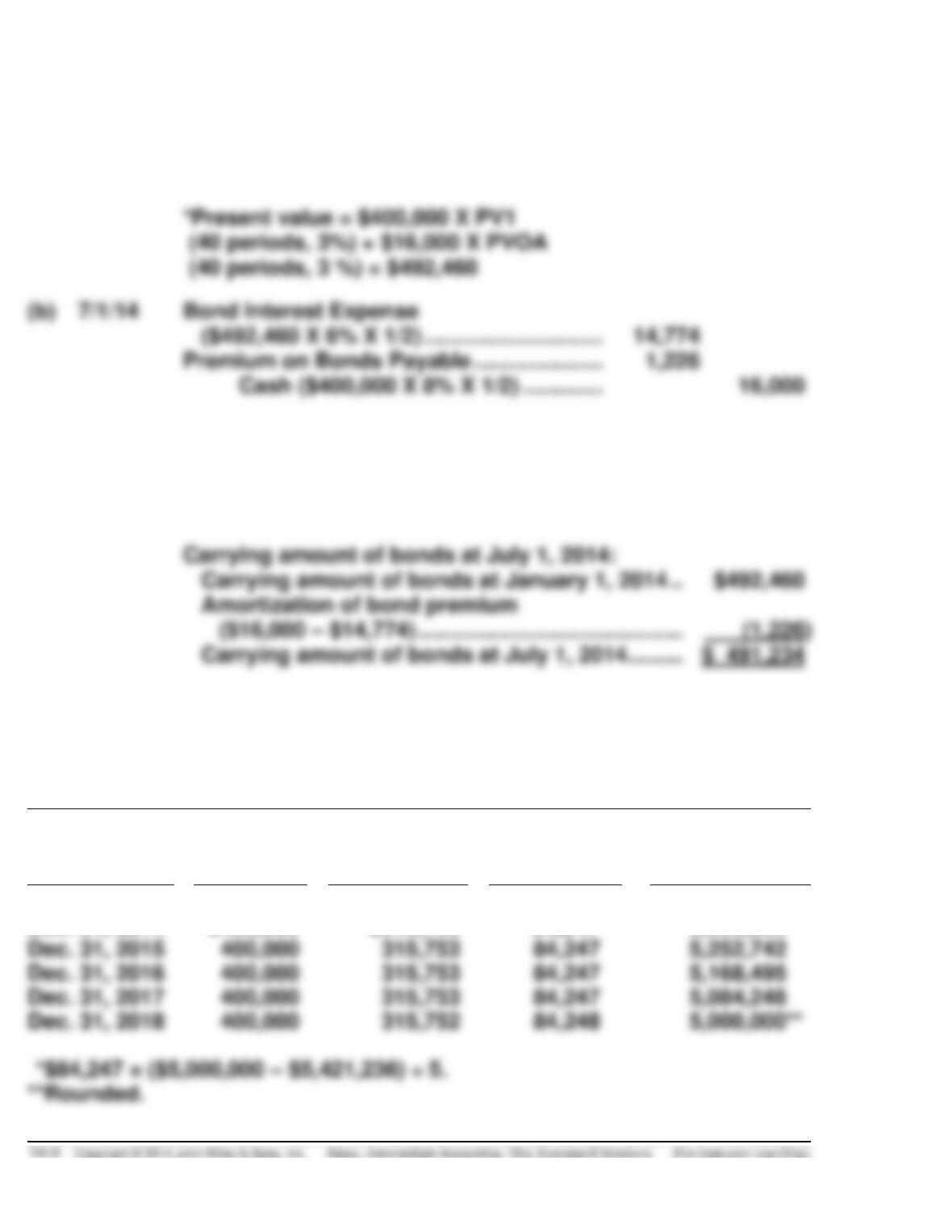

(a)

1/1/14

Cash …………………………..…………………………..

492,460*

Bonds Payable ……………………………………………….

400,000

Premium on Bonds Payable …………………………..

92,460

(b)

7/1/14

Bond Interest Expense

($492,460 X 6% X 1/2) …………………………..

Premium on Bonds Payable …………………………..

Cash ($400,000 X 8% X 1/2) …………………………..

16,000

(c)

12/31/14

Bond Interest Expense

($491,234 X 6% X 1/2) …………………………..

14,737

Premium on Bonds Payable …………………………..

1,263

Interest Payable …………………………..

16,000

Carrying amount of bonds at July 1, 2014:

Carrying amount of bonds at January 1, 2014 ..

$492,460

Amortization of bond premium

($16,000 – $14,774) …………………………..………..

E14-6B (15–20 minutes)

Schedule of Premium Amortization

Straight-Line Method

Year

Cash

Paid

Interest

Expense

Premium

Amortized

Carrying

Amount of

Bonds

Jan. 1, 2014

$5,421,236

Dec. 31, 2014

$400,000

$315,753

84,247*

5,336,989

Dec. 31, 2015

400,000

5,252,742

Dec. 31, 2016

400,000

5,168,495

Dec. 31, 2017

400,000

5,084,248

84,248

E14-7B (15–20 minutes)

The effective-interest or yield rate is 6%. It is determined through trial and

error using Table 6-2 for the discounted value of the principal ($3,736,291) and

Schedule of Premium Amortization

Effective-Interest Method (12%)

Year

Cash

Paid

Interest

Expense

Premium

Amortized

Carrying

Amount of

Bonds

(1)

(2)

(3)

(4)

Jan. 1, 2014

$5,421,236

Dec. 31, 2014

$400,000

$325,274

*

$74,726

5,346,510

Dec. 31, 2015

Dec. 31, 2016

Dec. 31, 2017

400,000

5,094,339

Dec. 31, 2018

E14-8B (15–20 minutes)

(a)

Printing and engraving costs of bonds ……………………….

$ 40,000

Legal fees …………………………………………………………………

120,000

Commissions paid to underwriter ………………………………

Amount to be reported as Unamortized Bond Issue

E14-8B (Continued)

(b)

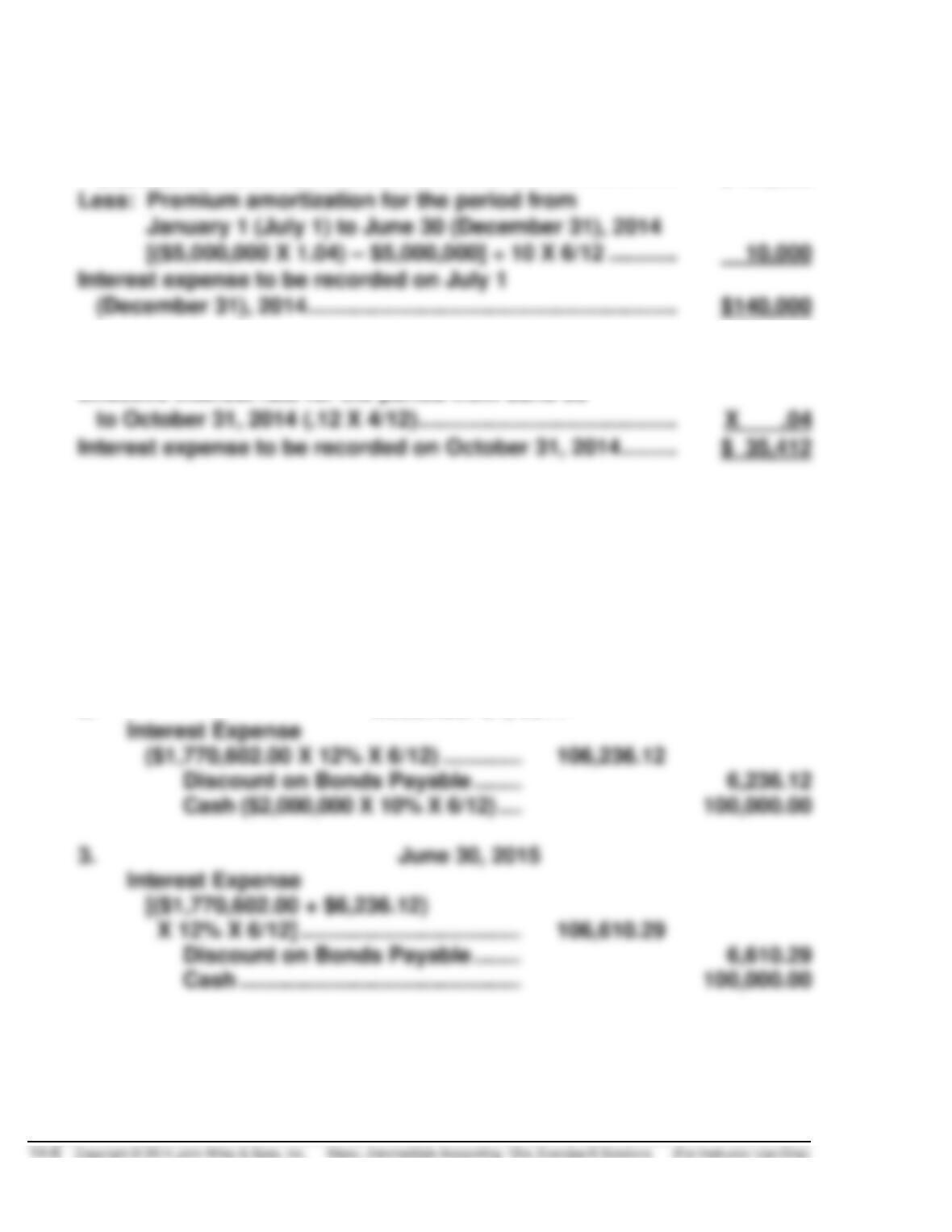

Interest paid for the period from January 1

(July 1) to June 30 (December 31), 2014;

$5,000,000 X 6% X 6/12………………………………………………..

$150,000

Less: Premium amortization for the period from

January 1 (July 1) to June 30 (December 31), 2014

[($5,000,000 X 1.04) – $5,000,000] ÷ 10 X 6/12 ………..

10,000

Interest expense to be recorded on July 1

(c)

Carrying amount of bonds on June 30, 2014 …………………..

$885,296

Effective interest rate for the period from June 30

to October 31, 2014 (.12 X 4/12) ……………………………………

E14-9B (20–30 minutes)

(a)

1.

July 1, 2014

Cash ……………………………………………………….

1,770,602.00

Discount on Bonds Payable …………………………..

229,398.00

Bonds Payable …………………………..

2,000,000.00

2.

December 31, 2014

Interest Expense

($1,770,602.00 X 12% X 6/12) …………………………..

Discount on Bonds Payable …………………………..

Cash ($2,000,000 X 10% X 6/12) …………………………

3.

Interest Expense

[($1,770,602.00 + $6,236.12)

X 12% X 6/12] ……………………………………………………..

106,610.29

Discount on Bonds Payable …………………………..

Cash …………………………..…………………………..

E14-9B (Continued)

4.

December 31, 2015

Interest Expense

[($1,770,602.00 + $6,236.12 +

$6,610.29) X 12% X 6/12] …………………………..

Discount on Bonds Payable …………………………..

Cash ……………………………………………………….

100,000.00

(b)

Long-term Liabilities:

Bonds payable, 10% (due on June 30, 2024) ……………..

$2,000,000.00

Discount on Bonds Payable* ……………………………………

209,544.69

(c)

1.

Interest expense for the period from

January 1 to June 30, 2015 from (a) 3. ……………………

$106,610.69

Interest expense for the period from

July 1 to December 31, 2015 from (a) 4. ………………….

Amount of bond interest expense

2.

the bond interest expense under the effective-interest method.

The amount of bond interest expense reported in 2015 will be less

than the amount that would be reported if the straight-line method

E14-9B (Continued)

3.

Total interest to be paid for the bond

($2,000,000 X 10% X 10) …………………………..

$2,000,000

Plus: Discount ……………………………………………………….

Total cost of borrowing over the life

4.

They will be the same.

E14-10B (15–20 minutes)

(a)

January 1, 2014

Cash ……………………………………………………….

1,075,814.74

Premium on Bonds Payable …………………………..

Bonds Payable ……………………………………………….

1,000,000.00

(b) Schedule of Interest Expense and Bond Premium Amortization

Effective-Interest Method

12% Bonds Sold to Yield 10%

Date

Credit Cash

Debit Interest

Expense

Debit

Bond

Premium

Carrying

Value of

Bonds

1/1/14

—

—

—

$1,075,814.74

12/31/14

12/31/16

(c)

December 31, 2014

Bond Interest Expense …………………………..

107,581.47

Premium on Bonds Payable …………………………..

12,418.53

Cash ……………………………………………………….

120,000.00

(d)

December 31, 2016

Bond Interest Expense …………………………..

Premium on Bonds Payable …………………………..

15,026.42

Cash ……………………………………………………….

120,000.00

E14-11B (20–30 minutes)

Secured

Bonds

Zero-Coupon

Bonds

Mortgage

Bonds

1.

Maturity value

$5,000,000

$8,000,000

$10,000,000

2.

Number of interest

20

20

40

periods

3.

Stated rate per period

8%

4.

Effective rate per period

5.

Payment amount per period

6.

Present value

(a)$5,000,000 X 8% = $400,000

$ 4,148,600

(d)Present value of $8,000,000 discounted

at 12% for 20 periods

($8,000,000 X 0.10367) = …………………………………………..

$ 829,360

(e)Present value of an annuity of $500,000 discounted

$11,979,285

E14-12B (15–20 minutes)

Reacquisition price ($2,500,000 X 105%) …………………..

$2,625,000

Less: Net carrying amount of bonds redeemed:

Par value ………………………………………………………

Unamortized premium ……………………………………

Unamortized bond issue costs ……………………….

Calculation of unamortized premium—

Original amount of premium:

$2,500,000 X 2% = $50,000

$50,000/10 = $5,000 amortization per year

Amount of discount unamortized:

$5,000 X 8 = $40,000

Calculation of unamortized issue costs—

Original amount of costs:

$81,000 X $2,500,000/$5,000,000 = $40,500

$40,500/10 = $4,050 amortization per year

Amount of costs unamortized:

$4,050 X 8 = $32,400

January 2, 2014

Bonds Payable ……………………………………………………….

2,500,000

Loss on Redemption of Bonds …………………………..

117,400

Premium on Bonds Payable …………………………………….

Unamortized Bond Issue Costs ………………

Cash ……………………………………………………….

E14-13B (15–20 minutes)

Cash ……………………………………………………………………….

11,760,000

Discount on Bonds Payable (.02 X $12,000,000) ……………

240,000

Bonds Payable ………………………………………………..

12,000,000

(To record issuance of 10% bonds)

Bonds Payable ……………………………………………………….

8,000,000

Loss on Redemption of Bonds …………………………..

Cash ($8,000,000 X 1.06) …………………………..

Discount on Bonds Payable …………………………..

Unamortized Bond Issue Costs ………………………..

(To record retirement of 12% bonds)

Reacquisition price ………………………………………………….

$8,480,000

Less: Net carrying amount of bonds redeemed:

Par value……………………………………………………….

$8,000,000

Unamortized bond discount …………………………..

Unamortized bond issue costs …………………………

E14-14B (12–16 minutes)

(a)

June 30, 2015

Bonds Payable ……………………………………………………….

1,000,000

Loss on Redemption of Bonds …………………………..

Discount on Bonds Payable …………………………..

Cash ……………………………………………………….

1,020,000

Reacquisition price ($1,000,000 X 102%) …………………..

$1,020,000

Net carrying amount of bonds redeemed:

Par value …………………………..…………………………..

Unamortized discount …………………………..

(13,000)

(987,000)

(0.02 X $1,000,000 X 13/20)

Cash ($1,100,000 X 101%) …………………………..

Premium on Bonds Payable …………………………..

E14-14B (Continued)

(b)

December 31, 2015

Interest Expense …………………………………………………….

32,725

Premium on Bonds Payable …………………………..

Cash ……………………………………………………….

*(1/40 X $11,000 = $275)

**(0.03 X $1,100,000 = $33,000)

E14-15B (10–15 minutes)

Reacquisition price ($1,500,000 X 103%) …………………..

$1,545,000

Less: Net carrying amount of bonds redeemed:

Par value ………………………………………………………

$1,500,000

Unamortized premium …………………………………..

Bonds Payable ……………………………………………………….

Loss on Redemption of Bonds …………………………..

Premium on Bonds Payable …………………………………….

(To record redemption of bonds

payable)

Cash …………………………..………………………………………….

Unamortized Bond Issue Costs …………………………..

Discount on Bonds Payable …………………………………….

(To record issuance of new bonds)

E14-16B (15–20 minutes)

(a)

1.

January 1, 2014

Land ……………………………………………………….

800,000.00

Discount on Notes Payable …………………………..

375,464.00

Notes Payable …………………………..

(The $800,000 capitalized land

cost represents the present

value of the note discounted

for 5 years at 8%)

2.

Equipment ……………………………………………………….

269,547.46

Discount on Notes Payable …………………………..

80,452.54*

Notes Payable …………………………..

350,000.00

*Computation of the discount on

notes payable:

Maturity value …………………………..

Present value of $350,000 due in

8 years at 8%—$350,000

X .54027 ……………………………………………………….

Present value of $14,000

payable annually for 8 years

at 8% annually—$14,000

X 5.74664 ……………………………………………………..

Present value of the note …………………………..

(b)

1.

Interest Expense ……………………………………………………..

64,000.00

Discount on Notes Payable …………………………..

64,000.00

($800,000 X .08)

2.

Interest Expense ……………………………………………………..

21,563.80

($269,547.46 X .08)

Discount on Notes Payable …………………………..

Cash ($350,000 X .04) …………………………..

14,000.00