CHAPTER 8

Valuation of Inventories: A Cost-Basis Approach

SOLUTIONS TO B PROBLEMS

PROBLEM 8-1B

1. $260,000 – ($260,000 X 0.25) = $195,000;

$195,000 – ($195,000 X 0.10) = $175,500, cost of goods purchased

3. Because no date was associated with the units issued or sold, the

periodic (rather than perpetual) inventory method must be assumed.

FIFO inventory cost:

500 units at $65

$ 32,500

1,000 units at 66

66,000

Total

$ 98,500

LIFO inventory cost:

$ 62,000

500 units at 63

31,500

Total

$ 93,500

Average cost:

1,000 at $62

$ 62,000

3,000 at 63

2,000 at 65

66,000

Totals

Ending inventory (1,500 X $63.86) is $95,790.

PROBLEM 8-1B (Continued)

4. Computation of price indexes:

12/31/2014

$375,440

= 104

$361,000

12/31/2015

$449,080

= 109

Dollar-value LIFO inventory 12/31/2014:

Increase in terms of 104

Base inventory

Dollar-value LIFO inventory 12/31/2015:

Increase $412,000 – $360,000 =

$ 52,000

12/31/2015 price index

Base inventory

5. The inventoriable costs for 2015 are:

Merchandise purchased …………………………...

$2,684,100

Add: Freight-in ………………………………………..

56,100

Deduct: Purchase returns ………………………..

Purchase discounts …………………….

PROBLEM 8-2B

MIAMI FIRE COMPANY

Schedule of Adjustments

December 31, 2014

Inventory

Accounts

Payable

Net Sales

Initial amounts

$2,590,000

$1,900,000

$16,680,000

Adjustments:

1.

NONE

21,500

NONE

2.

NONE

NONE

(34,000)

3.

NONE

4.

NONE

NONE

5.

NONE

(36,000)

6.

NONE

7.

NONE

NONE

8.

15,000

Total adjustments

156,800

81,700

1. The $21,500 of goods received on 12/29/2014 were properly included in

2. The $26,000 of tools on the loading dock were properly included in the

physical count. The sale should not be recorded until the goods are

picked up by the common carrier. Therefore, no adjustment is made to

inventory, but sales must be reduced by the $34,000 billing price.

3. The goods received from a vendor at 6:00 p.m. on 12/31/2014 should be

included in the ending inventory, but were not included in the physical

PROBLEM 8-2B (Continued)

4. The work-in-process inventory sent to an outside processor is Miami

5. The tools costing $21,000 were recorded as sales ($36,000) in 2014.

However, these items were returned by customers on December 31, so

2014 net sales should be reduced by the $36,000 return. Also, $21,000

has to be added to the inventory column since these goods were not

included in the physical count.

6. The $45,200 of goods in transit from a vendor to Miami Fire were

shipped f.o.b. shipping point on 12/26/2014. Title passes to the buyer

7. The $15,600 of Miami Fire’s tools shipped to a customer f.o.b.

destination are still owned by Miami Fire while in transit because title

8. Since one-third of the freight-in cost ($15,000) pertains to merchandise

properly included in inventory as of 12/31/2014, $5,000 should be

(a)

1.

3/8

Purchases ………………………………………………………

15,000

Accounts Payable …………………………………..

15,000

Accounts Payable …………………………………………..

Purchase Returns and Allowances …………..

Purchases ………………………………………………………

16,000

Accounts Payable …………………………………..

Accounts Payable …………………………………………..

Purchase Discounts ………………………………..

Cash ………………………………………………………

15,680

Purchases ………………………………………………………

36,000

2. Purchases—addition to beginning inventory in cost of goods

sold section of income statement.

Purchase returns and allowances—deduction from purchases in

cost of goods sold section of the income statement.

(b)

1.

3/8

Purchases ………………………………………………………

14,850

Accounts Payable ($15,000 X 0.99) …………..

14,850

PROBLEM 8-3B (Continued)

3/11

Accounts Payable……………………………………………

2,178

Purchase Returns and Allowances

($2,200 X 0.99) ………………………………………

3/17

Purchases ………………………………………………………

Accounts Payable ($16,000 X 0.98) …………..

Accounts Payable……………………………………………

Cash ………………………………………………………

Purchases ………………………………………………………

Accounts Payable ($36,000 X 0.98) …………..

2.

3/31

Purchase Discounts Lost …………………………………

128

Accounts Payable

(0.01 X [$15,000 – $2,200]) ……………………..

128

Same as part (a) (2) except:

Purchase Discounts is not used.

(c)

The second method is better theoretically because it results in the

inventory being carried net of purchase discounts, and purchase

discounts not taken are shown as an expense. The first method is

normally used, however, for practical reasons.

PROBLEM 8-4B

(a)

Purchases

Total Units

Sales

Total Units

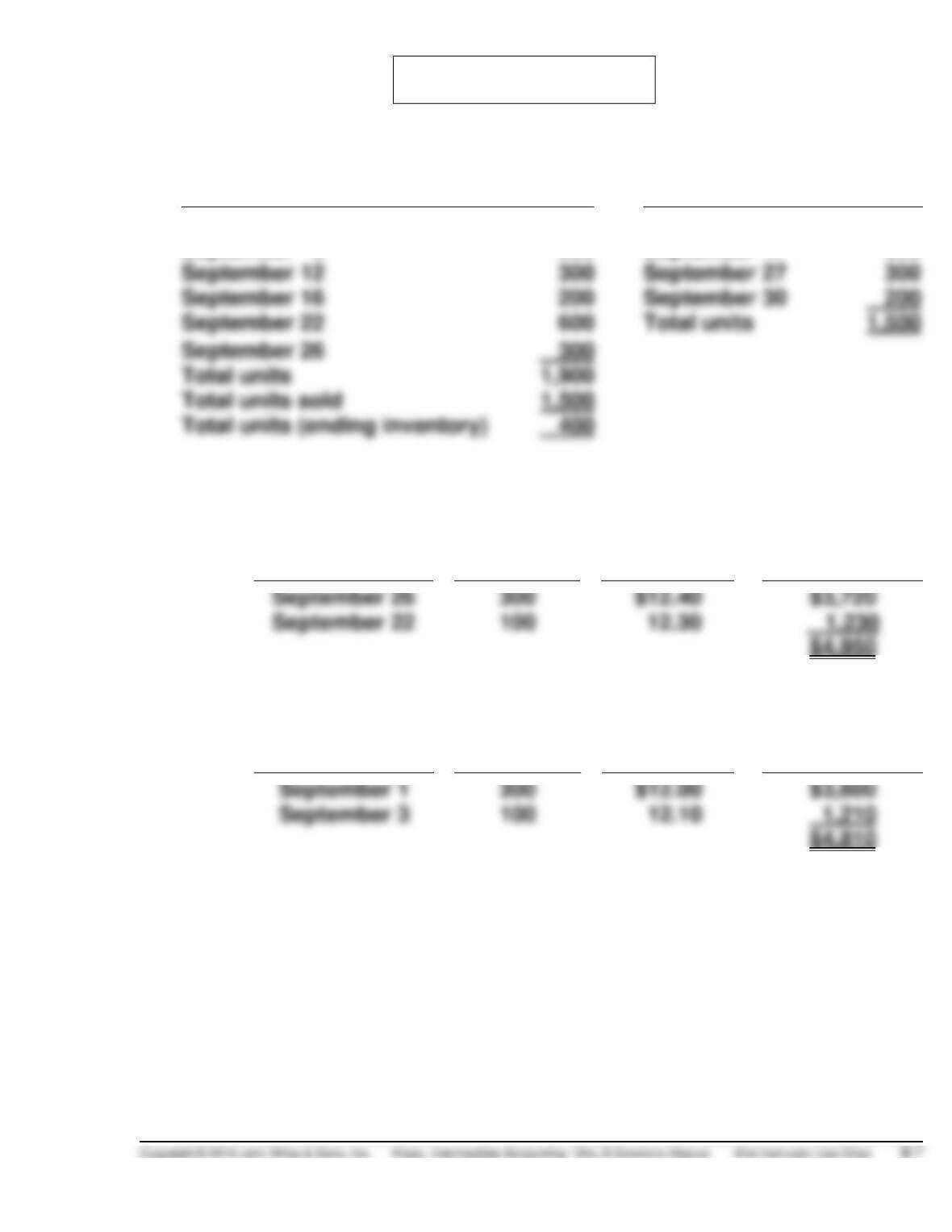

September 1 (balance on hand)

300

September 4

400

September 3

200

September 17

600

September 12

300

September 27

300

September 16

200

September 30

September 26

Total units

Total units sold

Assuming costs are not computed for each withdrawal:

1. First-in, first-out.

Date of Invoice

No. Units

Unit Cost

Total Cost

2. Last-in, first-out.

Date of Invoice

No. Units

Unit Cost

Total Cost

PROBLEM 8-4B (Continued)

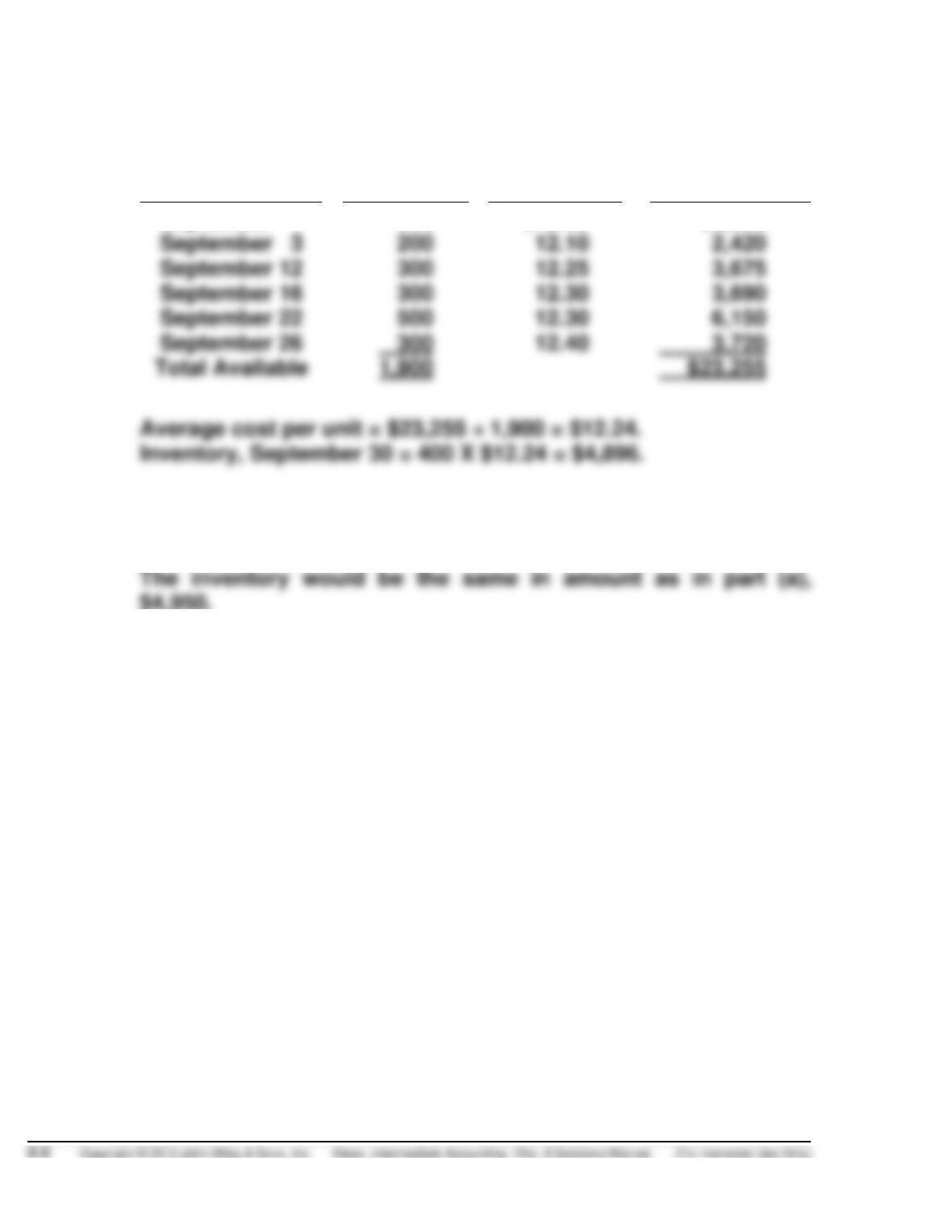

3. Average cost.

Cost of Part X available.

Date of Invoice

No. Units

Unit Cost

Total Cost

September 1

300

$12.00

$3,600

September 3

200

2,420

September 22

500

(b) Assuming costs are computed for each withdrawal:

1. First-in, first out.

PROBLEM 8-4B (Continued)

2. Last-in, first-out.

Purchased

Sold

Balance*

Date

No. of

units

Unit

cost

No. of

units

Unit

cost

No. of

units

Unit

cost

Amount

Sep. 1

300

$12.00

300

$12.00

$ 3,600

Sep. 3

200

12.10

300

12.00

200

6,020

Sep. 4

200 @

200 @

$12.00

100

1,200

Sep. 12

300

12.25

100

300

Sep. 16

200

100

12.00

300

12.25

200

12.30

7,335

Sep. 17

200 @

300 @

100

12.00

1,200

Sep. 22

500

12.30

100

12.00

500

12.30

7,350

Sep. 26

300

12.40

100

12.00

500

12.30

300

12.40

11,070

Sep. 27

300 @

12.40

100

12.00

500

12.30

7,350

Sep. 30

200 @

100

12.00

300

12.30

4,890

PROBLEM 8-4B (Continued)

3. Average cost.

Purchased

Sold

Balance

Date

No. of

units

Unit

cost

No. of

units

Unit cost

No. of

units

Unit

cost*

Amount

Sep. 1

300

$12.00

300

$12.0000

$3,600.00

Sep. 3

200

12.10

500

12.0400

6,02000

Sep. 4

100

12.0400

1,204.00

Sep. 12

300

12.25

400

4,879.00

Sep. 16

300

700

12.2414

8,569.00

Sep. 17

100

12.2414

1,224.14

Sep. 22

600

12.2902

7,374.14

Sep. 26

300

12.40

900

12.3268

11,094.14

Sep. 27

600

7,396.08

Sep. 30

400

Inventory, September 30 is $4,930.72

*Four decimal places are used to minimize rounding errors.

PROBLEM 8-5B

(a) Assuming costs are not computed for each withdrawal (units received,

7,000, minus units issued, 4,900, equals ending inventory at 2,100 units):

1. First-in, first-out.

Date of Invoice

No. Units

Unit Cost

Total Cost

2. Last-in, first-out.

Date of Invoice

No. Units

Unit Cost

Total Cost

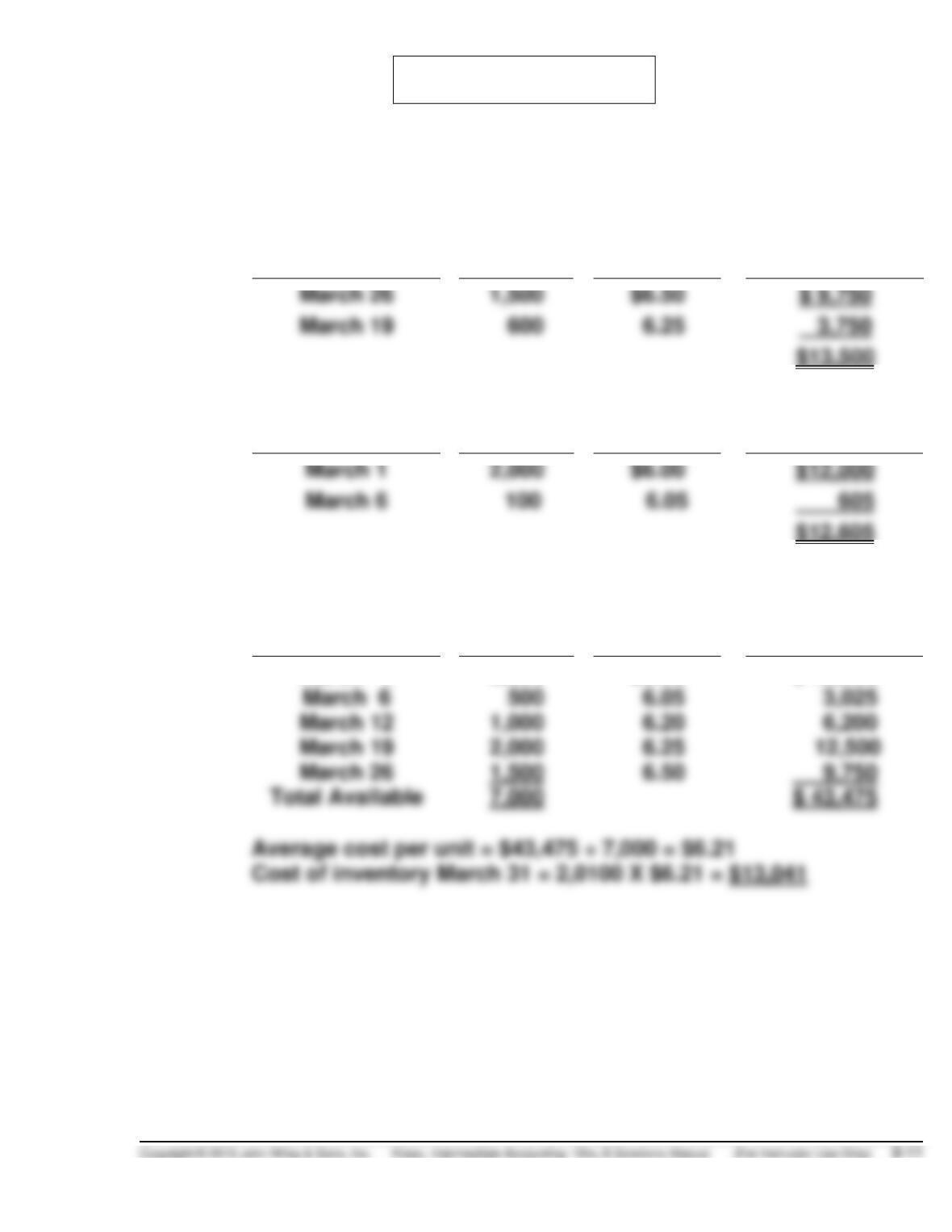

3. Average cost.

Cost of goods available:

Date of Invoice

No. Units

Unit Cost

Total Cost

March 1

2,000

$6.00

$ 12,000

March 12

1,000

6,200

PROBLEM 8-5B (Continued)

(b) Assuming costs are computed at the time of each withdrawal:

Under FIFO—Yes. The amount shown as ending inventory would be

The calculations to determine the inventory on this basis are given below.

1. First-in, first-out.

PROBLEM 8-5B (Continued)

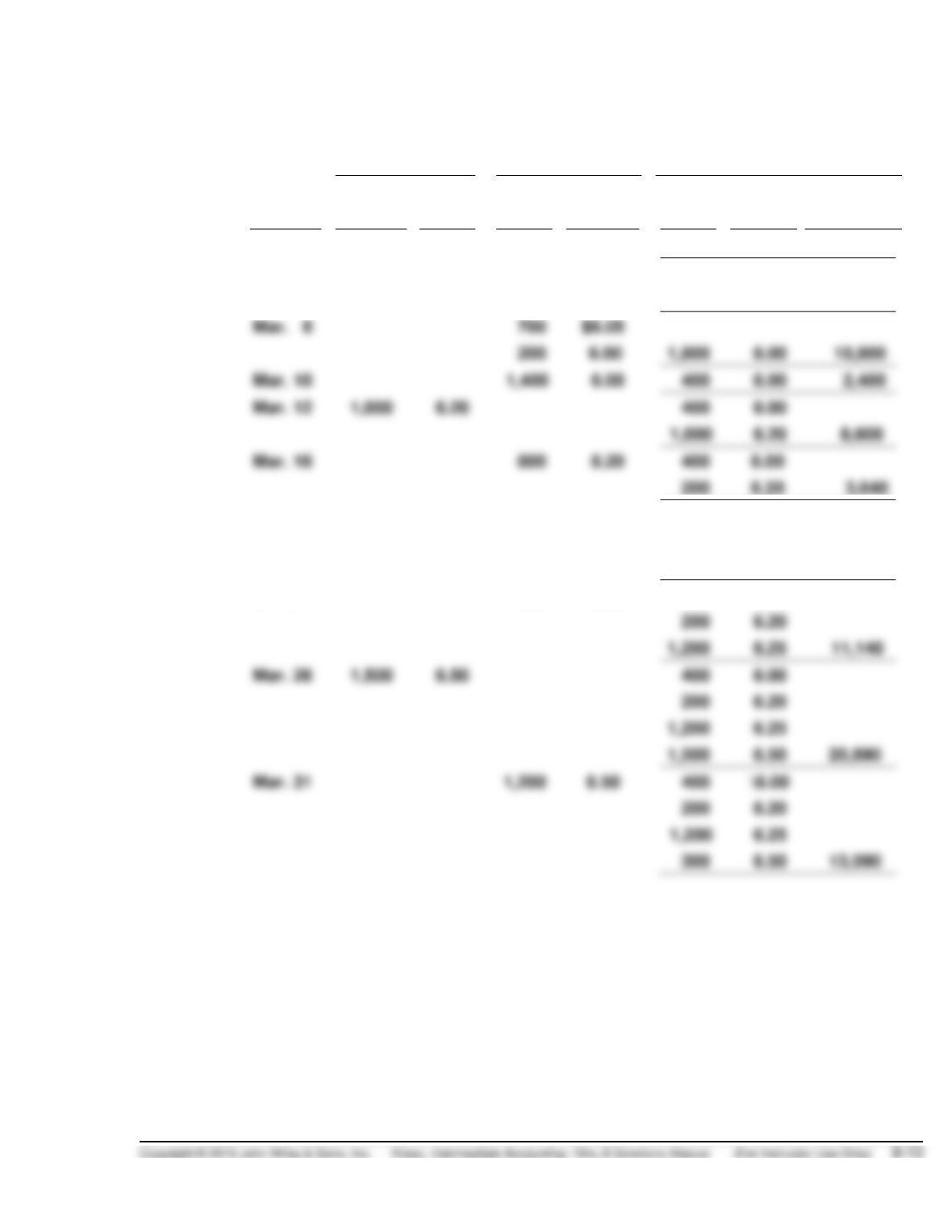

2. Last-in, first-out.

Received

Issued

Balance

Date

No. of

units

Unit

cost

No. of

units

Unit

cost

No. of

units

Unit

cost*

Amount

Mar. 1

2,000

$6.00

2,000

$6.00

$12,000

Mar. 6

500

6.05

2,000

6.00

15,025

500

6.05

Mar. 8

700

$6.05

200

1,800

6.00

10,800

Mar. 12

1,000

6.20

400

6.00

6.20

Mar. 16

800

400

200

Mar. 19

2,000

6.25

200

6.25

400

6.00

200

6.20

1,800

6.25

14,890

Mar. 22

600

6.25

400

6.00

200

6.20

1,200

6.25

Mar. 26

6.50

400

6.00

200

6.20

6.25

1,500

6.50

Mar. 31

400

\6.00

200

6.20

6.25

300

6.50

Inventory, March 31 is $13,090.