CHAPTER 16

Dilutive Securities and Earnings Per Share

SOLUTIONS TO B PROBLEMS

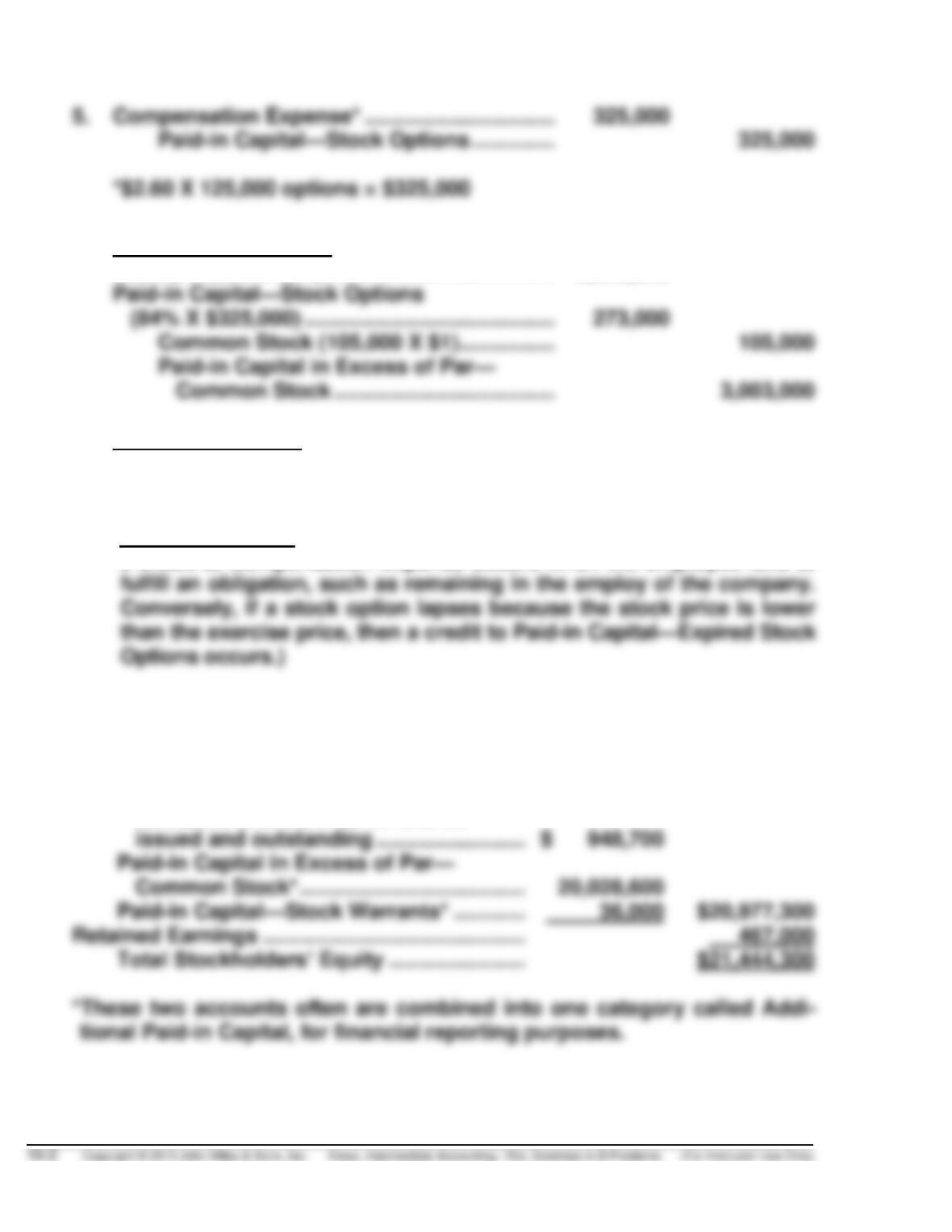

PROBLEM 16-1B

(a) 1. Memo Entry (memo entry made to indicate the number of rights

issued).

2. Cash ………………………………………………………… 1,060,000

Discount on Bonds Payable* …………………….. 30,000

Bonds Payable ………………………………….. 1,000,000

Paid-in Capital—Stock Warrants** ………. 90,000

3. Cash* ………………………………………………………. 892,500

Common Stock (42,500 X $1) ……………… 42,500

4. Cash* ………………………………………………………. 22,800

Paid-in Capital—Stock Warrants

PROBLEM 16-1B (Continued)

6. For options exercised:

Cash (105,000 X $27) ………………………………… 2,835,000

For options lapsed:

Paid-in Capital—Stock Options…………………. 52,000

Compensation Expense …………………….. 52,000

(Note to instructor: This entry provides an opportunity to indicate that

a credit to Compensation Expense occurs when the employee fails to

(b) Stockholders’ Equity:

Paid-in Capital:

Common Stock, $1 par value, authorized

5,000,000 shares, 948,700 shares

PROBLEM 16-1B (Continued)

Calculations:

Common Stock

Paid-in Capital

in Excess of Par

At beginning of year …………………..

800,000 shares

$16,100,000

From stock rights (entry #3) ……….

From stock warrants (entry #4) …..

Total …………………………………..

948,700 shares

PROBLEM 16-2B

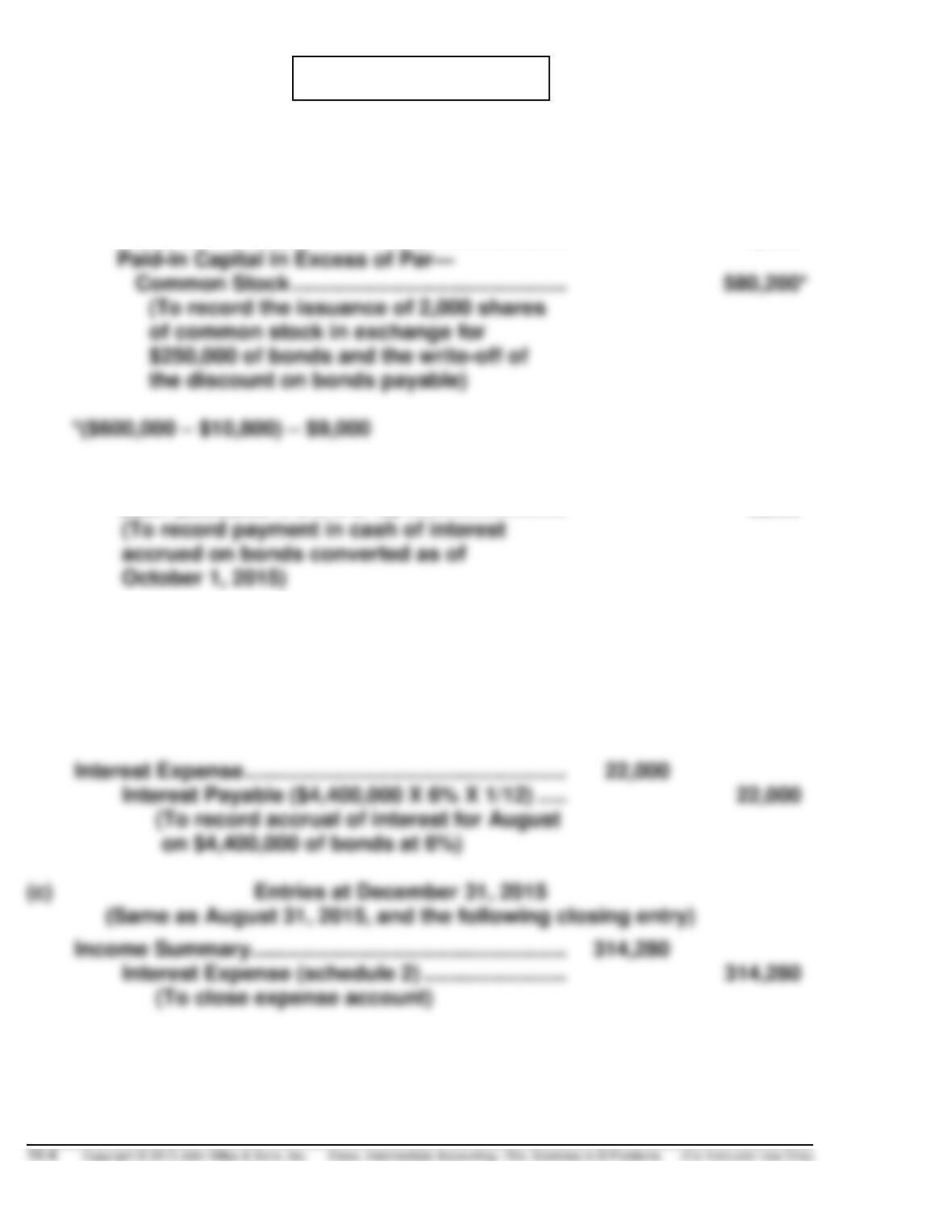

(a) Entries at October 1, 2015

Bonds Payable ………………………………………………… 600,000

Discount on Bonds Payable (Schedule 1) …… 10,800

Common Stock (15 X 600 X $1) ………………….. 9,000

Interest Payable ………………………………………………. 9,000

Cash ($600,000 X 6% X 3/12) ……………………… 9,000

(b) Entries at October 31, 2015

Interest Expense ……………………………………………… 1,760

Discount on Bonds Payable (Schedule 1) ….. 1,760

(To record amortization of one month’s

discount on $2,250,000 of bonds)

PROBLEM 16-2B (Continued)

Schedule 1

Monthly Amortization Schedule

Unamortized discount on bonds payable:

Amount to be amortized over 60 months …………………………..……. $120,000

Amount of monthly amortization ($120,000 ÷ 60) …………………….. $ 2,000

Schedule 2

Interest Expense Schedule

Amortization of bond discount charged to bond interest expense in 2015 would

be as follows:

Interest on Bonds:

6% on $5,000,000 …………………………………………………………………… $300,000

Total interest

Amortization of discount ……………… $ 23,280

Cash interest paid ……………………….. 291,000

Bond interest expense ………………… $314,280

PROBLEM 16-3B

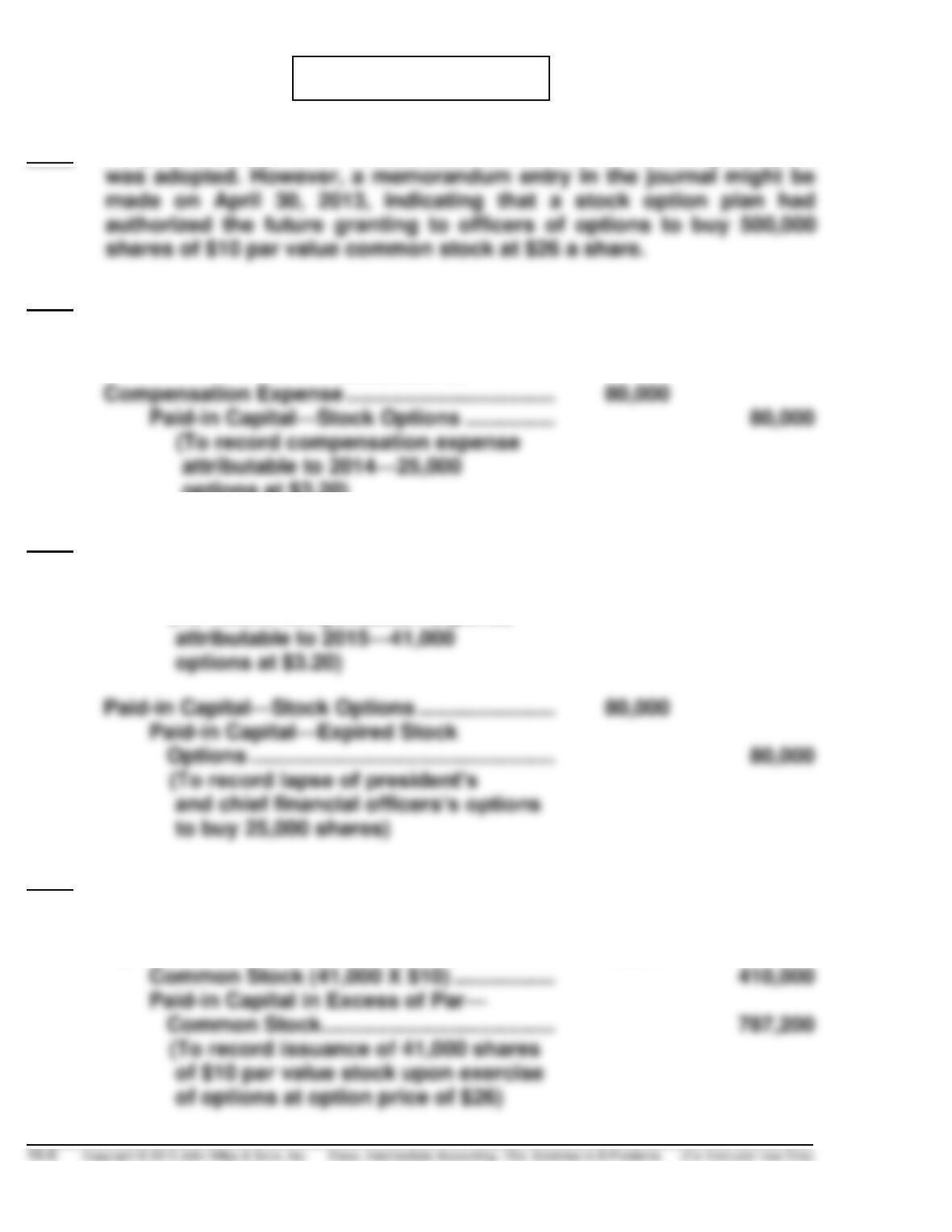

2013 No journal entry would be recorded at the time the stock option plan

2014 January 2

No entry

December 31

options at $3.20)

2015 December 31

Compensation Expense …………………………….. 131,200

Paid-in Capital—Stock Options …………… 131,200

(To record compensation expense

2016 December 31

Cash (41,000 X $26) …………………………………… 1,066,000

Paid-in Capital—Stock Options

(41,000 X $3.20) ………………………………………. 131,200

PROBLEM 16-4B

(a) 1/1/14 No entry

12/31/14 Compensation Expense ($2 X 75,000 ÷ 4) …. 37,500

Paid-in Capital—Stock Options ………… 37,500

(c) No change for part (a), unless the fair value of the options change.

For part (b):

PROBLEM 16-5B

The computation of Detroit Industries’ basic earnings per share and the

diluted earnings per share for the fiscal year ended March 31, 2014, are shown

below.

1Preferred dividend = 0.05 X $5,000,000 = $250,000

(b)

Diluted earnings per share

=

Net income – Preferred dividends +

Interest (net of tax)

Average common shares + Potentially

dilutive common shares

2Use “if converted” method for 4% bonds

Adjustment for interest expense (net of tax)

($8,000,000 X 0.04 X 0.70) ………………………………… $224,000

PROBLEM 16-5B (Continued)

4Use treasury stock method to determine incremental

shares outstanding

PROBLEM 16-6B

(a) Orlando Corporation has a simple capital structure since it does not have

any potentially dilutive securities.

(b) The weighted-average number of shares that Orlando Corporation would

use in calculating earnings per share for the fiscal years ended August

31, 2014, and August 31, 2015, is 2,530,000 and 3,040,000 respectively,

calculated as follows:

Event

Dates

Outstanding

Shares

Outstanding

Restatement

Fraction

of Year

Weighted

Shares

Beginning balance

Sep. 1–Dec. 1

New Issue

Stock Dividend

Jan. 1-Aug. 31

1,760,000

2,530,000

Event

Dates

Outstanding

Shares

Outstanding

Restatement

Fraction

of Year

Weighted

Shares

Beginning balance

Sep 1–Mar. 1

1,320,000

New Issue

3,040,000

(c) ORLANDO CORPORATION

Comparative Income Statement

For Fiscal Years Ended August 31, 2014 and 2015

2014

2015

Income from operations ……………………………………

$1,250,000

$1,800,000

Interest expense1 ……………………………………………..

180,000

180,000

Income taxes at 40% …………………………..…………….

428,000

648,000

Income before extraordinary item ………………………

taxes of $160,000 …………………………………………..

Net income ……………………………………………………….

$ 642,000

$ 732,000

Earnings per share:

Income before extraordinary loss ……………….

$0.152

$0.243

Extraordinary loss ……………………………………..

Net income ………………………………………………..

$0.15

$0.165

PROBLEM 16-6B (Continued)

=

3,040,000

=

=

=

*Preferred dividends = (No. of Shares X Par Value X Dividend %)

= (50,000 X $100 X 0.05)

= $250,000,000 per year

5Earnings per share

=

Net Income – Preferred Dividends

Weighted-Average Common Shares

=

$732,000 – $240,000

3,040,000

=

$0.16

PROBLEM 16-7B

(a) The number of shares used to compute basic earnings per share is

10,847,500, as calculated below.

Event

Dates

Outstanding

Shares

Outstanding

Restatement

Fractio

n

of Year

Weighted

Shares

Beginning Balance,

including 2 for 1

stock split

Jan. 1–Apr. 1

9,000,000

1.1

3/12

2,475,000

9,500,000

1.1

3/12

Conversion of

Oct. 1–Nov. 1

11,550,000

1/12

Purchase of Treasury

(b) The number of shares used to compute diluted earnings per share is

5,791,000, as shown below.

Number of shares to compute

basic earnings per share …………………………... 10,847,500

(c) The adjusted net income to be used as the numerator in the basic earnings

per share calculation for the year ended December 31, 2015, is $6,090,000, as

computed below.

After-tax net income …………………………..……….. $6,890,000

PROBLEM 16-8B

(a)

Basic EPS

=

$8,670,000 – ($2,500,000 X 0.04)

9,500,000

=

$0.90 per share

=

=

=

b$5,000,000 X 0.06 X (1 – 0.40)

cMarket price – Option price

X Number of options = incremental shares

Market price

PROBLEM 16-9B

(a)

Weighted-Average Shares

Before Stock

Dividend

After Stock

Dividend

Total as of November 1, 2013

2,000,000

2,300,000

Issue of February 1, 2014

600,000

690,000

Total as of October 31, 2015

2,990,000

2,990,000 X 9/12 =

2,242,500

Total

2,817,500

2,990,000

(b) PRAWNER CORPORATION

Comparative Income Statement

For the Years Ended October 31, 2015 and 2014

2015

2014

Income from operations before income taxes …..

$3,750,000

$3,200,000

Income taxes ………………………………………………….

1,500,000

1,280,000

Income before extraordinary item ……………………

2,250,000

1,920,000

Net income …………………………………………………….

$1,560,000

Per share of common stock

Income before extraordinary item …………………

Extraordinary loss, net of tax ……………………….

Net income …………………………………………………….

PROBLEM 16-9B (Continued)

EPS calculations =

Net income – Preferred dividends

Weighted-average common shares

(c) 1. A corporation’s capital structure is regarded as simple if it consists

only of common stock or includes no potentially dilutive securities.

2. A corporation having a complex capital structure would be required

to make a dual presentation of earnings per share; i.e., both basic

earnings per share and diluted earnings per share. This assumes that

the potentially dilutive securities are not antidilutive.