EXERCISE 14-8 (Continued)

(c)

Carrying amount of bonds on June 30, 2014

$562,500

Effective-interest rate for the period from June 30

to October 31, 2014 (.10 X 4/12)

EXERCISE 14-9 (20–30 minutes)

(a)

1.

June 30, 2014

Cash ……………………………………………………….

4,300,920.00

Bonds Payable …………………………..

Premium on Bonds Payable …………………………..

2.

December 31, 2014

Interest Expense …………………………..

258,055.20

($4,300,920.00 X 12% X 6/12)

Premium on Bonds Payable …………………………..

Cash ……………………………………………………….

($4,000,000 X 13% X 6/12)

3.

June 30, 2015

Interest Expense …………………………..

257,938.51

[($4,300,920.00 – $1,944.80)

X 12% X 6/12]

Premium on Bonds Payable …………………………..

Cash ……………………………………………………….

4.

December 31, 2015

Interest Expense …………………………..

257,814.82

[($4,300,920.00 – $1,944.80 –

$2,061.49) X 12% X 6/12]

Premium on Bonds Payable …………………………..

Cash ……………………………………………………….

EXERCISE 14-9 (Continued)

(b)

Long-term Liabilities:

Bonds payable, 13% (due on June 30, 2034)

Premium on bonds payable*

(c)

1.

Interest expense for the period from

January 1 to June 30, 2015 from (a) 3.

$257,938.51

Interest expense for the period from

July 1 to December 31, 2015 from (a) 4.

Amount of interest expense

2.

The amount of bond interest expense reported in 2015 will be

greater than the amount that would be reported if the straight–

line method of amortization were used. Under the straight-line

3.

Total interest to be paid for the bond

($4,000,000 X 13% X 20)

$10,400,000

Principal due in 2034

4,000,000

Total cash outlays for the bond

Cash received at issuance of the bond

(4,300,920)

Total cost of borrowing over the life

4.

They will be the same.

EXERCISE 14-10 (15–20 minutes)

(a)

January 1, 2014

Cash ……………………………………………………….

537,907.37

Premium on Bonds Payable …………………………..

Bonds Payable ……………………………………………….

(b) Schedule of Interest Expense and Bond Premium Amortization

Effective-Interest Method

12% Bonds Sold to Yield 10%

Date

Cash

Paid

Interest

Expense

Premium

Amortized

Carrying

Amount of

Bonds

1/1/14

–

–

–

$537,907.37

12/31/14

$60,000.00*

$6,209.26

12/31/15

12/31/16

(c)

December 31, 2014

Interest Expense …………………………………………………….

53,790.74

Premium on Bonds Payable …………………………..

Cash ……………………………………………………….

(d)

December 31, 2015

Interest Expense …………………………………………………….

52,486.79

Premium on Bonds Payable …………………………..

Cash ……………………………………………………….

EXERCISE 14-11 (20–30 minutes)

Unsecured

Bonds

Zero-Coupon

Bonds

Mortgage

Bonds

(1)

Maturity value

$10,000,000

$25,000,000

$20,000,000

(2)

Number of interest

40

10

10

periods

(3)

Stated rate per period

3.75% (

15%

)

0

10%

4

(4)

Effective rate per period

12%

period

(6)

Present value

(a)$10,000,000 X 15% X 1/4 = $375,000

(b)$20,000,000 X 10% = $2,000,000

(c)Present value of an annuity of $375,000

(d)Present value of $25,000,000 discounted

at 12% for 10 periods

($25,000,000 X .32197) =

$ 8,049,250

(e)Present value of an annuity of $2,000,000 discounted

EXERCISE 14-12 (15–20 minutes)

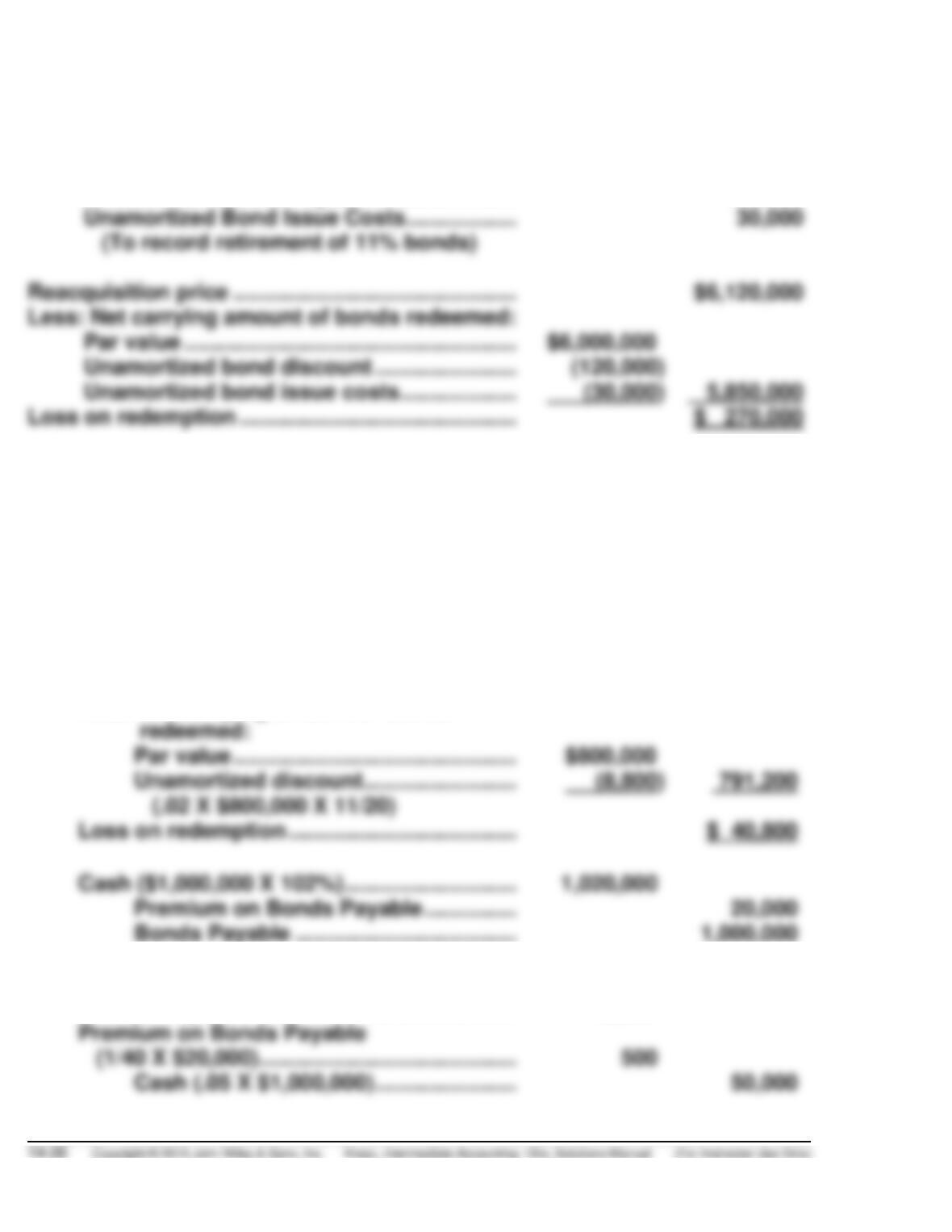

Reacquisition price ($900,000 X 101%)

$909,000

Less: Net carrying amount of bonds redeemed:

Par value

Unamortized discount

(13,500)

Unamortized bond issue costs

Loss on redemption

$ 29,700

Calculation of unamortized discount—

Original amount of discount:

$900,000 X 3% = $27,000

$27,000/10 = $2,700 amortization per year

Amount of discount unamortized:

$2,700 X 5 = $13,500

Calculation of unamortized bond issue costs—

Original amount of costs:

$24,000 X $900,000/$1,500,000 = $14,400

$14,400/10 = $1,440 amortization per year

Amount of costs unamortized:

$1,440 X 5 = $7,200

January 2, 2014

Bonds Payable ……………………………………………………….

900,000

Loss on Redemption of Bonds …………………………..

29,700

Unamortized Bond Issue Costs ……………………….

Discount on Bonds Payable …………………………..

Cash ……………………………………………………….

EXERCISE 14-13 (15–20 minutes)

Cash ………………………………………………………………………

8,820,000

Discount on Bonds Payable (.02 X $9,000,000) ………….

180,000

Bonds Payable ……………………………………………….

(To record issuance of 10% bonds)

EXERCISE 14-13 (Continued)

Bonds Payable ……………………………………………………….

6,000,000

Loss on Redemption of Bonds …………………………..

270,000

Cash ($6,000,000 X 1.02) …………………………..

6,120,000

Discount on Bonds Payable …………………………..

120,000

Unamortized Bond Issue Costs ………………………..

30,000

(To record retirement of 11% bonds)

Reacquisition price …………………………………………………

Less: Net carrying amount of bonds redeemed:

Par value ……………………………………………………….

Unamortized bond discount …………………………..

Unamortized bond issue costs …………………………

EXERCISE 14-14 (12–16 minutes)

(a)

June 30, 2015

Bonds Payable ……………………………………………………….

800,000

Loss on Redemption of Bonds …………………………..

40,800

Discount on Bonds Payable …………………………..

8,800

Cash ……………………………………………………….

832,000

Reacquisition price ($800,000 X 104%) ……………………..

$832,000

Par value ……………………………………………………….

Unamortized discount …………………………..

(.02 X $800,000 X 11/20)

Cash ($1,000,000 X 102%) …………………………..

Premium on Bonds Payable …………………………..

Bonds Payable ……………………………………………….

Less: Net carrying amount of bonds

(b)

December 31, 2015

Interest Expense …………………………………………………….

49,500

Premium on Bonds Payable

EXERCISE 14-15 (10–15 minutes)

Reacquisition price ($300,000 X 104%) ……………………..

$312,000

Less: Net carrying amount of bonds redeemed:

Par value ………………………………………………………

$300,000

Unamortized discount ……………………………………

(10,000)

290,000

Loss on redemption ………………………………………………..

$ 22,000

Bonds Payable ……………………………………………………….

300,000

Loss on Redemption of Bonds …………………………..

Discount on Bonds Payable …………………………..

(To record redemption of bonds

payable)

Cash ($300,000 X 1.03) …………………………..………………..

306,000

Unamortized Bond Issue Costs…………………………..

Premium on Bonds Payable …………………………..

Bonds Payable ……………………………………………….

(To record issuance of new bonds)

EXERCISE 14-16 (15–20 minutes)

(a)

1.

January 1, 2014

Land ……………………………………………………….

200,000.00

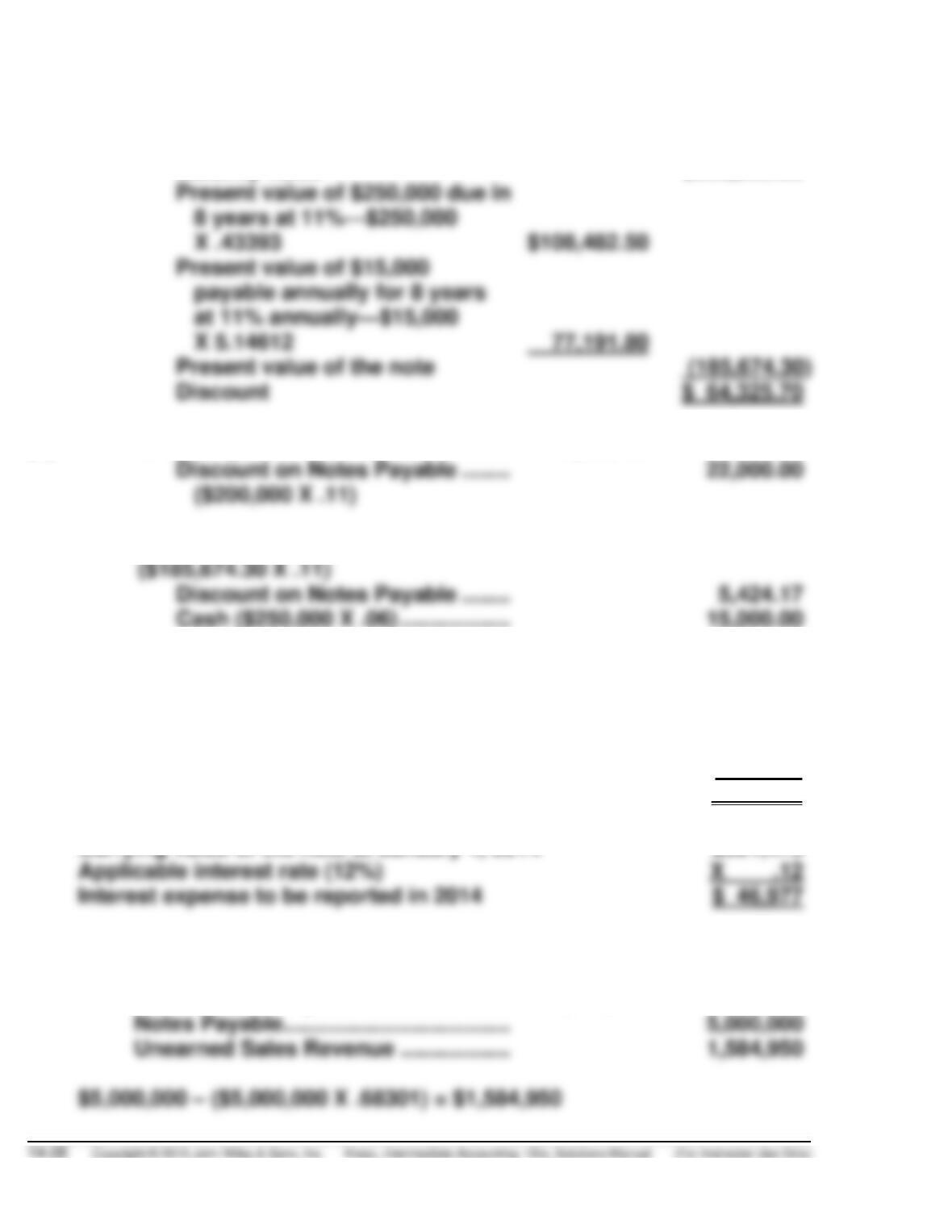

Discount on Notes Payable …………………………..

137,012.00

Notes Payable…………………………………………………

(The $200,000 capitalized land

cost represents the present

value of the note discounted

for five years at 11%.)

2.

Equipment……………………………………………………….

185,674.30

Discount on Notes Payable …………………………..

Notes Payable…………………………………………………

EXERCISE 14-16 (Continued)

*Computation of the discount on

notes payable:

Maturity value

$250,000.00

Present value of $250,000 due in

8 years at 11%—$250,000

X .43393

Present value of $15,000

payable annually for 8 years

at 11% annually—$15,000

X 5.14612

Present value of the note

Discount

(b)

1.

Interest Expense ……………………………………………………..

22,000.00

Discount on Notes Payable …………………………..

($200,000 X .11)

2.

Interest Expense ……………………………………………………..

20,424.17

($185,674.30 X .11)

Discount on Notes Payable …………………………..

Cash ($250,000 X .06) …………………………..

EXERCISE 14-17 (15–20 minutes)

(a)

Face value of the zero-interest-bearing note

$550,000

Discount factor (12% for 3 periods)

X .71178

Amount to be recorded for the land at January 1, 2014

$391,479

Carrying value of the note at January 1, 2014

$391,479

Applicable interest rate (12%)

(b)

January 1, 2014

Cash ……………………………………………………….

5,000,000

Discount on Notes Payable …………………………..

1,584,950

Notes Payable…………………………………………………

Unearned Sales Revenue …………………………..

EXERCISE 14-17 (Continued)

Carrying value of the note

at January 1, 2014

Applicable interest rate (10%)

Interest expense to be

**$5,000,000 – $1,584,950 = $3,415,050

EXERCISE 14-18 (15–20 minutes)

(a)

Cash ……………………………………………………….

400,000

Discount on Notes Payable …………………………..

82,468

Notes Payable ………………………………………………..

400,000

Unearned Sales Revenue …………………………..

82,468

($400,000 – $317,532)

Face value

(b)

Interest Expense ($317,532 X 8%) …………………………..

25,403

Discount on Notes Payable …………………………..

25,403

Unearned Sales Revenue ($82,468 ÷ 3)

27,489

Sales ……………………………………………………….

27,489

EXERCISE 14-19 (10–15 minutes)

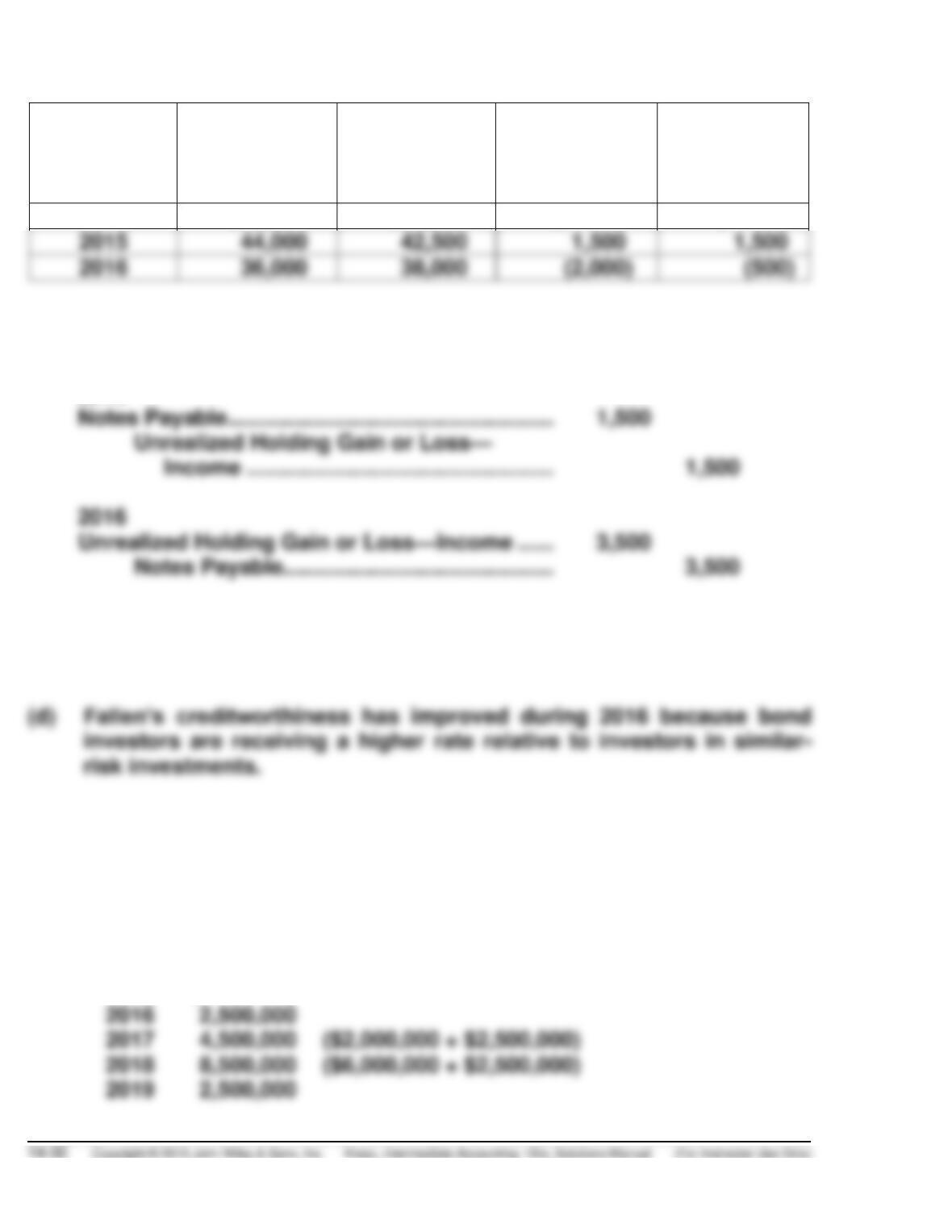

Year Ending

Carrying

Value

Fair Value

Unrealized

Holding Gain

or Loss

Change in

Unrealized

Holding

Gain or Loss

2014

$54,000

$54,000

$ 0

$ 0

2016

(a)

2014

No Entry (Carrying value = Fair Value)

2015

Notes Payable ……………………………………………………….

Unrealized Holding Gain or Loss—Income ……………….

Notes Payable……………………………………..

(b) The fair value of $42,500.

(c) Unrealized holding loss of $3,500.

EXERCISE 14-20 (10–15 minutes)

At December 31, 2014, disclosures would be as follows:

Maturities and sinking fund requirements on long-term debt are as follows:

2015

$ 0

2016

($2,000,000 + $2,500,000)

*EXERCISE 14-21 (15–20 minutes)

(a)

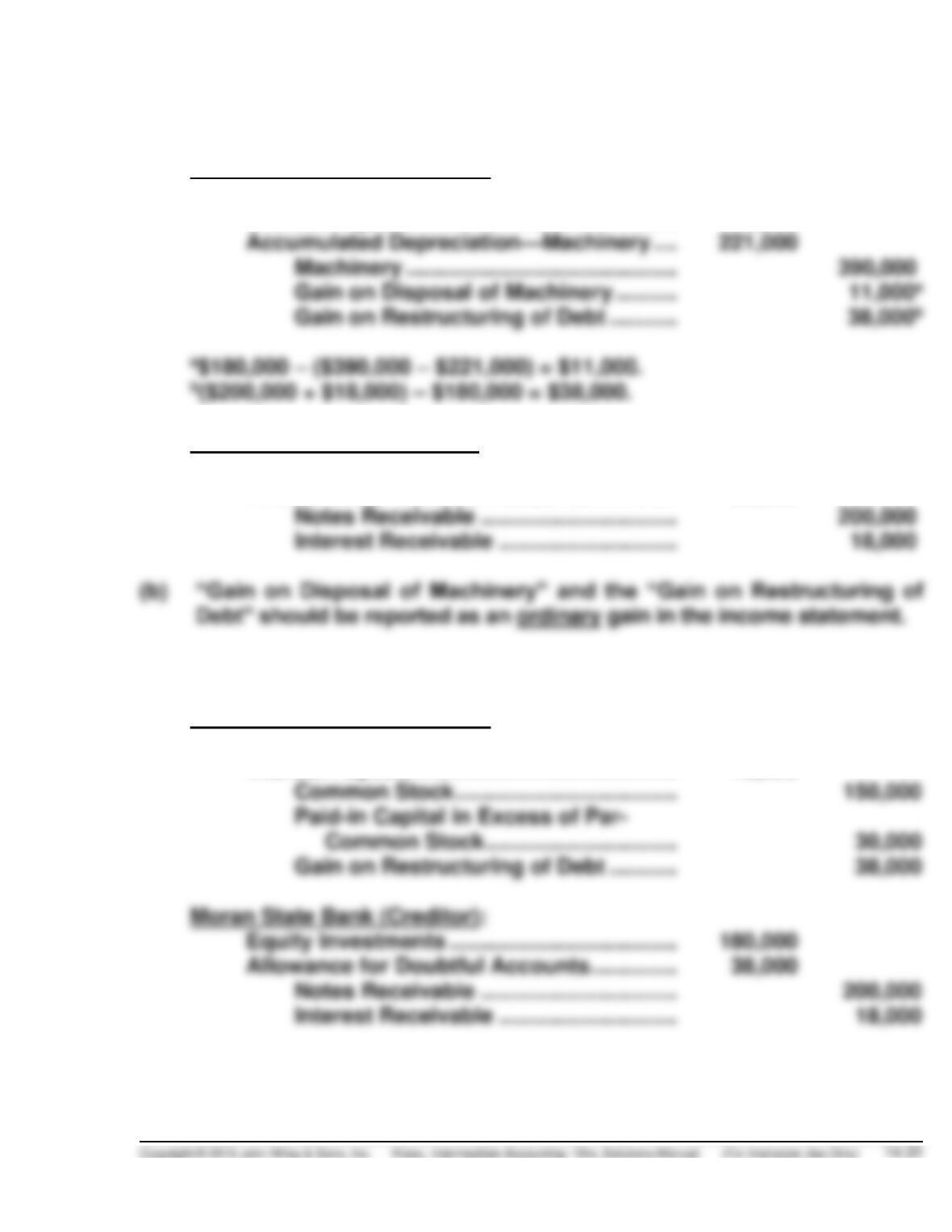

Transfer of property on December 31, 2014:

Strickland Company (Debtor):

Notes Payable ………………………………………………..

200,000

Interest Payable ……………………………………………..

18,000

Accumulated Depreciation—Machinery ……………

221,000

Machinery ……………………………………………….

390,000

Gain on Disposal of Machinery …………………

Gain on Restructuring of Debt ………………….

Moran State Bank (Creditor):

Machinery ………………………………………………………

180,000

Allowance for Doubtful Accounts …………………….

38,000

Notes Receivable …………………………………….

200,000

Interest Receivable …………………………..

(c)

Granting of equity interest on December 31, 2014:

Strickland Company (Debtor):

Notes Payable ………………………………………………..

200,000

Interest Payable ……………………………………………..

18,000

Common Stock ………………………………………..

Gain on Restructuring of Debt ………………….

Moran State Bank (Creditor):

Equity Investments …………………………………………

180,000

Allowance for Doubtful Accounts …………………….

Notes Receivable …………………………………….

Interest Receivable …………………………..

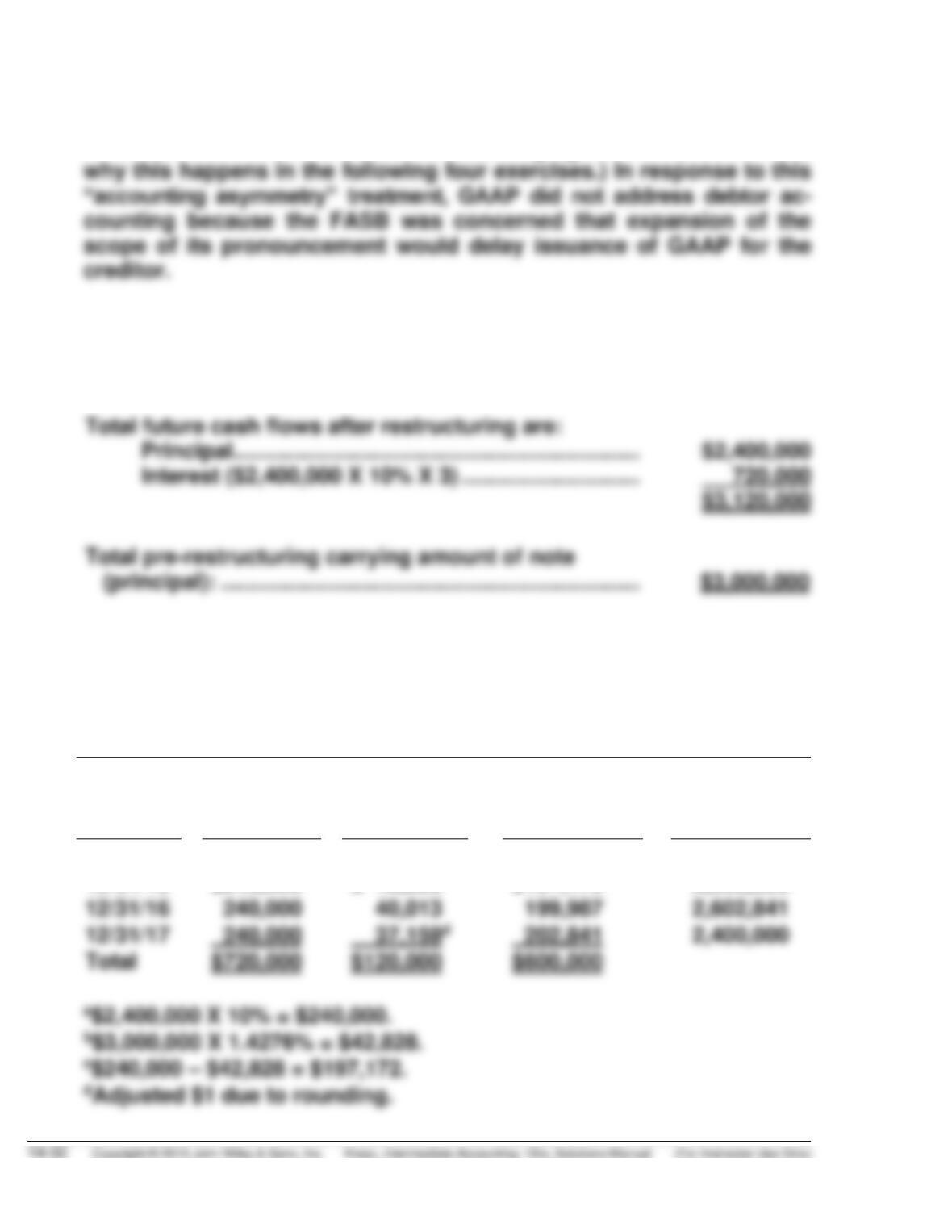

*EXERCISE 14-22 (20–30 minutes)

(a) No. The gain recorded by Barkley is not equal to the loss recorded by

American Bank under the debt restructuring agreement. (You will see

(b) No. There is no gain under the modified terms because the total future

cash flows after restructuring exceed the total pre–restructuring carrying

amount of the note (principal):

(c) The interest payment schedule is prepared as follows:

BARKLEY COMPANY

Interest Payment Schedule After Debt Restructuring

Effective-Interest Rate 1.4276%

Date

Cash

Paid

(10%)

Interest

Expense

(1.4276%)

Reduction

of Carrying

Amount

Carrying

Amount of

Note

12/31/14

$3,000,000

12/31/15

$240,000a

$ 42,828b

$197,172c

2,802,828

12/31/16

240,000

40,013

199,987

2,602,841

12/31/17

*EXERCISE 14-22 (Continued)

(d)

Interest payment entry for Barkley Company is:

December 31, 2016

Notes Payable ……………………………………………………….

Interest Expense …………………………………………………….

Cash ……………………………………………………….

(e)

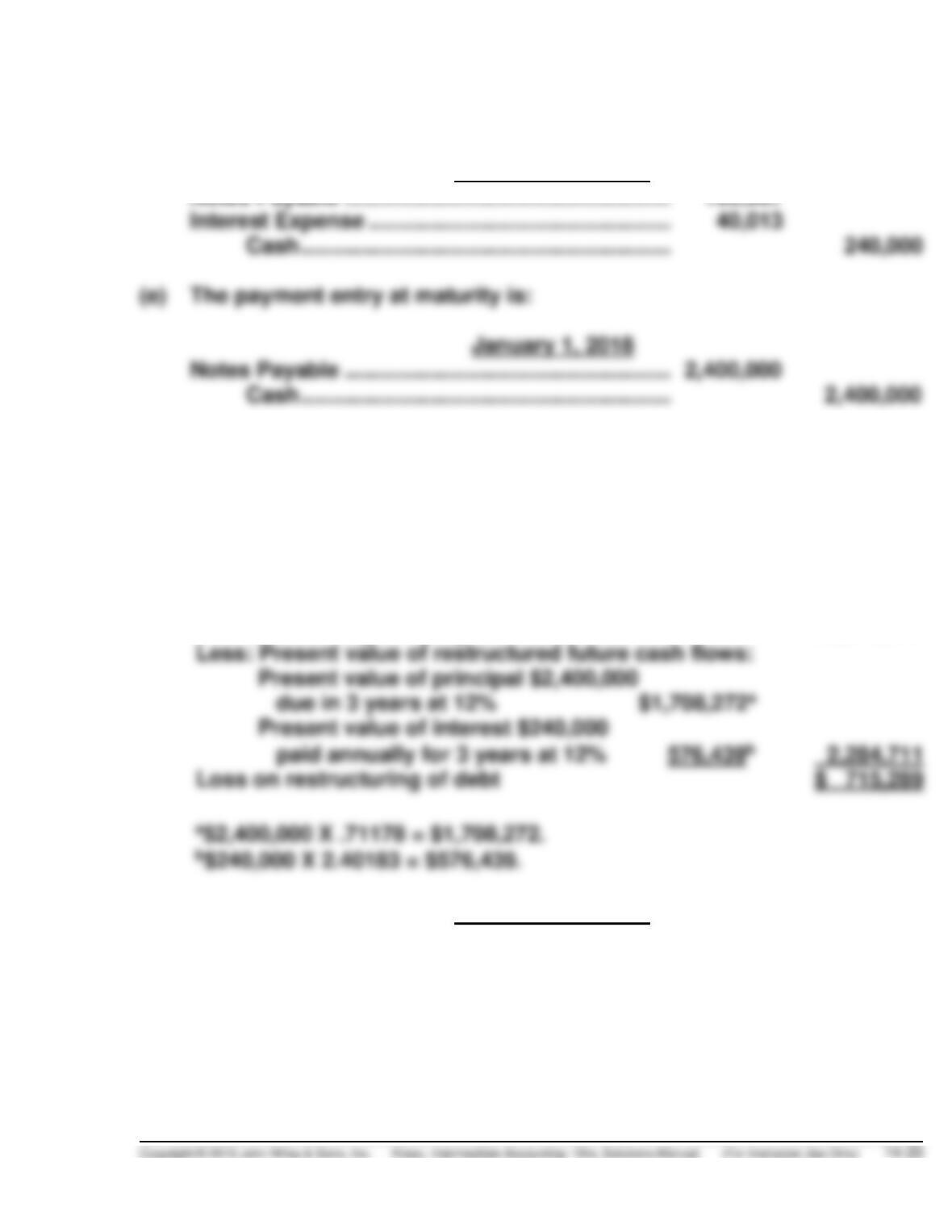

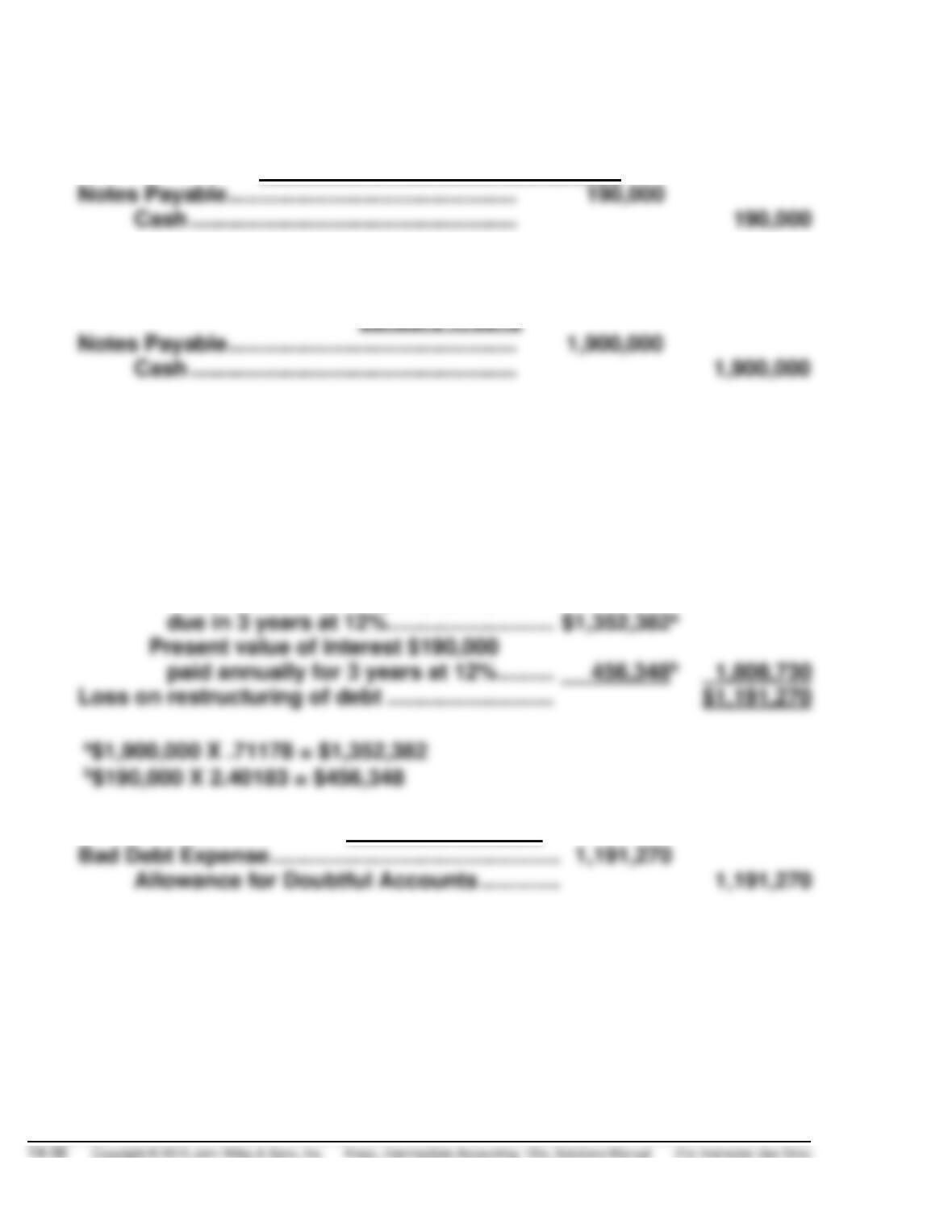

The payment entry at maturity is:

Notes Payable ……………………………………………………….

2,400,000

Cash ……………………………………………………….

*EXERCISE 14-23 (25–30 minutes)

(a) American Bank should use the historical interest rate of 12% to

calculate the loss.

(b)

The loss is computed as follows:

Pre-restructuring carrying amount of note

$3,000,000

Less: Present value of restructured future cash flows:

Present value of principal $2,400,000

due in 3 years at 12%

paid annually for 3 years at 12%

December 31, 2014

Bad Debt Expense …………………………………………………..

715,289

Allowance for Doubtful Accounts …………………….

715,289

*EXERCISE 14-23 (Continued)

(c) The interest receipt schedule is prepared as follows:

AMERICAN BANK

Interest Receipt Schedule After Debt Restructuring

Effective-Interest Rate 12%

Date

Cash

Received

(10%)

Interest

Revenue

(12%)

Increase

in Carrying

Amount

Carrying

Amount of

Note

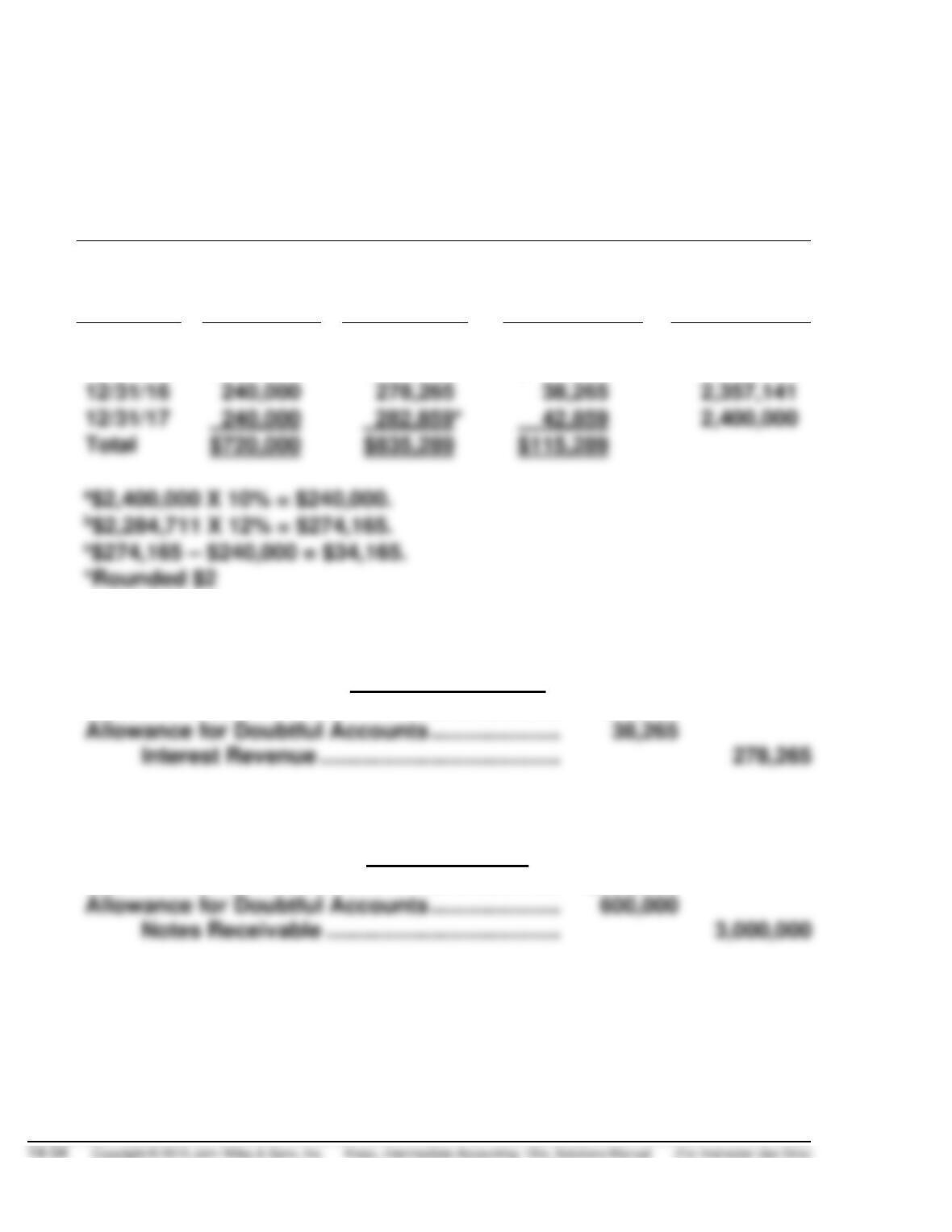

12/31/14

$2,284,711

12/31/15

$240,000a

$274,165b

$ 34,165c

2,318,876

12/31/16

12/31/17

(d)

Interest receipt entry for American Bank is:

December 31, 2016

Cash ………………………………………………………………………

240,000

Allowance for Doubtful Accounts …………………………..

Interest Revenue …………………………………………….

(e)

The receipt entry at maturity is:

January 1, 2018

Cash ………………………………………………………………………

2,400,000

Allowance for Doubtful Accounts …………………………..

Notes Receivable …………………………..……………….

*EXERCISE 14-24 (25–30 minutes)

(a) Yes. Barkley Company can record a gain under this term modification.

The gain is calculated as follows:

Total future cash flows after restructuring are:

Principal ……………………………………………………….

$1,900,000

Interest ($1,900,000 X 10% X 3) ………………..

570,000

$2,470,000

Therefore, the gain = $3,000,000 – $2,470,000 = $530,000.

(b)

The entry to record the gain on December 31, 2014:

Notes Payable ………………………………………………..

530,000

Gain on Restructuring of Debt ………………….

530,000

(c)

Because the new carrying value of the note ($3,000,000 – $530,000 =

(d) The interest payment schedule is prepared as follows:

BARKLEY COMPANY

Interest Payment Schedule After Debt Restructuring

Effective-Interest Rate 0%

Date

Cash

Paid

(10%)

Interest

Expense

(0%)

Reduction

of Carrying

Amount

Carrying

Amount of

Note

12/31/14

$2,470,000

Total

*EXERCISE 14-24 (Continued)

(e)

Cash interest payment entries for Barkley Company are:

December 31, 2015, 2016, and 2017

Notes Payable ……………………………………………………….

Cash ……………………………………………………….

(f)

The payment entry at maturity is:

January 1, 2018

Notes Payable ……………………………………………………….

Cash ……………………………………………………….

*EXERCISE 14-25 (20–30 minutes)

(a)

The loss can be calculated as follows:

Pre-restructuring carrying amount of note ……………….

$3,000,000

Less: Present value of restructured future

cash flows:

Present value of principal $1,900,000

due in 3 years at 12% …………………………..

Present value of interest $190,000

paid annually for 3 years at 12% ………………….

December 31, 2014

Bad Debt Expense …………………………………………………..

Allowance for Doubtful Accounts …………………….

*EXERCISE 14-25 (Continued)

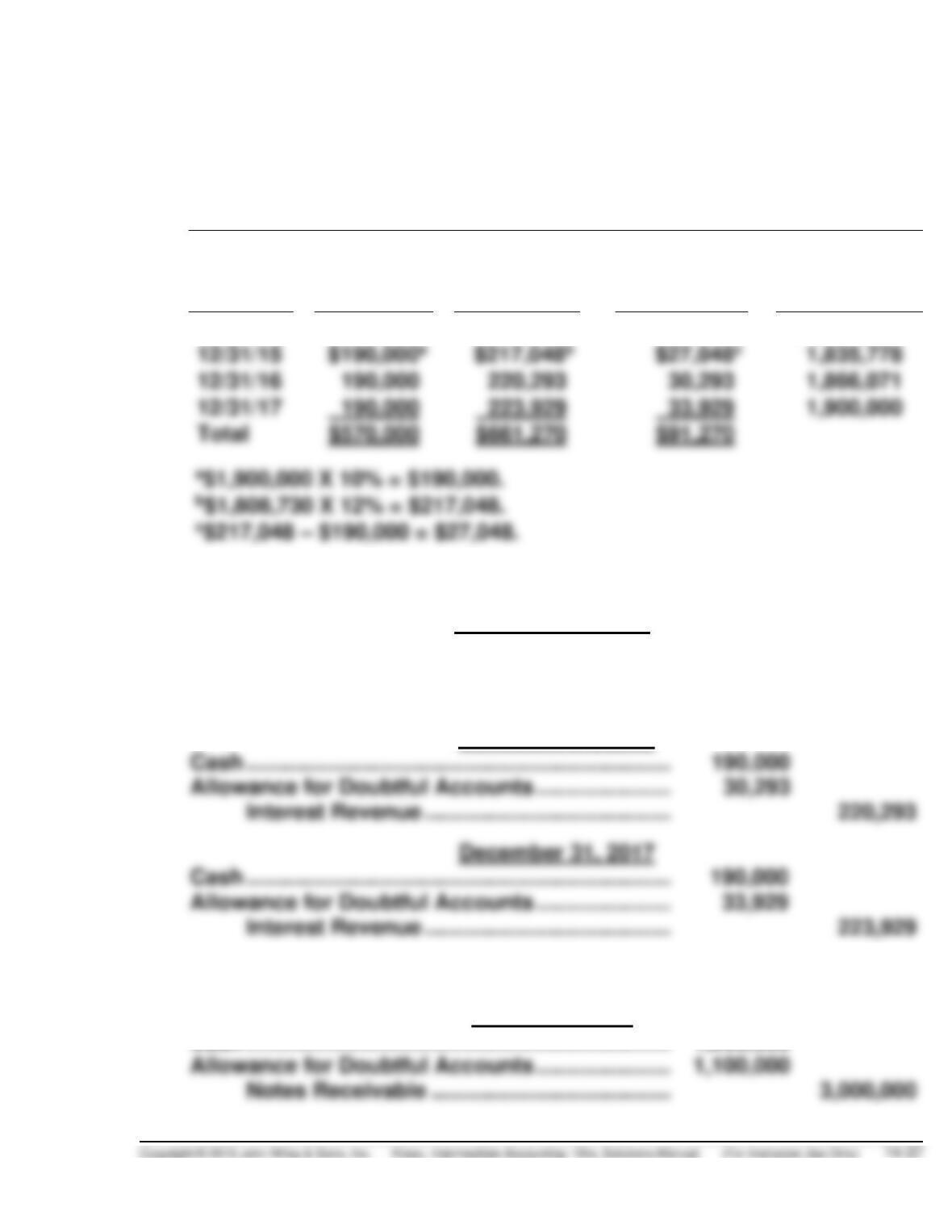

(b) The interest receipt schedule is prepared as follows:

AMERICAN BANK

Interest Receipt Schedule After Debt Restructuring

Effective-Interest Rate 12%

Date

Cash

Received

(10%)

Interest

Revenue

(12%)

Increase

in Carrying

Amount

Carrying

Amount of

Note

12/31/14

$1,808,730

12/31/17

(c)

Interest receipt entries for American Bank are:

December 31, 2015

Cash ………………………………………………………………………

190,000

Allowance for Doubtful Accounts …………………………..

27,048

Interest Revenue …………………………………………….

217,048

December 31, 2016

Cash ………………………………………………………………………

Allowance for Doubtful Accounts …………………………..

Interest Revenue …………………………………………….

Cash ………………………………………………………………………

Interest Revenue …………………………………………….

223,929

(d)

The receipt entry at maturity is:

January 1, 2018

Cash ………………………………………………………………………

1,900,000

Notes Receivable …………………………..……………….

*EXERCISE 14-26 (15–20 minutes)

(a)

Gottlieb Co.’s entry:

Notes Payable ……………………………………………………….

199,800

Land ……………………………………………………….

Gain on Disposal of Plant Assets

($140,000 – $90,000) …………………………..

Gain on Restructuring of Debt …………………………

*$199,800 – $140,000

(b)

Ceballos Inc. entry:

Land ………………………………………………………………………

140,000

Allowance for Doubtful Accounts …………………………..

Notes Receivable ……………………………………………

*EXERCISE 14-27 (20–25 minutes)

Because the carrying amount of the debt, $270,000 exceeds the total future

cash flows $242,000 [$220,000 + ($11,000 X 2)], a gain and a loss are

recognized and no interest is recorded by the debtor.

(a)

Vargo Corp.’s entries:

2014 Notes Payable…………………………………………………

28,000

Gain on Restructuring of Debt ………………….

28,000

2015 Notes Payable…………………………………………………

Cash (5% X $220,000) …………………………..

11,000

2016 Notes Payable…………………………………………………

Cash

[$220,000 + (5% X $220,000)] ………………….

*EXERCISE 14-27 (Continued)

(b)

First Trust’s entry on December 31, 2014:

Bad Debt Expense …………………………………………………..

76,027

Allowance for Doubtful Accounts …………………….

76,027

Pre-restructure carrying amount

$270,000

Present value of restructured cash flows:

Present value of $220,000 due in 2 years

at 12%, interest payable annually

(Table 6-2); ($220,000 X .79719) …………………….

Present value of $11,000 interest payable

annually for 2 years at 12% (Table 6-4);

($11,000 X 1.69005) ………………………………………

Date

Cash

Interest

Effective-

Interest

Increase

in Carrying

Amount

Carrying

Amount of

Note

12/31/14

$193,973

12/31/16

13,750

December 31, 2015

Cash ………………………………………………………………………

11,000

Allowance for Doubtful Accounts …………………………..

12,277

Interest Revenue …………………………………………….

23,277

December 31, 2016

Cash ………………………………………………………………………

11,000

Allowance for Doubtful Accounts …………………………..

13,750

Interest Revenue …………………………………………….

Cash ………………………………………………………………………

Allowance for Doubtful Accounts …………………………..

TIME AND PURPOSE OF PROBLEMS

Problem 14-1 (Time 15–20 minutes)

Purpose—to provide the student with the opportunity to interpret a bond amortization schedule. This

Problem 14-2 (Time 25–30 minutes)

Problem 14-3 (Time 20–30 minutes)

Purpose—to provide the student with an understanding of how interest rates can be used to deceive

a customer. The problem is challenging because for the first year of this transaction, negative amortization

results.

Problem 14-4 (Time 15–20 minutes)

Purpose—to provide the student with an understanding of the relevant journal entries which are necessi–

Problem 14-5 (Time 50–65 minutes)

Purpose—to provide the student with an understanding of the relevant journal entries which are neces-

Problem 14-6 (Time 20–25 minutes)

Purpose—to provide the student with an understanding of the relevant journal entries which are

Problem 14-7 (Time 20–25 minutes)

Purpose—to provide the student with a series of transactions from bond issuance, payment of bond

interest, accrual of bond interest, amortization of bond discount, and bond retirement. Journal entries

are required for each of these transactions.

Problem 14-8 (Time 15–25 minutes)

Purpose—to provide the student with an opportunity to become familiar with the application of GAAP,