ACCOUNTING, ANALYSIS, AND PRINCIPLES

Accounting

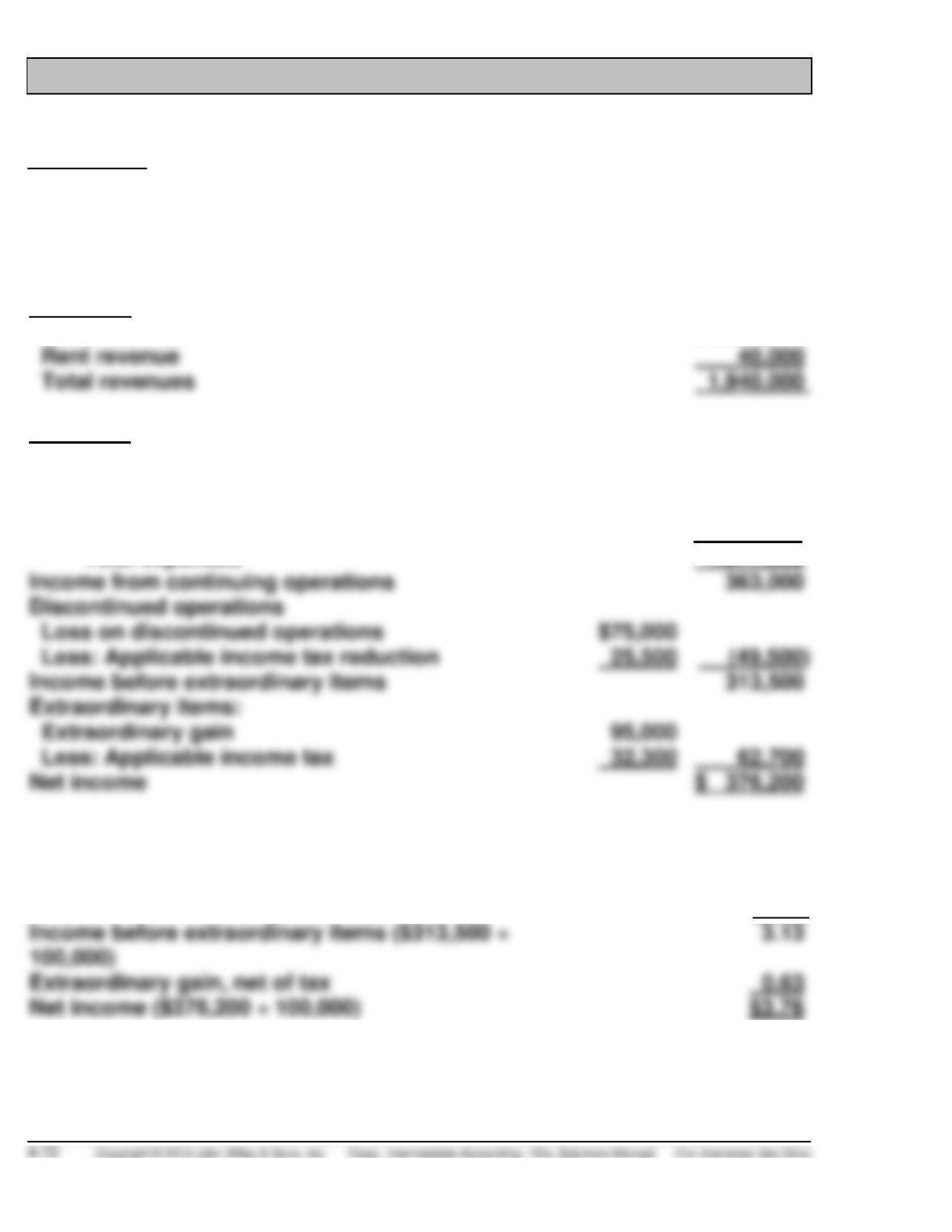

COUNTING CROWS, INC.

Income Statement

For the Year Ending December 31, 2014

Revenues

Sales revenue

$1,900,000

Rent revenue

40,000

Expenses

Cost of goods sold

850,000

Selling expenses

300,000

Administrative expenses

240,000

Income tax expense

187,000

Total expenses

1,577,000

Income from continuing operations

363,000

Discontinued operations

Loss on discontinued operations

$75,000

Less: Applicable income tax reduction

25,500

Income before extraordinary items

313,500

Extraordinary items:

Less: Applicable income tax

32,300

Net income

$ 376,200

Per share of common stock:

Income from continuing operations ($363,000 ÷

100,000)

$3.63

Loss on discontinued operations, net of tax

(0.50)

Extraordinary gain, net of tax

Net income ($376,200 ÷ 100,000)

ACCOUNTING, ANALYSIS, AND PRINCIPLES (Continued)

COUNTING CROWS, INC.

Retained Earnings Statement

For the Year ended December 31, 2014

Retained earnings, January 1

$600,000

Net income

376,200

Dividends declared

Retained earnings, December 31

$896,200

Net income

$376,200

Other comprehensive income:

Unrealized holding gain, net of tax

15,000

Comprehensive income

$391,200

Analysis

The multiple-step income statement recognizes important relationships

between income statement elements. For example, by separating operating

transactions from nonoperating transactions, the statement user can

Principles

Pro forma reporting is inconsistent with the conceptual framework’s qualita–

tive characteristic of comparability. For example, similar to the discussion

PROFESSIONAL RESEARCH

(a) FASB ASC 220 – Presentation, Comprehensive Income. The predecessor

standard for this topic is FAS No. 130 Reporting Comprehensive Income

(b) The definition of comprehensive income (Master Glossary of ASC):

The change in equity (net assets) of a business entity during a period

(c) Classifications within net income and examples (FASB ASC 220-10–45–7):

45-7 [Items included in net income are displayed in various

(d) The classifications within other comprehensive income (220–10–45–13):

45–13 [Items included in other comprehensive income shall be classified

based on their nature. For example, other comprehensive income

shall be classified separately into foreign currency items, gains

PROFESSIONAL RESEARCH (Continued)

(e) Reclassification adjustments (FASB ASC 220-10–45-15)

45–15 Reclassification adjustments shall be made to avoid double

counting in comprehensive income items that are displayed as

part of net income for a period that also had been displayed

as part of other comprehensive income in that period or earlier

PROFESSIONAL SIMULATION

Explanation

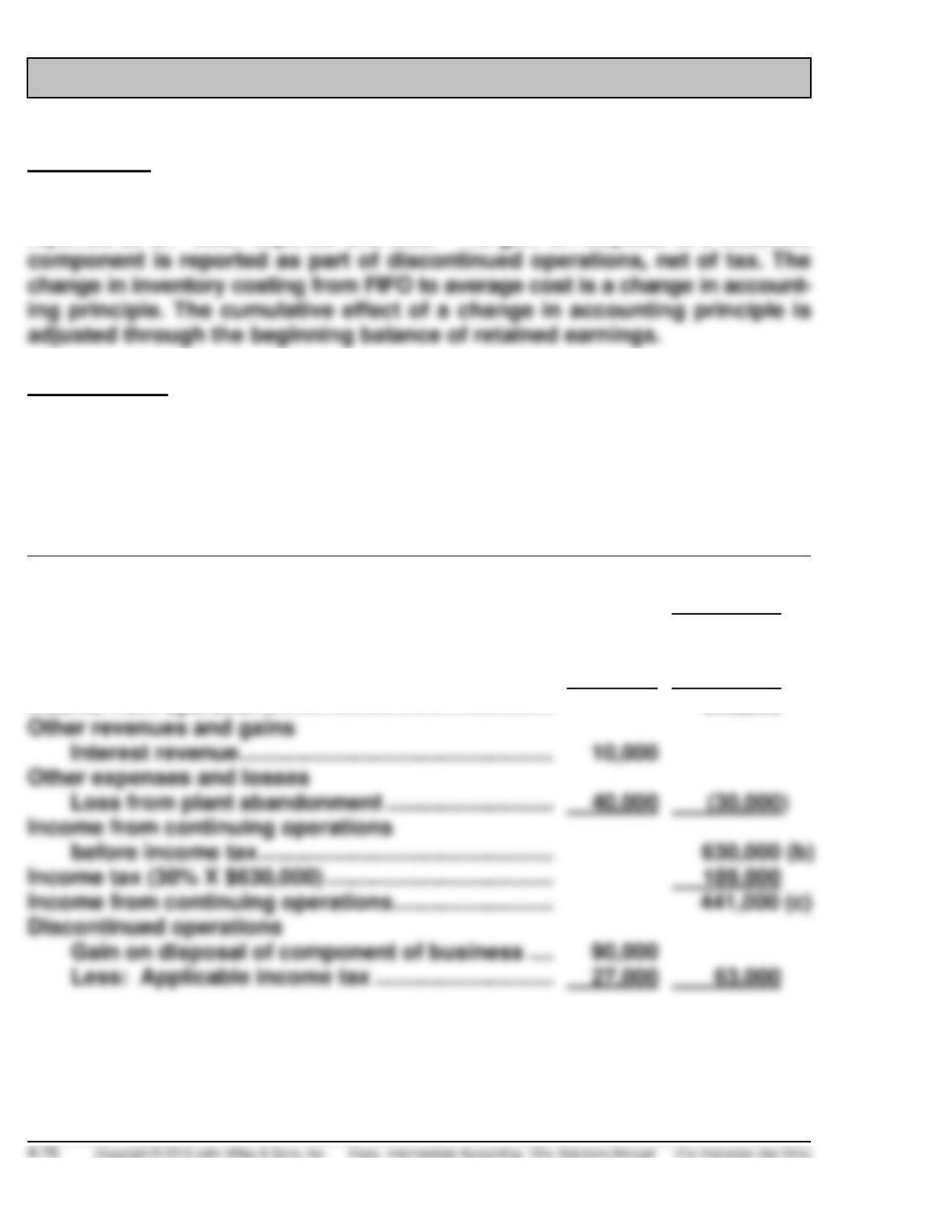

As indicated in the income statement below, the loss on abandonment is

reported as an “other expense and loss.” The gain on disposal of a business

Measurement

Answers are revealed in the income statement below.

JUDE LAW CORPORATION

Income Statement

For the Year Ended December 31, xxxx

Sales ………………………………………………………………….

$3,200,000

Cost of goods sold ……………………………………………..

1,920,000

Gross profit ………………………………………………………..

1,280,000 (a)

Selling expenses ………………………………………………..

$340,000

Administrative expenses …………………………………….

280,000

620,000

Income from operations ………………………………………

660,000

Other revenues and gains

Interest revenue ……………………………………………

Other expenses and losses

Loss from plant abandonment ………………………

40,000

Income tax (30% X $630,000) ……………………………….

Discontinued operations

Gain on disposal of component of business ….

Less: Applicable income tax ………………………..

63,000

PROFESSIONAL SIMULATION (Continued)

Income before extraordinary item ………………………………

504,000

Extraordinary item

Loss from earthquake ……………………………………….

40,000

Less: Applicable income tax ……………………………..

12,000

Net income ……………………………………………………………….

Per share of common stock

Income from continuing operations ………………………..

Discontinued operations, net of tax ………………………..

.63

Income before extraordinary item …………………………..

Extraordinary item, loss from earthquake, net of tax …..

Net income ……………………………………………………….

$4.76 (e)

Note to instructor: The change for inventory costing is reflected in the

current year’s cost of goods sold. If comparative statements are presented,

IFRS CONCEPTS AND APPLICATION

IFRS4-1

Companies are required to present an analysis of expenses classified

IFRS4-2

(a) A loss on discontinued operations is reported, net of tax in a separate

section between income from continuing operations and net income.

item of income or expense).

IFRS4-3

Bradshaw should report this item similar to other unusual gains and losses.

IFRS4-4

Sales revenue ……………………………………………………….

$310,000

Cost of goods sold ……………………………………………………….

140,000

Selling and administrative expenses …………………………..

50,000

Gain on sale of plant assets ……………………………………………

Income from operations …………………………..……………………..

150,000

(a)

Interest expense ……………………………………………………….

Income from continuing operations …………………………..

144,000

Discontinued operations …………………………………………………

Net income …………………………..…………………………..

Attributable to:

Non–controlling interest ………………………………………………..

(40,000)

Controlling shareholders ………………………………………………

92,000

(c)

142,000

(d)

IFRS4-5

(a) Some of the differences are:

1. Units of currency—Avon reports in pounds sterling and Earnings

per share in pence.

2. Terminology—Interest revenue and expense are referred to as

3. Avon provides a breakout of operating profit into before exceptional

items and exceptional items in 2010. The details for these items

IFRS4-5 (Continued)

(b) Both the “Exceptional items” and the “Discontinued operations” are

example of irregular items. As in the U.S., these items are included in

IFRS4-6

(a) International Accounting Standard 1, Presentation of Financial

Statements addresses the statement of comprehensive income

(b) Total comprehensive income is the change in equity during a period

resulting from transactions and other events, other than those

(c) Paragraphs 85 and 86 provide the rationale for presenting additional

information: An entity shall present additional line items, headings

IFRS4-6 (Continued)

Because the effects of an entity’s various activities, transactions and

other events differ in frequency, potential for gain or loss and

predictability, disclosing the components of financial performance

assists users in understanding the financial performance achieved

and in making projections of future financial performance. An entity

(d) When items of income or expense are material, an entity shall disclose

their nature and amount separately (Para. 97). Circumstances that

would give rise to the separate disclosure of items of income and

expense include:

a. write-downs of inventories to net realisable value or of property,

plant and equipment to recoverable amount, as well as reversals

of such write-downs;

IFRS4-7

(a) M&S uses a condensed format income statement. This format provides

highlights of a company’s performance without presenting unnecessary

detailed computations.

(d) M&S reports operating profit separately from nonoperating profit

because nonoperating profit is non-recurring and not expected to

(e) M&S did report Non-GAAP measures. The adjusted profit and earnings

per share measures provide additional useful information for share–

holders on the underlying performance of the business.

M&S provided the following disclosure:

Non-GAAP performance measures

The directors believe that the underlying profit and earnings per share

—profits and losses on the disposal of properties;

—significant and one-off impairment charges that distort underlying

trading;