CHAPTER 12

SOLUTIONS TO B EXERCISES

E12-1B (15–20 minutes)

(a) 1, 2, 3, 5, 9, 15, 17

(b) 4. Long-term investments, or other assets, in the balance sheet.

6. Expensed in the income statement.

7. Research and development expense in the income statement.

8. Research and development expense in the income statement.

10. Research and development expense in the income statement.

11. Property, plant, and equipment in the balance sheet.

E12-2B (10–15 minutes)

The following items would be classified as intangible assets:

Cable television franchises Film contract rights

E12-2B (Continued)

The following would be classified as current assets:

Cash Notes receivable

Accounts receivable Prepaid expenses

The following would be classified as non-current assets in the property, plant,

and equipment section:

The following would be classified as an operating expense:

Research and development costs

E12-3B (10–15 minutes)

(a)

Trademarks …………………………………………………………….

$150,000

Excess of cost over fair value of net assets of

acquired subsidiary (goodwill) ………………………………

E12-3B (Continued)

Deposits with advertising agency for ads to promote goodwill of company,

$25,000, should be reported either as an expense or as prepaid advertising in

the current assets section. Advertising costs in general are expensed when

E12-4B (15–20 minutes)

1. Tartabull should report the patent at $1,280,000 (net of $720,000 accu–

mulated amortization) on the balance sheet. The computation of accumu–

2. Tartabull should amortize the franchise over its estimated useful life.

Because it is uncertain that Tartabull will be able to retain the franchise at

3. These costs should be expensed as incurred (all in 2013).

4. Because the license can be easily renewed (at nominal cost), it has an

E12-5B (15–20 minutes)

Research and Development Expense ………………………..

1,160,000

Patents ……………………………………………………………………

30,000

Income Summary (or a loss account) ………………………..

86,000

Interest Expense ………………………………………………..

Paid in Capital in Excess of Par on Common Stock …..

Intangible Assets …………………………..…………………..

Patents (or Accumulated Amortization) …………….

E12-6B (15–20 minutes)

Patents …………………………………………………………………..

525,000

Goodwill …………………………..…………………………………….

540,000

Franchise …………………………..…………………………………..

675,000

Copyright ……………………………………………………………….

234,000

Research and Development Expense ……………………….

322,500

Intangible Assets …………………………………………….

Amortization Expense ……………………………………………..

118,875

Patents ($525,000/8) ………………………………………..

Franchise ($675,000/10 X 6/12) ………………………..

Copyright ($234,000/5 X 5/12) ………………………….

E12-7B (10–15 minutes)

(a) 2013 amortization: $50,000 ÷ 10 = $5,000

12/31/13 book value: $50,000 – $5,000 = $45,000

2014 amortization: ($45,000 + $20,000) ÷ 9 = $7,222

12/31/14 book value: ($45,000 + $20,000 – $7,222) = $57,778

E12-8B (10–15 minutes)

(a)

Attorney’s fees in connection with organization

of the company ………………………………………………………

$26,000

Costs of meetings of incorporators to discuss

State filing fees to incorporate …………………………………..

1,000

(b)

Organization Cost Expense ……………………………………..

44,000

Cash (Payables) ………………………………………………

E12-9B (15–20 minutes)

(a) YOUNT COMPANY

Intangibles Section of Balance Sheet

December 31, 2014

amortization of $280,000 (Schedule 1) …………………………….

amortization of $96,000 (Schedule 2) ………………………………

864,000

Patent from Ford Company, net of accumulated

Schedule 1 Computation of patent from Ford Company:

Cost of patent at date of purchase …………………………………….

$1,000,000

Amortization of patent for 2013 ($1,000,000 ÷ 10 years) …………

Amortization of patent for 2014 ($900,000 ÷ 5 years) …………..

Schedule 2 Computation of franchise from Reagan Company:

Cost of franchise at date of purchase ………………………………..

Amortization of franchise for 2014 ($960,000 ÷ 10) ……………..

(b) YOUNT COMPANY

Income Statement Effect

For the year ended December 31, 2014

Patent from Ford Company:

Amortization of patent for 2014

($900,000 ÷ 5 years) ……………………………………..

Franchise from Reagan Company:

Amortization of franchise for 2014

($960,000 ÷ 10) ……………………………………………..

($5,000,000 X 5%) …………………………………………

Research and development costs ……………………………..

E12-10B (15–20 minutes)

(a)

2010

Research and Development Expense ……………………….

510,000

Cash ………………………………………………………………

510,000

Patents ……………………………………………………….………….

Cash ………………………………………………………………

Patent Amortization Expense …………………………………..

Patents [($54,000 ÷ 10) X 3/12] …………………………

Patent Amortization Expense …………………………………..

Patents ($54,000 ÷ 10) ……………………………………..

(b)

2012

Patents ……………………………………………………….………….

28,440

Cash ………………………………………………………………

28,440

Patent Amortization Expense …………………………………..

5,820

Patents ($2,250 + $3,570) …………………………………

5,820

[Jan. 1—June 1: ($54,000 ÷ 10)

X 5/12 = $2,250

$5,400 – $2,250 + $28,440) = $73,440;

($73,440 ÷ 12) X 7/12 = $3,570]

2013

Patent Amortization Expense …………………………………..

6,120

Patents ($73,440 ÷ 12) ……………………………………..

6,120

(c)

2014 and 2015

Patent Amortization Expense …………………………………..

31,875

Patents ($63,750 ÷ 2) …………………………..…………..

31,875

($73,440 – $3,570 – $6,120) = $63,750

E12-11B (20–25 minutes)

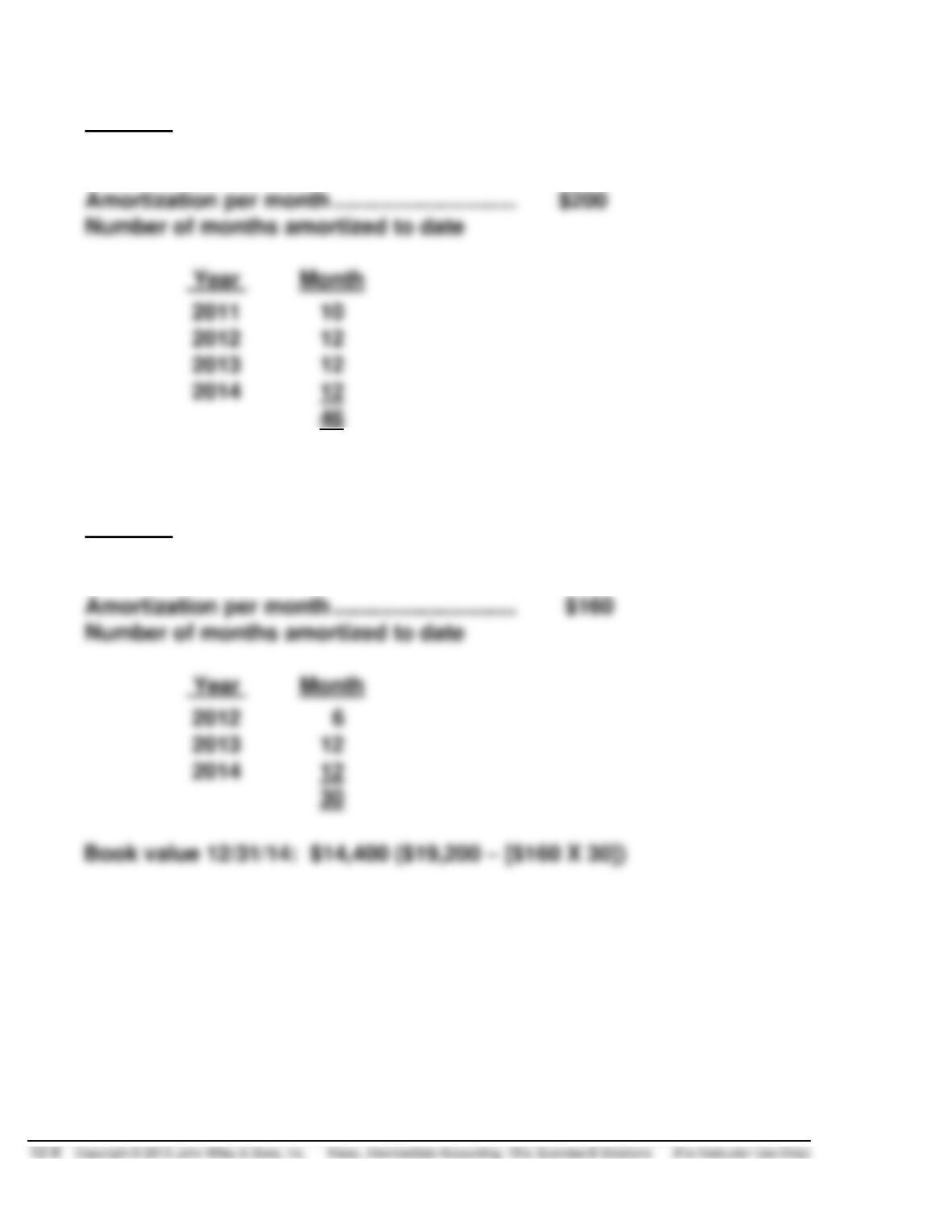

(a)

Patent A

Life in years ………………………………………….

20

Life in months (12 X 20) …………………………

240

Amortization per month …………………………

Number of months amortized to date

Book value 12/31/14: $38,800 ($48,000 – [46 X $200])

Patent B

Life in years ………………………………………….

10

Life in months (12 X 10) …………………………

120

Amortization per month …………………………

Number of months amortized to date

E12-11B (Continued)

Patent C

Life in years ……………………………………………

8

Life in months (12 X 8) …………………………….

96

Amortization per month …………………………..

Number of months amortized to date

Book value 12/31/14: $14,000 ($16,800 – [$175 X 16])

At December 31, 2014

Patent A ……………………………………………

$38,800

Patent B ……………………………………………

14,400

Patent C ……………………………………………

14,000

Total …………………………..………………..

$67,200

(b) Analysis of 2015 transactions:

1. The $347,000 incurred for research and development should be

expensed.

2. The book value of Patent B is $14,400 and its estimated future cash

E12-11B (Continued)

At December 31, 2015:

Patent A

$36,400

($38,800 – [12 X $200])

Patent B

(Present value of future cash flows)

Patent C

($14,000 – [12 X $175])

Patent D

($10,800 – $450*)

Patent D amortization:

Life in years

12

Amortization per month

$75 X 6 = $450

E12-12B (15 minutes)

Net assets of Ruth as reported …………………………...

$540,000

Adjustments to fair value ……………………………………

Increase in land value ………………………………..

$72,000

Decrease in equipment value ……………………..

60,000

Net assets of Ruth at fair value …………………………..

Selling price ………………………………………………………

The journal entry to record this transaction is as follows:

Cash ………………………………………………………………….

240,000

Land…………………………………………………………………..

240,000

Equipment ………………………………………………………….

408,000

Copyright …………………………………………………………..

Goodwill …………………………..………………………………..

240,000

Accounts Payable ………………………………………

Long-term Notes Payable …………………………...

Cash ………………………………………………………….

Copyright © 2013 John Wiley & Sons, Inc. Kieso, Intermediate Accounting, 15/e, Exercise B Solutions (For Instructor Use Only) 12–11

E12-13B (10–15 minutes)

(a)

Cash ………………………………………………………………………

37,500

Receivables …………………………………………………………….

67,500

Inventory ………………………………………………………………..

93,750

(b)

Amortization Expense (Copyrights) ………………………….

1,125

Copyrights ([$11,250 – $2,250] 1/4 X 6/12) ……………..

E12-14B (15–20 minutes)

(a)

December 31, 2014

Loss on Impairment …………………………………..

2,470,000*

Copyrights ………………………………………..

*Carrying amount

Land ……………………………………………………………………….

45,000

Buildings …………………………..……………………………………

56,250

Equipment ………………………………………………………………

52,500

Copyrights ……………………………………………………………..

11,250

Goodwill …………………………………………………………………

48,750

Accounts Payable …………………………………………..

Notes Payable …………………………………………………

Cash ………………………………………………………………

E12-14B (Continued)

(b)

Copyright Amortization Expense ………………..

385,000*

Copyrights ………………………………………..

385,000

*New carrying amount

Useful life

÷ 10 years

E12-15B (15–20 minutes)

(a)

December 31, 2014

Loss on Impairment ………………………………

12,000,000

Goodwill ……………………………………….

12,000,000

Fair value of division …………………………………………….

Carrying amount of division, net of goodwill …………..

Implied value of goodwill ……………………………………….

Carrying value of goodwill …………………………………….

The fair value of the reporting unit is below its carrying value. Therefore,

(b) No entry necessary. After a goodwill impairment loss is recognized, the

adjusted carrying amount of the goodwill is its new accounting basis.

E12-16B (15–20 minutes)

(a) The $183,000 is a research and development cost that should be

(b)

Research and Development Expense ……………………….

211,000

Cash, Accts. Payable, etc. ……………………………….

211,000

(To record research and

development costs)

Patents ……………………………………………………….………….

12,000

(To record legal and administrative

costs incurred to obtain patent )

Patent Amortization Expense …………………………………..

Patents …………………………………………………………..

[To record one year’s amortization

(c)

Patents ……………………………………………………….………….

18,600

Cash, Accts. Payable, etc. ……………………………….

18,600

(To record legal cost of successfully

defending patent)

Patent Amortization Expense …………………………………..

Patents …………………………………………………………..

Expense:

$12,000 – $2,000 = $10,000;

$18,600 ÷ 5 =

E12-16B (Continued)

(d) Additional engineering and consulting costs required to advance the

E12-17B (10–12 minutes)

Depreciation of equipment acquired that will have alternate

uses in future research and development projects over

the next 5 years ($300,000 ÷ 5) ……………………………………………

$ 60,000

Materials consumed in research and development projects ……

Consulting fees paid to outsiders for research and

development projects ………………………………………………………..

Personnel costs of persons involved in research and

development projects ………………………………………………………..

Indirect costs reasonably allocable to research and

development projects ………………………………………………………..

Total to be expensed in 2014 for research and

*E12-18B (10–15 minutes)

(a) Companies are required to use the greater of (1) the ratio of current

(b)

Percent-of–revenue approach:

$4,000,000

X $7,200,000 = $1,200,000

$24,000,000

*E12-19B (15–20 minutes)

(a)

Research and Development Expense ……………………….

5,000,000

Cash …………………………………………………………………

5,000,000

Computer Software Costs

($8,600,000 – $5,000,000) ………………………………………

Cash …………………………………………………………………

(b)

Amortization Expense* …………………………………………….

900,000

Computer Software Costs ………………………………….

900,000

*Percent of revenue, $3,500,000 / $35,000,000 = 10%; 10% X $3,600,000 =

(d) Extel Computing, Inc. Enterprises should disclose in its December 31, 2015,

financial statements the unamortized computer software costs included in

(e) The accounting guidance in this area applies only to the development of

computer software that is to be sold, leased, or otherwise marketed to