PROBLEM 22-7B (Continued)

(9)

Insurance Expense ($6,000 ÷ 2) ………………………………….. 3,000

PROBLEM 22-8B

Net Income for 2013

Retained Earnings 12/31/14

Item

Understated

Overstated

Understated

Overstated

1.

$6,800

0

0

0

2.

$ 15,200

0

$ 13,600

0

5.

0

0

0

Explanations:

1. The net income would be understated in 2013 because interest income

is understated. The net income would be overstated in 2014 because

2. The depreciation expense in 2013 should be $800 for this furniture.

Since the machine was bought on July 1, 2013, only one-half of a year’s

3. GAAP requires that all research and development costs should be ex–

pensed when incurred. Net income in 2013 is overstated $57,000 ($76,000

PROBLEM 22-8B (Continued)

4. The security deposit should be a long-term asset, called refundable

deposits. The $12,000 of the last month’s rent is also an asset, called

5. $14,000 or one-half of $28,000 should be reported as income each year.

In 2013, $28,000 was reported as income when only $14,000 should

6. The ending inventory would be understated since the merchandise was

omitted. Because ending inventory and net income have a direct relation-

PROBLEM 22-9B

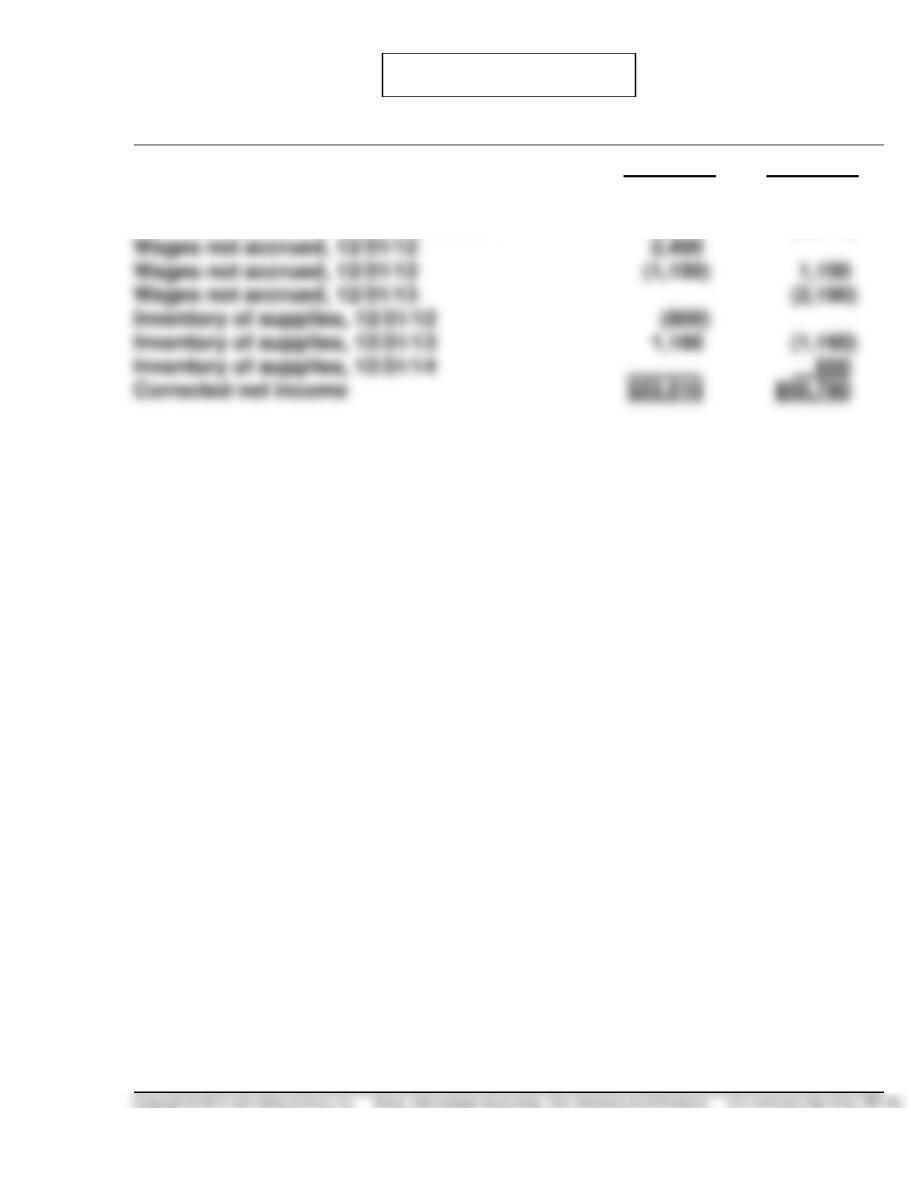

2013

2014

Net income, as reported

$46,000

$52,000

Rent received in 2013, earned in 2014

2,000

(2,000)

Wages not accrued, 12/31/12

Wages not accrued, 12/31/12

Wages not accrued, 12/31/13

Inventory of supplies, 12/31/12

Inventory of supplies, 12/31/13

1,160

Corrected net income

3. To correct C.O.D. sale

(6,800)

4. Adjustment of warranty

exp:

Sales per books

Correction for consignments

Correction for C.O.D. sale

Corrected sales

Less costs charged to exp

3,910

Additional expense

$ 5,713

$ 6,365

$ 8,571

(5,713)

(6,365)

(8,571)

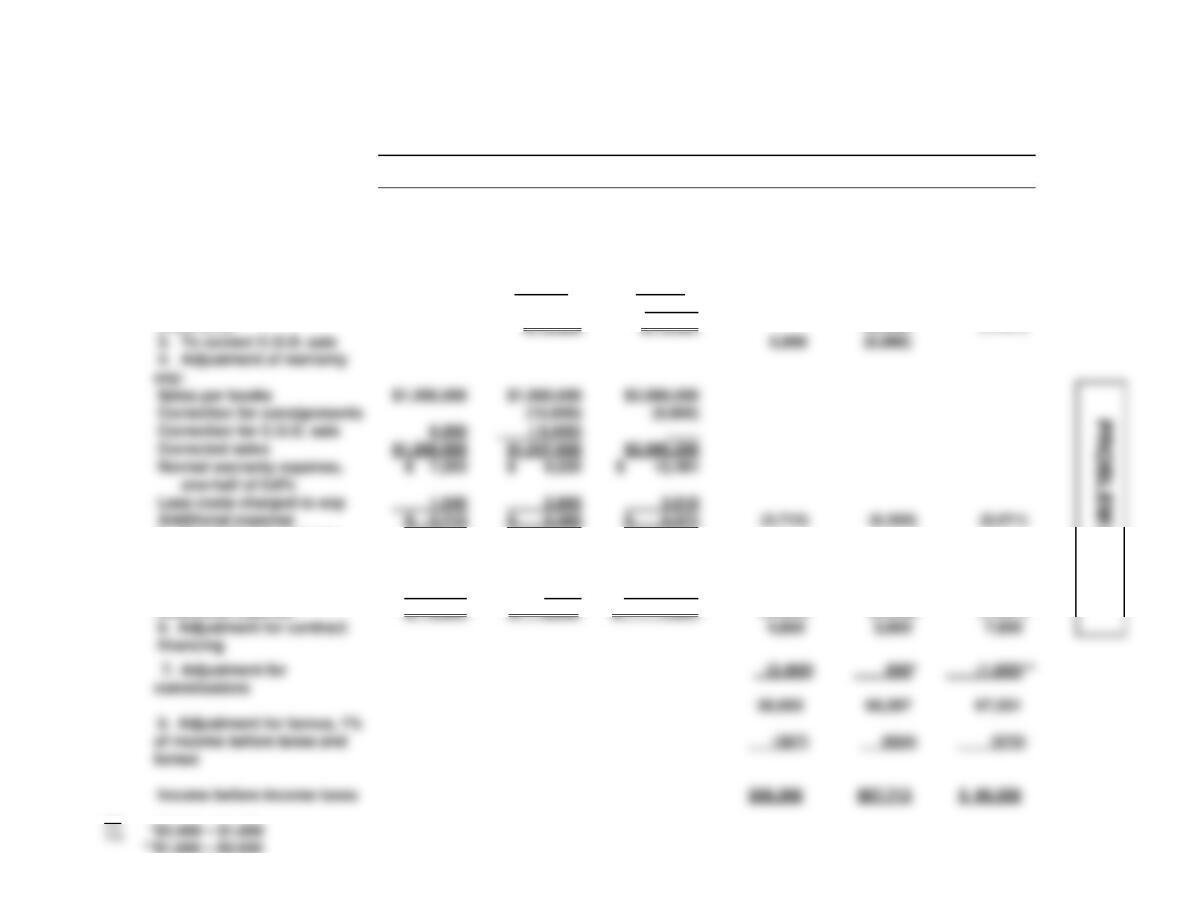

(a) BEACHES COMPANY

Schedule of Revised Net Income

For the Years Ended June 30, 2013, 2014, and 2015

COMPUTATIONS

SUMMARY

Increases (Decreases) in Income

2013

2014

2015

2013

2014

2015

1. Income before income

taxes, as reported

$40,600

$85,300

$78,900

2. Elimination of profit on

consignments:

Billed

$ 15,600

$ 8,800

at 120% of cost

÷ 120%

÷ 120%

Cost

$ 13,000

$7,333

Profit error

$ 2,600

$ 1,467

(2,600)

(1,467)

5. Bad debt adjustments:

Normal bad debt expense,

0.5% of sales

$ 6,044

$ 7,688

$ 10,401

Less previous write-offs

810

2,050

2,770

Additional expense

$ 5,234

$ 5,638

$ 7,631

(5,234)

(5,638)

(7,631)

7. Adjustment for

commissions

Income before income taxes

PROBLEM 22-10B (Continued)

(b) Sales Revenue ………………………………………………….. 8,800

Inventory on Consignment …………………………..……. 7,333

Cost of Goods Sold …………………………………….. 7,333

Accounts Receivable …………………………..……… 8,800

(To adjust for consignments treated

as sales, 6/30/15)

Due to Customer (held by bank) …………………………. 16,350

Finance Expense ………………………………………… 7,850

Retained Earnings ($4,600 + $3,900) …………….. 8,500

(To record finance charge reserve

held by bank)

*PROBLEM 22-11B

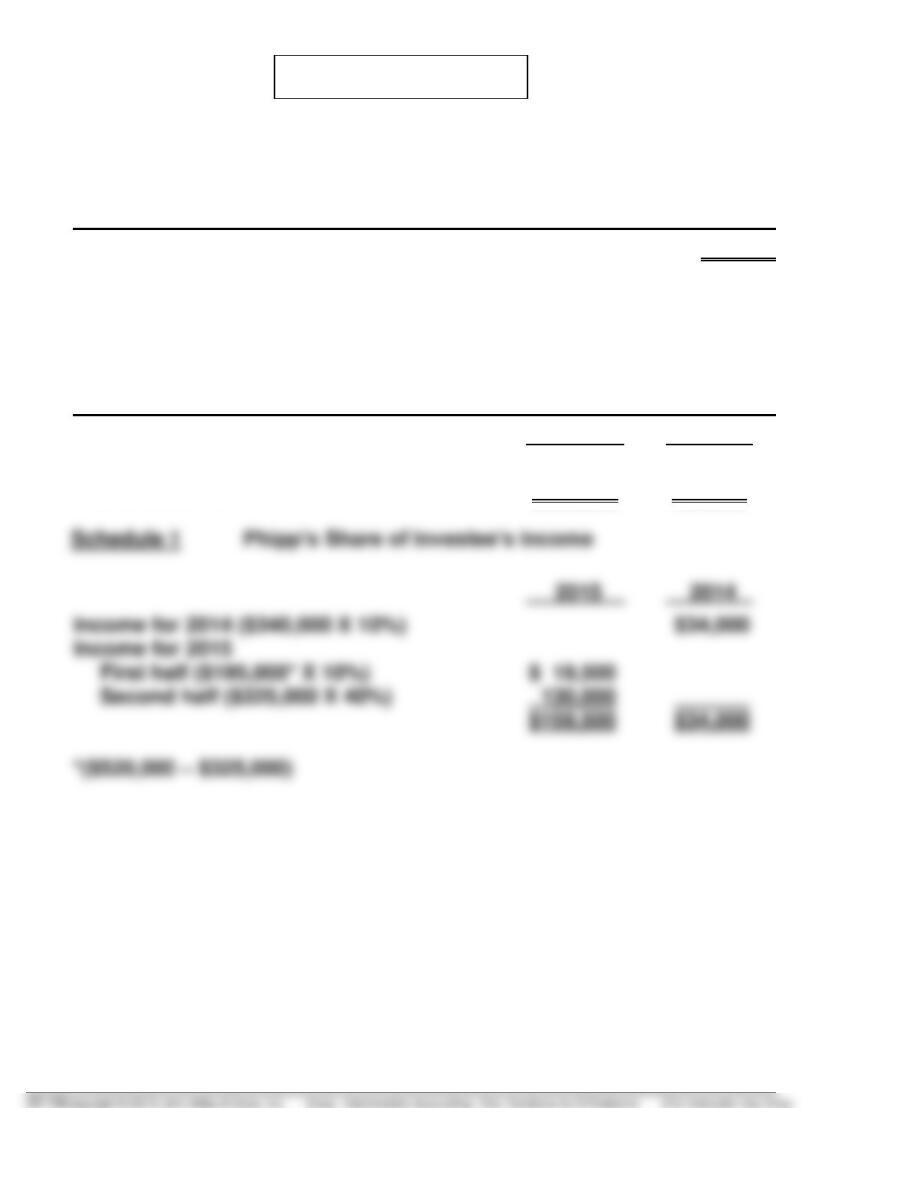

(a) PHIPPS INC.

Schedule of Income or Loss from Investment

For Year Ending December 31, 2014

Dividend revenue …………………………………………………………….. $25,000

(20,000 shares X $1.25 dividend/share)

(b) PHIPPS INC.

Schedule of Income or Loss from Investment

For Years Ending December 31, 2015 and 2014

2015

2014

Income from investment in Payson

(Schedule 1)

$159,500

$34,000

*PROBLEM 22-12B

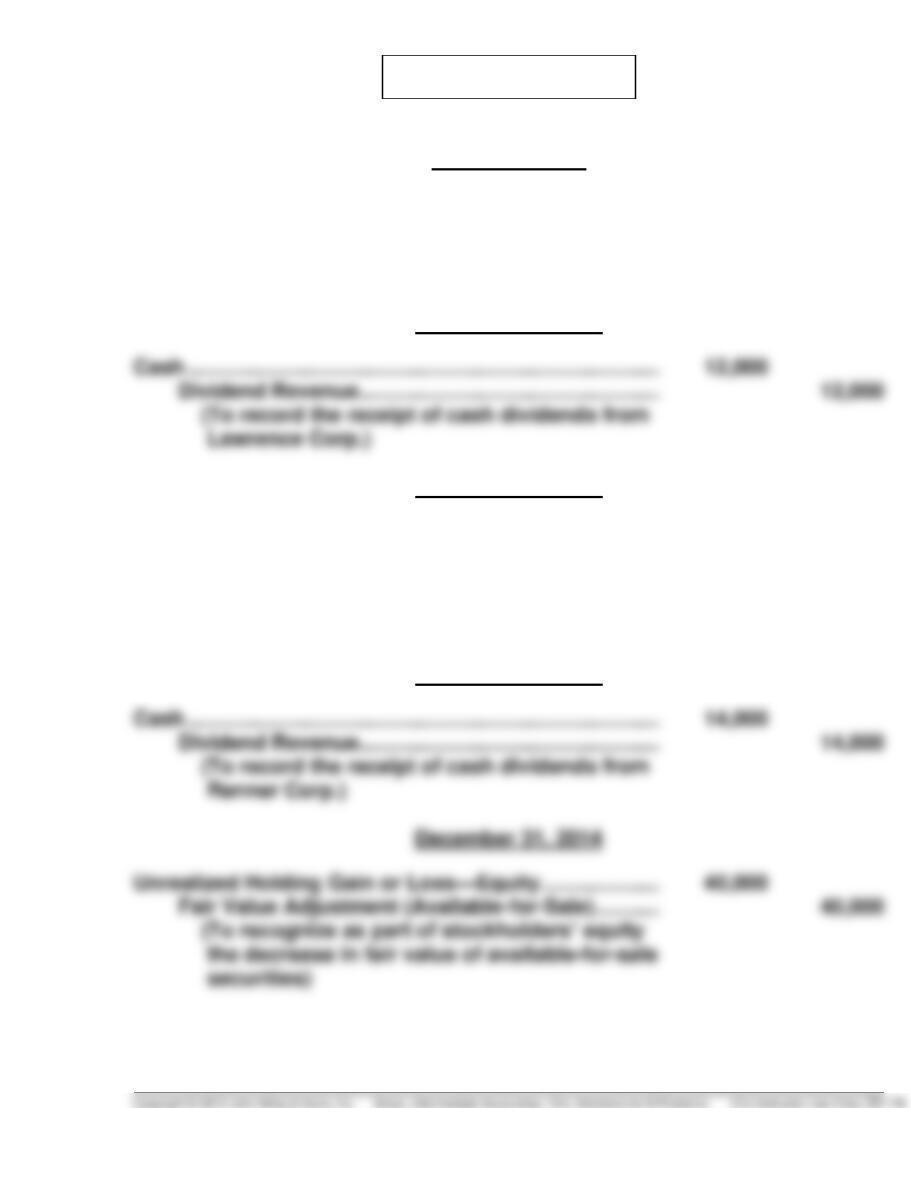

January 2, 2013

Equity Investments (Available-for-sale) …………………… 600,000

Cash ………………………………………………………………. 600,000

(To record the purchase of a 10% interest in

Lawrence Corp.)

December 31, 2013

December 31, 2013

Fair Value Adjustment (Available-for-Sale) ……………… 20,000

Unrealized Holding Gain or Loss—Equity ………… 20,000

(To recognize as part of stockholders’ equity

the increase in fair value of available-for-sale

securities)

December 31, 2014

*PROBLEM 22-12B (Continued)

January 2, 2015

Equity Investment (Equity Method) …………………… 2,273,500

Cash ………………………………………………………… 2,240,000

Retained Earnings ……………………………………. 33,500

(To record purchase of additional interest

in Lawrence and to reflect retroactively

a change from the fair value to the equity

method)

Computation of Prior Period Adjustment

2013

2014

Total

January 2, 2015

Equity Investment (Equity Method) …………………… 600,000

Equity Investments (Available-for-sale) ……… 600,000

(To reclassify investment carried under

*PROBLEM 22-12B (Continued)

December 31, 2015

Equity Investment (Equity Method). ………………………… 388,875

Revenue from Investment ……………………………….. 388,875

Cash …………………………………………………………………….. 32,000

Equity Investment (Equity Method). …………………. 32,000

(To record the receipt of cash dividends

from Lawrence Corp.)