Continuing Case Solution

Chapter 3

Memorandum

To: Eric Conner and Phil Martin, CM

From: L. Harbach

Re: Adjusting Entries and Accrual Accounting

Date: January 5, 2013

At the end of the year, it is critical to perform adjusting entries to ensure that the

company records revenues and expenses in the period in which they are earned/

incurred and that balance sheet accounts have the correct balances. I made the

following adjusting entries in order to properly report revenues and expenses

earned/incurred during the year and related balance sheet accounts as of year–

end:

An adjustment was made to the unearned revenue account to recognize

e that had been earned by year-end.

These adjustments allow the company to present its financial statements using

the accrual basis of accounting. The accrual basis of accounting allows external

based on the dates when income is

Continuing Case Solution

Additional Activity: Extend your accounting knowledge

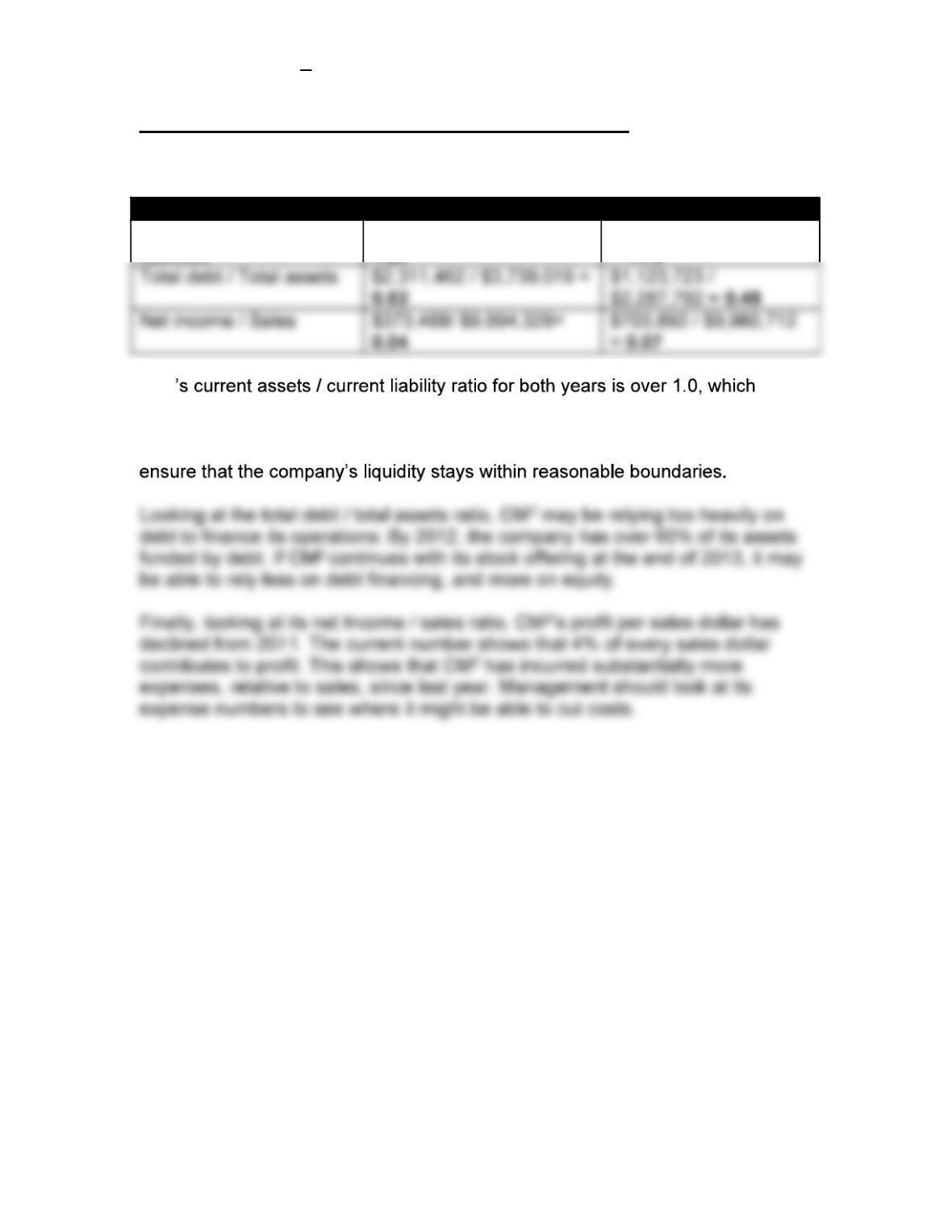

Financial Assessment

2012 2011

Current assets / Current

liabilities

$2,126,086 / $1,722,962 =

1.23

$1,483,062 / $845,198

= 1.75

CM2

means that the company has the liquidity to cover its current liabilities. In other

words, CM2 has slightly more current assets each year than current liabilities.

This ratio has declined and is something that management needs to monitor to