CHAPTER 21

SOLUTIONS TO B EXERCISES

E21-1B (15–20 minutes)

(a) This is a capital lease to Manor since the lease term (6 years) is greater

than 75% of the economic life (6 years) of the leased asset. The lease

term is 100% (6 ÷ 6) of the asset’s economic life.

(c) 1/1/14 Leased Machine Under Capital

Leases …………………………………………. 250,000

Lease Liability …………………………... 250,000

Lease Liability …………………………………. 54,291

Cash …………………………………………. 54,291

E21-2B (20–25 minutes)

(a) To Jupiter, the lessee, this lease is a capital lease because the terms

satisfy the following criteria:

1. The lease term is greater than 75% of the economic life of the leased

(b) The minimum lease payments in the case of a guaranteed residual value

by the lessee include the guaranteed residual value. The present value

therefore is:

(c) Leased Property Under Capital Leases ………………. 102,168

Lease Liability ……………………………………………. 102,168

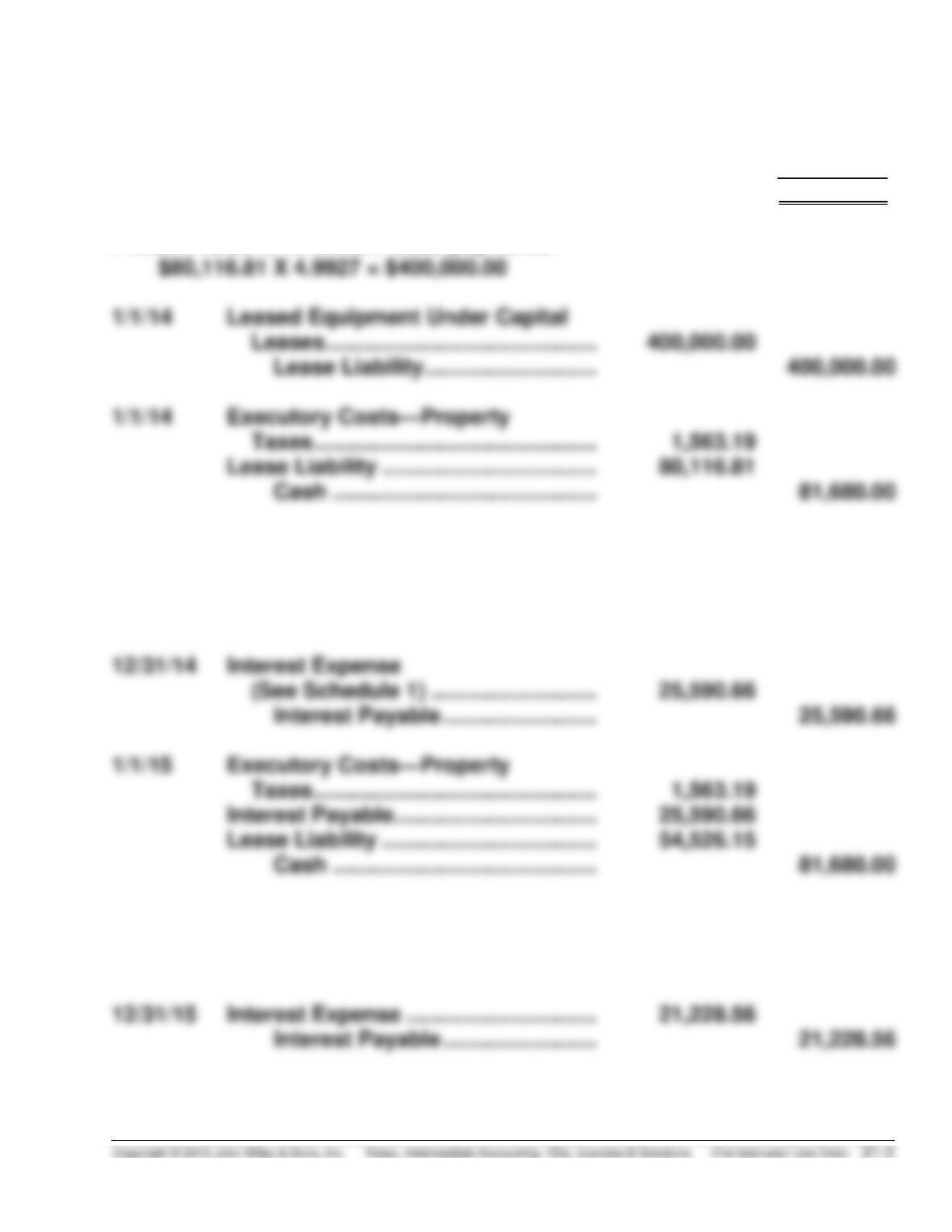

E21-3B (20–30 minutes)

Capitalized amount of the lease:

Yearly payment …………………………………………………….. $81,680.00

Executory costs …………………………………………………… (1,563.19)

Minimum annual lease payment…………………………….. $80,116.81

Present value of minimum lease payments:

12/31/14 Depreciation Expense ………………….. 66,666.67

Accumulated Depreciation—

Capital Leases

($400,000 ÷ 6) ……………………. 66,666.67

12/31/15 Depreciation Expense ………………….. 66,666.67

Accumulated Depreciation—

Capital Leases ………………….. 66,666.67

E21-3B (Continued)

Schedule 1

Yard Waste Corp.

Lease Amortization Schedule

(Lessee)

Date

Annual

Payment Less

Executory

Costs

Interest (8%) on

Liability

Reduction

of Lease

Liability

Lease Liability

E21-4B (20–25 minutes)

Computation of annual payments:

Cost (fair market value) of leased asset to lessor ………………. $325,000.00

Less: Present value of salvage value

E21-4B (Continued)

POWER TOP LEASING (Lessor)

Lease Amortization Schedule

Date

Annual Payment

Less Executory

Costs

Interest

on Lease

Receivable

Recovery

of Lease

Receivable

Lease

Receivable

1/1/14

$325,000.00

12/31/14

12/31/15

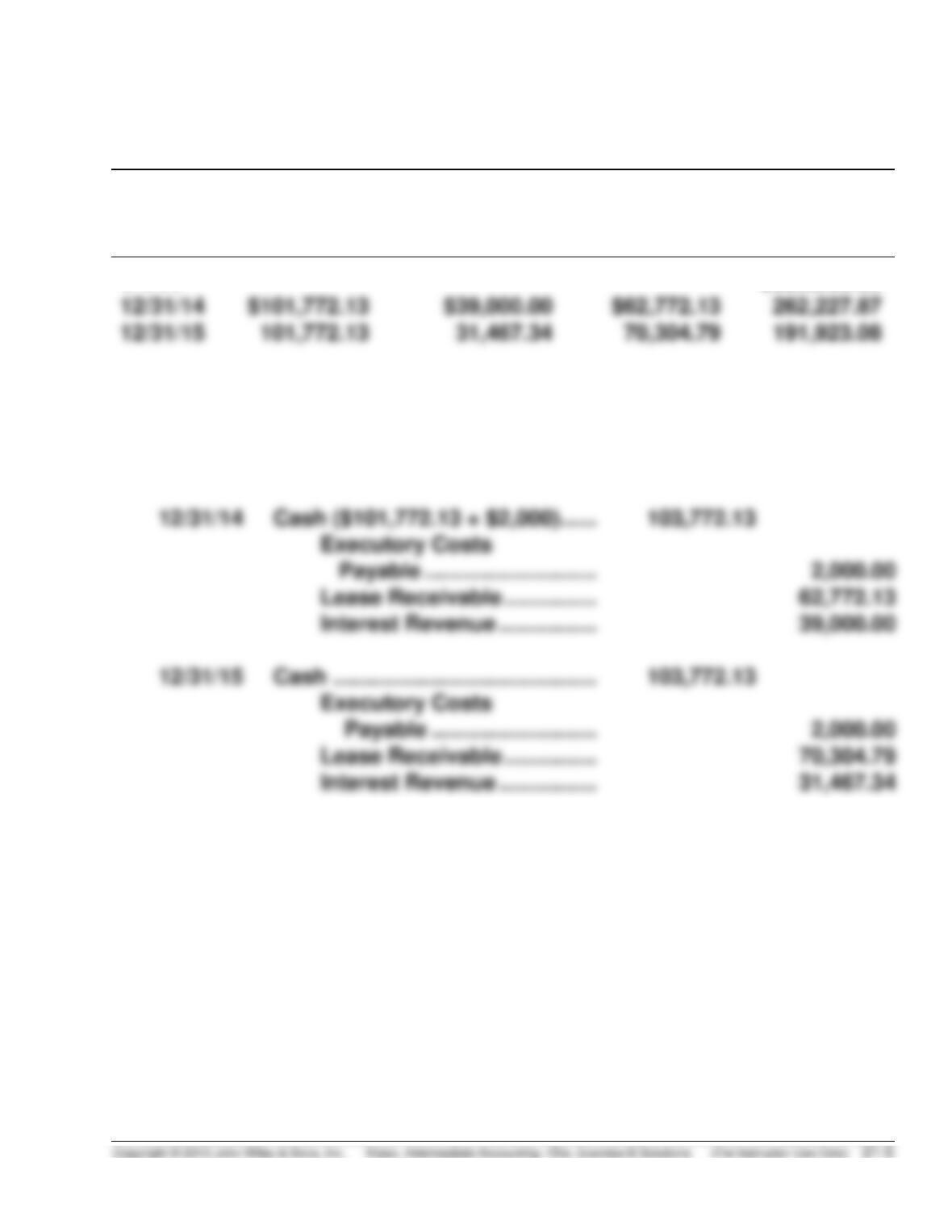

(a) 1/1/14 Lease Receivable ………………….. 325,000.00

Equipment …………………….. 325,000.00

(b) 12/31/17 Cash ……………………………………. 25,000.00

Lease Receivable …………… 25,000.00

E21-5B (15–20 minutes)

(a) Because the lease term is longer than 75% of the economic life of the

asset, it is a capital lease to the lessee. Assuming collectibility of the

rents is reasonably assured and no important uncertainties surround the

amount of unreimbursable costs yet to be incurred by the lessor, the

lease is a direct financing lease to the lessor.

The lessor should adopt the direct financing lease method and replace

the asset cost of $225,000 with Lease Receivable of $225,000. (See

schedule on next page.) Interest would be recognized annually at

a constant rate relative to the unrecovered net investment.

Cost (fair market value of leased asset) …………………………... $225,000

E21-5B (Continued)

(b) Schedule of interest and amortization:

Rent Receipt/

Payment

Interest

Revenue/

Expense

Reduction of

Principal

Receivable/

Liability

1/1/14

—

—

—

$225,000

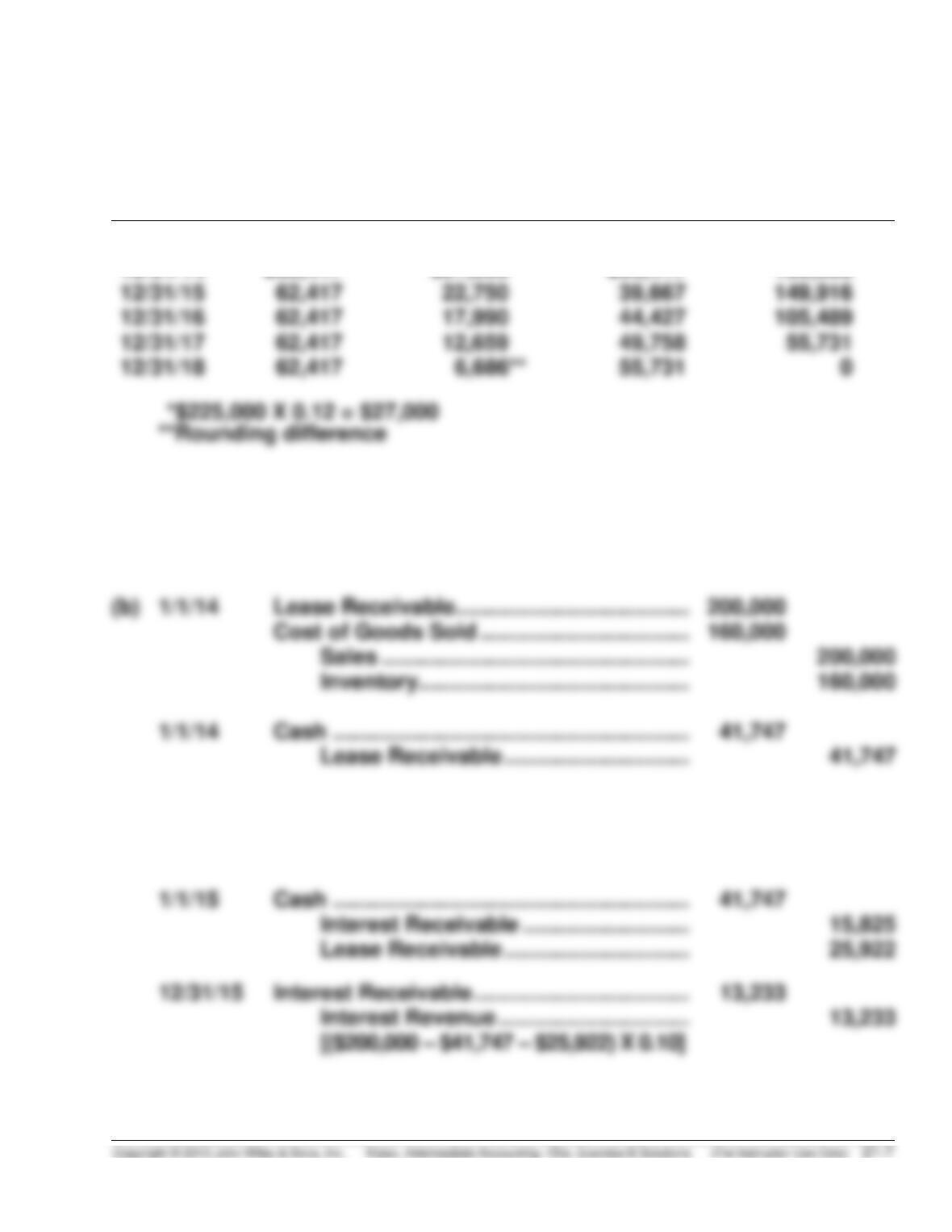

12/31/14

$62,417

*$27,000*

$35,417

189,583

12/31/15

149,916

EXERCISE 21-6B (15–20 minutes)

(a) $41,747 X 4.7908 = $200,000 (rounded by $1)

12/31/14 Interest Receivable …………………………….. 15,825

Interest Revenue

[($200,000 – $41,747) X 0.10] …….. 15,825

E21-7B (20–25 minutes)

(a) Computation of annual rental payment:

(b) This is a capital lease to Local since the lease term is 75% of the asset’s

economic life (6/8 = 75%). Also, the present value of the minimum lease

payments is more than 90% of the fair value of the asset.

(c) 1/1/14 Leased Equipment Under Capital

Leases ……………………………………… 317,112

12/31/14 Depreciation Expense …………………… 52,852

Accumulated Depreciation

($317,112 ÷ 6 years) ……………. 52,852

E21-7B (Continued)

(d) 1/1/14 Lease Receivable ………………………… 320,000*

Cost of Goods Sold …………………….. 249,799**

Sales …………………………………… 304,799***

E21-8B (20–30 minutes)

(a) The lease agreement has a bargain purchase option and thus meets the

criteria to be classified as a capital lease from the viewpoint of the lessee.

The present value of the minimum lease payments also exceeds 90% of

the fair value of the assets.

(b) The lease agreement has a bargain purchase option. The collectibility of the

E21-8B (Continued)

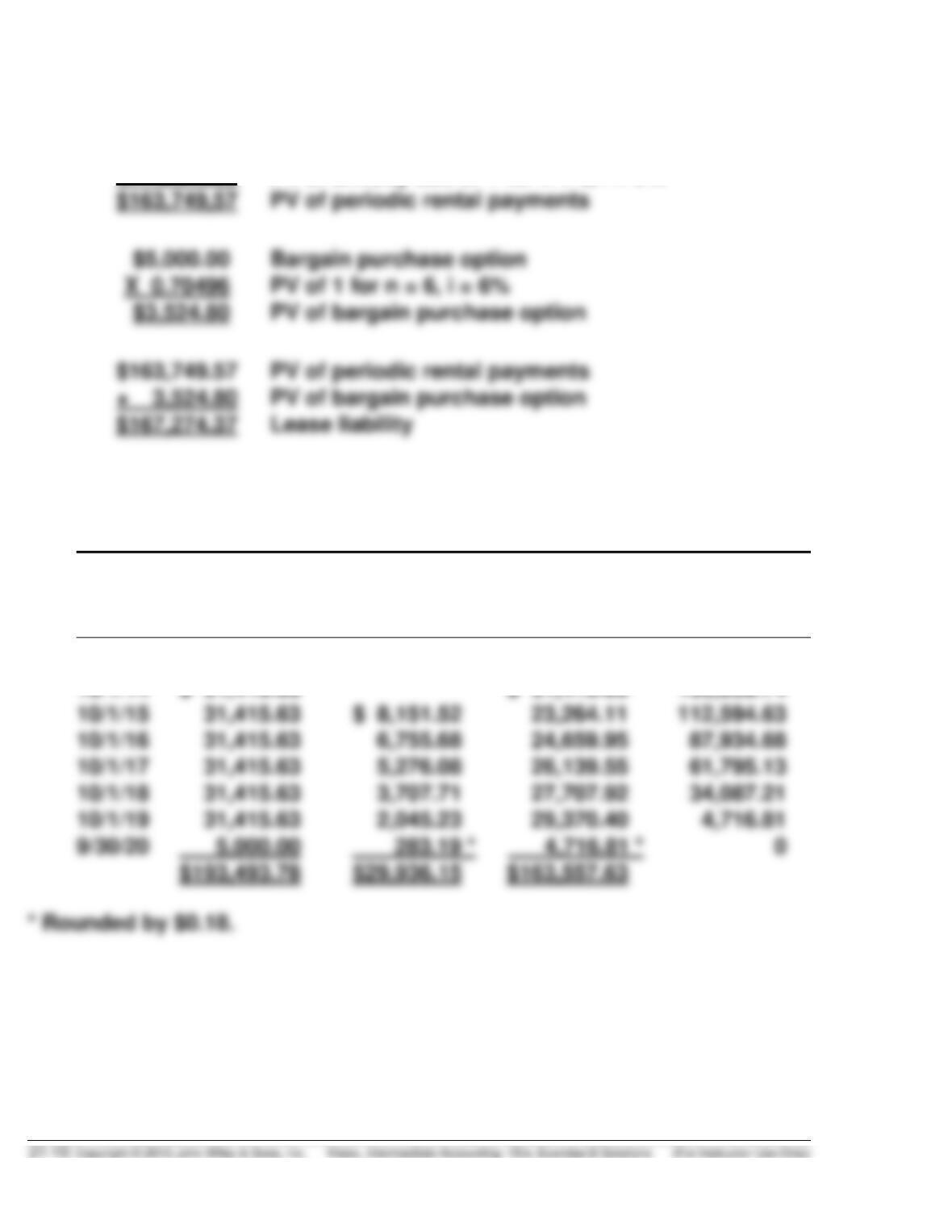

(c) Computation of lease liability:

$ 31,415.63 Annual rental payment

X 5.21236 PV of annuity due of 1 for n = 6, i = 6%

NEW MOON COMPANY (Lessee)

Lease Amortization Schedule

Date

Annual Lease

Payment Plus

BPO

Interest (6%)

on Liability

Reduction

of Lease

Liability

Lease

Liability

10/1/14

$167,274.37

10/1/14

10/1/15

10/1/16

10/1/17

10/1/18

10/1/19

E21-8B (Continued)

(d) 10/1/14 Leased Equipment Under

Capital Leases ……………………….. 167,274.37

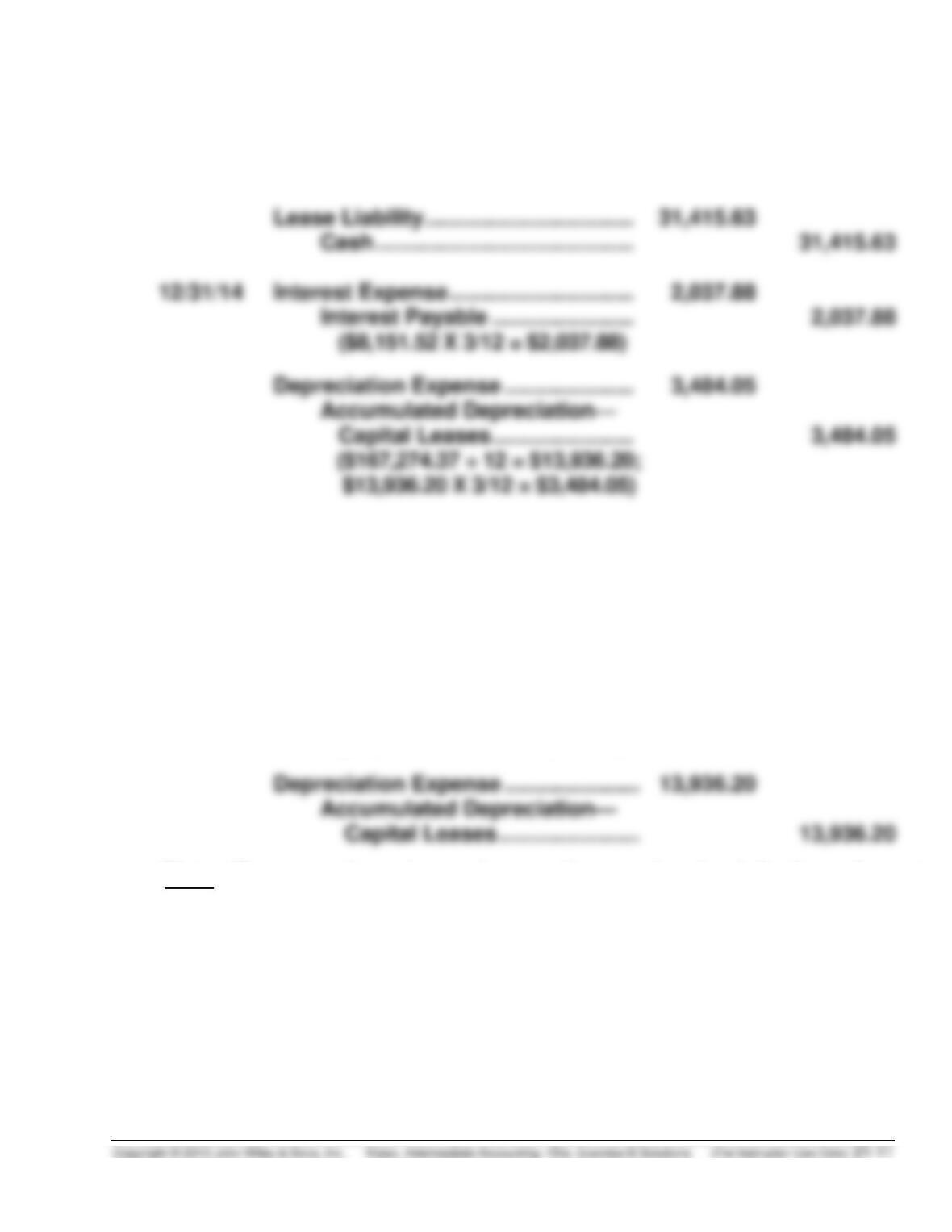

Lease Liability …………………….. 167,274.37

1/1/15 Interest Payable ………………………….. 2,037.88

Interest Expense ………………….. 2,037.88

10/1/15 Interest Expense …………………………. 8,151.52

Lease Liability …………………………….. 23,264.11

Cash ……………………………………. 31,415.63

12/31/15 Interest Expense …………………………. 1,688.92

Interest Payable …………………… 1,688.92

($6,755.68 X 3/12 = $1,688.92)

(Note: Because a bargain purchase option was involved, the leased asset

is depreciated over its economic life rather than over the lease term.)