CHAPTER 14

Long-Term Liabilities

SOLUTIONS TO B PROBLEMS

PROBLEM 14-1B

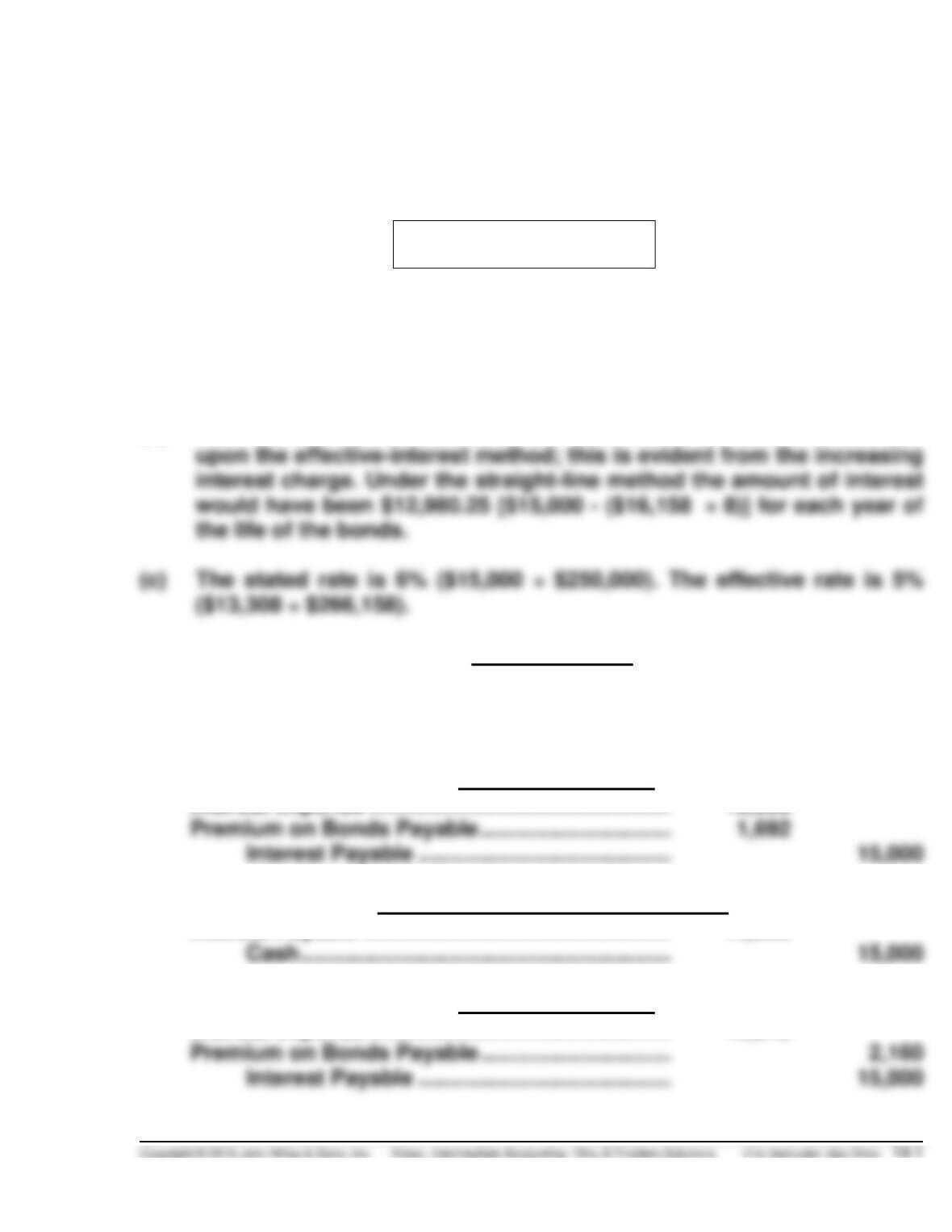

(a) The bonds were sold at a premium of $16,158. Evidence of the

discount is the January 1, 2010 book value of $266,158, which is less

than the maturity value of $250,000 in 2017.

(b) The interest allocation and bond discount amortization are based

(d)

January 1, 2010

Cash ………………………………………………………………………

266,158

Premium on Bonds Payable …………………………..

16,158

Bonds Payable ……………………………………………….

250,000

(e)

December 31, 2010

Interest Expense …………………………………………………….

13,308

Premium on Bonds Payable …………………………..

Interest Payable ……………………………………………..

(f)

January 1, 2015 (Interest Payment)

Interest Payable ……………………………………………………..

15,000

Cash ……………………………………………………….

December 31, 2015

Interest Expense …………………………………………………….

12,840

Premium on Bonds Payable …………………………..

PROBLEM 14-2B

(a)

Present value of the principal

$5,000,000 X 0.14864 (PV20, 10%) …………………..

$ 743,200

Present value of the interest payments

$400,000* X 8.51356 (PVOA20, 10%) ……………….

Cash ………………………………………………………………………

Unamortized Bond Issue Costs…………………………..

Discount on Bonds Payable …………………………..

Bonds Payable ……………………………………………….

(b)

Date

Cash

Paid

Interest

Expense

Discount

Amortization

Carrying

Amount of

Bonds

1/1/13

$4,148,624

1/1/14

$400,000

$414,862

$14,862

4,163,486

1/1/15

416,349

4,179,835

1/1/16

1/1/17

419,782

4,217,601

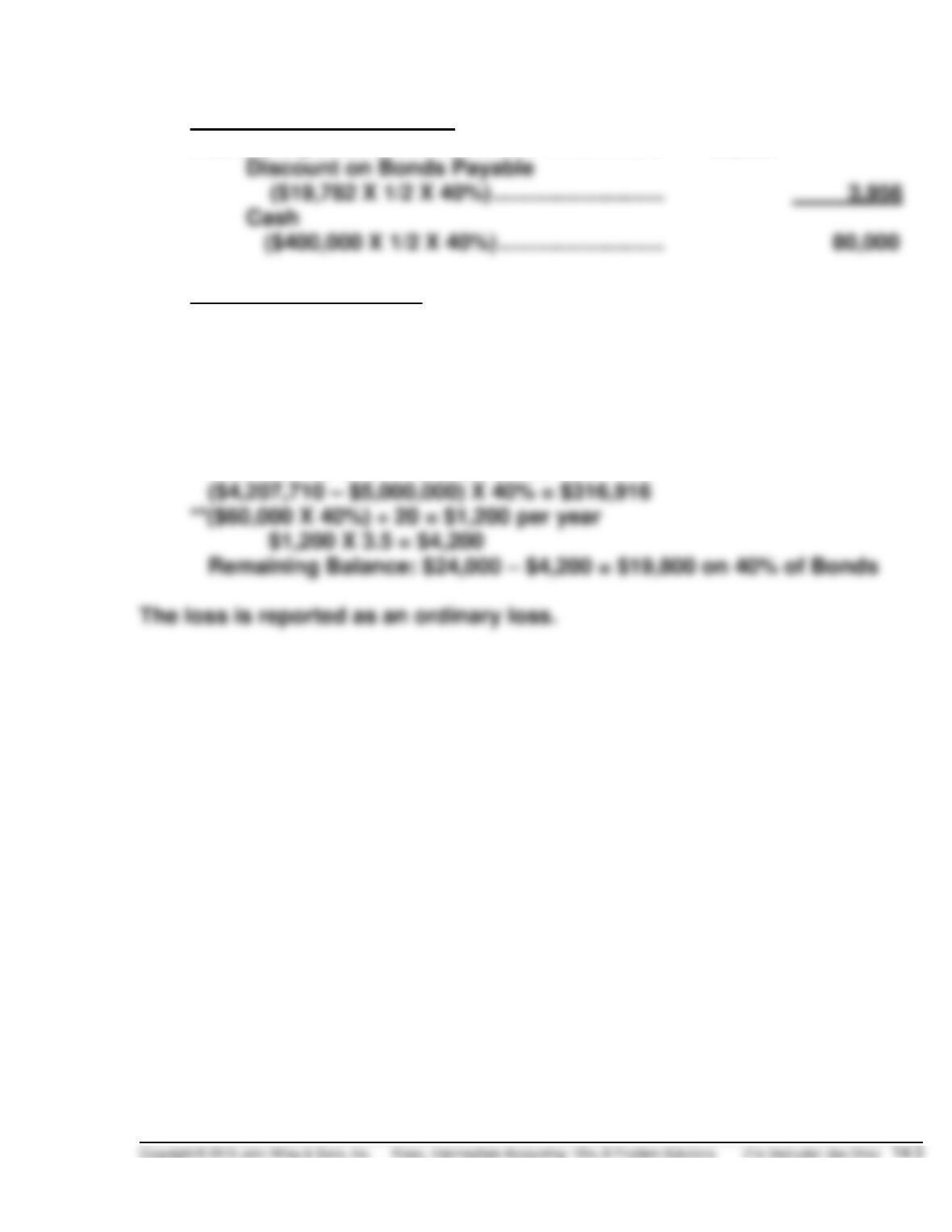

(c)

Carrying amount as of 1/1/16 ………………………….

$4,197,819

Plus: Amortization of bond discount

(19,782 ÷ 2) …………………………………………..

9,891

Carrying amount as of 7/1/16 ………………………….

$4,207,710

Reacquisition price ………………………………………..

Carrying amount as of 7/1/16

($4,207,710 X 40%) ………………………………………

Unamortized bond issue costs ($49,500 X 40%) .

Loss on redemption of bonds …………………………

PROBLEM 14-2B (Continued)

Entry for accrued interest

Interest Expense …………………………………………………….

83,956

Discount on Bonds Payable

($19,782 X 1/2 X 40%) …………………………..

3,956

Cash

($400,000 X 1/2 X 40%) …………………………..

Entry for reacquisition

Bonds Payable ……………………………………………………….

2,000,000

Loss on Redemption of Bonds …………………………..

376,716

Discount on Bonds Payable …………………………..

316,916*

Unamortized Bond Issue Costs ……………………….

19,800**

Cash ……………………………………………………….

2,040,000

*Premium as of 7/1/16 to be written off

($4,207,710 – $5,000,000) X 40% = $316,916

$1,200 X 3.5 = $4,200

Remaining Balance: $24,000 – $4,200 = $19,800 on 40% of Bonds

PROBLEM 14-3B

(a)

Date

Cash

Paid

Interest

Expense

Discount

Amortized

Carrying

Amount of

Note

1/1/14

$59,000

4/1/14

$500

$1,770

$1,270

60,270

7/1/14

10/1/14

1/1/15

500

64,813

PROBLEM 14-3B (Continued)

(d)

Date

Cash

Paid

Interest

Expense

Discount

Amortized

Carrying

Amount of

Note

1/1/15

$64,813

4/1/15

$5,160

$1,944

3,216

61,597

7/1/15

5,160

1,848

3,312

58,285

10/1/15

5,160

1,749

3,411

54,874

1/1/16

5,160

1,646

3,514

51,360

4/1/16

5,160

1,541

3,619

47,741

7/1/16

5,160

1,432

3,728

44,013

10/1/16

5,160

1,320

3,840

40,173

1/1/17

5,160

1,205

3,955

36,218

4/1/17

5,160

1,087

4,073

32,145

7/1/17

5,160

4,196

27,949

10/1/17

5,160

839

4,321

23,628

1/1/18

5,160

709

4,451

19,177

4/1/18

5,160

575

4,585

14,592

7/1/18

5,160

438

4,722

10/1/18

5,160

296

4,864

1/1/19

5,160

154

*

5,006

*rounded up $4

(e) The new sales gimmick may bring people in the first time but will

drive them away once they learn of the amount of their required

payments in years 2 through 5. Many will not have budgeted for these

PROBLEM 14-4B

(a)

Entry to record the issuance of the 10% bonds on December 1, 2014:

Cash ………………………………………………………………………

2,525,000

Bonds Payable ……………………………………………….

2,500,000

Premium on Bonds Payable …………………………..

25,000

Entry to record the retirement of the 8% bonds on January 2, 2015:

Bonds Payable ……………………………………………………….

1,000,000

Loss on Redemption of Bonds …………………………..

Discount on Bonds Payable …………………………..

45,000

($60,000 X 15/20)

Cash ($1,000,000 X 110%) …………………………..

1,100,000

[The loss represents the excess of the

cash paid ($1,100,000) over the

carrying amount of the bonds

($955,000).]

(b) The loss is reported as an ordinary loss.

Note 1. Loss on Bond Redemption

The loss represents a loss of $135,000 from the redemption and re–

PROBLEM 14-5B

1. Lime Co.

Schedule of Bond Discount Amortization

Effective-Interest Method

9% Bonds Sold to Yield 8%

Date

Cash

Paid

Interest

Expense

Premium

Amortized

Carrying

Amount of

Bonds

4/1/14

$622,306

10/1/14

$27,000

$24,892

2,108

620,198

10/1/15

24,720

4/1/17

24,436

10/1/18

*

4/1/14

Cash ……………………………………………………….

622,306

Premium on Bonds Payable …………………………..

22,306*

Bonds Payable ……………………………………………….

600,000

*Maturity value of bonds payable ……………………………..

$600,000

Present value of $600,000 due in 9 periods at 4%

($600,000 X 0.70259) …………………………………………….

Present value of interest payable semiannually

($27,000 X 7.43533) ………………………………………………

Proceeds from sale of bonds ………………………………….

Interest Expense ……………………………………………………..

Premium on Bonds Payable …………………………..

Cash ……………………………………………………….

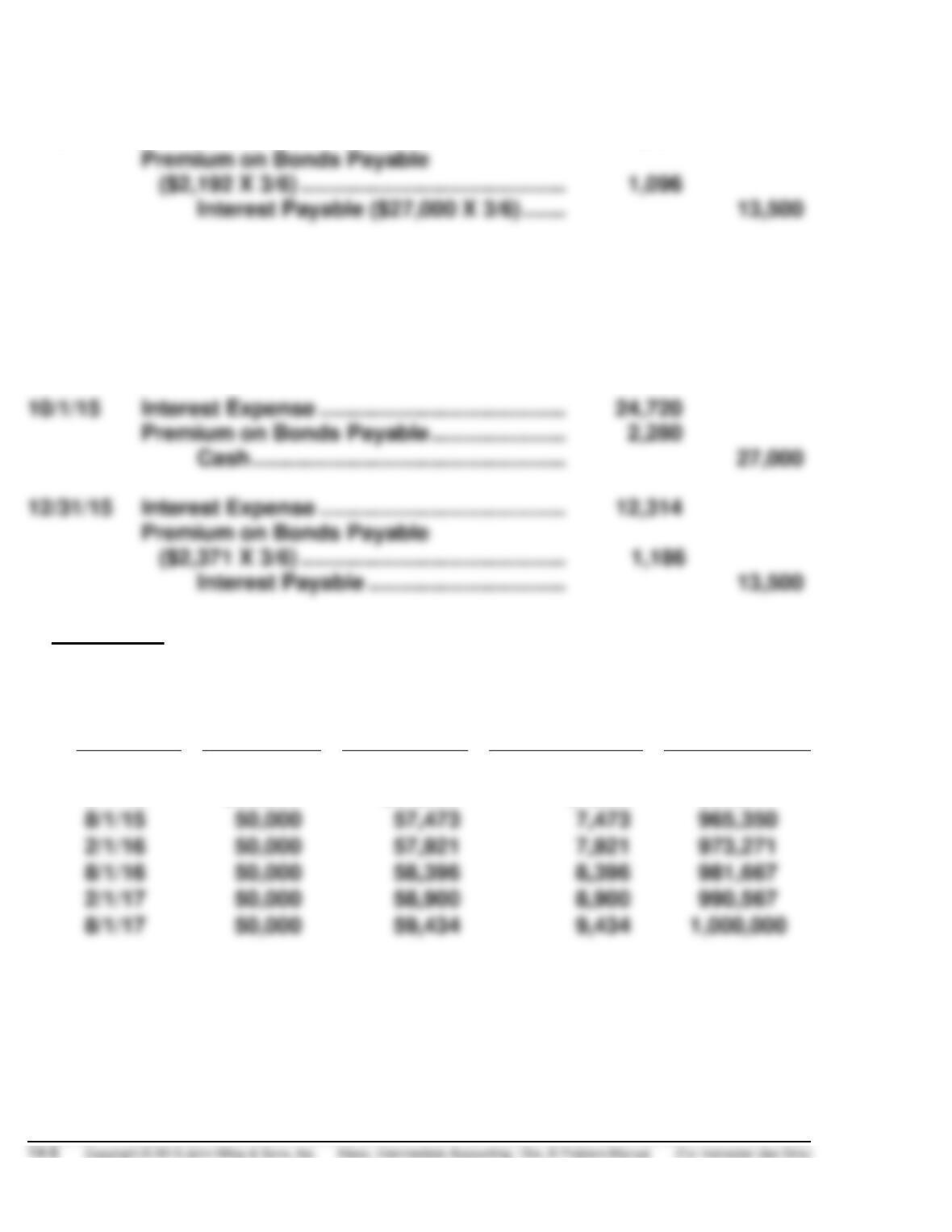

PROBLEM 14-5B (Continued)

12/31/14

Interest Expense …………………………………………………….

12,404

Premium on Bonds Payable

($2,192 X 3/6) ……………………………………………………….

1,096

Interest Payable ($27,000 X 3/6) ……………………….

13,500

4/1/15

Interest Expense …………………………………………………….

12,404

Interest Payable ……………………………………………………..

13,500

Premium on Bonds Payable

($2,192 X 3/6) ……………………………………………………….

1,096

Cash ……………………………………………………….

27,000

10/1/15

Interest Expense …………………………………………………….

24,720

Premium on Bonds Payable …………………………..

Cash ……………………………………………………….

12/31/15

Interest Expense …………………………………………………….

12,314

Premium on Bonds Payable

($2,371 X 3/6) ……………………………………………………….

Interest Payable …………………………..

13,500

2. Lemon Co.

Date

Cash

Paid

Interest

Expense

Discount

Amortized

Carrying

Amount of

Bonds

8/1/14

$950,827

2/1/15

$50,000

$57,050

$7,050

957,877

8/1/15

57,473

965,350

2/1/16

57,921

8/1/16

58,396

981,667

8/1/17

59,434

PROBLEM 14-5B (Continued)

8/1/14

Cash ……………………………………………………….

950,827

Discount on Bonds Payable …………………………..

49,173

Bonds Payable ……………………………………………….

1,000,000

Maturity value of bonds payable ………………………………

$1,000,000

Present value of $1,000,000 due in 6 periods at 6%

($1,000,000 X 0.70496) …………………………………………..

Present value of interest payable semiannually

($50,000 X 4.91732) ……………………………………………….

Proceeds from sale of bonds …………………………………..

Premium on bonds payable ……………………………………..

12/31/14

Interest Expense …………………………..…………………………

47,542

Discount on Bonds Payable

($7,050 X 5/6) ………………………………………………..

5,875

Interest Payable ($50,000 X 5/6) ………………………..

41,667

2/1/15

Interest Expense …………………………..…………………………

9,508

Interest Payable ………………………………………………………

41,667

Discount on Bonds Payable …………………………..

Cash ($1,000,000 X 0.10 X 6/12) ………………………..

Interest Expense …………………………..…………………………

57,743

Discount on Bonds Payable …………………………..

Cash ……………………………………………………….

Interest Expense

($57,921 X 0.20* X 2/6)…………………………..

Discount on Bonds Payable

($7,921 X 0.20 X 2/6) …………………………..

Cash ($50,000 X 0.20 X 2/6) …………………………..

PROBLEM 14-5B (Continued)

10/1/15

Bonds Payable ……………………………………………………….

200,000

Loss on Redemption of Bonds …………………………..

21,069*

Discount on Bonds Payable …………………………..

6,402

Cash ……………………………………………………….

214,667

*Reacquisition price

$218,000 – ($200,000 X 10% X 2/12)

Par value

Unamortized discount

[0,20 X ($49,173 – $7,050 – $7,473)] – $528

12/31/15

Interest Expense ($57,921 X 0.80* X 4/6) …………………..

38,614

Discount on Bonds Payable

($7,921 X 0.80 X 5/6) …………………………..

5,281

Interest Payable

($50,000 X 0.80 X 5/6) …………………………..

33,333

*($1,000,000–$200,000)÷$1,000,000=0.80

2/1/16

Interest Expense ($57,921 X 0.80 X 1/6) …………………….

Interest Payable

33,333

Discount on Bonds Payable

($7,921 X 0.80 X 1/6) …………………………..

1,056

Cash ($50,000 X 0.80)…………………………..

PROBLEM 14-6B

June 1, 2014

Cash

($600,000 X 98%) + ($600,000 X 8% X 5/12) ……………..

608,000

Discount on Bonds Payable …………………………………….

12,000

Bonds Payable ……………………………………………….

600,000

Interest Expense ($600,000 X 8% X 5/12) …………..

20,000

December 31, 2014

Interest Expense ($600,000 X 8%) …………………………..

48,000

Interest Payable ………………………………………………

Interest Expense

Discount on Bonds Payable …………………………..

($12,000 X 7/115* = $3,724.14) ……………………….

*(12 X 10) – 5 = 115

January 1, 2015

Interest Payable ………………………………………………………

48,000

Cash ………………………………………………………………

48,000

August 1, 2015

Bonds Payable ……………………………………………………….

240,000

Interest Expense ($240,000 X 8% X 7/12) …………………..

11,200

Loss on Redemption of Bonds …………………………………

Cash ($242,400 + $11,200) …………………………..

Discount on Bonds Payable …………………………..

Reacquisition price (including accrued interest)

($240,000 X 101%) + ($240,000 X 8% X 7/12) ……………

Net carrying value of bonds redeemed:

Par value ………………………………………………………………..

Unamortized discount

[$12,000 X ($240,000 ÷ $600,000) X 101/115]……………

Accrued interest ($240,000 X 8% X 7/12) …………………..

PROBLEM 14-6B (Continued)

December 31, 2015

Interest Expense ($360,000 X 8%) …………………………..

28,800

Interest Payable ………………………………………………

28,800

Interest Expense ……………………………………………………..

1,043

Discount on Bonds Payable …………………………..

1,043

Amortization per year on $360,000

($12,000 X 12/115 X 0.60*) ……………………………………..

Amortization on $240,000 for 7 months

($12,000 X 7/115 X 0.40**) ………………………………………

PROBLEM 14-7B

(a)

6/1/14

Cash (6,000 X $1,000 X 98%) …………………………..

5,760,000

Discount on Bonds Payable …………………………..

240,000

Bonds Payable …………………………..

6,000,000

(b)

12/1/14

Interest Expense ………………………………………………………

186,000

Cash (6,000,000 X 6% X 6/12) …………………………..

Discount on Bonds Payable …………………………..

($240,000 ÷ 240 months =

$1,000/mo.; $1,000/mo.

X 6 months = $6,000)

(c)

12/31/14

Interest Expense ………………………………………………………

31,000

Interest Payable

($180,000 X 1/6) …………………………..

Discount on Bonds Payable

($1,000 X 1 month) …………………………..

(d)

2/1/15

Interest Payable ……………………………………………………….

20,000

Interest Expense ………………………………………………………

20,667

Cash ……………………………………………………….

40,000*

Discount on Bonds Payable …………………………..

*Cash paid to retiring

bondholders: $4,000,000

X 6% X 2/12 = $40,000

At February 1, 2015 the carrying amount of the retired

bonds is:

Bonds payable ………………………………………………………………

$4,000,000

Less: Unamortized discount …………………………..…………….

PROBLEM 14-7B (Continued)

The reacquisition price: 500,000 shares X $8.50 = $4,250,000.

The loss on redemption of bonds is:

Reacquisition price …………………………..…………………..

$4,250,000

Less: Carrying amount …………………………..

The entry to record extinguishment of the bonds is:

Bonds Payable ……………………………………………….

Loss on Redemption of Bonds ………………………..

Discount on Bonds Payable ……………………..

Common Stock ………………………………………..