CHAPTER 22

Accounting Changes and Error Analysis

ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC)

Topics

Questions

Brief

Exercises

Exercises

Problems

Concepts

for Analysis

1. Differences between change in

principle, change in estimate,

change in entity, errors.

2, 4, 6, 7,

8, 9, 12, 13,

15, 21

8

3

1, 2, 3, 4

2. Accounting changes:

a. Comprehensive.

3, 6, 7

1, 2, 4, 5

b. Changes in estimate,

changes in depreciation

methods.

8, 9

4, 5, 9

16, 17

for long-term construction

2, 10

1, 2, 10

1, 8, 13

3

1, 2

2, 8, 14

e. Change from FIFO to LIFO.

2, 11

1, 2

8

3

2, 3, 5,

8, 14

2, 5

1, 3, 4,

5, 8

8, 9, 10

3, 4, 6, 7,

8, 9, 10,

11, 12,

1, 2, 4,

6, 7

1, 2, 3,

4, 5, 6

3. Correction of an error.

a. Comprehensive.

8, 14, 15,

17, 19

8, 9, 10

8, 15, 16,

18, 19,

20, 21

3, 6, 7, 8,

9, 10

2, 3, 4

2, 18, 21

6, 7

9, 15,

17, 18

1, 6, 8

9, 16, 20

7, 17, 18

2, 10

1, 2

11, 12

22, 23

11, 12

ASSIGNMENT CLASSIFICATION TABLE (BY LEARNING OBJECTIVE)

Learning Objectives

Questions

Brief

Exercises

Exercises

Problems

Concepts

for

Analysis

1. Identify the types of accounting

changes.

2. Describe the accounting for

changes

in accounting principles.

1, 2, 3, 4

CA22-4

4. Understand how to account for

impracticable changes.

11

2

5. Describe the accounting for

changes

in estimates.

12

4, 5, 9

6, 7, 8, 9,

10, 11, 12

1, 2, 3,

4, 6

CA22-5,

CA22-6

7. Describe the accounting for

correction of errors.

15, 16, 17,

18, 19, 20,

6, 7, 8, 10

7, 8, 9, 15,

16, 17, 18,

1, 2, 3, 6,

7, 8, 9, 10

8. Identify economic motives for

changing accounting methods.

21

9, 10

*10. Make the computations and

prepare the entries necessary

to record a change from or to

the equity method of

accounting.

11, 12

22, 23

11, 12

ASSIGNMENT CHARACTERISTICS TABLE

Item

Description

Level of

Difficulty

Time

(minutes)

E22-1

Change in principle—long-term contracts.

Moderate

10–15

E22-2

Change in principle—inventory methods.

Moderate

10–15

E22-3

Accounting change.

Difficult

25–30

E22-4

Accounting change.

Difficult

25–30

E22-5

Accounting change.

Difficult

30–35

E22-6

Accounting changes—depreciation.

Difficult

30–35

E22-7

Change in estimate and error; financial statements.

25–30

E22-8

Accounting for accounting changes and errors.

Simple

E22-9

Error and change in estimate—depreciation.

Simple

15–20

E22-10

Depreciation changes.

Moderate

20–25

E22-12

Simple

20–25

E22-13

Change in principle—long-term contracts.

Simple

10–15

E22-14

Various changes in principle—inventory methods.

Moderate

20–25

E22-15

Error correction entries.

Simple

15–20

E22-16

Error analysis and correcting entry.

Simple

10–15

E22-17

Error analysis and correcting entry.

Simple

10–15

E22-18

Error analysis.

Moderate

25–30

E22-19

Error analysis and correcting entries.

Simple

20–25

E22-20

Error analysis.

Moderate

20–25

E22-21

Error analysis.

Moderate

10–15

*E22-22

Change from fair value to equity.

Complex

25–30

*E22-23

Change from equity to fair value.

Moderate

15–20

P22-1

Change in estimate and error correction.

Moderate

30–35

P22-2

Comprehensive accounting change and error analysis problem.

Complex

30–40

P22-3

Error corrections and accounting changes.

Complex

30–40

P22-4

Accounting changes.

Moderate

40–50

P22-5

Change in principle—inventory—periodic.

Moderate

30–35

P22-6

Accounting change and error analysis.

Moderate

25–30

P22-7

Error corrections.

Moderate

25–30

P22-8

Comprehensive error analysis.

Difficult

30–35

P22-9

Error analysis.

Moderate

20–25

P22-10

Error analysis and correcting entries.

Complex

50–60

*P22-11

Fair value to equity method with goodwill.

Moderate

20–25

*P22-12

Change from fair value to equity method.

Moderate

20–25

CA22-1

Analysis of various accounting changes and errors.

Moderate

25–35

CA22-2

Analysis of various accounting changes and errors.

Moderate

20–30

CA22-3

Analysis of three accounting changes and errors.

Moderate

30–35

CA22-4

Analysis of various accounting changes and errors.

Moderate

20–30

CA22-5

Change in principle, estimate.

Moderate

20–30

CA22-6

Change in estimate, ethics.

Moderate

20–30

SOLUTIONS TO CODIFICATION EXERCISES

CE22-1

Master Glossary

(a) A change that has the effect of adjusting the carrying amount of an existing asset or liability or

altering the subsequent accounting for existing or future assets or liabilities. A change in accounting

estimate is a necessary consequence of the assessment, in conjunction with the periodic presen–

(b) A change from one generally accepted accounting principle to another generally accepted

accounting principle when there are two or more generally accepted accounting principles that

apply or when the accounting principle formerly used is no longer generally accepted. A change

in the method of applying an accounting principle also is considered a change in accounting

principle.

CE22-2

According to FASB ASC 250-10–50-7 (Accounting Changes and Error Corrections—Disclosure):

When financial statements are restated to correct an error, the entity shall disclose that its previously

issued financial statements have been restated, along with a description of the nature of the error. The

entity also shall disclose both of the following:

CE22-3

According to FASB ASC 250-10–45-5 (Accounting Changes and Error Corrections—Other Presentation

Matters):

An entity shall report a change in accounting principle through retrospective application of the new

accounting principle to all prior periods, unless it is impracticable to do so. Retrospective application

requires all of the following:

(a) The cumulative effect of the change to the new accounting principle on periods prior to those

CE22-4

According to FASB ASC 250-10-S99-4 (Accounting Changes and Error Corrections—SEC Materials):

Question 5: If a registrant justified a change in accounting method as preferable under the circum–

stances, and the circumstances change, may the registrant revert to the method of accounting used

before the change?

ANSWERS TO QUESTIONS

1. The major reasons why companies change accounting methods are:

(a) Desire to show better profit picture.

2. (a) Change in accounting principle; retrospective application is generally not made because it is

impracticable to determine the effect of the change on prior years. The FIFO inventory amount

is therefore generally the beginning inventory in the current period.

3. The three approaches suggested for reporting changes in accounting principles are:

(a) Currently—the cumulative effect of the change is reported in the current year’s income as

a special item.

4. The FASB believes that the retrospective approach provides financial statement users the most

useful information. Under this approach, the prior statements are changed on a basis consistent

with the newly adopted standard; any cumulative effect of the change for prior periods is recorded

as an adjustment to the beginning balance of retained earnings of the earliest period reported.

5. The indirect effect of a change in accounting principle reflects any changes in current or future

cash flows resulting from a change in accounting principle that is applied retrospectively. An

6. A change in an estimate is simply a change in the way an individual perceives the realizability of

an asset or liability. Examples of changes in estimate are: (1) change in the realizability of trade

receivables, (2) revisions of estimated lives, (3) changes in estimates of warranty costs, and

Questions Chapter 22 (Continued)

7. This is an example of a situation in which it is difficult to differentiate between a change in account–

ing principle and a change in estimate. In such a situation, the change should be considered a

8. (a) Charge to expense—possibly separately disclosed.

(b) Change in estimate that is effected by a change in accounting principle—currently and

prospectively.

9. This change is to be handled as a correction of an error. As such, the portion of the change

attributable to prior periods ($23,000) should be reported as an adjustment to the beginning

10. Preferability is a difficult concept to apply. The problem is that there are no basic objectives to

indicate which is the most preferable method, assuming a selection between two generally accepted

11. When a company changes to the LIFO method, the base-year inventory for all subsequent LIFO

calculations is the beginning inventory in the year the method is adopted. This assumes that prior

12. Where individual company statements were reported in prior years and consolidated financial

statements are to be prepared this year, the following reporting and disclosure practices should

be implemented:

(1) The financial statements of all prior periods presented should be restated to show the

13. This change represents a change in reporting entity. This type of change should be reported by

restating the financial statements of all prior periods presented to show the financial information

Questions Chapter 22 (Continued)

14. Counterbalancing errors are errors that will be offset or corrected over two periods. Non-

15. A correction of an error in previously issued financial statements should be handled as a prior–

period adjustment. Thus, such an error should be reported in the year that it is discovered as an

adjustment to the beginning balance of retained earnings. And, if comparative statements are

16. This change represents a change from an accounting principle that is not generally accepted to

an accounting principle that is acceptable. As such, this change should be handled as a

correction of an error. Thus, in the 2014 statements, the cumulative effect of the change should

17. Retained earnings is correctly stated at December 31, 2016. Failure to accrue salaries in earlier

years is a counterbalancing error that has no effect on 2016 ending retained earnings.

18. December 31, 2015

Machinery …………………………………………………………………………………….. 6,000

Accumulated Depreciation—Equipment ……………………………………… 600

19. The amortization error decreases net income by $2,700 in 2014. Interest expense related to the

discount should have been charged for $300, but was charged for $3,000. The entry to correct for

this error is as follows:

Questions Chapter 22 (Continued)

20. This error has no effect on net income because both purchases and inventory were understated.

The entry to correct for this error, assuming a periodic inventory system, is:

SOLUTIONS TO BRIEF EXERCISES

BRIEF EXERCISE 22-1

Construction in Process ($120,000 – $80,000) ……… 40,000

BRIEF EXERCISE 22-2

Difference in profit-sharing expense—prior years

BRIEF EXERCISE 22-3

Inventory ……………………………………………………….….. 1,200,000

BRIEF EXERCISE 22-4

This is a change in estimate effected by a change in accounting principle.

Cost of depreciable assets …………………………………. $250,000

BRIEF EXERCISE 22-5

Depreciation Expense ………………………………………………. 24,000

Accumulated Depreciation—Equipment ……………… 24,000

BRIEF EXERCISE 22-6

Equipment……………………………………………………………….. 50,000

BRIEF EXERCISE 22-7

BEIDLER COMPANY

Retained Earnings Statement

For the Year Ended December 31, 2014

Retained earnings, January 1, as previously reported ……. $2,000,000

BRIEF EXERCISE 22-8

2014

2015

a.

Overstated

Overstated

c.

Understated

Overstated

Overstated

Understated

BRIEF EXERCISE 22-9

1. The change to a three-year remaining life for the purpose of computing

depreciation on production equipment is a change in estimate due to a

change in conditions.

BRIEF EXERCISE 22-10

1. Both FIFO and LIFO are generally accepted accounting principles;

thus, this item is a change in accounting principle.

*BRIEF EXERCISE 22-11

Cash ($95,000 X 10%) …………………………………………….. 9,500

*BRIEF EXERCISE 22-12

Equity Investments (Equity Method)

($475,000 + $33,000) ………………………………………….. 508,000

Cash ………………………………………………………………. 475,000

SOLUTIONS TO EXERCISES

EXERCISE 22-1 (10–15 minutes)

(a) The net income to be reported in 2015, using the retrospective approach,

would be computed as follows:

(b) Construction in Process………………………………… 190,000

Deferred Tax Liability ($190,000 X 35%) …….. 66,500

EXERCISE 22-2 (10–15 minutes)

(a) Inventory …………………………………………………………. 14,000*

Retained Earnings ……………………………………… 14,000

*($19,000 + $23,000 + $25,000) – ($15,000 + $18,000 + $20,000)

EXERCISE 22-3 (25–30 minutes)

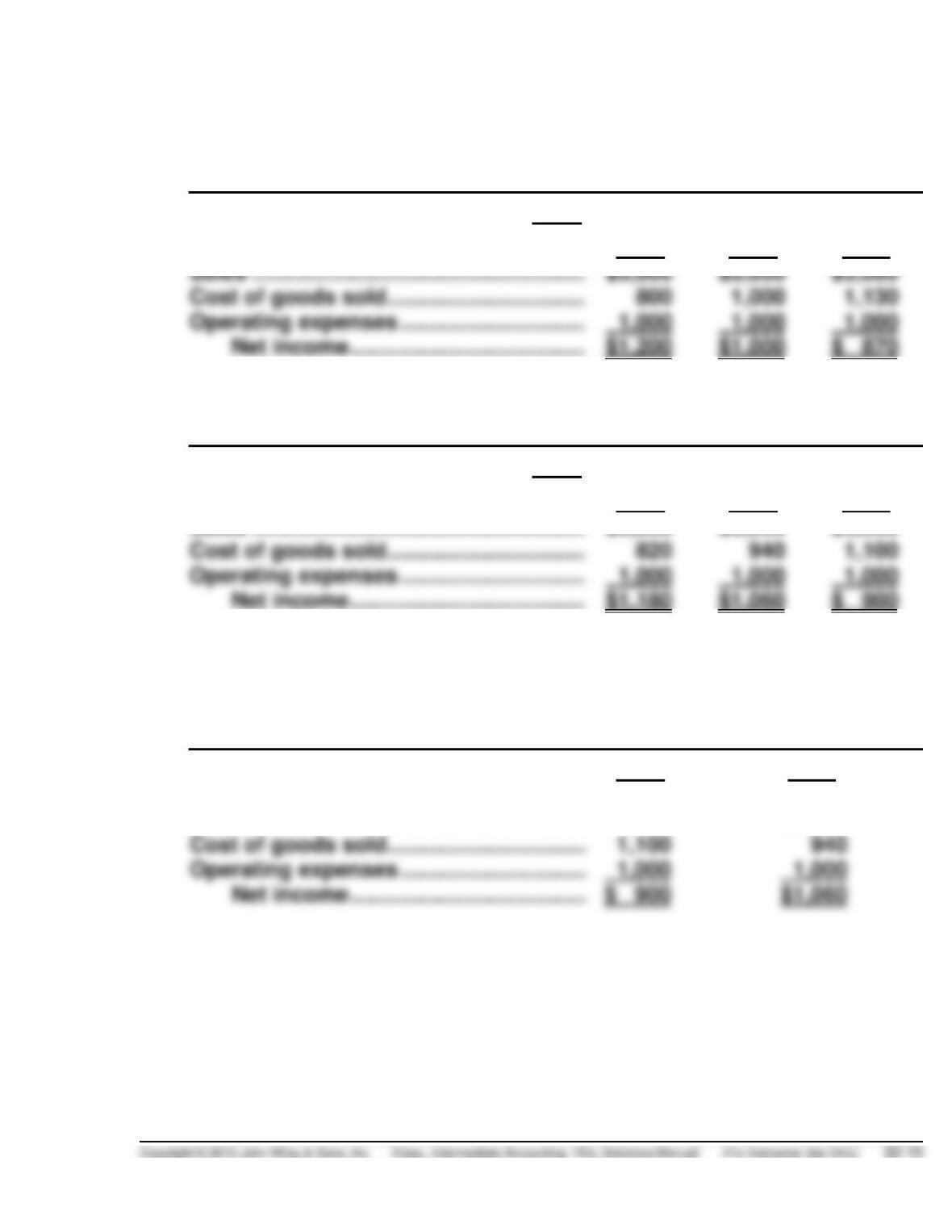

(a) TAVERAS CO.

Income Statement

For the Year Ended December 31

LIFO

2012

2013

2014

Sales ………………………………………………..

$3,000

$3,000

$3,000

Cost of goods sold …………………………….

Operating expenses …………………………..

Net income ………………………………….

$1,200

$1,000

$ 870

Income Statement

For the Year Ended December 31

FIFO

2012

2013

2014

Sales ………………………………………………..

$3,000

$3,000

$3,000

Cost of goods sold …………………………….

Operating expenses …………………………..

Net income ………………………………….

$1,180

$1,060

$ 900

(b) TAVERAS CO.

Income Statement

For the Year Ended December 31

2014

2013

As adjusted (Note A)

Sales …………………………..……………………

$3,000

$3,000

Cost of goods sold …………………………….

Operating expenses …………………………..

Net income ………………………………….

$ 900

$1,060

EXERCISE 22-3 (Continued)

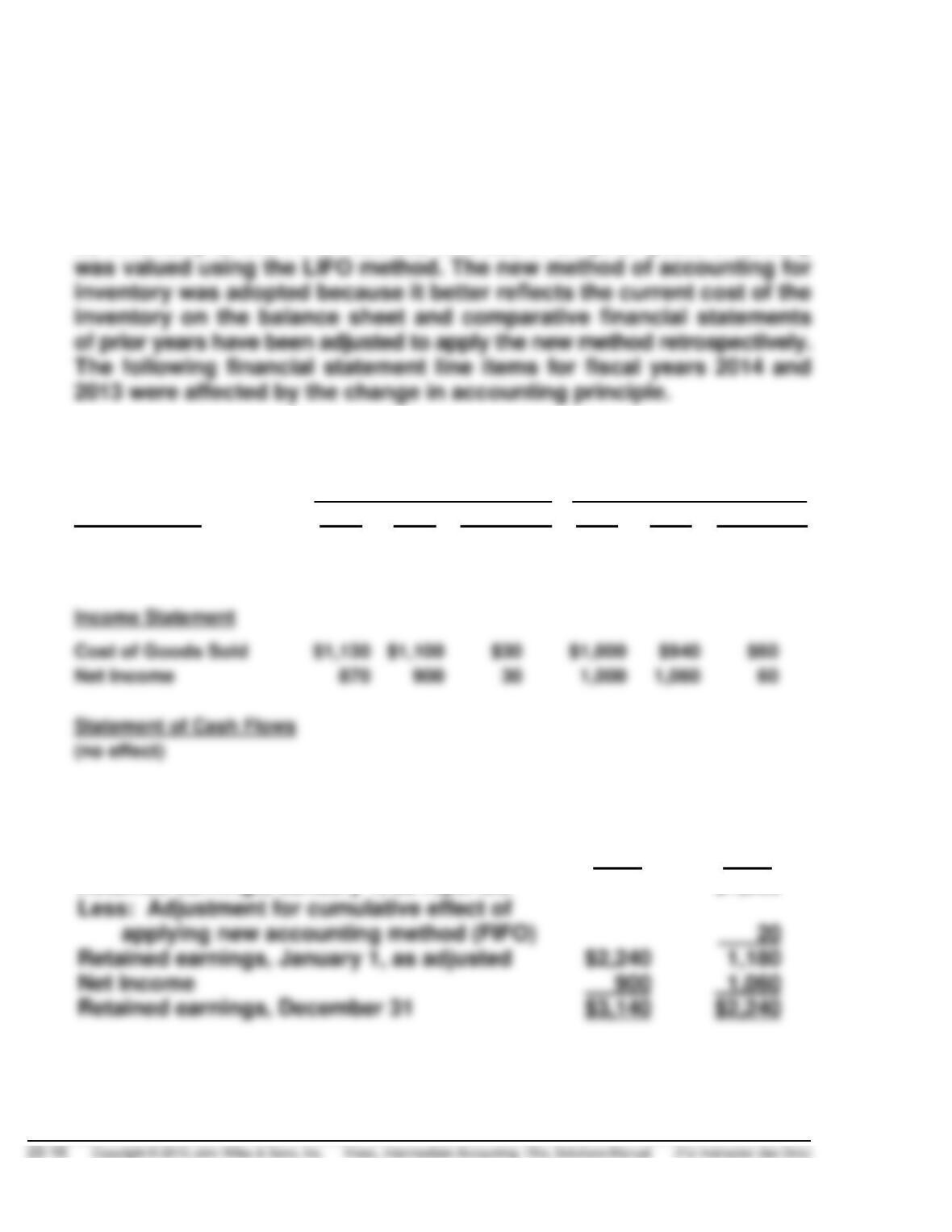

(c) Note A:

Change in Method of Accounting for Inventory Valuation

On January 1, 2014, Taveras elected to change its method of valuing

its inventory to the FIFO method, whereas in all prior years inventory

2014

2013

Balance Sheet

LIFO

FIFO

Difference

LIFO

FIFO

Difference

Inventory

$ 320

$ 390

$70

$ 200

$ 240

$40

Retained Earnings

3,070

3,140

70

2,200

2,240

40

Income Statement

Cost of Goods Sold

$1,130

$1,100

$1,000

Net Income

30

1,000

1,060

60

(no effect)

(d) Retained earnings statements after retrospective application.

2014

2013

Retained earnings, January 1, as reported

$1,200

Retained earnings, January 1, as adjusted

$2,240

Net Income

900

EXERCISE 22-4 (25–30 minutes)

2011

(a) Retained earnings, January 1, as reported …………….. $160,000

Cumulative effect of change in accounting

2014

(b) Retained earnings, January 1, as reported …………….. $590,000

Cumulative effect of change in accounting

2015

(c) Retained earnings, January 1, as reported …………….. $780,000

Cumulative effect of change in accounting

2012 2013 2014

(d) Net Income ……………………….. $130,000 $290,000 $310,000

EXERCISE 22-5 (30–35 minutes)

(a) KENSETH COMPANY

Income Statement

For the Year Ended

2014

2013

Sales ………………………………………………………..

$3,000

$3,000

Cost of goods sold ……………………………………

1,100

940

Operating expenses

Income before profit sharing ……………….

$ 900

$1,060

Profit sharing expense ………………………………

Net income …………………………………………

(b) The profit sharing expense reflects an indirect effect of the change in

accounting principle. Under GAAP, indirect effects from periods before

(c) Retained Earnings Statement

2014

Retained earnings, January 1, as reported …………….. $8,000

Cumulative effect of change to FIFO ($960 – $900) …… 60

EXERCISE 22-6 (30–35 minutes)

(a) Depreciation to date on equipment

Sum-of-the-years’-digits depreciation

2012 (5/15 X $510,000) $170,000

2013 (4/15 X $510,000) 136,000

(b) Depreciation to date on building

$693,000/30 years = $23,100 per year

$23,100 X 3 = $69,300 depreciation to date

EXERCISE 22-7 (25–30 minutes)

Change from sum-of-the-years digit to straight-line

Cost of depreciable assets …………………………... $100,000

DENISE HABBE INC.

Retained Earnings Statement

For the Year Ended

2015

2014

Retained earnings, January 1, unadjusted ………..

$125,000

$157,000

Note to instructor:

1. 2014 Cost of sales increased $24,000; 2015 cost of sales decreased

$24,000. As a result, net income for 2014 is overstated $24,000 and

net income for 2015 is understated $24,000 as a result of the

inventory error.