SOLUTIONS TO CONCEPTS FOR ANALYSIS

CA 23-1

(a) The main purpose of the statement of cash flows is to show the change in cash from one period to

the next. Another objective of a statement of the type shown is to summarize the financing and

(b) The following are weaknesses in form and format of Maloney Corporation’s Statement of Sources

and Application of Cash:

1. The title of the statement should be Statement of Cash Flows.

2. The statement should add back to (or deduct from) net income certain items that did not use

(or provide) cash during the period. The resulting total should be described as net cash provided

(c) 1. (i) The $25,000 option plan salaries and wages expense should be included in the statement

as an amount added back to net income, an expense not requiring the outlay of cash

during the period.

(ii) Since the statement balances and no reference is made to the $25,000 salaries and wages

expense, it appears the expense was not recorded or that there is an offsetting error

elsewhere in the statement.

3. Stock dividends or stock splits need not be disclosed in the statement because these trans-

actions do not significantly affect financial position.

4. The issuance of the 16,000 shares of common stock in exchange for the preferred stock

CA 23-1 (Continued)

6. The details of changes in long-term debt should be shown separately. Payments should not be

CA 23-2

(a) From the information given, it appears that from an operating standpoint Pacific Clothing Store did

not have a superb first year, having suffered an $11,000 net loss. Lenny is correct; the statement of

cash flows is not prepared in correct form. The sources and uses format is not an acceptable form.

in cash.

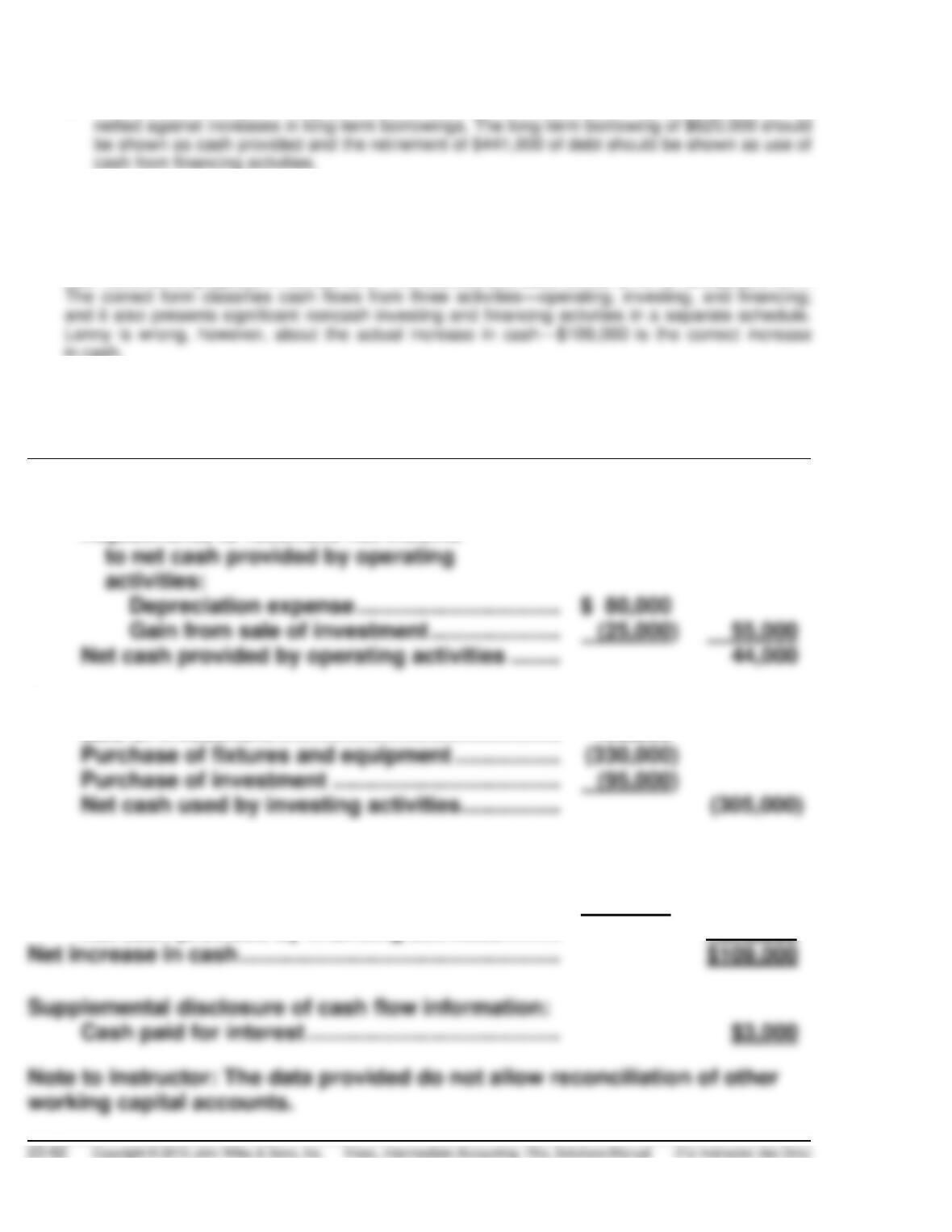

(b) PACIFIC CLOTHING STORE

Statement of Cash Flows

For the Year Ended January 31, 2014

Cash flows from operating activities

Net loss ……………………………………………………….

$ (11,000)*

Adjustments to reconcile net income

to net cash provided by operating

activities:

Depreciation expense …………………………...

Gain from sale of investment …………………

Net cash provided by operating activities ……..

Cash flows from investing activities

Sale of investment ……………………………………….

120,000

Purchase of fixtures and equipment ……………..

Purchase of investment ……………………………….

Net cash used by investing activities …………….

Cash flows from financing activities

Sale of capital stock …………………………………….

380,000

Purchase of treasury stock …………………………..

(10,000)

Net cash provided by financing activities ………

370,000

Supplemental disclosure of cash flow information:

CA 23-2 (Continued)

Noncash investing and financing activities

Issuance of note for truck ………………………………..

$ 30,000

*Computation of net income (loss)

Sales of merchandise ………………………………………

$382,000

Interest revenue ………………………………………………

25,000

Total revenues………………………………………….

Merchandise purchases …………………………………..

Depreciation ……………………………………………………

Total expenses …………………………………………

Net loss ………………………………………………………….

CA 23-3

1. The earnings are treated as an inflow of cash and should be reported as part of the net cash

2. The $315,000 depreciation expense is neither an inflow nor an outflow of cash. Because

depreciation is an expense, it was deducted in the computation of net income. Accordingly, the

$315,000 must be added back to income before extraordinary items in the operating activities

section because it was deducted in determining earnings, but it was not a use of cash.

3. The write-off of uncollectible accounts receivable against the allowance account has no effect on

cash because the net accounts receivable remain unchanged. An adjustment to income is only

necessary if the net receivable amount increases or decreases. Because the net receivable amount

4. The $6,000 gain realized on the sale of the machine is an ordinary gain, not an extraordinary gain,

5. Generally, extraordinary items are investing or financing activities and the cash inflow or outflow

resulting from such events should be reported in the investing or financing activities section of the

CA 23-3 (Continued)

6. The $75,000 use of cash should be reported as a cash outflow from investing activities. The

CA 23-4

Where to Present

How to Present

1.

Investing and operating

Cash provided by sale of fixed assets, $4,750 as an investing

activity. In addition, the loss of $2,250 ([($20,000 x 31/2) ÷ 10] –

$4,750) on the sale would be added back to net income.

3.

Financing

Cash provided by the issuance of capital stock of $16,000.

depreciation of $2,000 and amortization of $400 are added

back to the loss from operations. Net cash provided by operating

activities is $300.

5.

Not reported in statement.

6.

Investing and operating

Cash provided by the sale of the investment, $10,600 as an

investing activity. The loss of $1,400 is added back to net

income.

of $24,240. Additionally, the gain (of $1,760 = $26,000 –

$24,240) is deducted from net income in the operating activities

section.

CA 23-5

(a) The primary purpose of the statement of cash flows is to provide information concerning the cash

receipts and cash payments of a company during a period. The information contained in the

statement of cash flows, together with related disclosures in other financial statements, may help

(b) The statement of cash flows classifies cash inflows and outflows as those resulting from operating

activities, investing activities, and financing activities.

Cash inflows from operating activities include receipts from the sale of goods and services,

CA 23-5 (Continued)

Cash inflows from investing activities include receipts from collections or sales of debt instruments

of other companies, from the sale of the investments in those stocks, and from sales of various

productive fixed assets. Cash outflows for investing activities include payments for stocks of other

companies, purchase of productive fixed assets, and debt instruments of other companies.

Cash inflows from financing activities include proceeds from the company issuing its own stock or

CA 23-6

(a) It is true that selling current assets, such as receivables and notes to factors, will generate cash

flows for the company, but this practice does not cure the systemic cash problems for the

(b) Barbara Brockman should be told that if she executes her plan, the company may not survive.

While the factoring of receivables and the liquidation of inventory will indeed generate cash, the

actual amount of cash the company receives will be less than the carrying value of the receivables

and the raw materials. In addition, the company would still have the future expenditure of

replenishing its raw materials inventories, at a cost higher than the sales price.

FINANCIAL REPORTING PROBLEM

(a) P&G uses the indirect method to compute and report net cash provided

by operating activities. The amounts of net cash provided by operating

(b) The most significant item in the investing activities section is the

$3,306 million that P&G spent on “capital expenditures.” The most sig–

nificant item in the financing activities section is the $7,039 million

that P&G paid to purchase treasury stock.

COMPARATIVE ANALYSIS CASE

(a) Both Coca-Cola and PepsiCo use the indirect method of computing and

reporting net cash provided by operating activities in 2009–2011.

(b) The most significant investing activities items in 2011:

Coca-Cola

Proceeds from disposal of short term investments $5,647 million

(c) The Coca-Cola Company has increased net cash provided by operating

activities from 2009 to 2011 by $1,288 million or 15.7%. PepsiCo, Inc.

has increased net cash provided by operating activities by $2,148

(d) Both Coca-Cola and PepsiCo report depreciation and amortization in

the operating activities section:

COMPARATIVE ANALYSIS CASE (Continued)

(e)

Coca-Cola

PepsiCo

(f) The current cash debt coverage ratio uses cash generated from

operations during the period and provides a better representation of

liquidity on an average day. PepsiCo’s ratio of $0.53 of cash flow from

operations for every dollar of current debt was approximately 20%

FINANCIAL STATEMENT ANALYSIS CASE

VERMONT TEDDY BEAR CO.

(a) Even though prior year income exceeded the current year income by

$821,432 ($838,955 – $17,523), the current year cash flow from

operations exceeded prior year’s cash flow from operations by

$937,437 [$236,480 – ($700,957).]. This apparent paradox can be

explained by evaluating the components of net cash flow from

inventories did increase by $1,599,014.

(b) Liquidity: current cash debt coverage ratio (net cash provided by

operating activities ÷ average current liabilities)

$236,480 ÷ (($4,055,465 + $1,995,600) ÷ 2) = .078:1

Solvency: cash debt coverage (net cash provided by operating

activities ÷ average total liabilities)

ACCOUNTING, ANALYSIS, AND PRINCIPLES

Accounting

LASKOWSKI COMPANY

Statement of Cash Flows

For the Year Ended December 31, 2014

Cash flows from operating activities

Net income …………………………………………………… $ 430,000

Cash flows from investing activities

Sale of machinery …………………………………………. 270,000

Purchase of machinery………………………………….. (750,000)

Net cash used by investing activities ……………… (480,000)

Analysis

Laskowski’s free cash flow is:

Net cash provided by operating activities …… $1,222,000

ACCOUNTING, ANALYSIS, AND PRINCIPLES (Continued)

Laskowski’s free cash flow for the current year ($272,000) is less than the

amount needed for expansion next year ($500,000). Thus, assuming

Principles

According to Statement of Financial Accounting Concepts No. 1, paragraph

37, “Financial reporting should provide information to help present and

potential investors and creditors and other users in assessing the

amounts, timing, and uncertainty of prospective cash receipts from

PROFESSIONAL RESEARCH

(a) According to FASB ASC 230–10-10 (Statement of Cash Flows/Overall/

Objectives):

10-1 The primary objective of a statement of cash flows is to provide

relevant information about the cash receipts and cash payments

of an entity during a period.

As indicated in the glossary at this same section (230-10-20), cash

includes not only currency on hand but demand deposits with banks or

other financial institutions. Cash also includes other kinds of accounts

(b) See FASB ASC 230-10-10 (Statement of Cash Flows—Objectives)

10-2 The information provided in a statement of cash flows, if used

with related disclosures and information in the other financial

statements, should help investors, creditors, and others (including

donors) to do all of the following:

a. Assess the entity’s ability to generate positive future net cash

flows