PROBLEM 6-15

(a) The expected cash flows to meet the asset retirement obligation repre-

sent a deferred annuity. Developing a fair value estimate requires

determining the present value of the annuity of expected cash flows

to be paid in three years and then determine the present value of that

amount today.

Cash Flow Probability

Estimate X Assessment = Expected Cash Flow

$15,000 10% $ 1,500

The value today of the annuity payments to commence in ten years is:

Alternatively, the present value of the deferred annuity can be computed

as follows:

(b) This fair value estimate is based on unobservable inputs—Murphy’s

own data on the expected future cash flows associated with the

obligation to restore the site. This fair value estimate is considered

Level 3, as discussed in Chapter 2.

FINANCIAL REPORTING PROBLEM

(a) 1. Long-lived assets, goodwill

For impairment of goodwill and long-lived assets, fair value is deter-

(b) (1) The following rates are disclosed in the accompanying notes:

Debt

Weighted-Average Effective Interest Rate

FINANCIAL REPORTING PROBLEM (Continued)

Benefit Plans

Pension Benefits

Other Retiree

Benefits

United States

2011

2010

2011

2010

Discount rate

5.3%

Stock-Based Compensation

Assumptions

2011

2010

2009

used in Stock Option Valuation

(2) There are different rates for various reasons:

1. The maturity dates—short-term vs. long-term.

2. The security or lack of security for debts—mortgages and col–

lateral vs. unsecured loans.

FINANCIAL STATEMENT ANALYSIS CASE

(a) Cash inflows of $375,000 less cash outflows of $125,000 = Net cash

flows of $250,000.

(c) The estimate of future cash flows is very useful. It provides an under–

standing of whether the value of gas and oil properties is increasing

ACCOUNTING, ANALYSIS, AND PRINCIPLES

Accounting

(a) The present value of the note is presumably equal to the fair-value of

the inventory. The note has 20 semi-annual periods to maturity.

Analysis

If interest rates increase, the fair-value of the note will decline. This is

because the remaining cash flows are being discounted at a higher rate.

That is, the present value of the future cash flows is less at a higher

discount rate.

Principles

Fair-value versus historical cost potentially involves a trade-off between

the primary qualities of relevance and faithful representation. The fair-

PROFESSIONAL RESEARCH

Search strings: “present value”, present and value, Present value $, “best

estimate”, “estimated cash flow”, “expected cash flow”, “fresh-start

measurement”, “interest methods of allocation”

2000).

(b) See Appendix B: APPLICATIONS OF PRESENT VALUE IN FASB

STATEMENTS AND APB OPINIONS, CON7, Par. 119

119. . . . The accompanying table is presented to assist readers in

Some examples are:

• Debt payable and related premium or discount

• Asset acquired by incurring liabilities in a business combination—“An

asset acquired by incurring liabilities is recorded at cost—that is, at

the present value of the amounts to be paid” (paragraph 67(b)).

PROFESSIONAL RESEARCH (Continued)

• FASB Statement No. 106, Employers’ Accounting for Postretirement

Benefits Other Than Pensions . . . Effective settlement rate—“. . . as

(c) 1. CON7, Glossary of terms: Best estimate: The single most-likely

amount in a range of possible estimated amounts; in statistics, the

estimated mode. In the past, accounting pronouncements have used

2. CON7, Glossary of terms: Estimated Cash Flow and Expected Cash

Flow: In the past, accounting pronouncements have used the terms

3. CON7, Glossary of terms: Fresh-Start Measurements: Measurements

in periods following initial recognition that establishes a new

carrying amount unrelated to previous amounts and accounting

PROFESSIONAL RESEARCH (Continued)

4. CON7, Glossary of terms: Interest Methods of Allocation: Reporting

conventions that use present value techniques in the absence of a

Note to instructor: The concepts statements are not in the codification.

Thus, the references to previous FASB standards

above do not have codification sections indicated.

PROFESSIONAL SIMULATION

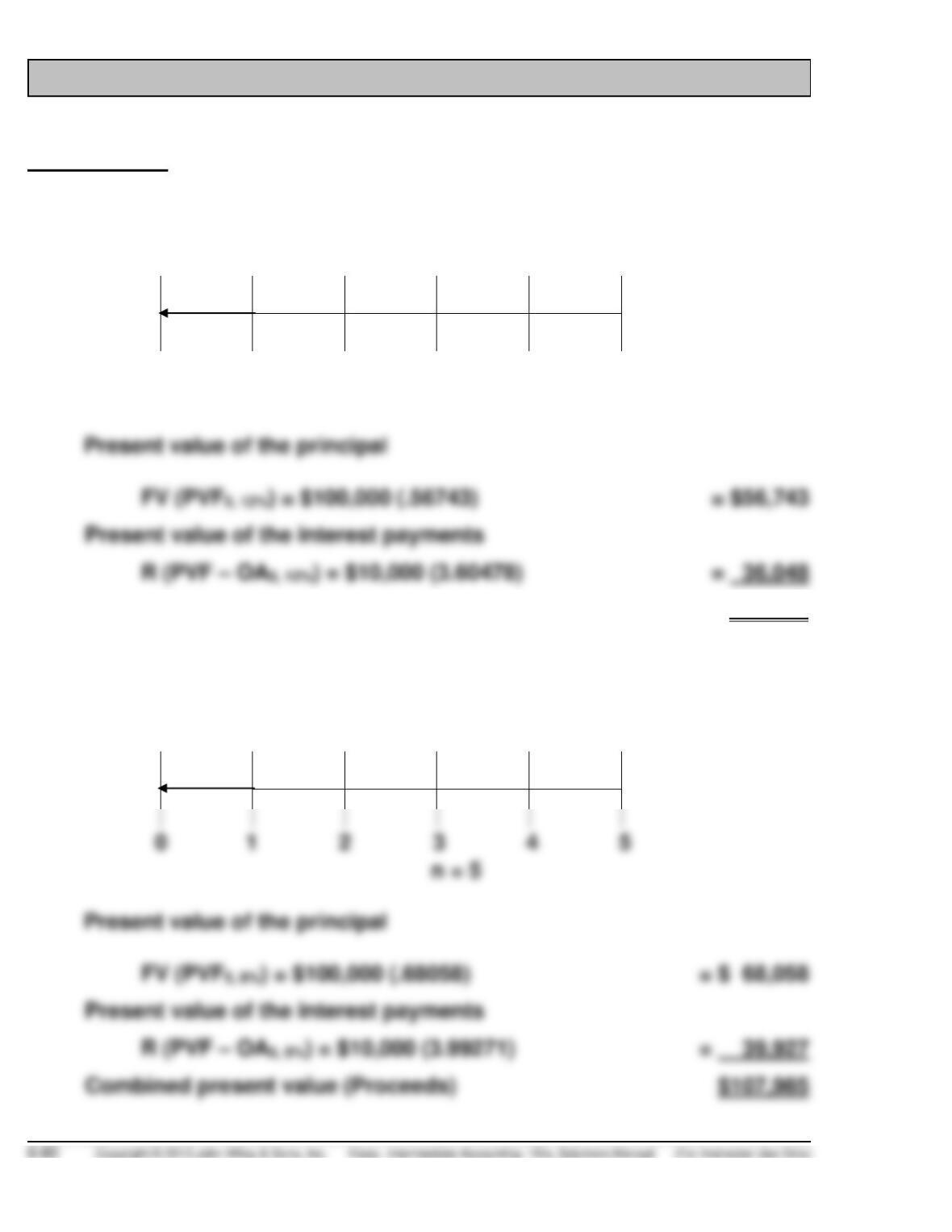

Measurement

i = 12%

Principal

$100,000

Interest

PV – OA = ? $10,000 $10,000 $10,000 $10,000 $10,000

0 1 2 3 4 5

n = 5

FV (PVF5, 12%) = $100,000 (.56743)

Present value of the interest payments

Combined present value (purchase price)

$92,791

i = 8%

Principal

$100,000

Interest

PV – OA = ? $10,000 $10,000 $10,000 $10,000 $10,000

FV (PVF5, 8%) = $100,000 (.68058)

Present value of the interest payments

Combined present value (Proceeds)

PROFESSIONAL SIMULATION (Continued)

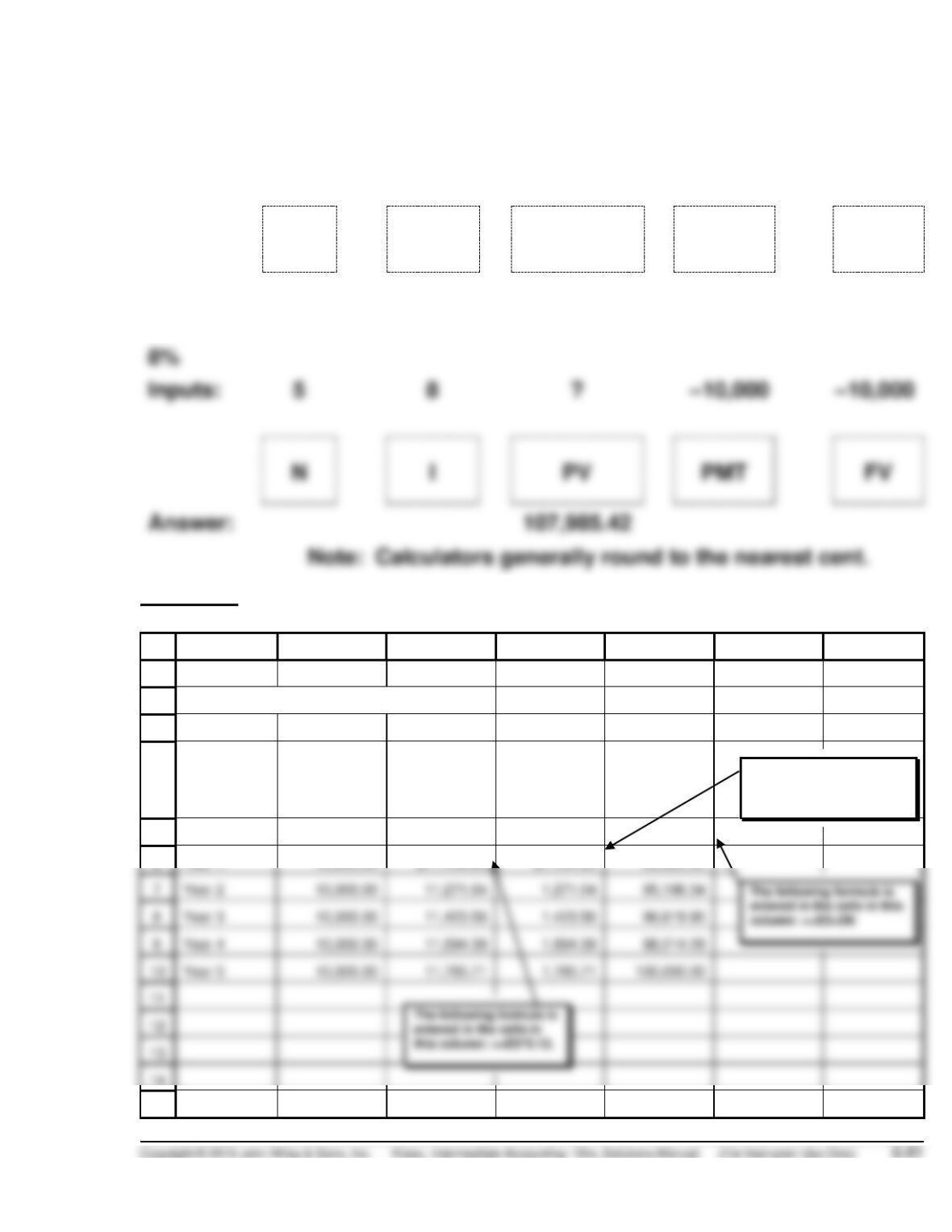

12%

Inputs:

5

12

?

–10,000

–10,000

N

I

PV

PMT

FV

Answer:

92,790.45

Answer:

Valuation

A

B

C

D

E

F

G

1

2

Bond Amortization Schedule

3

4

Date

Cash Interest

Interest

Expense

Bond Discount

Amortization

Carrying

Value of

Bonds

5

Year 0

$92,790.45

6

Year 1

10,000.00

$11,134.85

$1,134.85

93,925.30

7

Year 2

10,000.00

11,271.04

1,271.04

95,196.34

Year 5

10,000.00

11,785.71

1,785.71

100,000.00

14

The following formula is

entered in the cells in

this column: =+E5*0.12.

column: =+E5+D6

15

The following formula is

entered in the cells in this

column: =+C6-B6.