PROBLEM 11-2

Depreciation Expense

2014

2015

(a)

Straight-line:

($89,000 – $5,000) ÷ 7 = $12,000/yr.

2014: $12,000 X 7/12

$7,000

2015: $12,000

$12,000

(b)

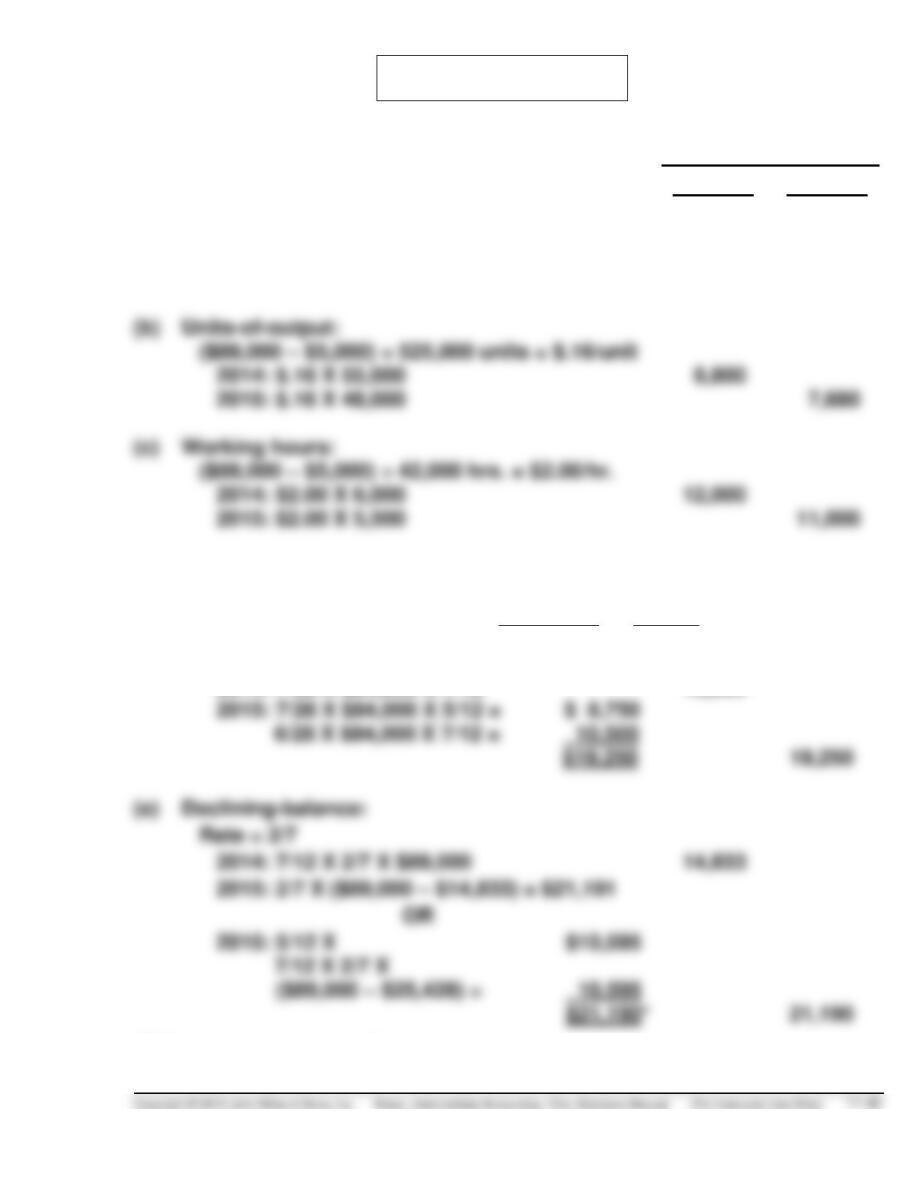

2014: $.16 X 55,000

2015: $.16 X 48,000

(c)

Working hours:

($89,000 – $5,000) ÷ 42,000 hrs. = $2.00/hr.

2014: $2.00 X 6,000

12,000

2015: $2.00 X 5,500

(d)

Sum-of-the-years’-digits:

1 + 2 + 3 + 4 + 5 + 6 + 7 = 28 or

n(n + 1)

=

7(8)

= 28

2

2

2014: 7/28 X $84,000 X 7/12

12,250

2015: 7/28 X $84,000 X 5/12 = $ 8,750

6/28 X $84,000 X 7/12 = 10,500

$19,250

(e)

Declining-balance:

Rate = 2/7

2015: 5/12 X $10,595

$21,190*

*Difference due to rounding.

PROBLEM 11-3

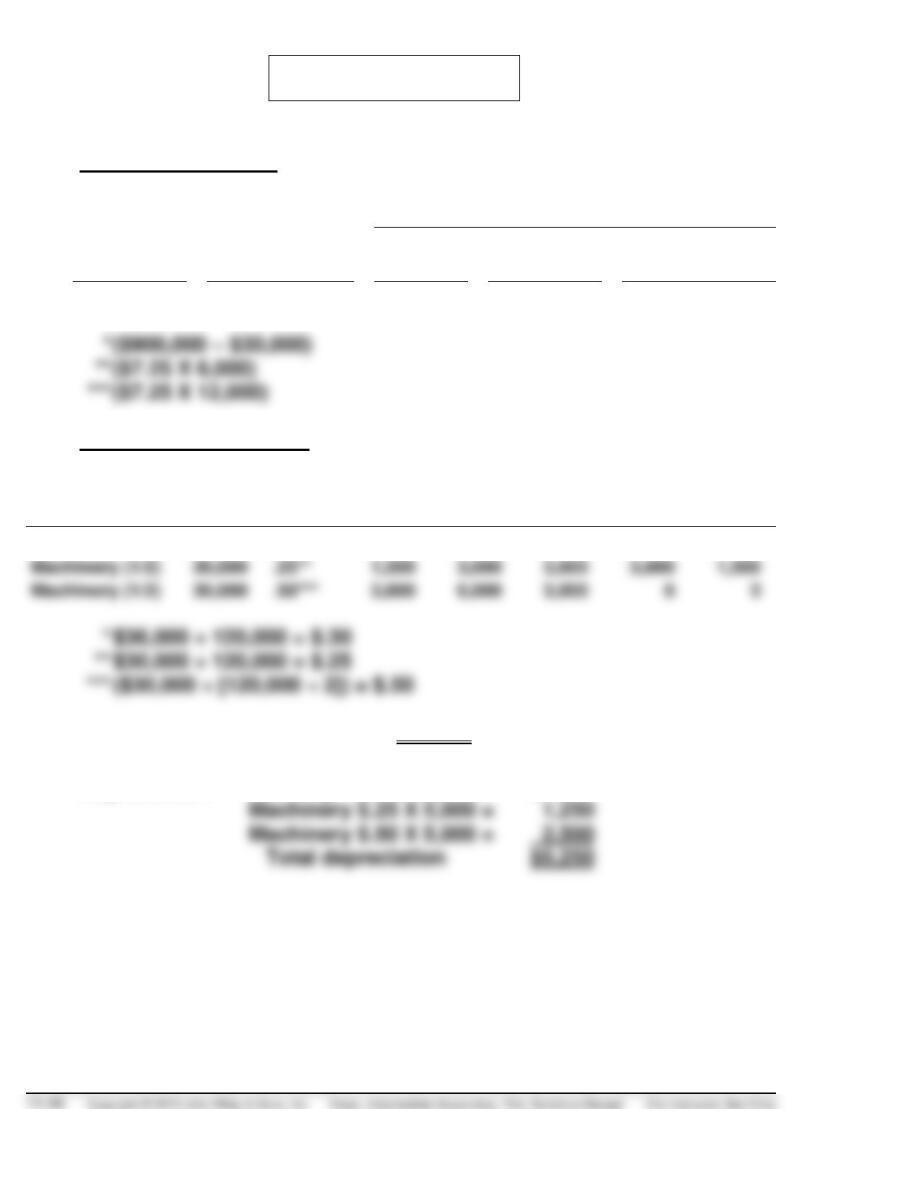

(a)

Depreciation Expense ……………………………………………..

3,900

Accumulated Depreciation—Machinery (A)

(5/55 X [$46,000 – $3,100]) …………………………..

3,900

Accumulated Depreciation—Machinery (A) ………………

35,100

Machinery (A) ($46,000 – $13,000) ……………………

33,000

Gain on Disposal of Machinery ………………………..

2,100

(b)

Depreciation Expense ……………………………………………..

Accumulated Depreciation—Machinery (B)

([$51,000 – $3,000] ÷ 15,000 X 2,100)………………

6,720

(c)

Depreciation Expense ……………………………………………..

6,000

Accumulated Depreciation—Machinery (C)

([$80,000 – $15,000 – $5,000] ÷ 10) …………………

6,000

(d)

Machinery (E) ……………………………………………………….

28,000

Retained Earnings …………………………………………..

28,000

Accumulated Depreciation—Machinery (E) ………

5,600

*($28,000 X .20)

Copyright © 2013 John Wiley & Sons, Inc. Kieso, Intermediate Accounting, 15/e, Solutions Manual (For Instructor Use Only) 11–43

Net

Income

Overstated

(Understated)

$ 3,000

(1,200)

1,800

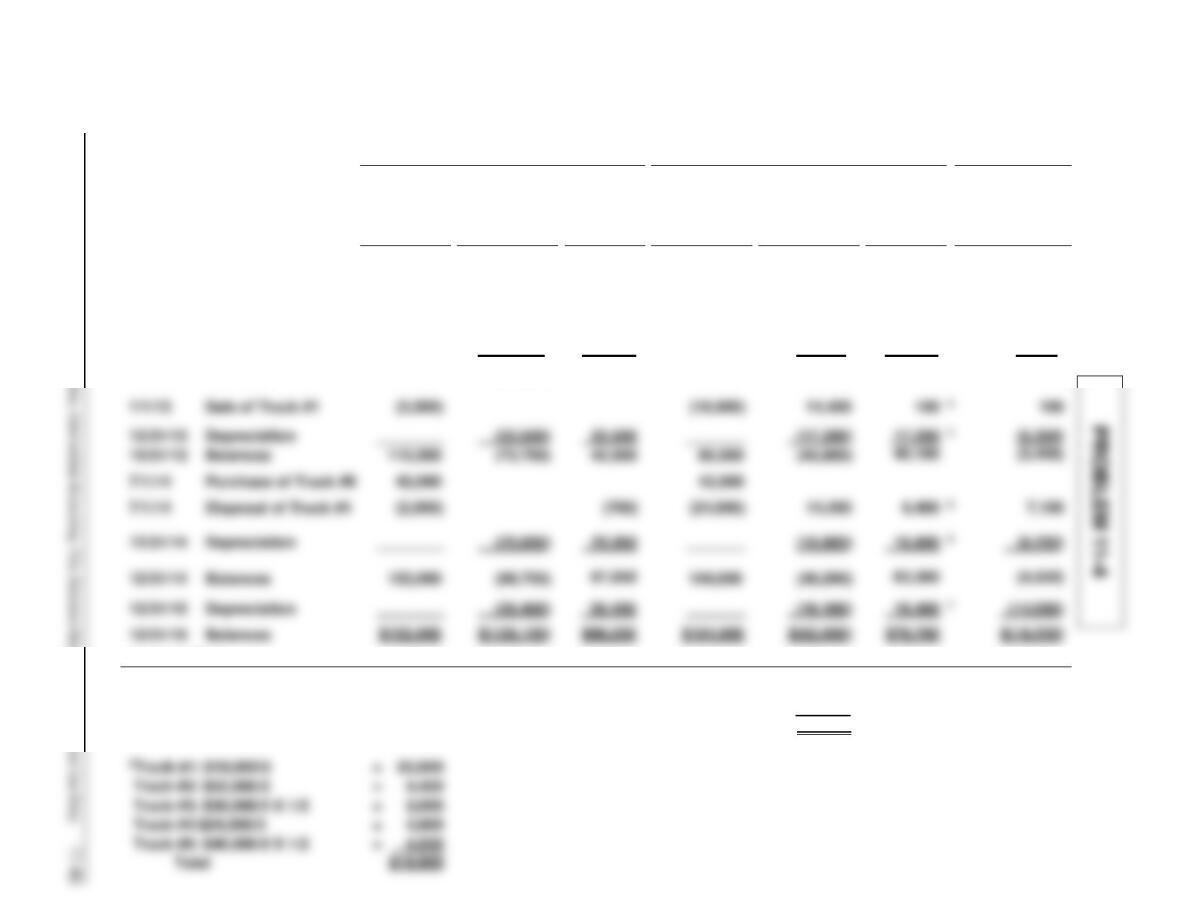

2Truck #1: $18,000/5

1

2

As Adjusted

Retained

Earnings

dr, (cr.)

$ 3,000

19,800

22,800

Acc. Dep.,

Trucks dr,

(cr.)

$(30,200)

9,000

(19,800)

(41,000)

$18,000

(21,000)

$ 3,000

Trucks dr.

(cr.)

$94,000

40,000

(30,000)

_______

104,000

Book value of Truck #3 [$30,000 – ($30,000/5 X 1 1/2 yrs.)] = $30,000 – $9,000 =

Per Company Books

Retained

Earnings

dr. (cr.)

$21,000

21,000

Acc. Dep.

Trucks dr.

(cr.)

$(30,200)

(21,000)

(51,200)

1Implied fair value of Truck #3 ($40,000 – $22,000)

Trucks dr.

(cr.)

$ 94,000

22,000

________

116,000

Balance

Purchase Truck #5

Trade Truck #3

Depreciation

Balances

Income effect

Loss on Trade

(a)

1/1/12

7/1/12

12/31/12

12/31/12

Sale of Truck #1

Disposal of Truck #4

PROBLEM 11-4 (Continued)

3Book value of Truck #1 [$18,000 – ($18,000/5 X 4 yrs.)] =

$18,000 – $14,400 ……………………………………………………

= $3,600

Cash received on sale ……………………………………………………..

= 3,500

Loss on sale …………………………………………………………..

$ 100

$22,000/5

=

$24,000/5

=

Truck #5:

$40,000/5

=

Total

5Book value of Truck #4 $24,000 – [($24,000/5 X 3 yrs.)] …….

= $9,600

Cash received ($700 + $2,500) ………………………………………….

= 3,200

Loss on disposal …………………………………………………….

$6,400

6Truck #2:

$22,000/5 X 1/2

=

$ 2,200

Truck #4:

$24,000/5 X 1/2

=

2,400

$40,000/5

$42,000/5 X 1/2

=

4,200

Total

7Truck #2:

(fully dep.)

=

$40,000/5

=

Truck #6:

$42,000/5

=

Total

(b)

Compound journal entry December 31, 2015:

Accumulated Depreciation—Trucks ………………………

66,550

Trucks …………………………………………………………

Retained Earnings ………………………………………..

Depreciation Expense ………………………………….

PROBLEM 11-4 (Continued)

Summary of Adjustments:

Per

Books

As

Adjusted

Adjustment

Dr. or (Cr.)

Trucks

$152,000

$104,000

$(48,000)

Accumulated Depreciation

$129,150

$ 62,600

$ 66,550

Totals

$ 67,850

$ 63,300

$ (4,550)

Depreciation Expense, 2015

$ 30,400

$ 16,400

$(14,000)

PROBLEM 11-5

(a) Estimated depletion:

Estimated Depletion

Depletion

Base

Estimated

Yield

Per

Ton

1ST & 11th

Yrs.

Each of Yrs.

2-10 Incl.

$870,000*

120,000 tons

$7.25

$43,500**

$87,000***

Estimated depreciation:

Asset

Cost

Per ton

Mined

1st

Yr.

Yrs.

2–5

6th

Yr.

Yrs.

7–10

11th

Yr.

Building

$36,000

$.30*

$1,800

$3,600

$3,600

$3,600

$1,800

(b) Depletion: $7.25 X 5,000 tons = $36,250

Depreciation:

Building $.30 X 5,000 =

$1,500

Machinery $.50 X 5,000 =

Total depreciation

PROBLEM 11-6

(a)

Original cost

$550 X 3,000 =

$1,650,000

Deduct residual value of land

$200 X 3,000 =

600,000

1,050,000

Cost of logging road

150,000

$1,200,000

500,000 ft.

(b)

Inventory ……………………………………………………….

240,000

Timber ……………………………………………………….

240,000

Depletion, 2014: 20% X 500,000 bd. ft. = 100,000 bd. ft.;

100,000 bd. ft. X $2.40 = $240,000

(c)

Loss of timber

[$1,050,000 – ($1,050,000 X 20%)] …………………….

$ 840,000

Cost of salvaging timber ……………………………………

Less: Recovery ($3 X 400,000 bd. ft.) ………………….

$ 340,000

Loss of land value ……………………………………………..

600,000

Logging equipment ……………………………………………

300,000

Extraordinary loss due to the eruption

PROBLEM 11-7

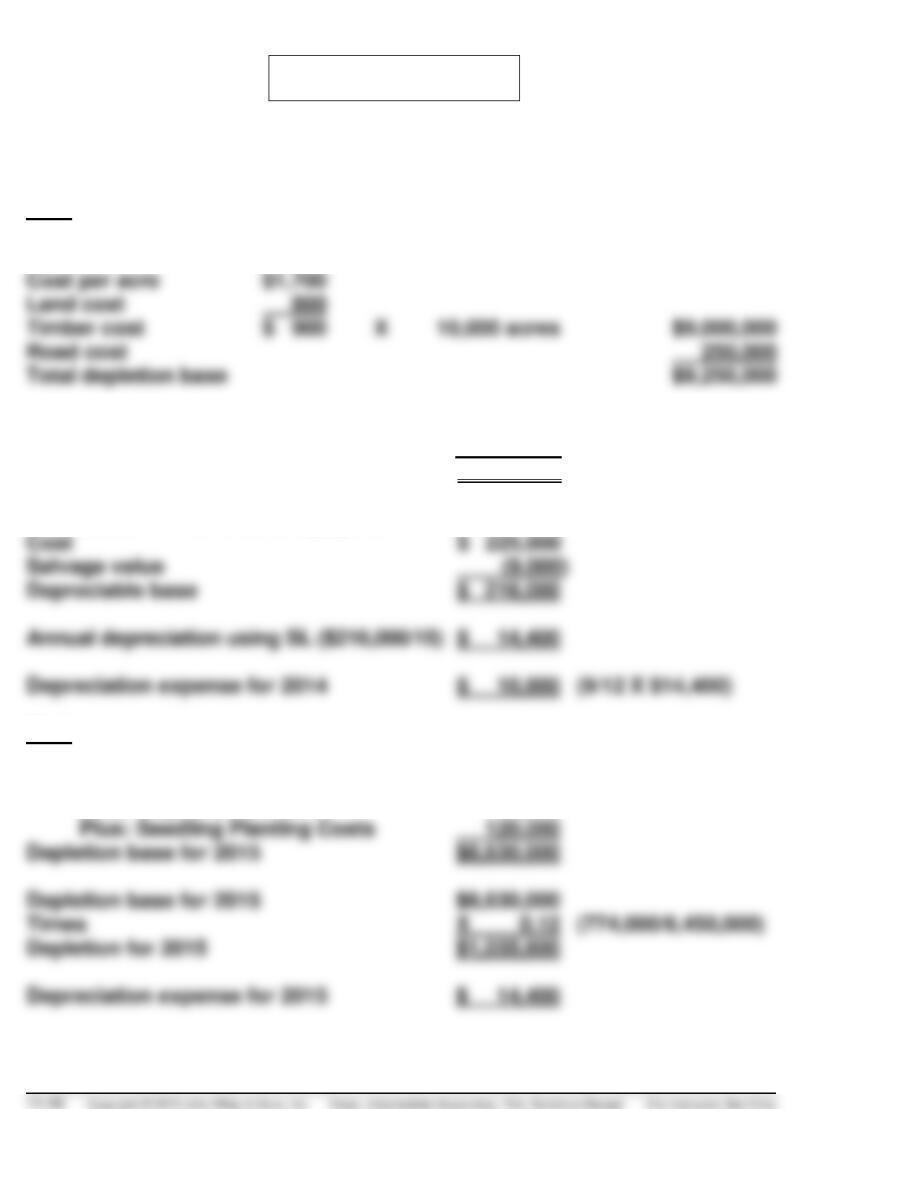

Instructors should note the changing depletion base in this problem.

2014

Computation of depletion base for 2014

Timber

Cost per acre

$1,700

Land cost

800

Timber cost

$ 900

10,000 acres

Road cost

Total depletion base

Estimated depletion for 2014

$9,250,000

X 0.08

(540,000/6,750,000)

Depletion expense for 2014

$ 740,000

Depreciation of removable equipment

Cost

Salvage value

Depreciable base

Annual depreciation using SL ($216,000/15)

Depreciation expense for 2014

(9/12 X $14,400)

2015

Depletion base for 2015

Base for 2014

$9,250,000

Less: Depletion for 2014

740,000

Plus: Seedling Planting Costs

120,000

Depletion base for 2015

$8,630,000

Depletion base for 2015

$8,630,000

Times

(774,000/6,450,000)

Depletion for 2015

$1,035,600

Depreciation expense for 2015

$ 14,400

PROBLEM 11-7 (Continued)

2016

Depletion Base for 2016

Base for 2015

$ 8,630,000

Less: Depletion for 2015

1,035,600

Plus: Seedling Planting Costs

Depletion Base for 2016

$ 7,744,400

Depletion Base for 2016

Times

(650,000/6,500,000)

Depletion for 2016

Depreciation Expense for 2016

$ 14,400

PROBLEM 11-8

(a) The amounts to be recorded on the books of Darby Sporting Goods

Inc. as of December 31, 2014, for each of the properties acquired from

Encino Athletic Equipment Company are calculated as follows:

Cost Allocations to Acquired Properties

Appraisal

Value

Remaining

Purchase

Price

Allocations

Renovations

Capitalized

Interest

Total

(1) Land

$290,000

$290,000

(2) Buildings

Supporting Calculations

1Balance of purchase price to be allocated.

Total purchase price …………………………………………………..

$400,000

Less: Land appraisal …………………………………………………..

Machinery

PROBLEM 11-8 (Continued)

2Capitalizable interest.

Expenditures

Capitalization

Period

Weighted-Average

Accumulated Expenditures

Date

Amount

1/1

$ 50,000

12/12

$ 50,000

4/1

90,000

$500,000

$175,000

Note to instructor: If the interest is allocated between the building and the

machinery, $14,700 ($21,000 X 105/150) would be allocated to the building

and $6,300 ($21,000 X 45/150) would be allocated to the machinery.

(b) Darby Sporting Goods Inc.’s 2015 depreciation expense, for book

purposes, for each of the properties acquired from Encino Athletic

Equipment Company is as follows:

1.

Land: No depreciation.

= Cost X Rate X 1/2 year

3.

Machinery: Depreciation rate

= 2.00 X 1/5 = .40

PROBLEM 11-8 (Continued)

(c) Arguments for the capitalization of interest costs include the following.

1. Diversity of practices among companies and industries called for

standardization in practices.

2. Total interest costs should be allocated to enterprise assets and

PROBLEM 11-9

(a) Carrying value of asset: $10,000,000 – $2,500,000* = $7,500,000.

*($10,000,000 ÷ 8) X 2

(b) Depreciation Expense …………………………………….. 1,400,000**

Accumulated Depreciation—Equipment ….. 1,400,000

**($5,600,000 ÷ 4)

(c) No depreciation is recorded on impaired assets to be disposed of.

Recovery of impairment losses are recorded.

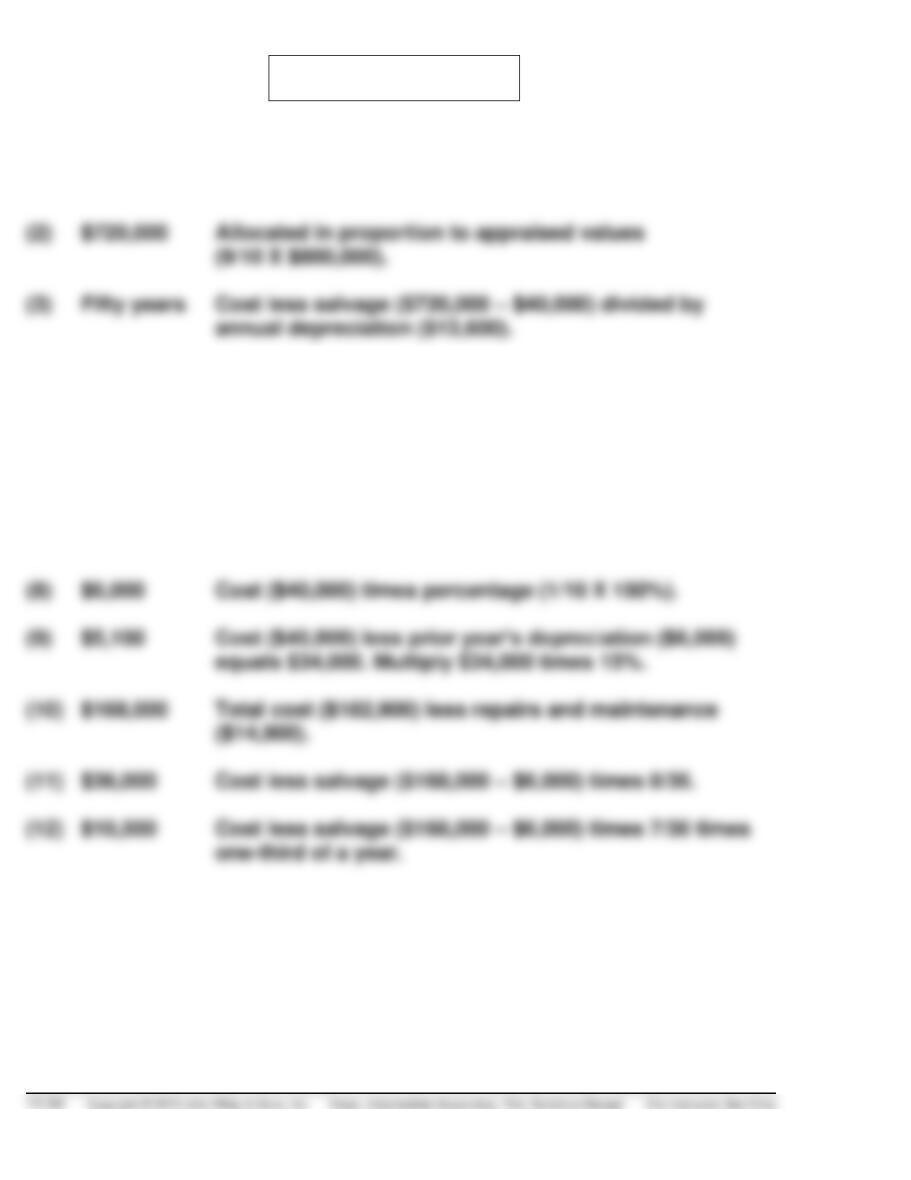

PROBLEM 11-10

(1)

$80,000

Allocated in proportion to appraised values

(1/10 X $800,000).

(2)

$720,000

Allocated in proportion to appraised values

(9/10 X $800,000).

(3)

Fifty years

annual depreciation ($13,600).

(4)

$13,600

Same as prior year since it is straight-line depreciation.

(5)

$91,000

[Number of shares (2,500) times fair value ($30)]

plus demolition cost of existing building ($16,000).

(6)

None

No depreciation before use.

(7)

$40,000

Fair value.

(8)

$6,000

Cost ($40,000) times percentage (1/10 X 150%).

(9)

$5,100

equals $34,000. Multiply $34,000 times 15%.

(10)

$168,000

Total cost ($182,900) less repairs and maintenance

($14,900).

(11)

$36,000

(12)

$10,500

one-third of a year.

PROBLEM 11-10 (Continued)

(13)

$52,000

obtain $46,260, and then add the $5,740 down payment.

Annual payment ($6,000) times present value of annuity

due at 8% for 11 years (7.710) plus down payment ($5,740).

This can be found in an annuity due table since the

(14)

$2,600

Cost ($52,000) divided by estimated life (20 years).

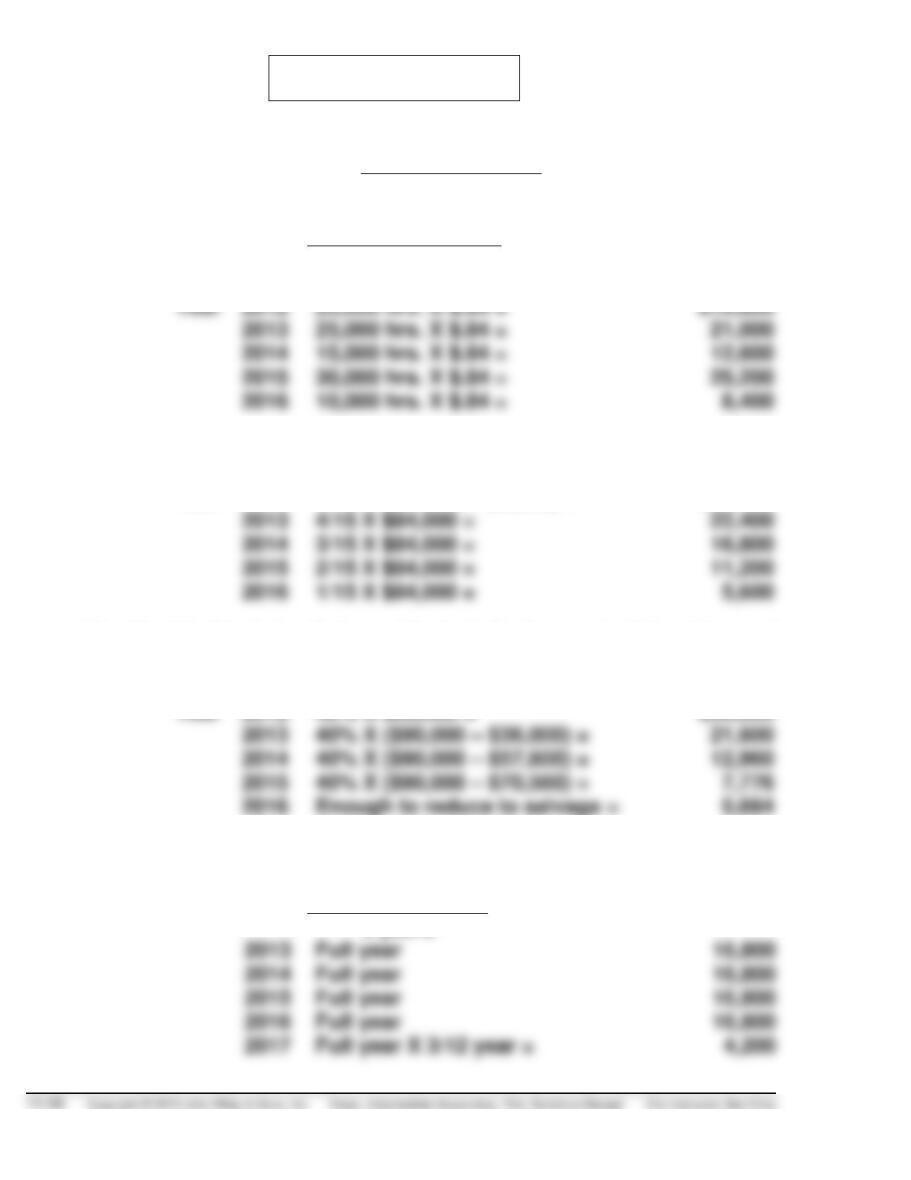

PROBLEM 11-11

(a)

(1)

Straight-line Method:

$90,000 – $6,000

= $16,800 a year

5 years

(2)

Activity Method:

$90,000 – $6,000

= $.84 per hour

100,000 hours

2014

15,000 hrs. X $.84 =

(3) Sum-of-the-Years’-Digits: 5 + 4 + 3 + 2 + 1 = 15

Year

2012

5/15 X ($90,000 – $6,000) =

$28,000

2015

2/15 X $84,000 =

(4) Double-Declining-Balance Method: Each year is 20% of its total

life. Double the rate to 40%.

Year

2012

40% X $90,000 =

2015

40% X ($90,000 – $70,560) =

(b) (1) Straight-line Method:

Year

2012

$90,000 – $6,000

X 9/12 =

$12,600

5 years

2015

Full year

PROBLEM 11-11 (Continued)

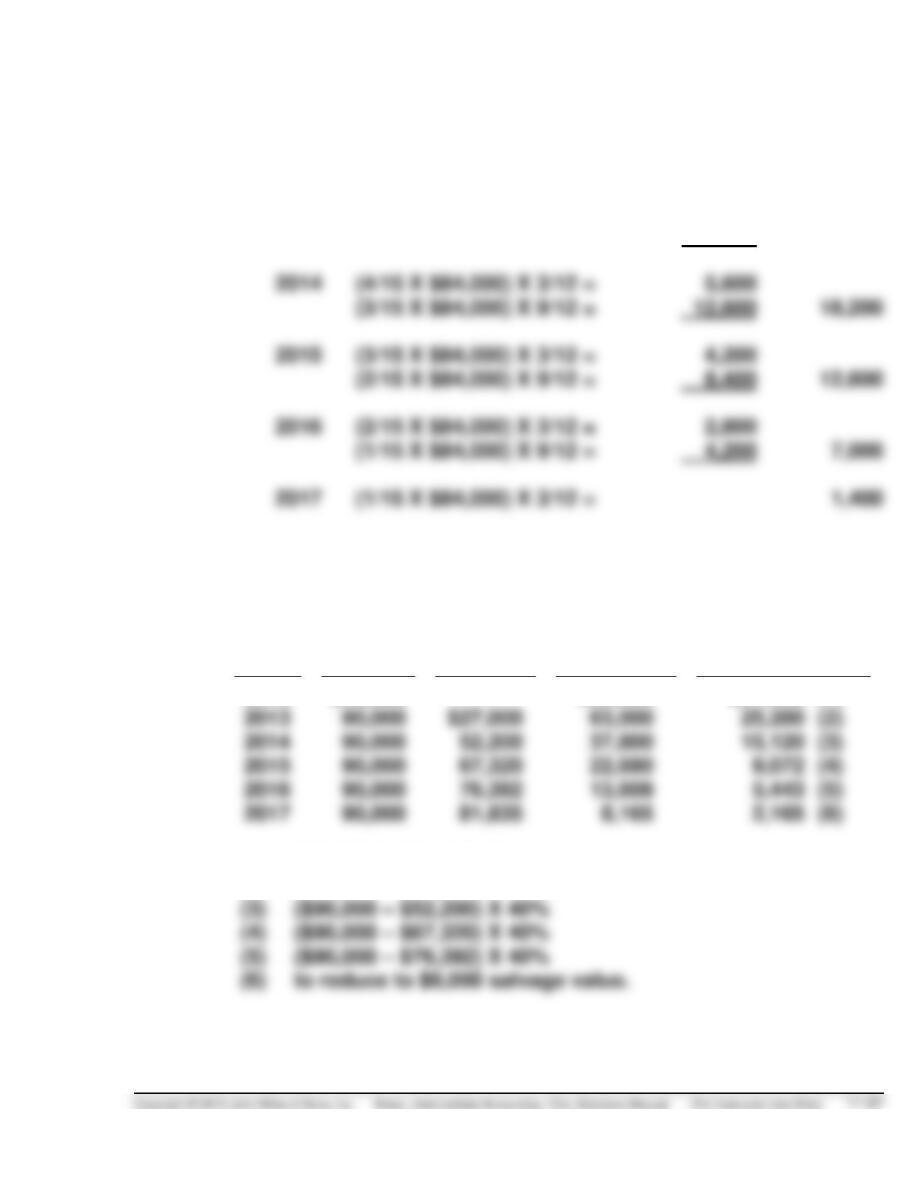

(2) Sum-of-the-Years’-Digits Method:

2012

(5/15 X $84,000) X 9/12 =

$21,000

2013

(5/15 X $84,000) X 3/12 =

$ 7,000

(4/15 X $84,000) X 9/12 =

16,800

23,800

2014

(4/15 X $84,000) X 3/12 =

(3/15 X $84,000) X 9/12 =

12,600

18,200

2015

(3/15 X $84,000) X 3/12 =

(2/15 X $84,000) X 9/12 =

12,600

2016

(2/15 X $84,000) X 3/12 =

(1/15 X $84,000) X 9/12 =

2017

(1/15 X $84,000) X 3/12 =

(3) Double-Declining Balance Method:

Year

Cost

Accum.

Depr. at

beg. of

year

Book

Value at

beg. of

year

Depr.

Expense

2012

$90,000

—

$90,000

$27,000 (1)

2013

25,200 (2)

2016

5,443 (5)

(1) $90,000 X 40% X 9/12

(2) ($90,000 – $27,000) X 40%

*PROBLEM 11-12

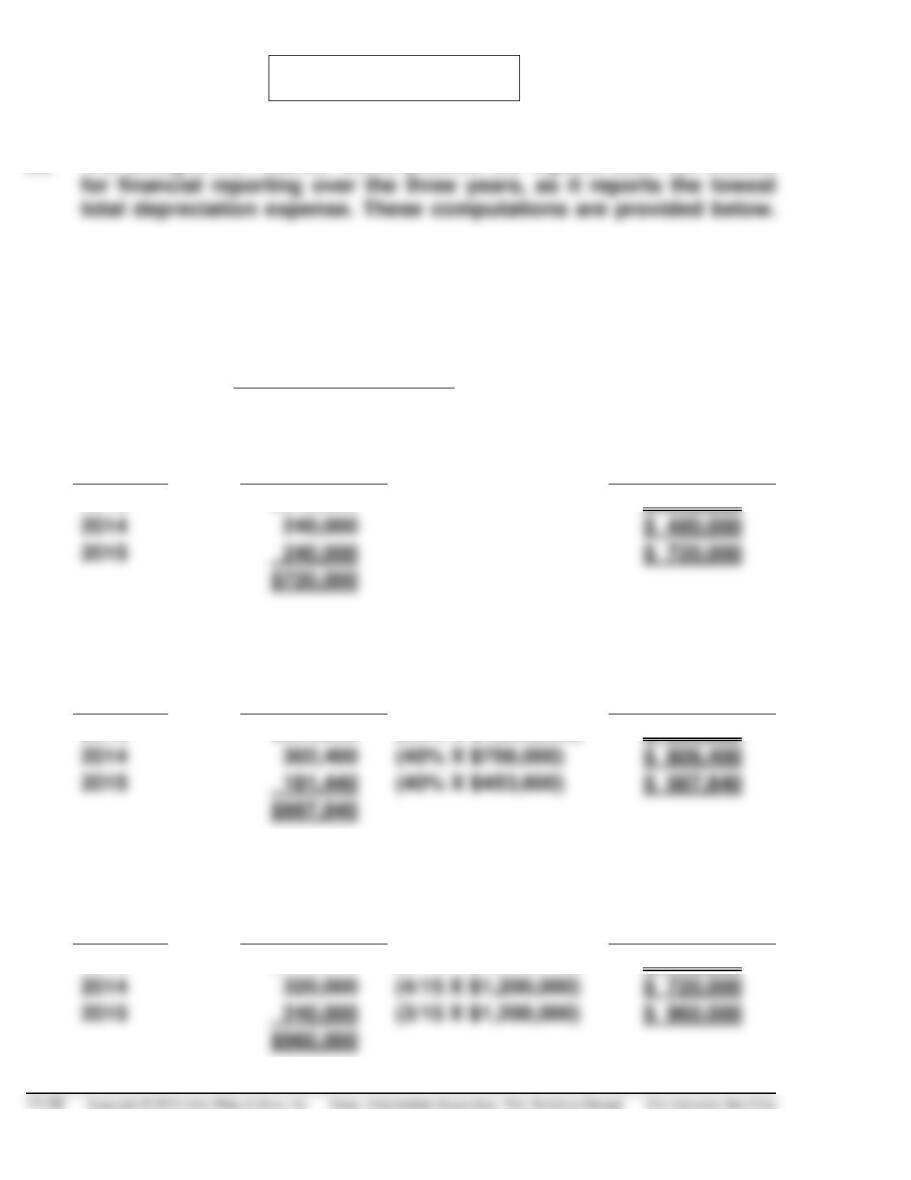

(a) The straight-line method would provide the highest total net income

Computations of depreciation expense and accumulated depreciation under

various assumptions:

(1) Straight-line:

$1,260,000 – $60,000

= $240,000

5 years

Year

Depreciation

Expense

Accumulated

Depreciation

2013

$240,000

$ 240,000

2014

$ 480,000

2015

$ 720,000

$720,000

(2) Double-declining-balance:

Year

Depreciation

Expense

Accumulated

Depreciation

2013

$504,000

(40% X $1,260,000)

$ 504,000

2014

(40% X $756,000)

$ 806,400

2015

(40% X $453,600)

$ 987,840

$987,840

(3) Sum-of-the-years’-digits:

Year

Depreciation

Expense

Accumulated

Depreciation

2013

$400,000

(5/15 X $1,200,000)

$ 400,000

2014

(4/15 X $1,200,000)

$ 720,000

2015

(3/15 X $1,200,000)

$ 960,000

*PROBLEM 11-12 (Continued)

(4) Units-of-output:

Year

Depreciation

Expense

Accumulated

Depreciation

2013

$288,000

($24* X 12,000)

$288,000

2015

($24 X 10,000)

$792,000

$792,000

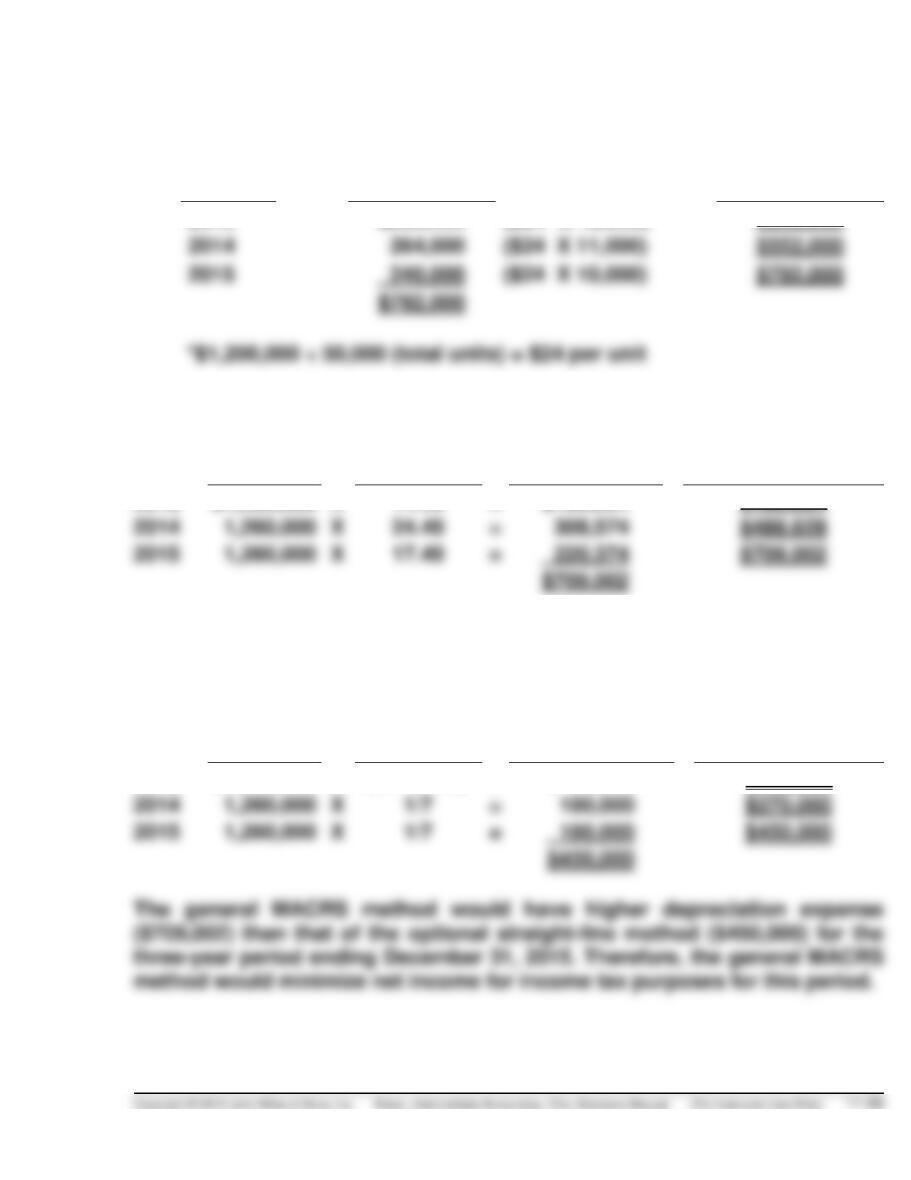

(b) General MACRS method:

Total Cost

MACRS

Rates (%)*

Annual

Depreciation

Accumulated

Depreciation

2013

$1,260,000

X

14.29

=

$180,054

$180,054

2014

X

=

2015

X

=

*Taken from the MACRS rates schedule.

Optional straight-line method:

Total Cost

Depreciation

Rate

Annual

Depreciation

Accumulated

Depreciation

2013

$1,260,000

X

(1/7 X 1/2)

=

$ 90,000

$ 90,000

2014

X

=

$270,000

2015

X

=

$450,000

TIME AND PURPOSE OF CONCEPTS FOR ANALYSIS

CA 11-1 (Time 25–35 minutes)

Purpose—to provide the student with an understanding of the basic objective of depreciation accounting.

In addition, the case involves a reverse sum-of-the-years’-digits situation and the student is to comment

CA 11-2 (Time 20–25 minutes)

Purpose—to provide the student with a basic understanding of the difference between the unit and

CA 11-3 (Time 25–35 minutes)

Purpose—to provide the student with an understanding of a number of unstructured situations involving

depreciation accounting. The first situation considers whether depreciation should be recorded during a

CA 11-4 (Time 25–35 minutes)

Purpose—to provide the student with an understanding of the objectives of depreciation and the

theoretical basis for accelerated depreciation methods.

CA 11-5 (Time 20–25 minutes)